DNNGY - Ørsted A/S: The Front-Runner In Offshore Wind

2024-01-17 04:30:59 ET

Summary

- Wall Street firms pushed for ESG-focused companies post-pandemic, leading to Ørsted's stock reaching all-time highs.

- Government funding for renewable infrastructure projects caused offshore wind leases to skyrocket to over $1 billion.

- Despite challenges, there is potential for offshore wind to regain commercial growth with upcoming offshore wind leases in Europe and Southeast Asia.

Editor's note: Seeking Alpha is proud to welcome Matt Farley as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Ørsted (DNNGY) has a unique opportunity, being a front-runner in the offshore wind market and generating power from nearly 100% renewable sources. This is why I am confident that Ørsted's stock price is currently 20% undervalued based on current earnings and multiples. I am also confident that Ørsted's stock price will grow extensively from the $18-19 price today to $30 by YE 2025 to get closer to that fair valuation and the stock will grow to $70 or more by 2030 due to EBITDA growth and minor multiple expansion. During the next seven years, EBITDA is expected to grow from $3bn today to $7.5b in 2030 by investing more in the Americas, European and Asia Pacific markets . During this time, the P/EBITDA multiple for Ørsted should expand from 7.5 today to 12x in 2030. All the while you will receive an annual dividend steadily growing between 5-6% per annum.

Company Overview

Ørsted is a Danish renewables company focused on creating a world powered entirely by green energy. The company itself is nearly 100% renewable and is the leader by a significant margin in the offshore wind space. To give some color to this statement, Ørsted controls 70% more awarded capacity than the 2nd place company and their offshore wind portfolio is 2.2 times larger than the closest competitor (this includes installed, under construction, and awarded). Ørsted originally had non-renewable beginnings, previously operating as DONG. In 2017, the company refocused its strategy fully dissolved its coal assets, and sold its oil and gas assets to INEOS for $1bn.

Orsted Ambition (Orsted Capital Markets Day (June 2023) )

{kind=link}

Recent Price History And Volatility Of The Stock Price

In the wake of the pandemic, Wall Street firms witnessed a large push to buy up ESG-focused companies. This propelled Danish offshore wind leader, Ørsted, from a mere $30 stock in 2020 to unsustainable all-time highs north of $70 USD in January 2021.

Since the 2021 peak in the stock price, the ongoing War in Ukraine started in February 2022 and kept energy prices in Europe elevated through 2022. This provided short-lived inflation to the stock price on a fundamental basis, but the price retraced back to a more normal $30 range before entering 2023.

Opportunities And Challenges In The Evolving Offshore Wind Industry Post-2023

The landscape for the offshore wind industry changed in FY 2023. Global government entities, aligning with the objectives of the 2015 Paris Agreement, directed their efforts towards transitioning their respective country's long-term energy infrastructure goals towards renewables. These moves have created dozens of countries to push towards an environmental goal with renewables regardless of commercial economics. The 2023 Inflation Reduction Act ((IRA)) and other legislative and global ESG objectives have provided billions of dollars of funding for infrastructure projects. Legislative action like this over the past decade has inflated offshore wind leases to absurd prices where economics for wind projects remain challenged. To put it in perspective, US offshore wind leases initially cost hundreds of thousands of dollars in 2009 but with all the publicity and politics behind this space, leases have grown to hundreds of millions or even north of $1B for some European leases! This upfront lease cost and competition provided by government stimulus has lowered the economic returns of these offshore wind projects to single digits or sometimes even negative returns.

All of this does not make me bearish on the renewable front - quite the contrary. The current emphasis on the future of the offshore wind space coupled with the recent write-downs by several companies in New York in New Jersey taken in 2023 makes me confident that profitable growth is back on the horizon if deflation in the offshore wind supply chain and leases takes place. All the while, there are dozens of renewable electricity capacity goals unfulfilled by numerous North American, European and Asian countries (these capacity goals are generally measured in gigawatts, sometimes shortened to GW).

