SEVN - 'Tis The Season For Dividends

2023-12-10 09:00:00 ET

Summary

- U.S. equity markets advanced for a sixth-straight week after the major employment reports showed trends that were broadly consistent with a 'soft landing' for the U.S. economy.

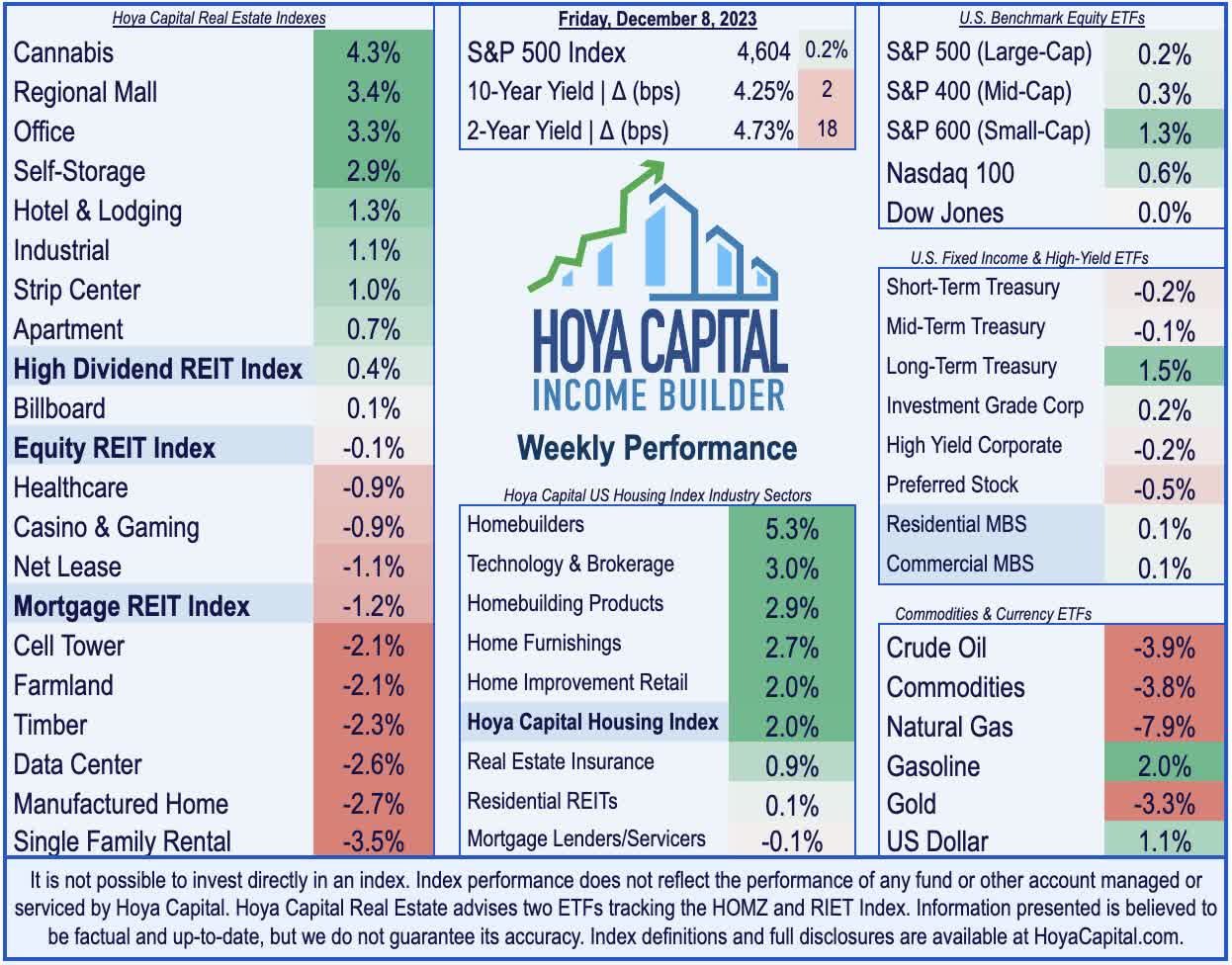

- Gaining for a sixth-straight week since dipping into "correction territory" at the end of October, the S&P 500 gained another 0.2% on the week, extending its six-week gains to 12%.

- Real estate equities - the top-performing equity sector during the rebound - were mixed this week as the lift in benchmark interest rates offset encouraging business updates and dividend news.

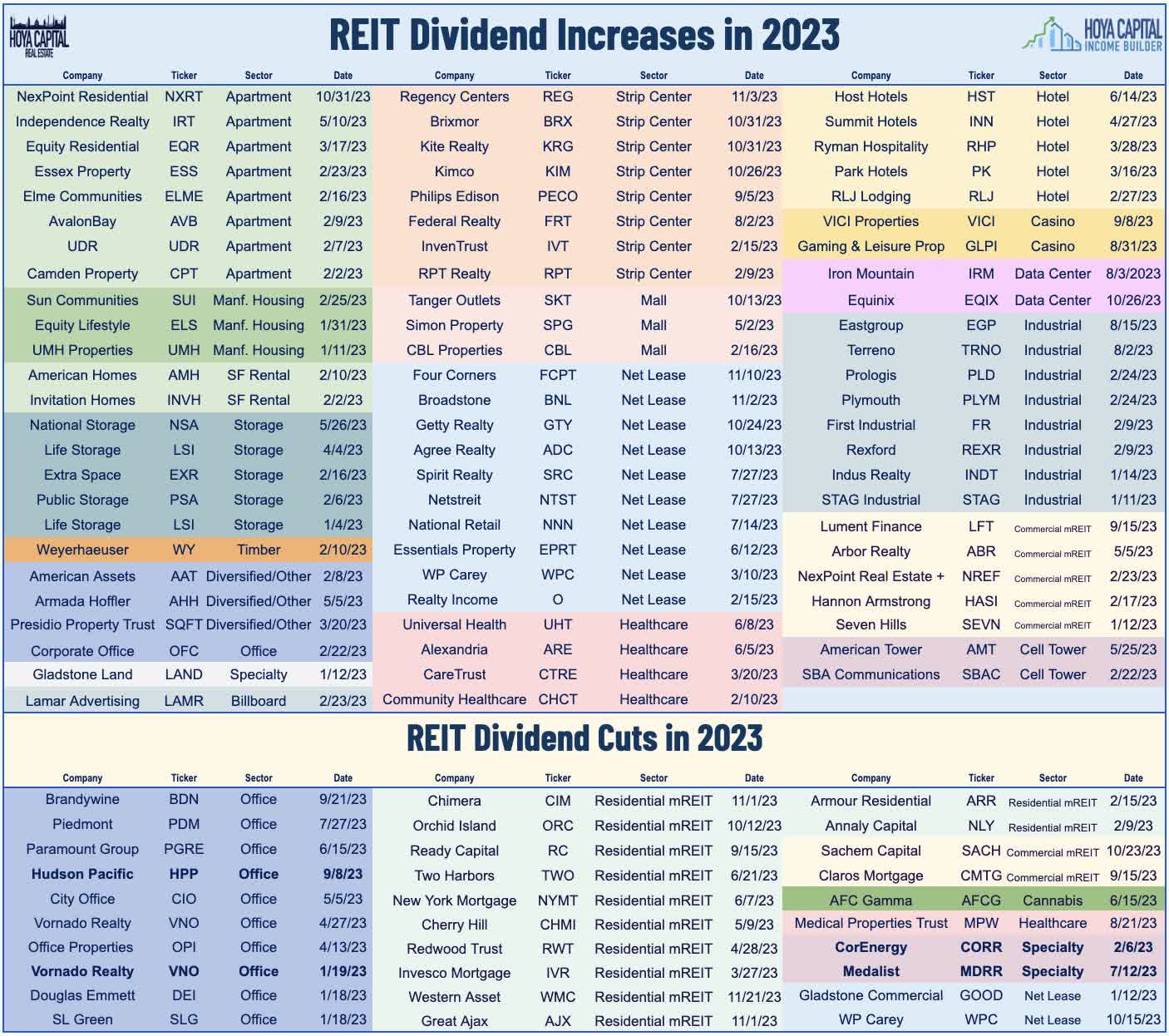

- 'Tis the season for dividends. Six REITs raised their dividends this week, raising the full-year total across the REIT sector to 76. Two REITs trimmed their dividend payouts, lifting the total to 30.

- Following a double-digit rally last week, office REITs were again among the leaders this week following business updates from Kilroy and SL Green showing a notable rebound in leasing activity.

Real Estate Weekly Outlook

U.S. equity markets advanced for a sixth-straight week after the major employment reports showed trends that were consistent with an economic 'soft landing,' while a sustained decline in commodities prices emboldened calls that the Federal Reserve will begin cutting interest rates by mid-2024. With the FOMC's policy meeting looming in the week ahead, economic data showed a continued trend towards pre-pandemic "normalization" - but also left the door slightly ajar for Fed officials to push back on recent market optimism.

