DNNGY - Ørsted: Beaten Down By Lower Energy Prices (Downgrade)

2023-08-30 10:58:27 ET

Summary

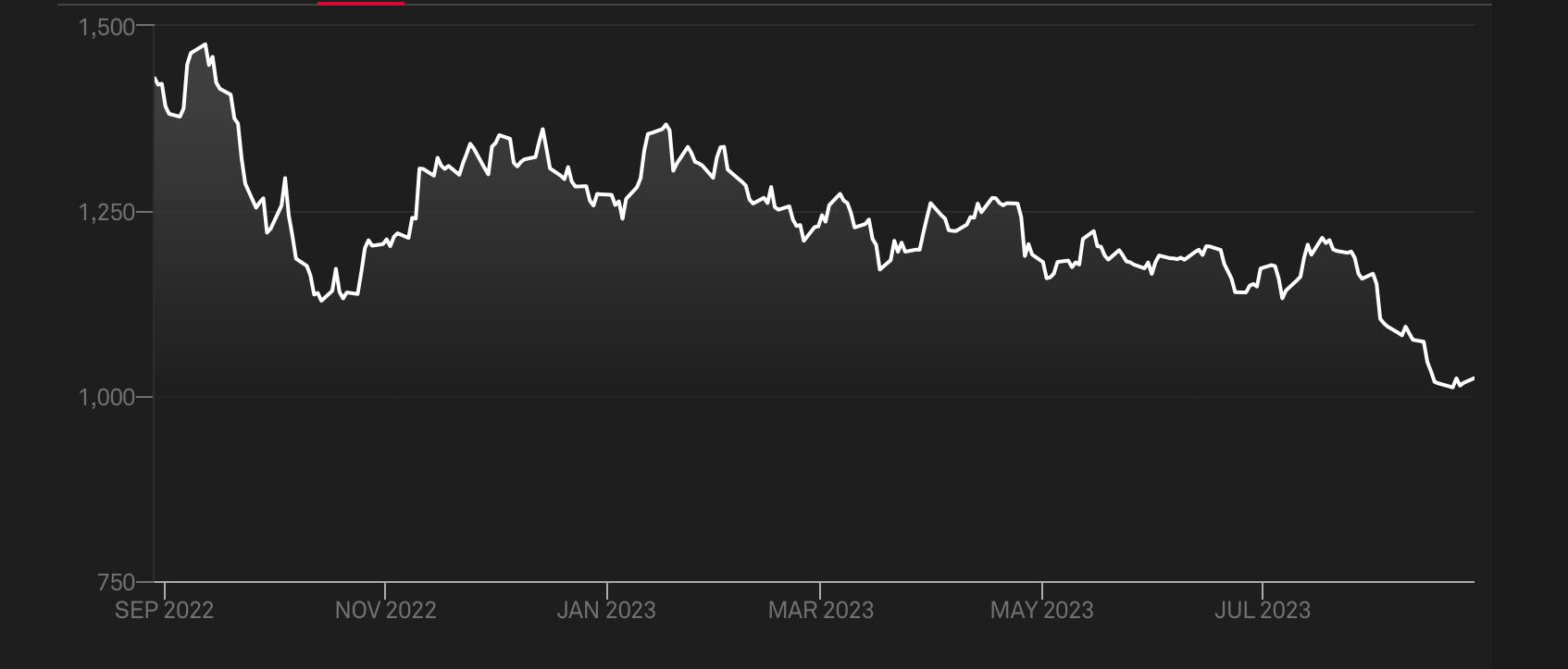

- Ørsted's stock has declined by 10.2% since February and 18% over the past year, along with the S&P Global Clean Energy Index on falling energy prices.

- Despite the decline, Ørsted's price-to-earnings ratio has increased, indicating its price still hasn't fallen proportionally to the profit decline.

- Its long-term potential is still intact as a wind energy producer at a time when renewables are gaining ground, but for now, it's due for further correction.

The Danish clean energy utility Ørsted (DNNGY) has declined by 10.2% since I last wrote about it in February and has performed even worse over the past year, declining by 18%. It’s not alone in the drop, though. The S&P Global Clean Energy Index has dropped by an even bigger 29.6% over the year as energy prices have dropped.