For instance, the United States has a national offshore wind goal of 30 gigawatts of offshore wind by 2030. The east coast leases will be in the Gulf of Maine, the New York Bight, Central Atlantic, and Carolina Long Bay. The west coast leases will be in Northern & Central California and Oregon, and the third and best coast, the Gulf of Mexico. 2021 offshore lease sales off the East Coast of the United States brought in over $2bn in awards. In December 2022, the five offshore wind leases in California awarded through the Bureau of Ocean Energy Management ((BOEM)) brought in $757 million in awards and over $100m in training for local workforce and US supply chains.

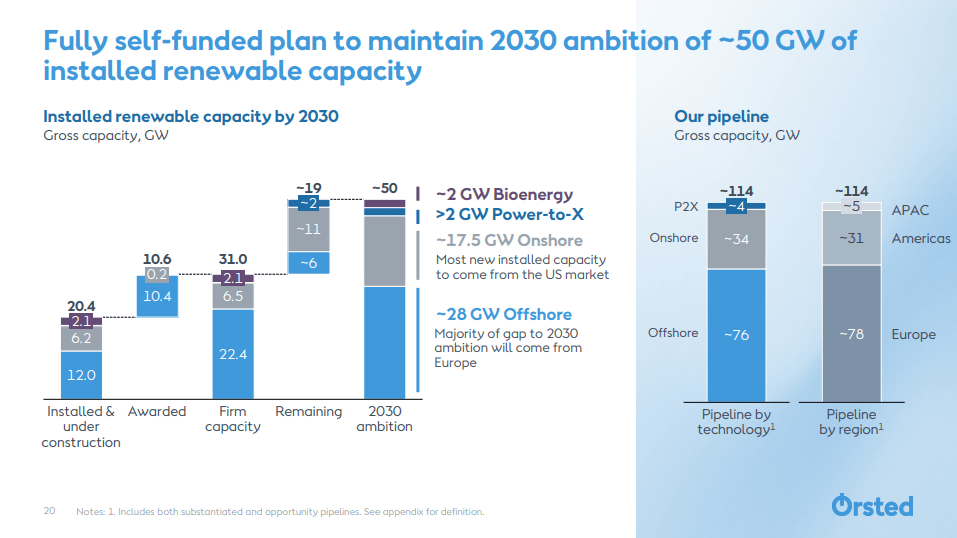

So why am I optimistic about Ørsted? As the leader in offshore installed wind capacity, Ørsted aims to create a world powered entirely by green energy, with a renewable portfolio of over 50 GW by 2030. Ørsted controls 70% more awarded capacity than the 2nd place company and their offshore wind portfolio is 2.2 times larger than the closest competitor (this includes installed, under construction, and awarded). Between now and 2030, Ørsted plans to maintain this leadership in the Americas, European, and AsPac markets.

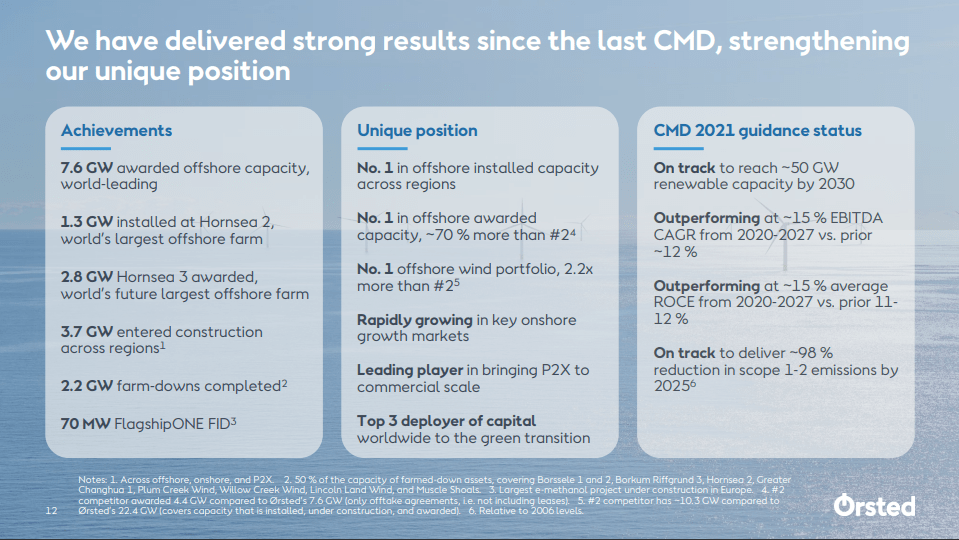

Orsted 50 GW Renewables Capacity Growth to 2030 (Orsted Capital Markets Day (June 2023)) Orsted achievements, unique position and status on previous capital markets day (Orsted Capital Markets Day June 2023)