{kind=link}

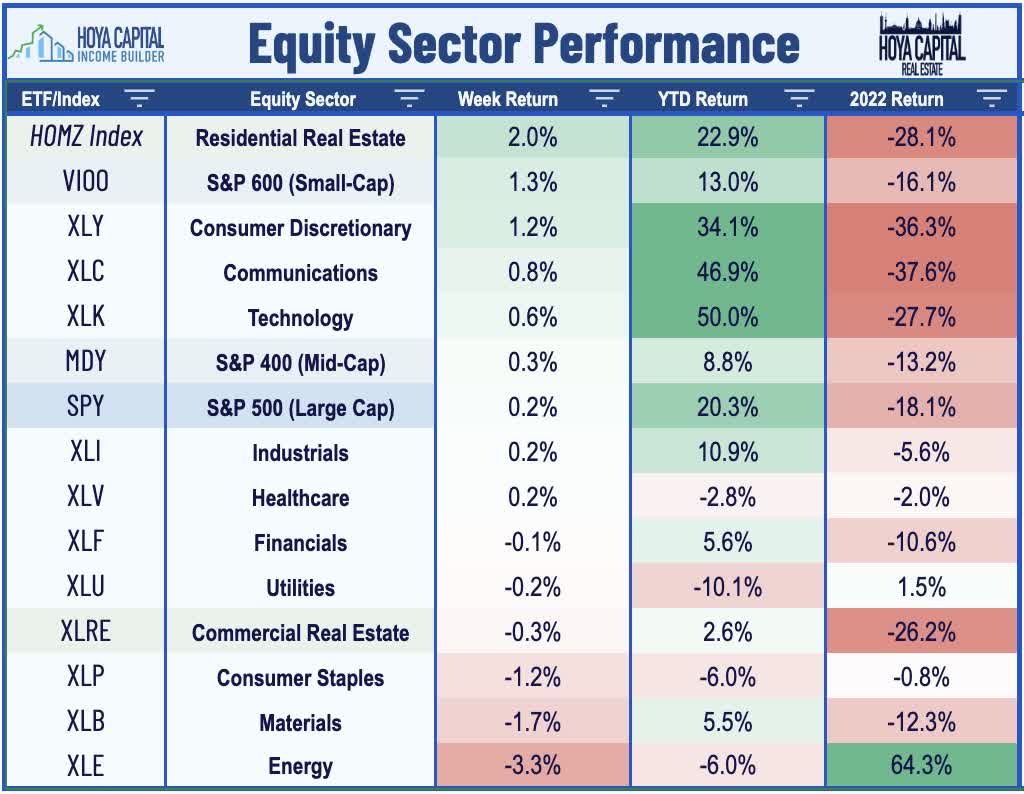

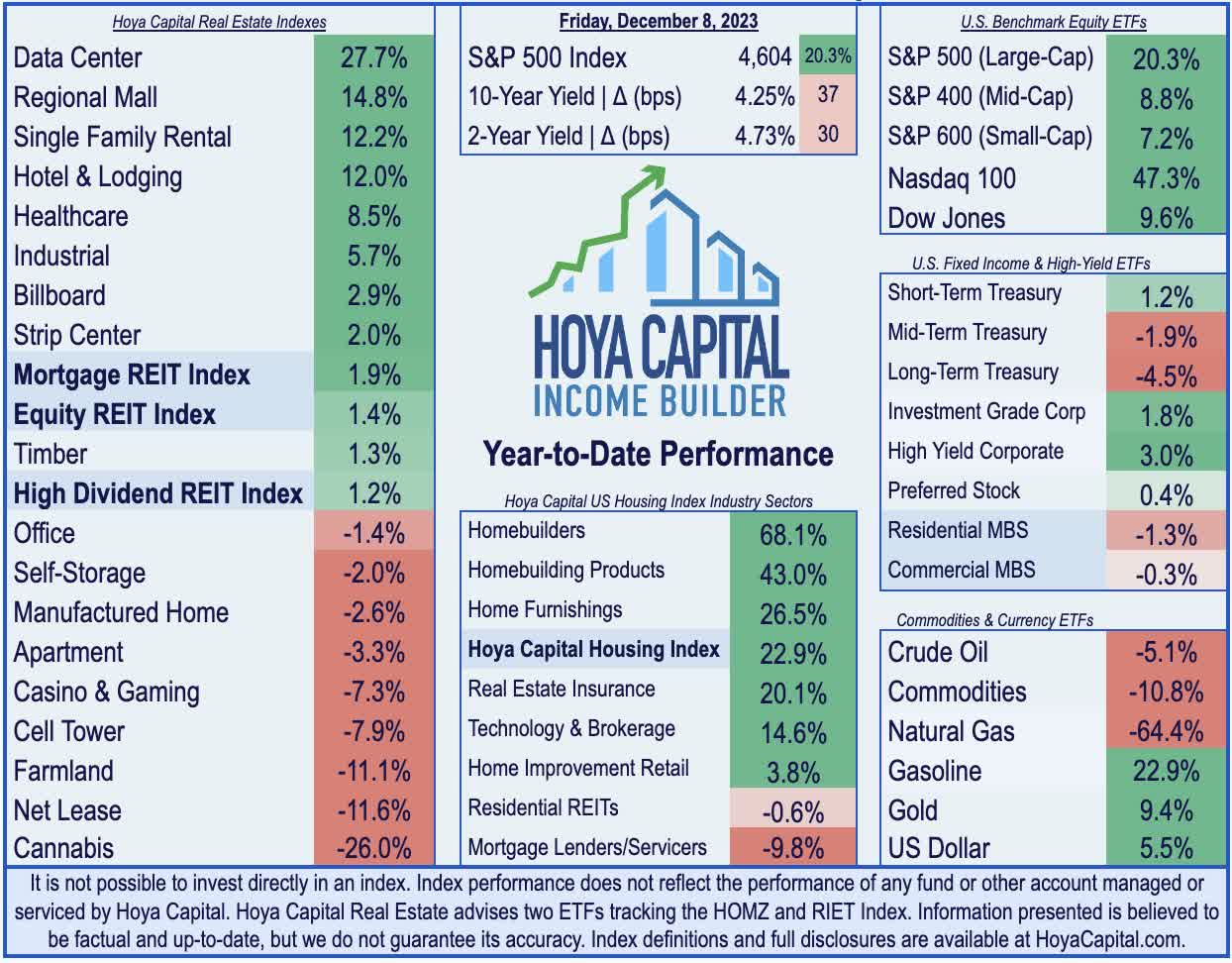

Gaining for a sixth-straight week since dipping into "correction territory" at the end of October, the S&P 500 gained another 0.2% on the week, extending its six-week gains to over 12%. The tech-heavy Nasdaq 100 advanced 0.6% this week to lift its year-to-date gains to nearly 50%. After lagging for most of the year, small-caps and mid-caps continued to close their historically wide underperformance gap this week, with the Small-Cap 600 posting gains of 1.3% - the strongest among the major equity benchmarks. Real estate equities - which have been the top-performing GICS equity sector during this six-week rebound - were mixed this week as the lift in benchmark interest rates offset several encouraging business updates and dividend hikes. The Equity REIT Index finished lower by 0.1% this week, with 10-of-18 property sectors in positive territory, while the Mortgage REIT Index slipped 1.2%. Homebuilders rallied more than 5%, however, on strong earnings from luxury builder Toll Brothers alongside a continued retreat in mortgage rates.

{kind=link}

Benchmark interest rates trended lower for much of the week but rebounded rather sharply on Friday following the stronger-than-expected nonfarm payrolls report. Briefly dipping below 4.10% mid-week on the heels of soft JOLTs and ADP data, the 10-Year Treasury Yield ultimately closed the week at 4.25% - up two basis points from last week - while the policy-sensitive 2-Year Treasury Yield jumped by 18 basis points to 4.73%. Swaps market now imply a 45% probability that the Federal Reserve will cut rates for the first time in March - down from roughly 65% last week. Fueling further optimism over disinflation, WTI Crude Oil prices dipped another 4% this week on data showing that inventories have swelled from the combination of softer demand and a revival in U.S. production to fresh all-time highs, offsetting cuts from OPEC counterparts. Oil prices are now more than 25% below their recent highs in late September, while consumer gasoline prices posted an 11th-straight week of declines to levels that are nearly 20% below late-summer peaks. Six of the eleven GICS equity sectors finished lower on the week, with Energy ( XLE ) stocks continuing to lag on the downside.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

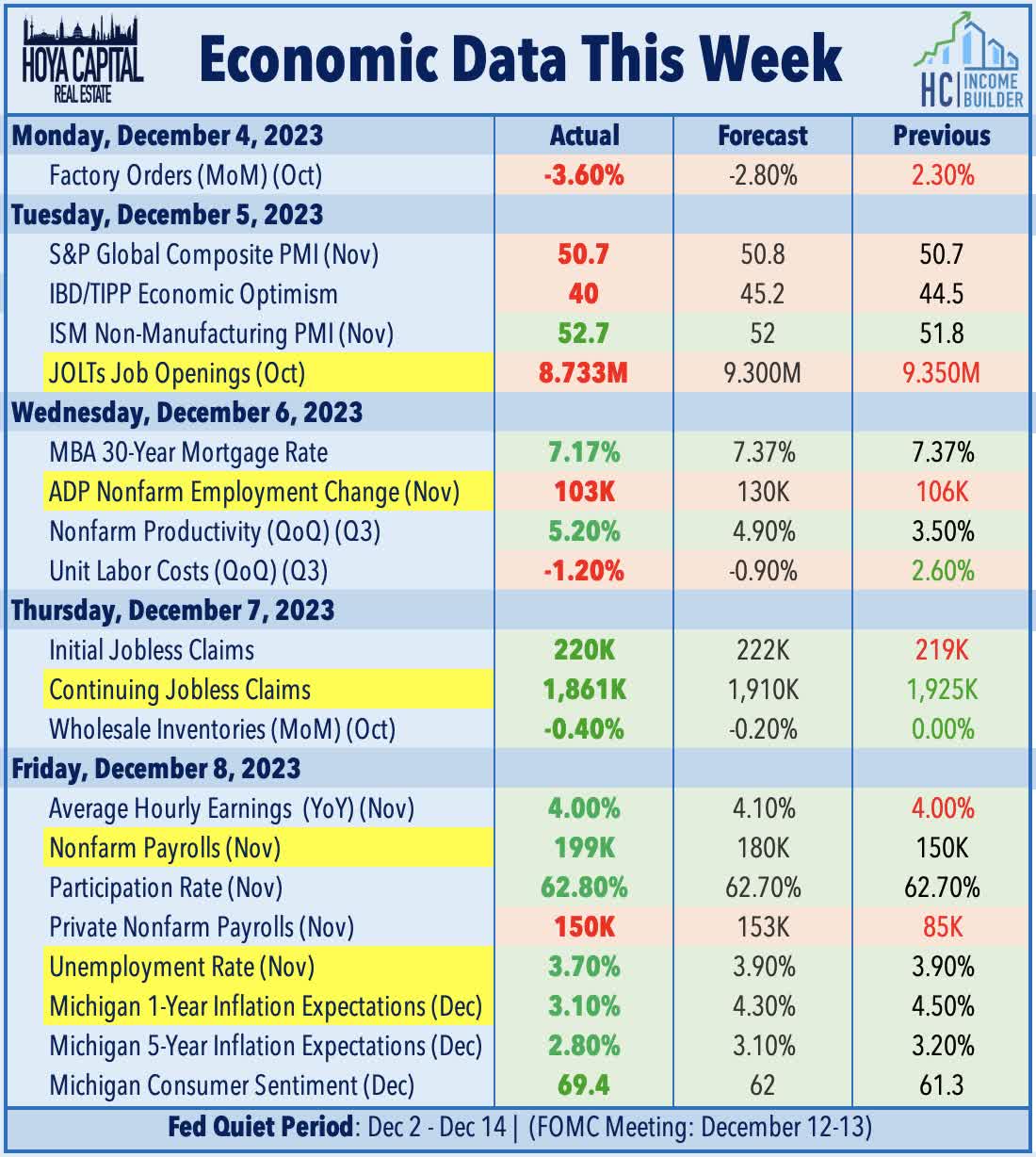

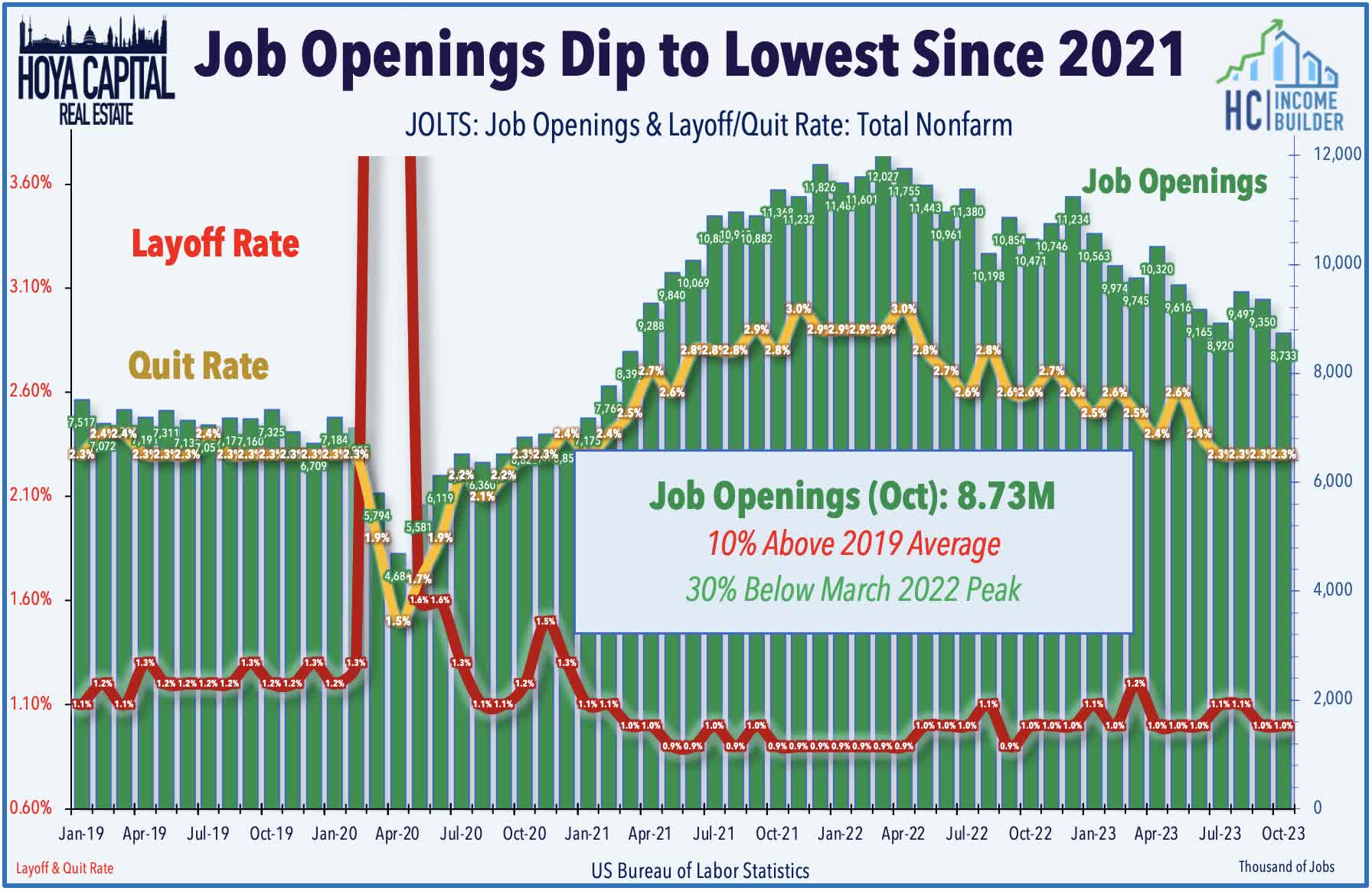

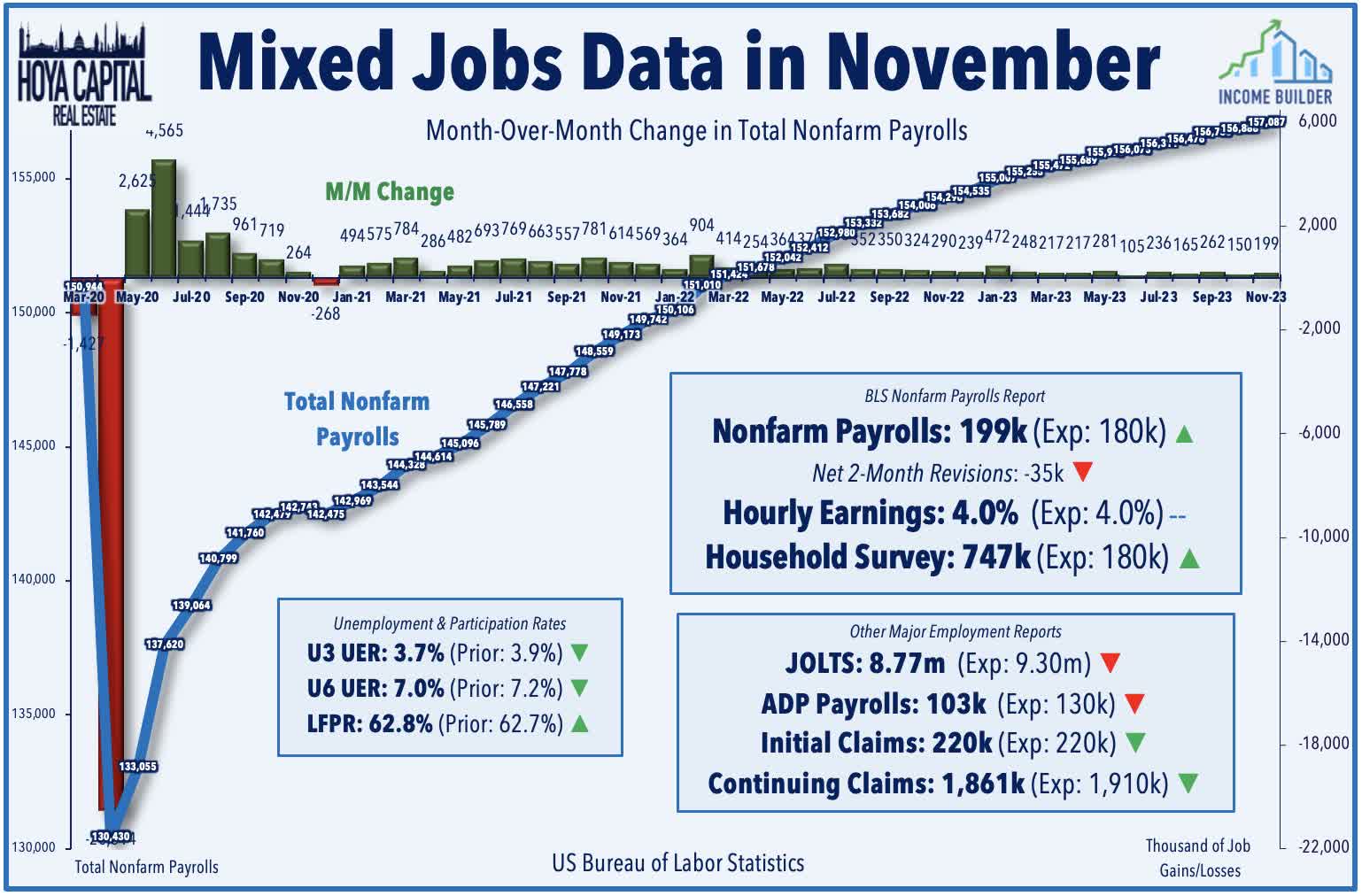

The long-awaited cooldown in labor markets - which most Fed officials have pinned their "pivot" upon - appears to finally be upon us, according to the busy slate of employment data this week. The Labor Department's Job Openings and Labor Turnover Survey ("JOLTS") showed that job openings in October dipped to the lowest level since March 2021 at 8.73 million - the lowest since the "reopening" of the US economy in early 2021 - and down roughly 30% from the peak of the labor market shortages seen in early 2022. The figure was well below consensus estimates, and the prior month was revised lower as well. The ratio of vacancies for every unemployed worker fell to 1.3, returning much closer to the pre-pandemic high of 1.2. The report showed that while we haven't yet seen a major uptick in corporate layoffs, employees are far more hesitant to voluntarily quit their jobs than seen earlier in the pandemic. ADP data showed similar trends of slowing job creation in November, with wages posting their smallest growth in more than two years. Private payrolls grew by just 103k in November - below consensus estimates of around 125k - and below the downwardly revised 106k in October.

{kind=link}

The BLS' nonfarm payrolls report later in the week painted a more positive picture, however, showing that the U.S. economy added 199k jobs in November - above consensus estimates of 180k - while the unemployment rate unexpectedly improved to a four-month low of 3.7% resulting from a sizable jump in the labor force and uptick in the participation rate. The report wasn't quite as strong as it appeared on the surface, however, as net revisions subtracted 35k from the prior two months - the tenth downward revision in the past eleven reports - while government hiring was largely responsible for the "beat" on the headline figure, as private payroll gains of 150k were slightly below estimates of 155k. Resolutions of labor union strikes in the auto and entertainment sector also resulted in some one-time gains during the month, offsetting a notable 38k decline in retail employment and a 5k decline in transportation and warehousing. Hiring in healthcare and hospitality was notably strong in the BLS report, adding 77k and 40k jobs, respectively.

{kind=link}

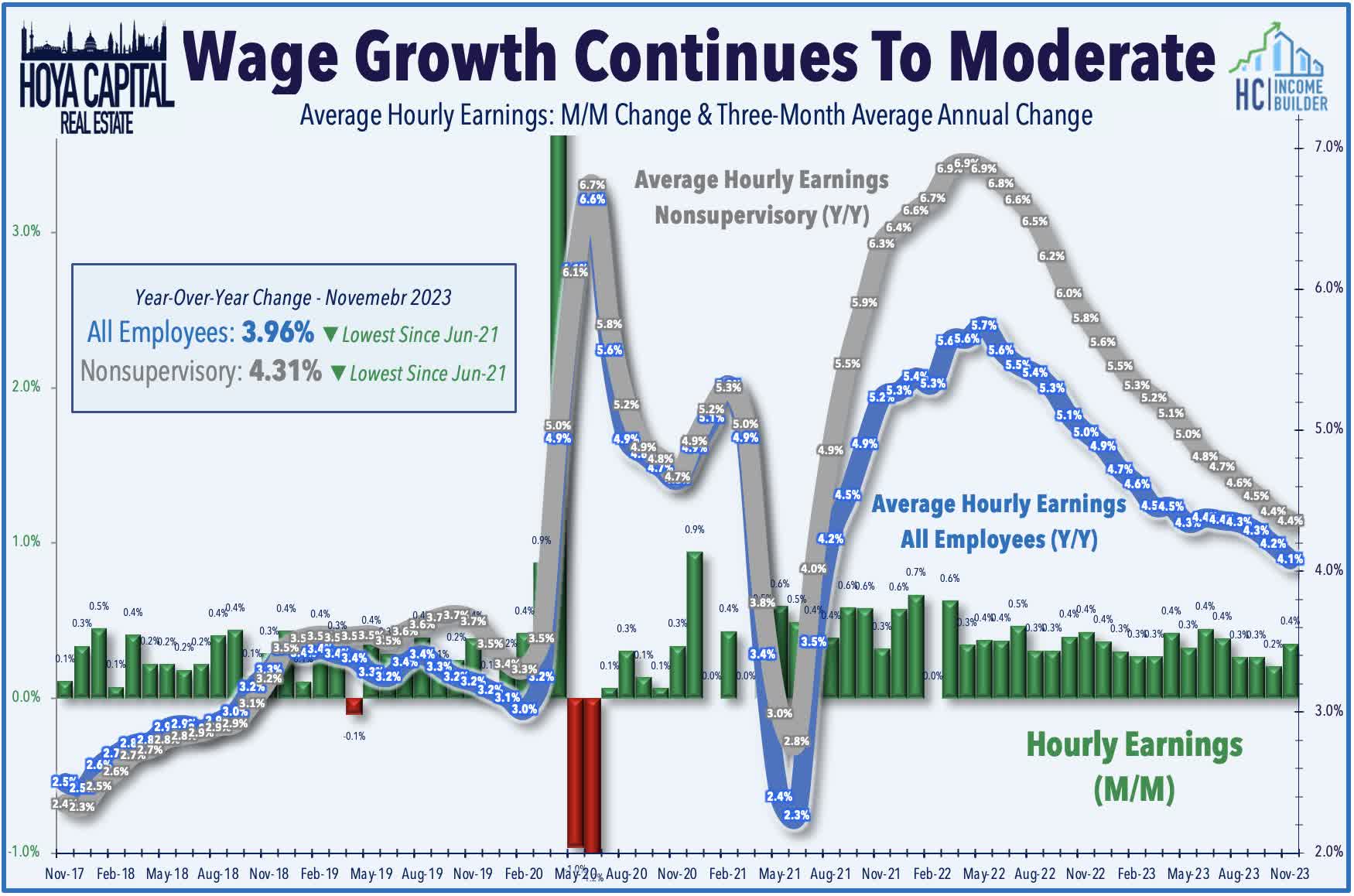

Average hourly earnings ("AHE") - a key inflation indicator - provided additional evidence of normalizing labor market conditions following pandemic-era shortages. AHE for all employees moderated to a 4.0% year-over-year increase in November - the softest since June 2021 - and moderated to 4.3% for nonsupervisory workers, down sharply from the peak of around 7% in early 2022. Since the start of 2023, AHE for all employees has averaged 3.9% on an annualized basis - slightly above the 3.3% increase in 2019 in a year when CPI inflation averaged just 1.8%. ADP also reported that its measure of annual pay posted its smallest annual gain since September 2021 at 5.6%. Job changers saw wage increases of 8.3% - the smallest premium for switching positions since ADP began tracking the data three years ago.

{kind=link}

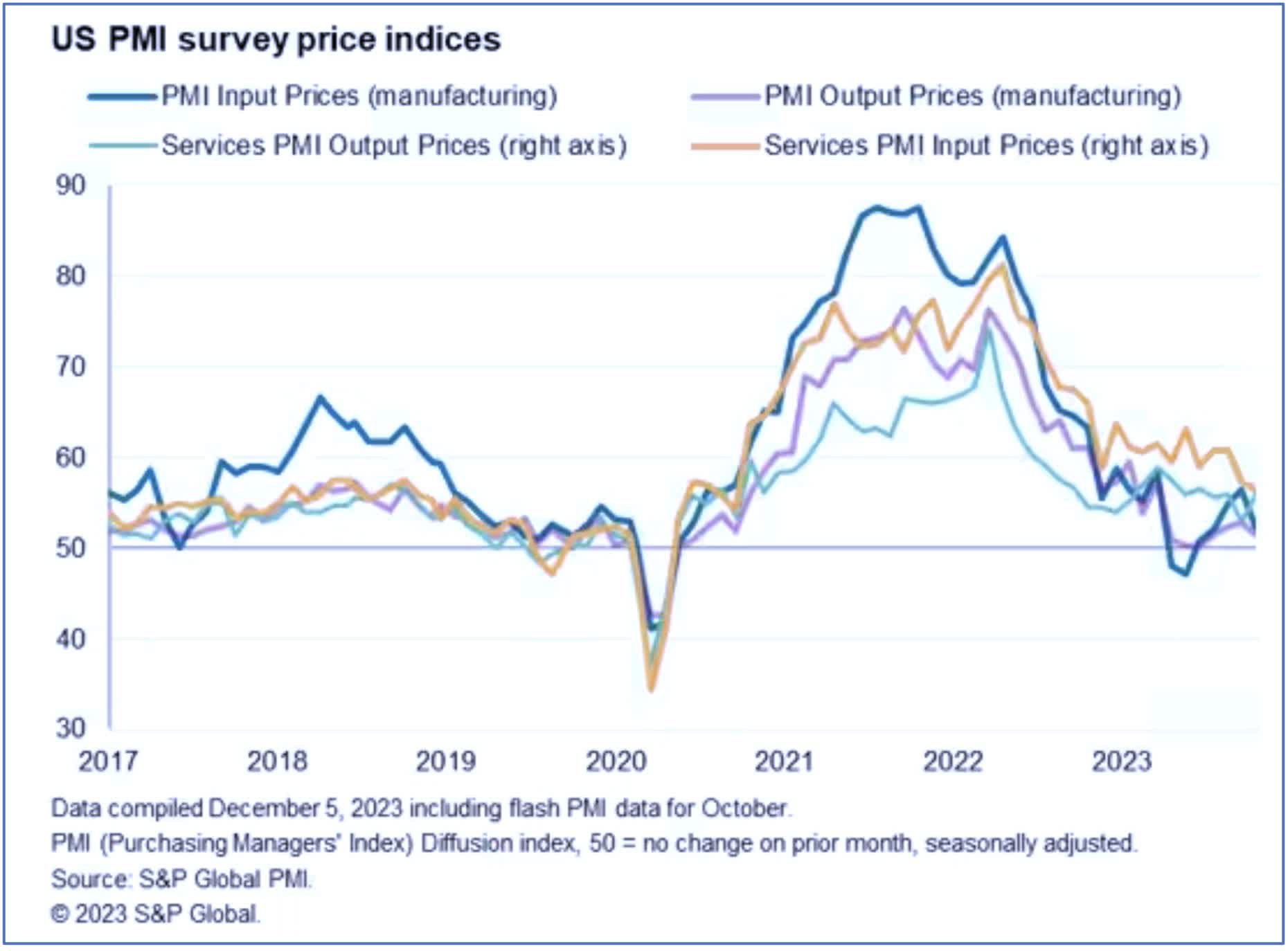

The latest PMI data released by S&P Global and ISM this week also pointed to a further cooling of pandemic-era inflation pressures. S&P's report noted that its November survey indicated "only modest economic growth and near-stagnant employment, with the risk of the expansion losing further momentum as we head towards 2024... while businesses continued to report further output gains in November, growth remains considerably weaker than seen earlier in the year, and forward-looking indicators point to growth slowing in the months ahead." S&P's Service PMI showed that the pace of input price inflation dropped to the slowest in over three years, while its Manufacturing PMI report showed that input price inflation eased to the slowest since August and was well below the historic trend rate. S&P noted, "firms have become increasingly concerned about excessive staffing levels in the face of weakened demand, resulting in the smallest jobs gain recorded by the survey since the early pandemic lockdowns of 2020. The cooling jobs market has been accompanied by lower wage growth which, combined with recent oil price falls, helped pull business cost growth down to its lowest for three years."