{kind=link}

{kind=link}

Despite a $4bn write-down of the New Jersey Ocean Wind project taken in the 4th quarter of 2023, the stock plummeted to $13 USD, where I picked up a small position. The stock has since rebounded to the $18-$19 range. There will be a balance point where offshore wind gets back to commercial economic growth as renegotiations and supply chains deflate.

Ørsted Financial Targets And Return To Shareholders

The comprehensive strategy outlined above makes Ørsted the clear front-runner in offshore wind and also the world's first major green energy player. As the projected 50 GW of installed renewables capacity comes online, by 2030, EBITDA growth is expected to expand by a 13% CAGR, with a return on capital employed growing to 14%. This means EBITDA will grow from $3bn in 2023 to slightly over $7.5bn EBITDA.

Orsted Future Metrics To Arrive at Future Stock Price (Orsted Capital Markets Day)

With a price to EBITDA of 10x, Ørsted grows to $30 by the end of 2025. Based on a 2030 EBITDA of $7.5bn, the market cap of Ørsted grows to over $75bn from $24bn today, a 212% increase with a minor multiple expansion. The corresponding stock price would be approximately $75 with a P/EBITDA multiple growing to 12x.

The current $0.66 annual dividend is expected to grow by circa 7% to 2025 and 5-6% dividend growth out to 2030, all while maintaining the balance sheet and credit rating. (The 2023 annual dividend of $0.66 represents a 3.6% dividend at current stock price as of Jan 7, 2024).

Recap Of Capital Markets Day (June 2023)

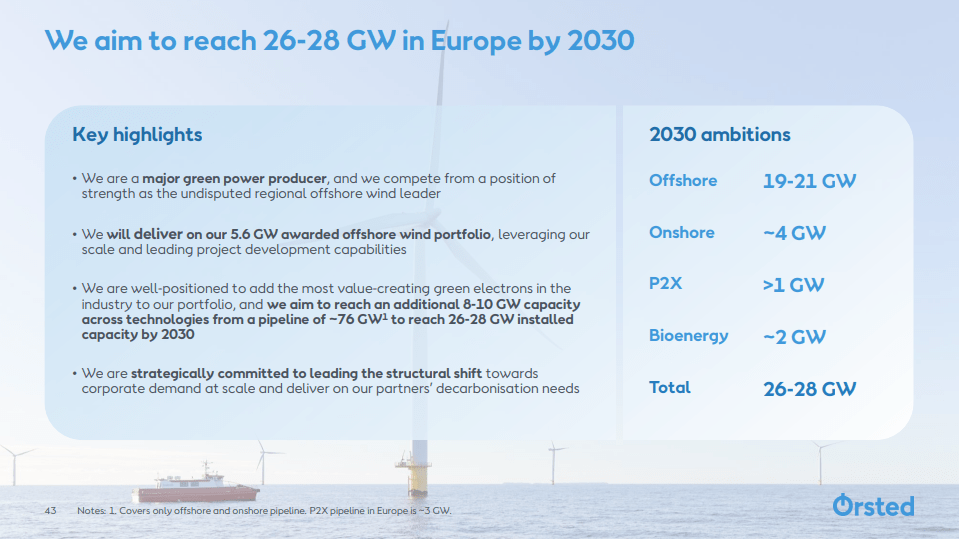

Ørsted's plans and ambitions are clearly defined in their June 2023 Capital Markets day . The European offshore wind capacity is expected to go from 30 GW in 2022 to over 140 GW in 2030 - growth of over 3.6x. By 2030, Ørsted plans to take a 19-21 GW offshore wind position in the European Market and a 26-28 GW renewable portfolio.