{kind=link}

Equity REIT Week In Review

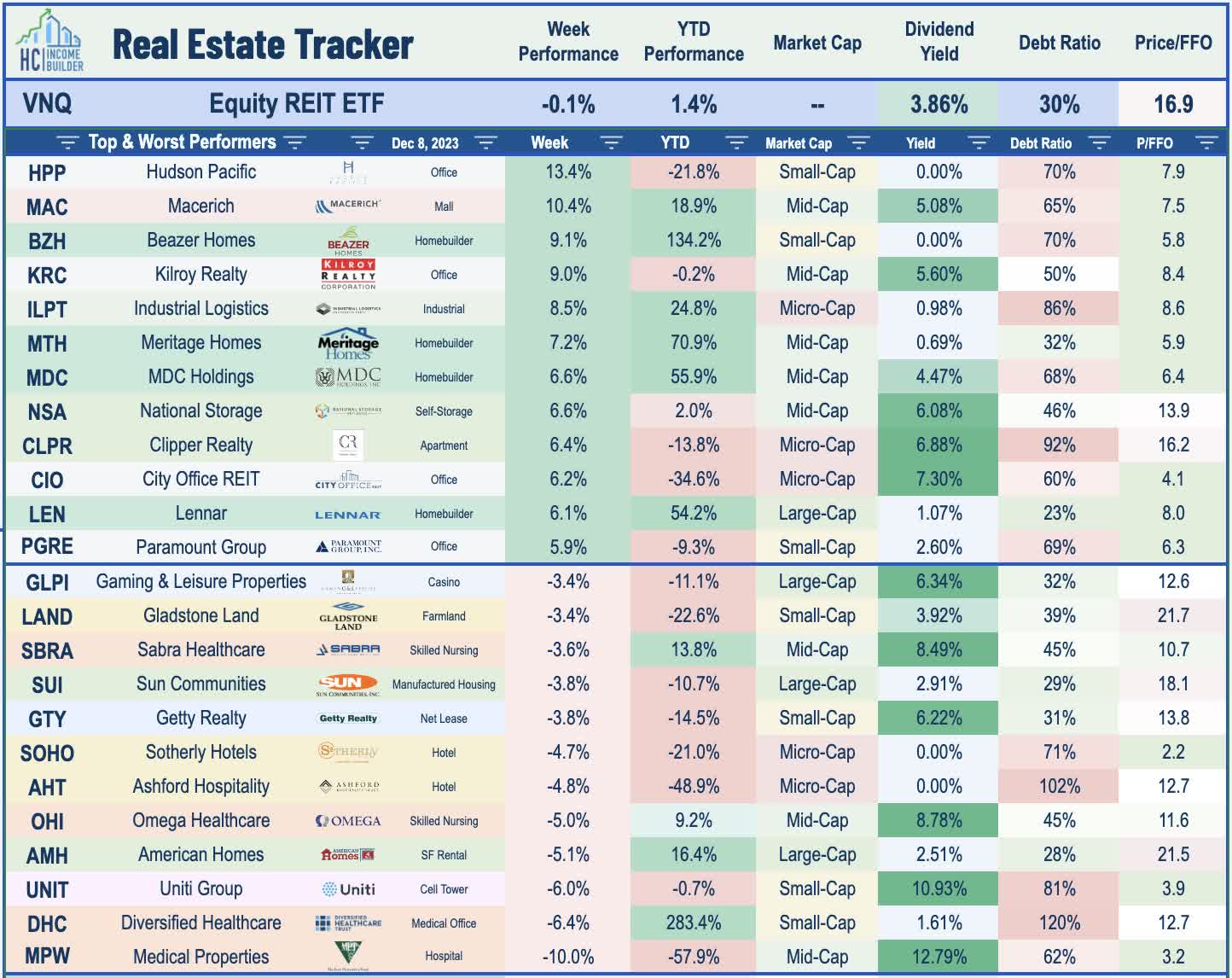

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Another week, another wave of REIT dividend hikes. Self-storage REIT CubeSmart ( CUBE ) rallied 3% this week after it hiked its quarterly dividend by 4% to $0.51/share (4.9% dividend yield). CUBE had been the only storage REIT that hadn't yet raised its dividend this year. Ryman Hospitality ( RHP ) gained 2% this week after it hiked its quarterly dividend by 10% to $1.10/share (4.3% dividend yield) - the fifth hotel REIT to raise its dividend. Sunstone Hotel ( SHO ) gained 1% after it declared a supplemental dividend of $0.06/share in addition to its regular quarterly dividend of $0.07/share (2.8% dividend yield). Essential Properties ( EPRT ) was little changed after hiking its quarterly dividend for the second time this year to $0.285/share (4.6% dividend yield), up 4% from a year earlier. Single-family rental REIT Invitation Homes ( INVH ) slipped 3% despite hiking its quarterly dividend by 8% to $0.28/share (3.4% dividend yield). Universal Health Realty ( UHT ) gained 1% after it hiked its quarterly dividend for the second time this year, increasing its payout by 1% to $0.725/share (6.9% dividend yield). Lab space operator Alexandria Real Estate ( ARE ) gained 1% after it hiked its dividend for the second time this year, raising its quarterly payout by 2.4% to $1.27/share (4.3% dividend yield), which is 5% higher than last year. In our State of the REIT Nation report last week, we noted that 75 REITs have raised their dividends this year, while 30 REITs have lowered their payouts.

{kind=link}

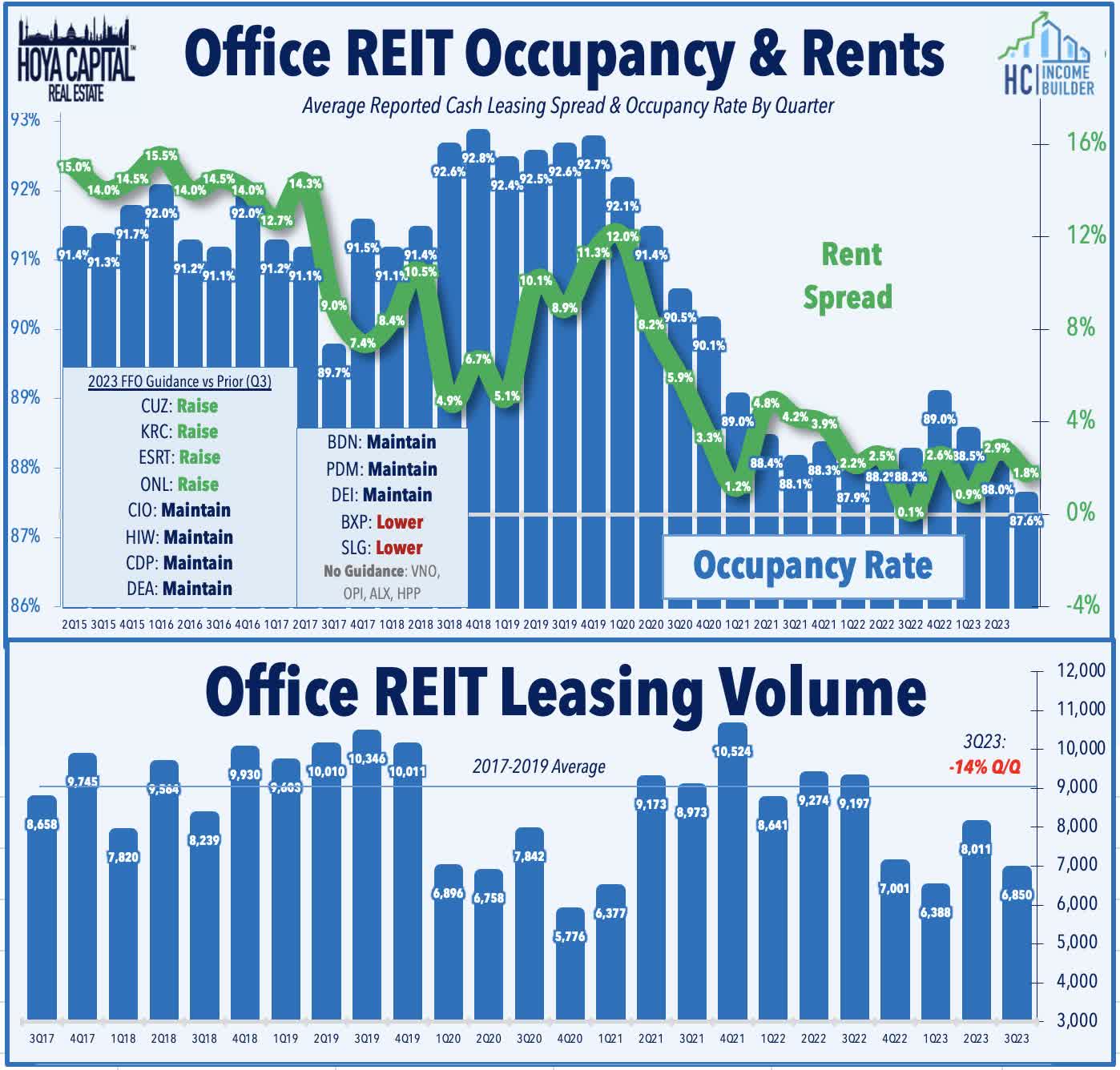

Office : Following a double-digit sector-wide rally last week, office REITs were again among the leaders this week following business updates showing a rebound in leasing activity. West Coast-focused Kilroy Realty ( KRC ) rallied 9% this week after reporting strong leasing activity so far in Q4, signing 520K square feet ("SF") of new and renewing leases, its best quarter of volume since 2019 and significantly above this year's quarterly average of 250k. KRC noted that year-to-date, rents are approximately flat on a cash basis and up 15% on a GAAP basis over the prior leases. NYC-focused office REIT SL Green ( SLG ) rallied after making several announcements, including a deal to sell 625 Madison Avenue for $632.5M ($1,123/sf), and plans to use the proceeds to repay corporate debt. The company also announced a pair of large lease signings, including a 270k SF lease covering six floors at 280 Park Avenue and a 77k SF 15-year lease for two floors at 245 Park Avenue, and SLG reaffirmed its 2023 FFO guidance - down 24% from last year - and expects its 2024 FFO to be roughly flat at the midpoint of its initial range while expecting same-store NOI growth between -1% to -2%. SLG also announced an 8% reduction to its monthly dividend to $0.25/share (7.5% dividend yield). In our Earnings Recap , we noted that overall office leasing activity was down about 15% from the prior quarter in Q3 and roughly 25% below the pre-pandemic average from 2017-2019, while cash leasing spreads were essentially flat.