Orsted's Europe Ambitions by 2030 (Orsted Capital Markets Day (June 2023))

{kind=link}

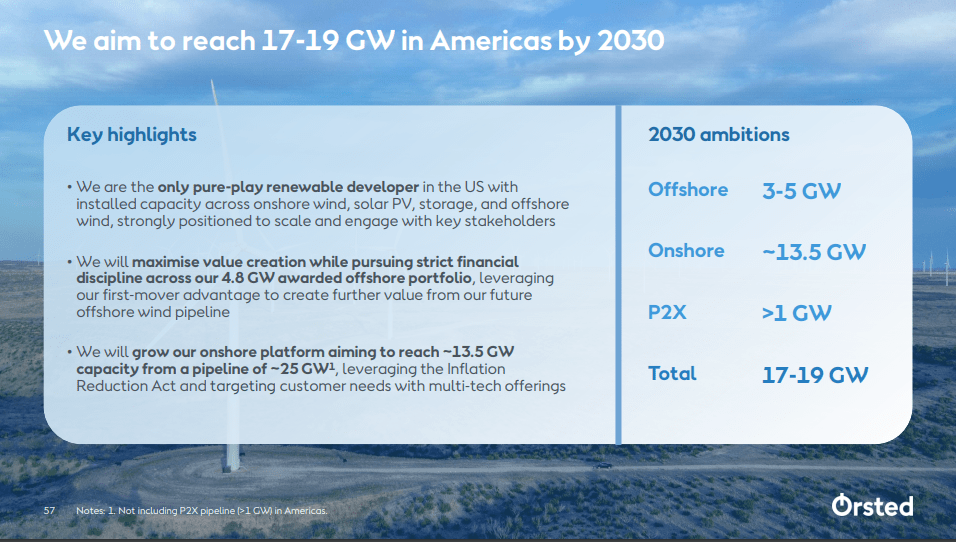

Offshore wind capacity in Asia Pacific (excluding China) is expected to grow substantially, from 2 GW installed in 2022 to over 30 GW in 2030, and to 60 GW in 2035. Ørsted currently has a 1.9 GW position in Asia and plans to grow this to a 3-5 GW position by 2030 pending farm-downs (to maximize returns).

Ørsted boasts that they are the only pure-play renewable developer in the United States with onshore and offshore wind, solar and energy storage. Ørsted has an awarded Offshore wind capacity in the Americas of 5 GW - this volume is in question with the recent write-down of the New Jersey Ocean Wind project awaiting renegotiations. Ørsted plans to take a position of 3-5 GW in offshore wind and a more substantial 13.5 GW in onshore wind. Increasing the Americas' renewable portfolio to 17-19 GW.

Orsted's Americas Ambitions to 2030 (Orsted Capital Markets Day (June 2023) )

{kind=link}

Ørsted has also introduced a Power-to-X portion of their portfolio, which is curating renewable energies to provide direct hydrogen and e-fuels too hard to decarbonize and electrify industries. This space is expected to grow from less than 1 GW today to 21 GW in 2030 and over 150 GW in 2050. Ørsted plans to deliver greater than 2 GW in electrolyser capacity by 2030 and maintain a 4 GW pipeline across priority markets.

Risks To Delivery

I believe there is a continued risk that inflation in materials costs and supply chain costs associated with offshore wind persists, making projects uneconomic for the entire industry. And the reluctance of governments to have offshore lease sales may slow down the growth trajectory of Ørsted's offshore wind-focused businesses. The materials and supply chain cost concerns are already a risk that has been realized over the past two years with the recent $4bn write-downs in New Jersey, but I believe industry inflation is normalizing. However, if inflation continues in the materials and supply chain, there may be more write-downs to come.

If deflation of costs does not occur and governments slow down offshore lease offerings, I may be included to rethink or adjust my growth trajectories and bull thesis.

Conclusion

As we transition the energy grid away from fossil fuels, and we witness Wall Street's continued focus on ESG organizations, Ørsted stands out as a top tier choice for portfolios seeking a lower-risk profile. I anticipate the return of the stock price to a fairer valuation of $30 USD by YE 2025, which represents a 65% capital return over the next 24 months all while paying a $0.70 annual dividend payable in March/April 2024 (estimated) and a $0.75 dividend in 2025. Feel free to take your profits at YE2025 or hold until 2030 while the stock grows closer to $75/share.

For further details see:

Ørsted A/S: The Front-Runner In Offshore Wind