{kind=link}

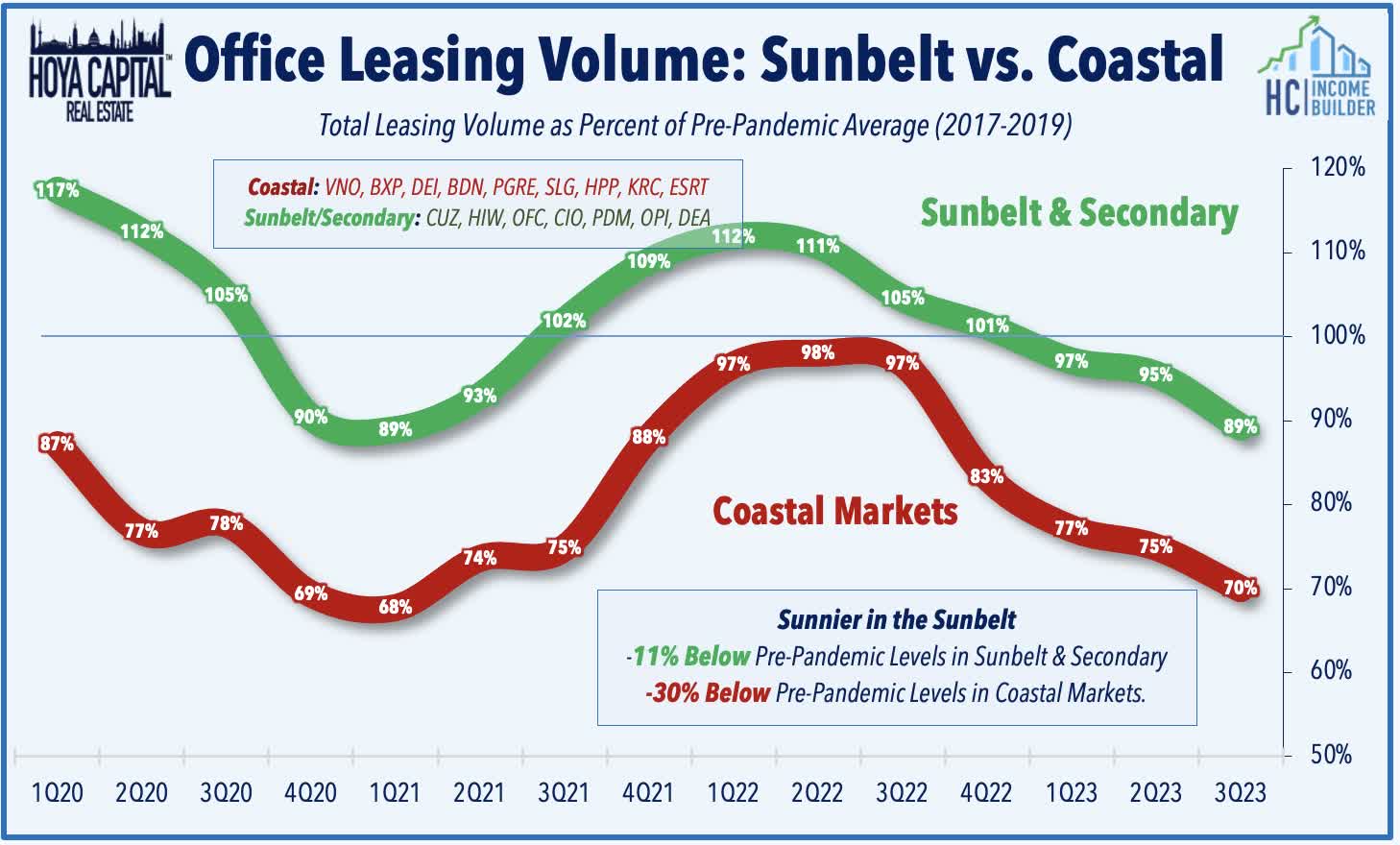

Of note, sunbelt and secondary-focused office REITs reported activity that was only about 10% below pre-pandemic levels, however, while Coastal-focused REITs reported a 30% dip. Sticking in the office sector, West Coast-focused Hudson Pacific ( HPP ) surged 13% after announcing that it generated $189M of proceeds through the sale of a land parcel in Silicon Valley for $44M and through the sale of certain tranches of a loan secured by its Hollywood Media Portfolio for $146M. Elsewhere, Vornado Realty ( VNO ) - which suspended its dividend in April - gained 5% this week after it announced that it would pay a fourth dividend of $0.30/share. VNO indicated in April and in subsequent earnings call commentary that a fourth-quarter dividend would be necessary to meet its minimum distribution requirements as a REIT, noting that cash retained from dividends or from asset sales will be used to reduce debt and/or fund share repurchases. Importantly, Vornado noted that it anticipates that its common share dividend policy for 2024 will be to pay one common share dividend in the fourth quarter of 2024.

{kind=link}

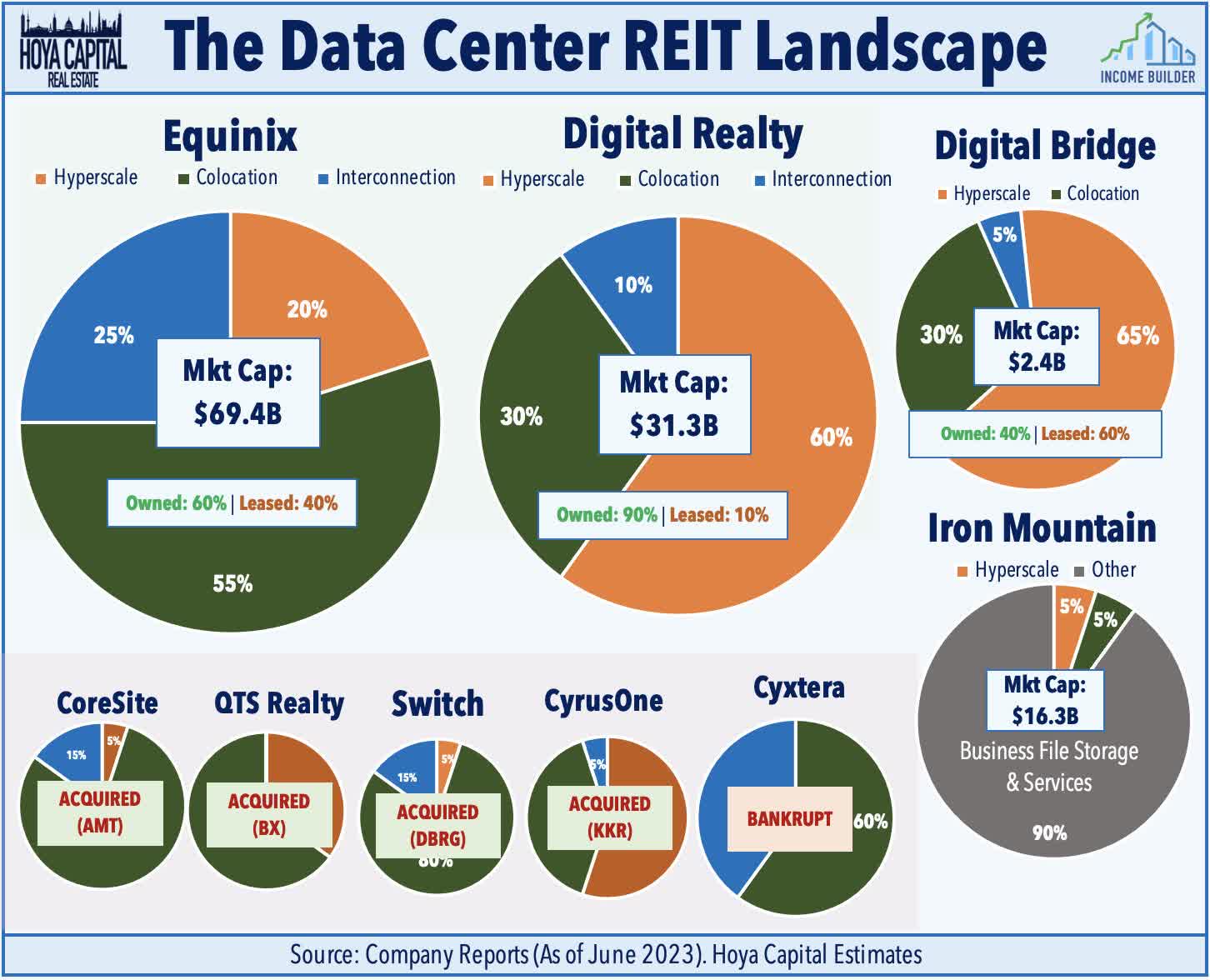

Data Center : Digital Realty ( DLR ) slipped 3% this week despite announcing a $7 billion joint venture deal with Blackstone ( BX ) to develop ten data centers across three metro areas - Frankfurt, Paris, and Virginia. Blackstone - through its Opportunities Fund - will make the initial capital contribution of $700M and get an 80% stake in the JV, while Digital Realty will own the remaining 20%, with both partners funding their pro rata share of the remaining development costs. A fifth of the total potential capacity is expected to be delivered through 2025, with the balance in 2026 or later. DLR will manage the development and day-to-day operations, for which it will receive fees. DLR noted that the deal marks "the culmination of a record year of capital recycling and aptly reflects the shift in our funding strategy to diversify our sources of capital and bolster our balance sheet." The deal follows a pair of similar JVs announced over the past several months: a $200M JV with Realty Income ( O ) to develop two data centers in Virginia, and a JV with TPG Real Estate in which DLR sold an 80% share in three existing data centers. Relative to its peer Equinix ( EQIX ), DLR's more "capital heavy" strategy in which it has full ownership in nearly all of its data center properties had been viewed as a sub-optimal structure. Data Center REITs have been the top-performing property sector this year despite their relatively high use of variable rate debt, benefiting from AI-driven demand and a positive inflection in pricing power.

{kind=link}

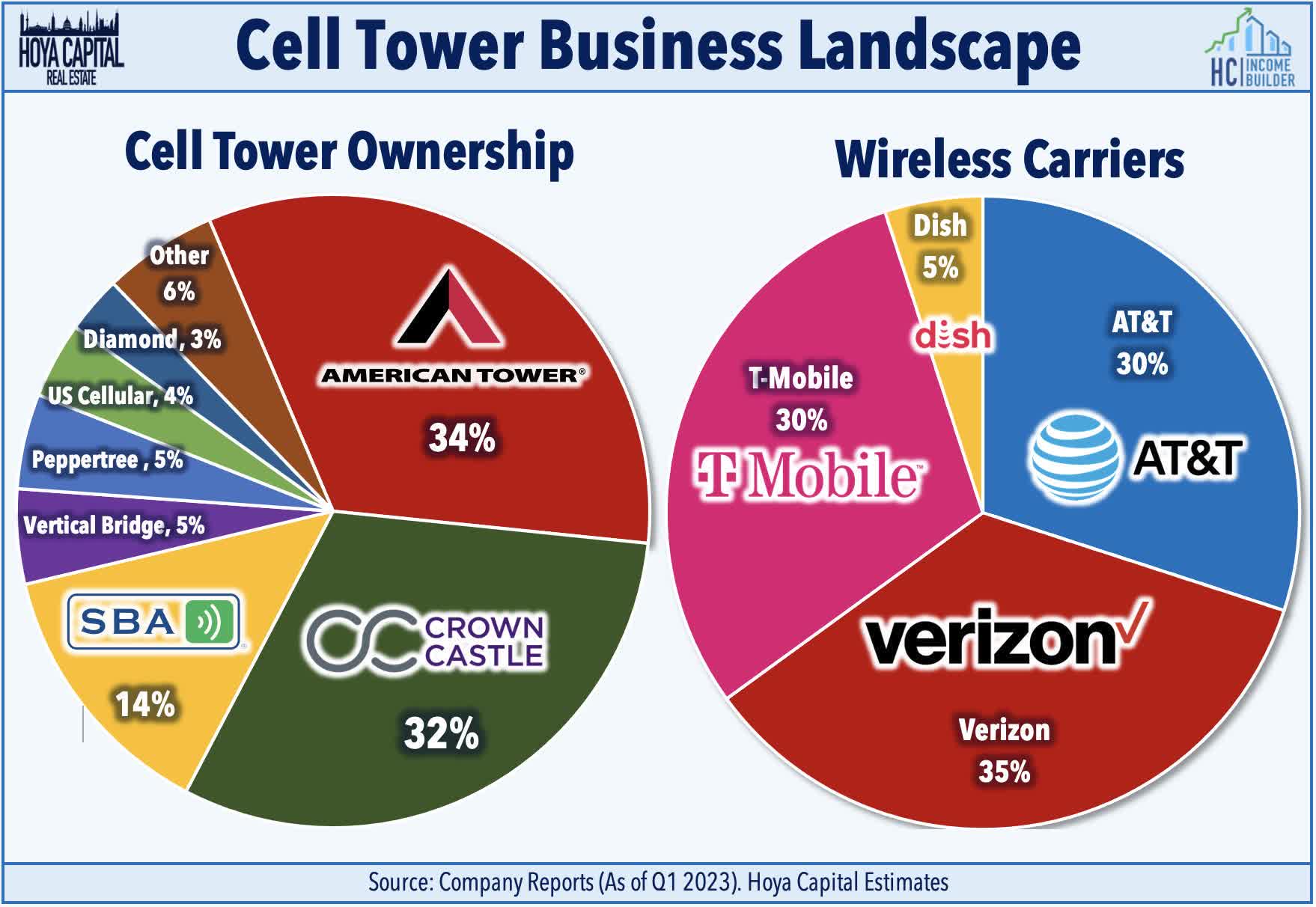

Cell Tower : Sticking in the technology space, Crown Castle ( CCI ) finished lower by about 2% this week after it announced that its CEO Jay Brown will retire next month - an unexpected departure that comes as activist investor Elliott Investment has doubled down on efforts to enact leadership changes at the REIT. CCI appointed Anthony Melone, a member of its Board, to begin serving as interim CEO at that time, during which time the Board will conduct a search process to identify a permanent CEO. Earlier in the week, Elliott published another letter summarizing the feedback received since publicly sharing its views on CCI, concluding that "it is even clearer to us today based on the feedback we have received that Crown Castle requires CEO change and a robust review of the Fiber business." The prior week, Elliott announced a $2B stake in CCI after its initial campaign in 2020 was "disregarded... and its recommended changes were neither made nor taken seriously." The investment firm - which had previously disclosed a $1B stake in 2020 - published a new letter calling for board and executive changes and a "re-evaluation" of its strategy around its fiber business, which Elliott blames for its underperformance relative to its cell tower REIT peers, American Tower ( AMT ) and SBA Communications ( SBAC ). Unlike its peers, Crown Castle has opted to focus exclusively on the United States market, making a play on 4G and 5G network densification through small-cells and fiber networks.

{kind=link}

Apartment : Relevant to the inflation discussion above, RealPage published its monthly Apartment Report this week, which noted that effective asking rents were essentially flat on a year-over-year basis in November, continuing a trend of moderation from the record-setting double-digit increases seen at the peak in early 2022. Of note, however, rent growth inched up 0.2% year-over-year nationally in November, a slight acceleration from the 0.1% annual increase in October, which snapped a streak of 20 straight months of rent deceleration. Last week, Apartment List reported that rent growth was -1.1% lower year-over-year in December, which was the fifth-straight month of negative rent growth but slightly above the bottom of -1.5% in October. Data from Realtor.com reported similar trends in its latest report, showing that annual rent growth was down -0.5% last month - the sixth month of negative growth - but also above the bottom in August. Zillow data - which includes single-family rentals as well - shows slightly more buoyant trends, with rent growth of 3.5% in October. CoreLogic data shows that single-family rent growth has trended 200-400 basis points higher than apartment rent growth during this moderation, consistent with reports from public REITs.

{kind=link}

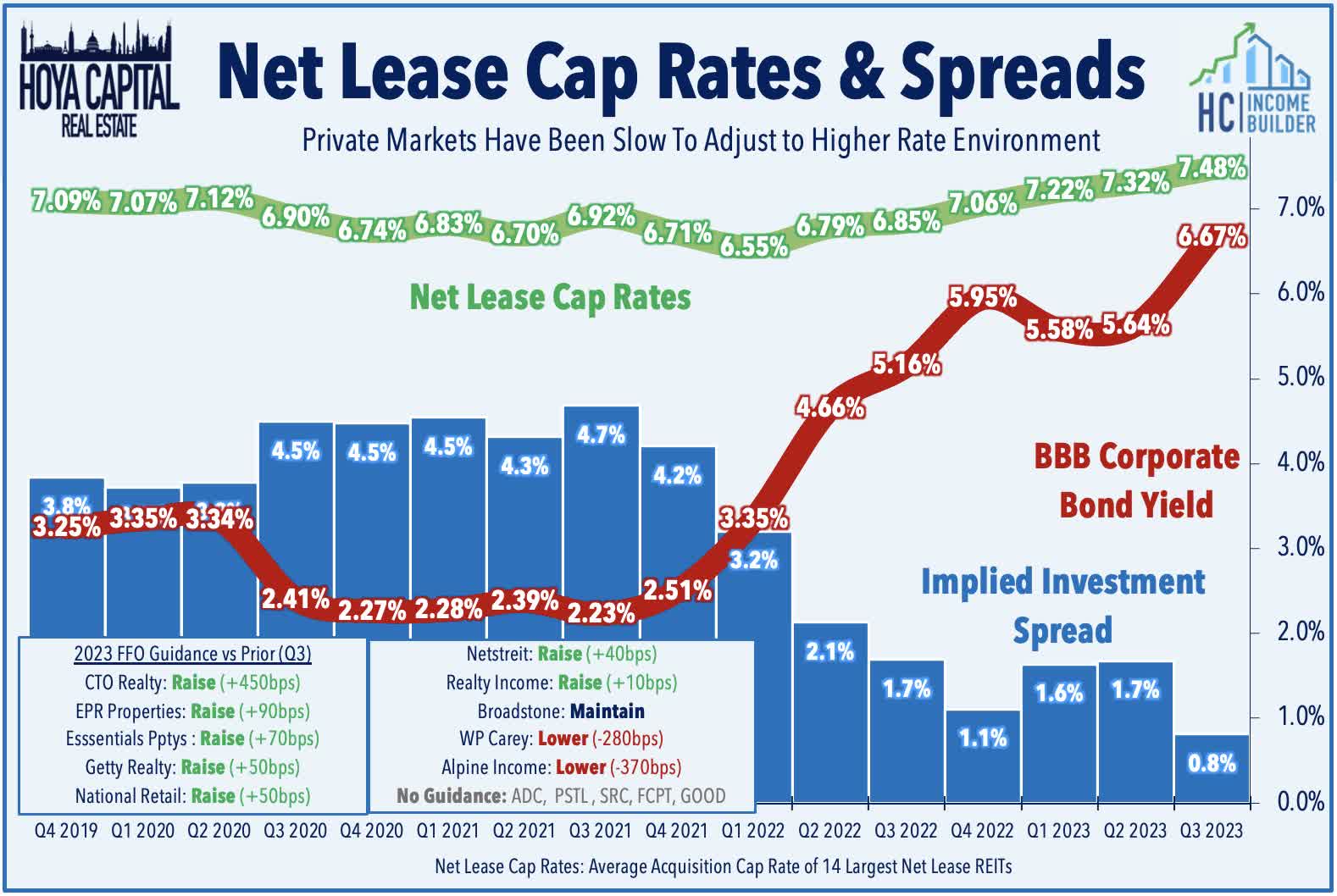

Net Lease : As expected following its office divestiture, net lease REIT W. P. Carey ( WPC ) announced this week that it will trim its quarterly dividend by 20% to $0.86/share (5.4% dividend yield). WPC has regained nearly all of its decline following its announcement in late September that it would sell its office assets - which comprise roughly 16% of its portfolio - aimed at "driving a re-rating" of WPC's stock price, which has traded at discounted valuations to similar-sized net lease peers. As part of the plan, WPC spun off 59 U.S. office properties into a new REIT - Net Lease Office Properties ( NLOP ) - that began trading in late October. WPC expects to complete the sale of the remaining 87 European office properties by early 2024. Post-transaction, roughly two-thirds of WPC's portfolio will be industrial net lease assets, with the bulk of the remainder in retail and self-storage. Industrial REITs trade with a current Price-to-FFO of around 20x, while WPC trades at 12x P/FFO. Elsewhere in the net lease space, Global Net Lease ( GNL ) slipped 2% after providing a business update in which it noted that it has completed 1.7 million SF of leasing activity so far this quarter, comprised of 313k SF of multi-tenant assets and nearly 1.4M SF of single-tenant assets. GNL achieved renewal leasing spreads of 9.8% on its single-tenant leases and achieved leasing spreads of 3.4% on its multi-tenant leases. In our Earnings Recap , we noted that net lease cap rates remained sticky in the third quarter as private market property owners have generally been slow to adjust their valuation expectations to the higher interest rate environment.

{kind=link}

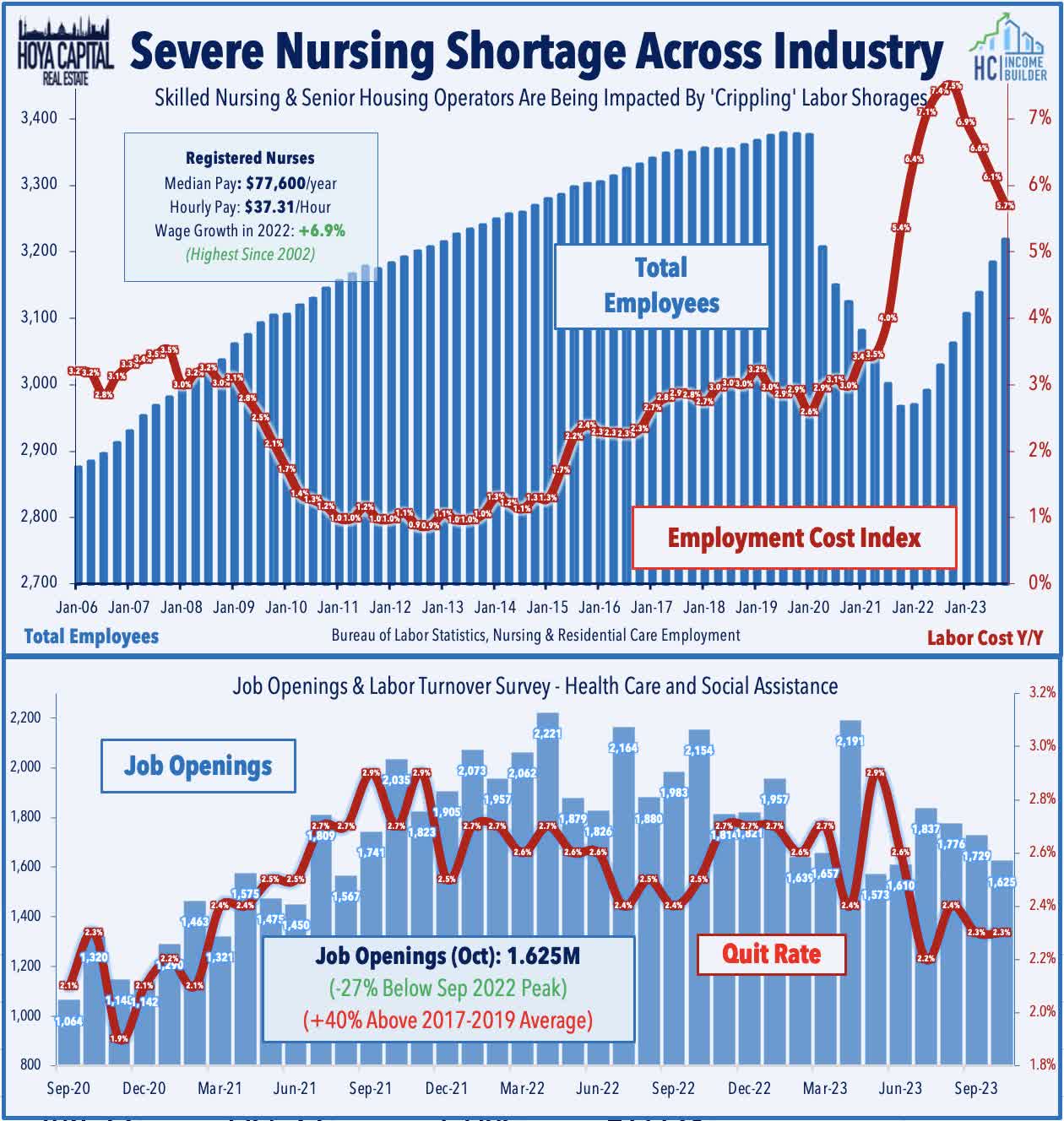

Healthcare : Also on the downside this week, Omega Healthcare ( OHI ) dipped 5% after it provided an operating update in which it noted that two of its operators - Maplewood and LaVie - paid less contractual rent than owed in November. As a result, OHI noted that "the combined impact of these expected shortfalls means that we no longer expect our 4th quarter FAD to approximate our dividend." OHI did not comment on whether or not it would reduce its dividend but noted that it expects cash flows to "materially exceed the Q4 run rate" upon the conclusion of its in-progress LaVie restructuring. Last quarter, OHI reported Funds Available for Distribution (“FAD”) of $0.68/share, which narrowly covered its dividend of $0.67/share. OHI also commented, "with many operators continuing to struggle with the impact of COVID-19 on both occupancy and staffing, there remains an elevated risk that additional operators may be unable to pay rent." Employment data this week showed that healthcare labor shortages are easing a bit, as job openings in healthcare and social assistance dropped to the lowest levels since June, while average hourly earnings of healthcare and education workers rose just 2.5% year-over-year in November, the lowest since the start of the pandemic and down from a peak of 7.3% in early 2022. Healthcare data provider NIC reported last month that national skilled nursing occupancy rates recovered to 82.3% in August - up significantly from the lows of around 70% in 2021, but still 6.9 percentage points below the February 2020 pre-pandemic level of 89.1%.

{kind=link}

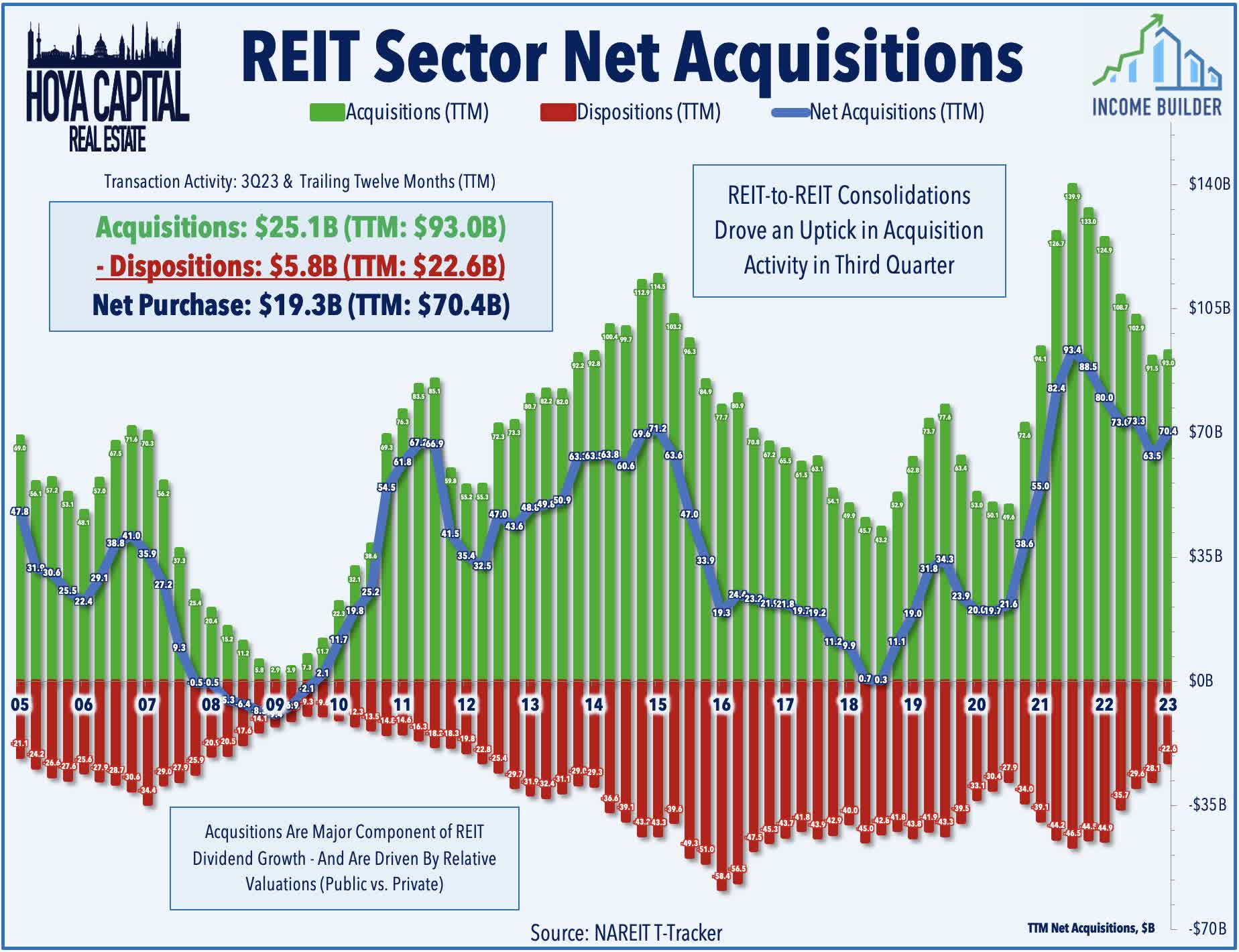

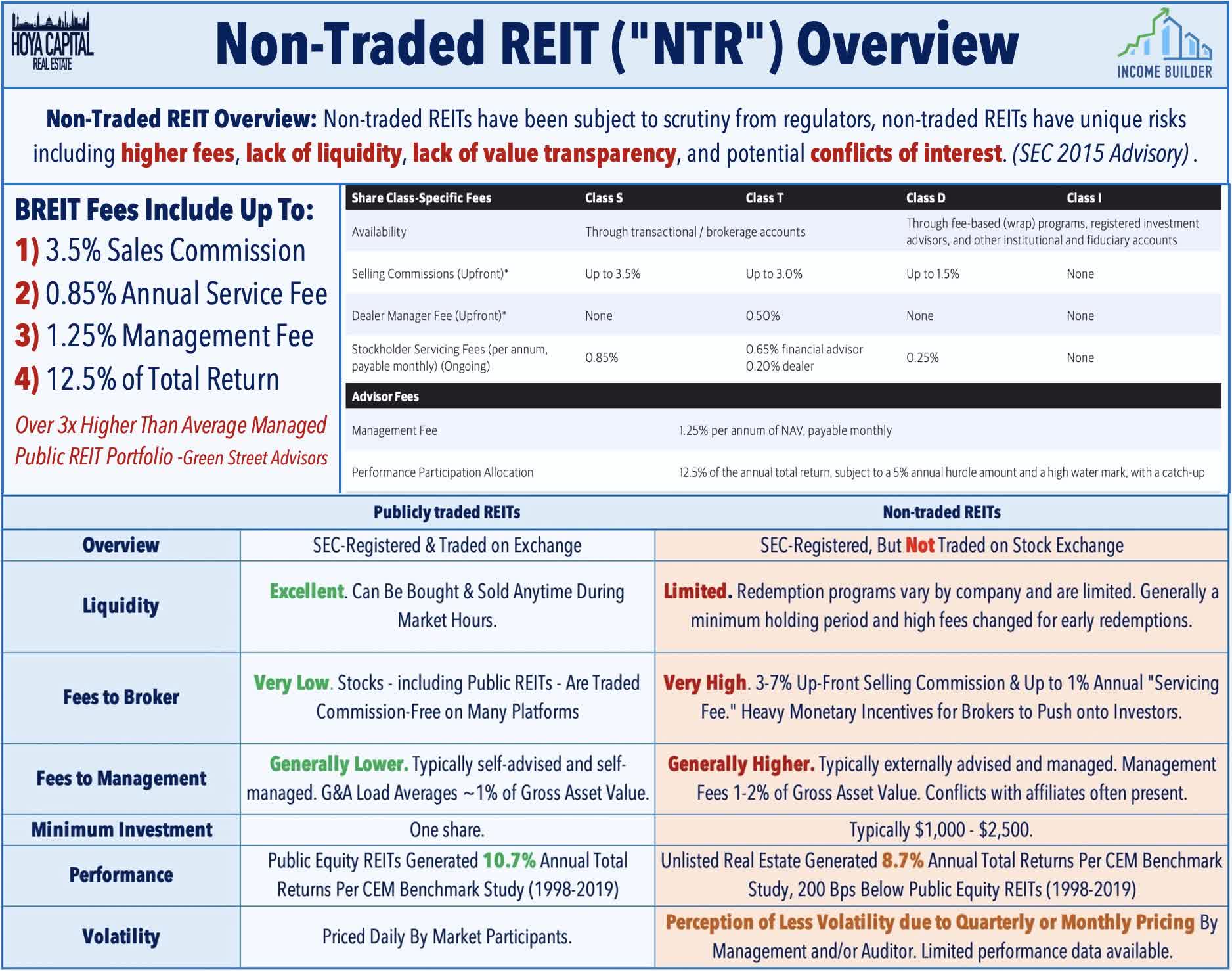

Last week, we published our State of the REIT Nation. Two years of persistent rate-driven pressure on residential and commercial real estate markets appears to finally be abating as the worst of pandemic-era inflationary pressures subside. This 'light-at-the-end-of-the-tunnel' comes as commercial property values were approaching the critical 20% drawdown level, a level that can result in cascading distress that extends beyond the weakest players. We're not out of the woods, yet, as expectations of "Higher for Longer" are merely shifting to "High for Long" in which benchmark rates will remain materially above pre-pandemic levels into 2025. The 'unwind' is just beginning for the "Zero-Rate Heroes," however, as the business models of many private equity funds and non-traded REITs are contingent on cheap and plentiful debt, which counteracted the drag from higher fees, inefficient structure, and often sub-standard corporate governance. We noted that macroeconomic conditions are aligning in an ideal manner for low-levered entities with access to "nimble" equity capital - conditions that maximize the true competitive advantage of the public REIT model, which these entities have been unable to exploit in the "lower forever" environment.

{kind=link}

On that note, asset manager Blackstone ( BX ) was in focus this week after The Wall Street Journal published a column this week that raised questions about the self-calculated valuations for its non-traded real estate platform, BREIT. An issue that we've flagged for several years over various reports, the column noted that non-traded funds "have broad leeway to define their NAV measurements however they want" and highlighted the wide disparity between exchange-listed REIT valuations and those reported by several of the largest non-traded vehicles. BREIT frequently cities these self-calculated performance metrics in marketing pieces, including the claim that BREIT has outperformed publicly-traded REITs "by more than 4x" since inception and "outperformed its non-traded REIT peers by nearly 700 basis points over the last year." While the Equity REIT Index has dipped roughly 25% since the start of 2022, BREIT's self-reported NAV is actually up by 2%, while Starwood's comparable NTR is lower by 5%. Investors attempting to "call" these NTRs on these self-reported valuations by redeeming their shares at this reported NAV have had to wait in line for over a year. BREIT announced last week that it limited redemptions for the 13th straight month in November, exercising its cap at 2% of NAV in any month and 5% of NAV in a calendar quarter. Since November 2022, when BREIT raised the redemption gates, BREIT has returned $13.8B to investors.

{kind=link}

Additional Headlines from The Daily REITBeat

- VICI Properties ( VICI ) announced a deal to provide a $212M mezzanine loan investment to Kalahari Resorts and Conventions to fund the development of a Kalahari indoor waterpark resort in Thornburg, VA.

- Easterly Government ( DEA ) announced a series of executive suite changes, including that its CEO William Trimble will retire at the end of the year, while Darrell Crate, the current Chairman will assume the role as CEO.

- Ashford Hospitality ( AHT ) completed the transfer of ownership of five hotels in the KEYS F loan pool to its mortgage lender: 1) Embassy Suites Flagstaff, AZ; 2) Embassy Suites Walnut Creek, CA; 3) Marriott Bridgewater, NJ; 4) Marriott Research Triangle, NC; 5) W Atlanta Downtown

Mortgage REIT Week In Review

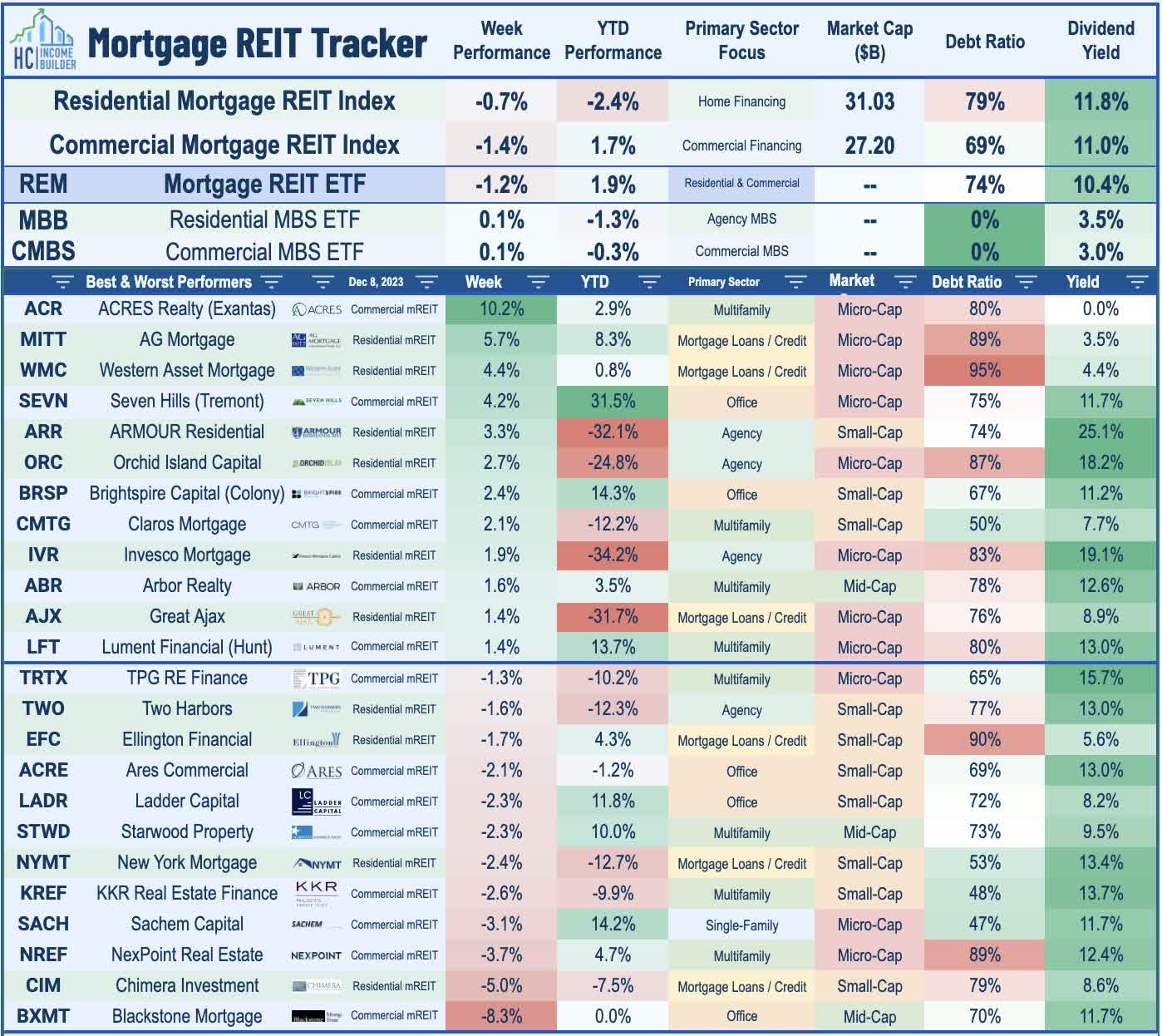

Following gains of over 5% last week - which pushed their six-week rally to nearly 25% - Mortgage REITs traded modestly lower this week, with the iShares Mortgage Real Estate Capped ETF ( REM ) slipping 1.2%. Residential mortgage REITs were the leaders this week as MBS spreads and benchmark interest rates continued to trend favorably following a rough period of stiff headwinds for much of 2023. A half-dozen mREITs declared dividends this week, each of which held their payouts steady with current levels including Annaly Capital ( NLY ), PennyMac ( PMT ), Cherry Hill ( CHMI ), Ellington Residential ( EARN ), and Redwood Trust ( RWT ). The average residential mREIT now pays a dividend yield of 11.8%, while the average commercial mREIT yields 11.0%.

{kind=link}

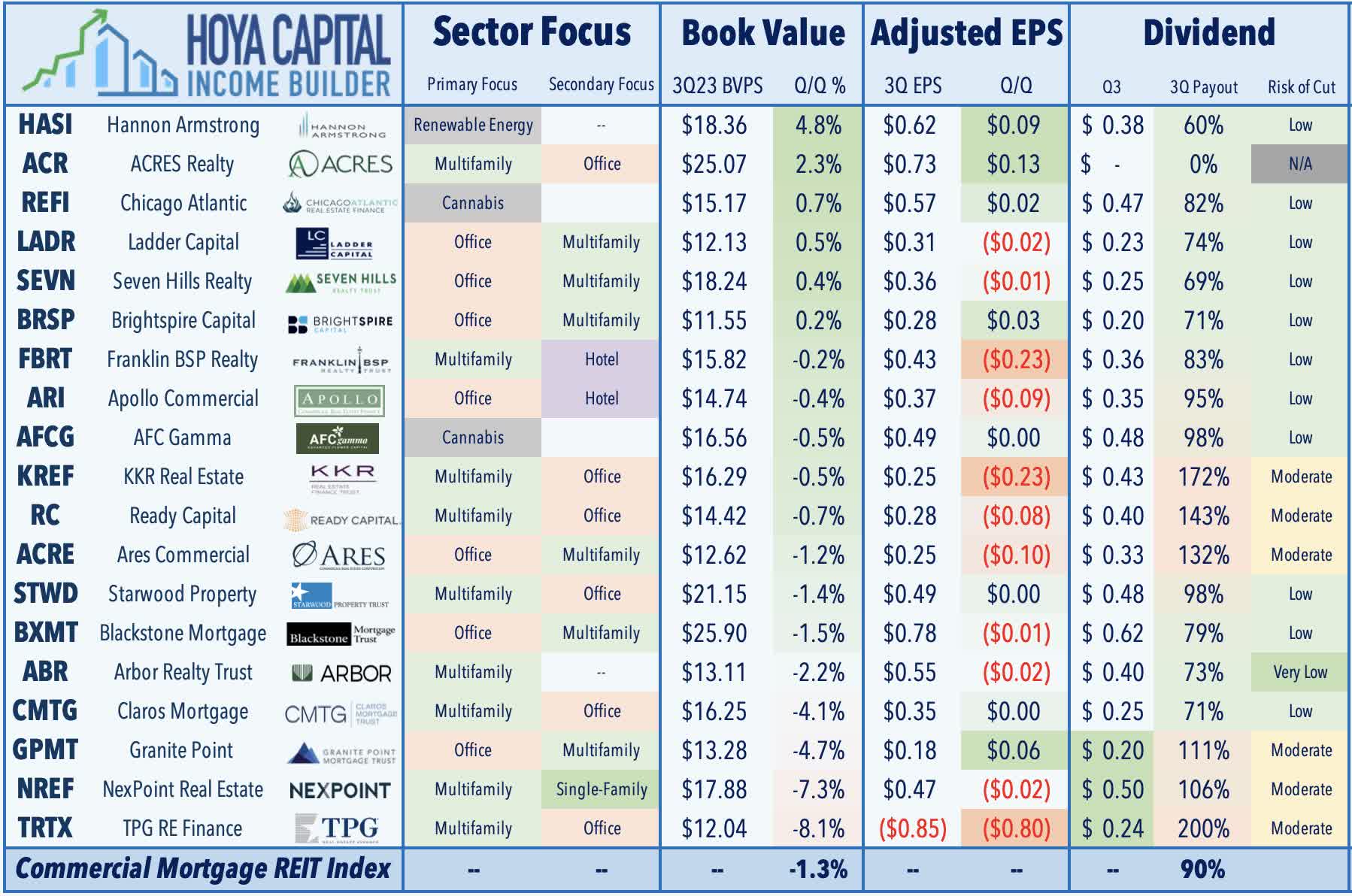

Perhaps coincidentally following the WSJ column on BREIT, another Blackstone affiliate was also under scrutiny this week. Blackstone Mortgage ( BXMT ) - the second-largest commercial mortgage REIT - dipped 8% this week after short seller Carson Block of Muddy Waters said he's short BXMT during a presentation at the Sohn Investment Conference. Block believes that BXMT is facing a "possible liquidity crisis" and predicts it will be forced to cut its dividend "by at least half," reasoning that BXMT's borrowers will be unable to refinance at their higher floating interest rates. BXMT reported last quarter that only 5% of its $22B loan portfolio is non-performing, and that its weighted-average origination loan-to-value is a relatively modest 64%. BXMT reported distributable EPS of $0.78 in Q3 - up 10% from last year and easily covering its $0.62/share dividend. BXMT has been among the better-performing REITs this year, producing a total return of 16.5% thus far in 2023 - primarily from its double-digit-yielding dividend. A spokesperson for the BXMT said in an emailed statement that the trust’s liquidity is at “record levels,” it has continued to reduce its leverage, and has taken steps that leave it “well positioned to navigate this environment.”

{kind=link}

2023 Performance Recap & 2022 Review

With just three weeks left in 2023, the Equity REIT Index is now higher by 1.2% on a price return basis for the year (4.2% on a total return basis), while the Mortgage REIT Index is higher by 1.9% (+13.1% on a total return basis). This compares with the 20.3% gain on the S&P 500 and the 8.8% gain for the S&P Mid-Cap 400 . Within the real estate sector, nine property sectors are now in positive territory on the year, led by Data Center, Single-Family Rental, and Mall REITs, while Net Lease and Farmland REITs have lagged on the downside. At 4.25%, the 10-Year Treasury Yield has climbed 37 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but down from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is slightly higher this year, producing total returns of 2.7% thus far. WTI Crude Oil - perhaps the most important "swing" inflation input - is now lower by 5.1% this year, while Natural Gas is lower by over 60% this year.

{kind=link}

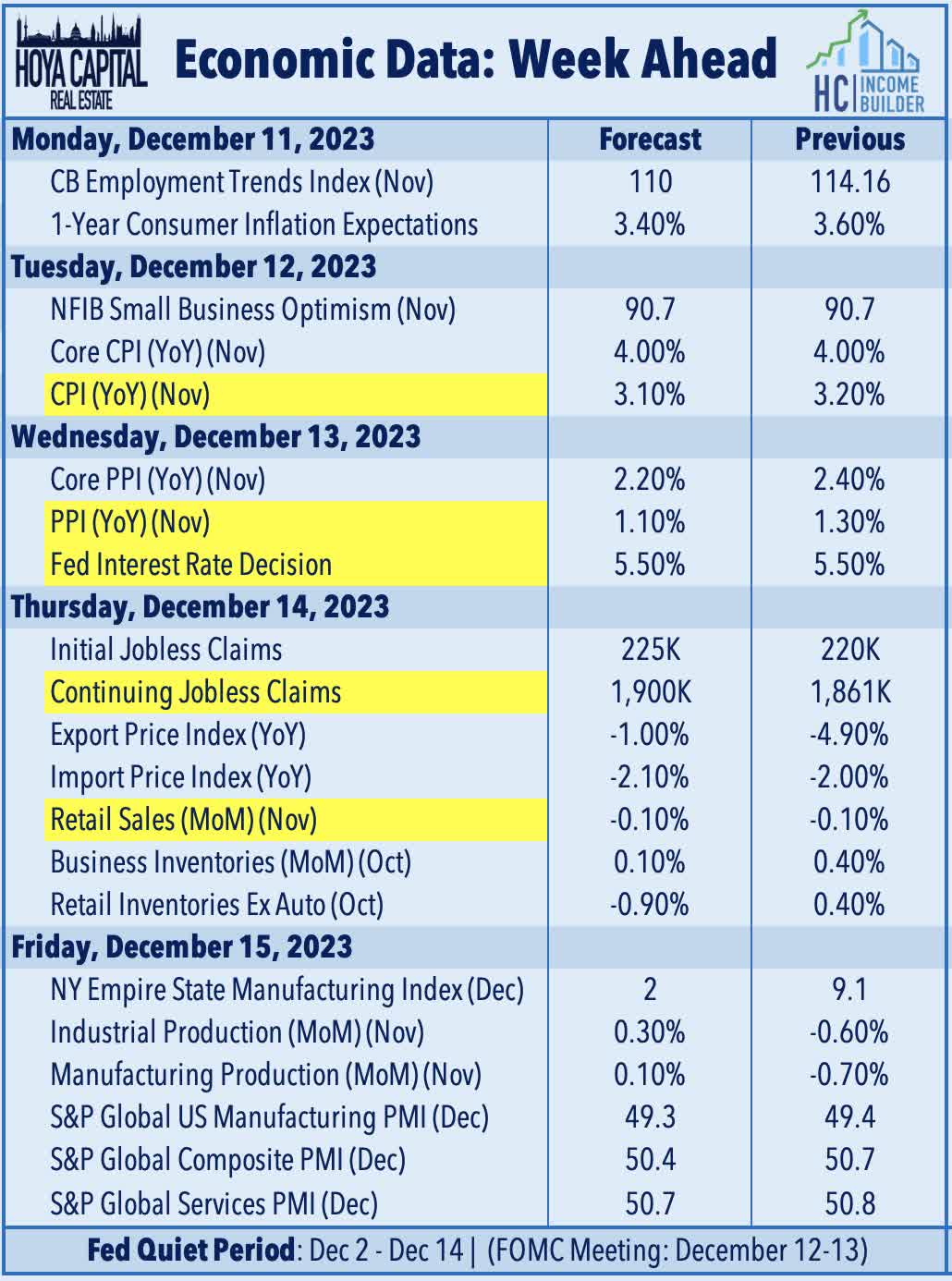

Economic Calendar In The Week Ahead

A critical slate of inflation data will precede the Fed's decision. The main event comes on Tuesday with the Consumer Price Index for November, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The Headline CPI is expected to moderate to a 3.1% year-over-year rate - down from 3.2% last month - while the Core CPI is expected to remain at 4.0% as some of the "hottest" prints seen in mid-2022 begin to roll off, while the heavily-weighted shelter component finally begins to moderate. Gasoline prices - which drove a reacceleration in inflation from June through September - were lower by an average of 8% during November compared with the prior month, and are currently 16% below the September peak. On Wednesday, we'll see the Producer Price Index, which has recently shown an even more significant cooling of price pressures. The Headline PPI is expected to decline back below the Fed's 2% target to 1.1% in November, while the Core PPI is expected to cool to 2.2%. We'll also be watching Retail Sales data on Thursday, covering the first month of the important holiday shopping season. Retail sales - which had been surprisingly resilient for much of the year - showed signs of softness in the latest October report. We'll also be watching a busy slate of Purchasing Managers Index ("PMI") data throughout the week, including S&P Global's December PMI report on Friday.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

'Tis The Season For Dividends