{kind=link}

Higher market multiples

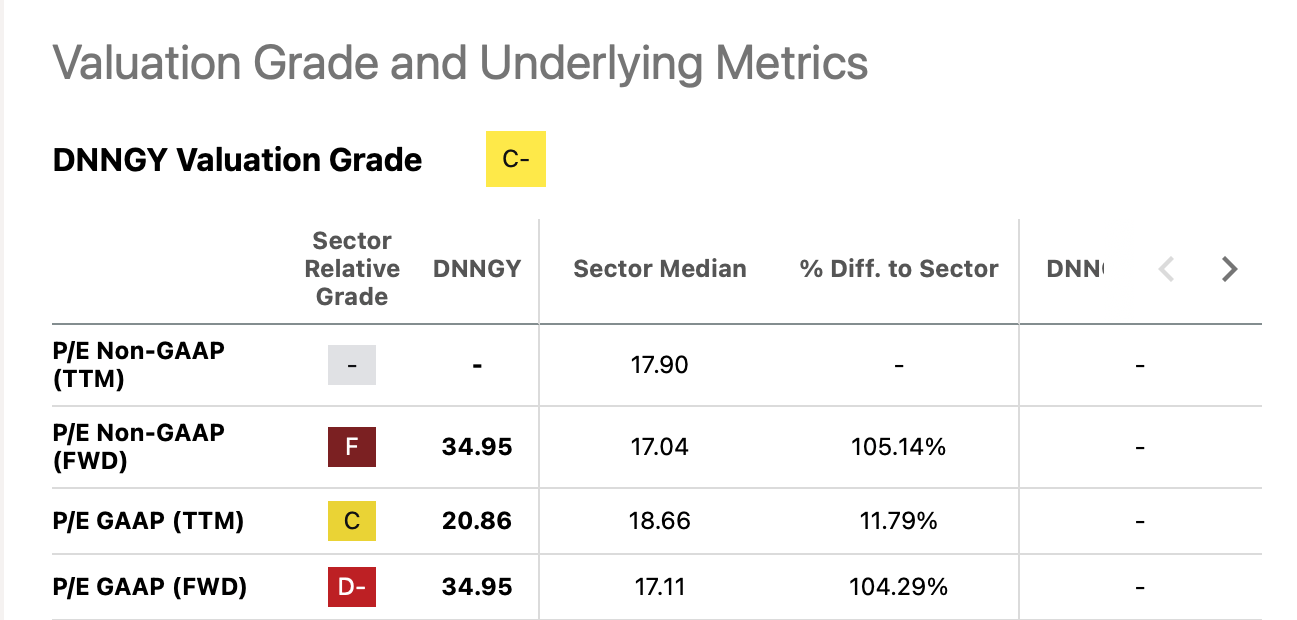

But here’s the rub. Despite the continued price decline Ørsted’s looking pricier than it was the last I checked, when the trailing twelve months GAAP price-to-earnings (P/E) ratio was at 18.6x, below both that for the utilities sector and the S&P 500 ( SP500 ).

{kind=link}

Market Multiples (Source: Seeking Alpha)

The ratio is now at 20.9x, clearly indicating that its profits have fallen by more than the price in the meantime. It’s also higher than utilities’ P/E at 18.7x, though it's some comfort that it’s still below that for the S&P 500 which has run up even higher to 25.6x .

While the long-term prospects for Ørsted remain unchanged with the fast rise of renewable energy, do the valuations indicate that it might be richly priced for now? Let’s consider its financials to figure out.

A look back

When I last wrote, the utility was fresh from its robust full-year numbers. Its EBITDA had risen by 32%, the return on capital employed [ROCE] had improved by 2 percentage points to 17% and it had a nice pipeline of projects underway too.

Falling energy prices impact financials

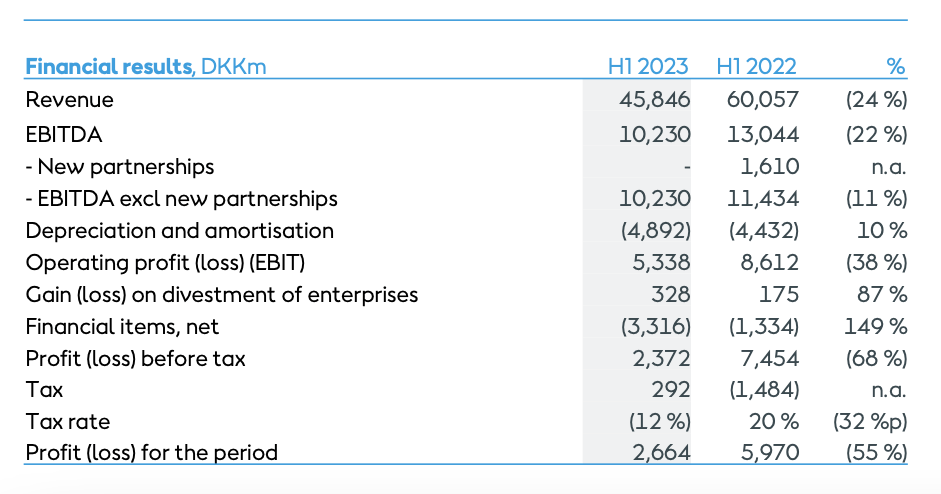

Since then, the company has released its results for both the first and second quarters of the year. The first half of 2023 (H1 2023) isn’t looking pretty, considering the energy prices. Revenues have declined by 24% year-on-year (YoY) owing to lower power and gas prices, but also due to lower gas demand.

{kind=link}

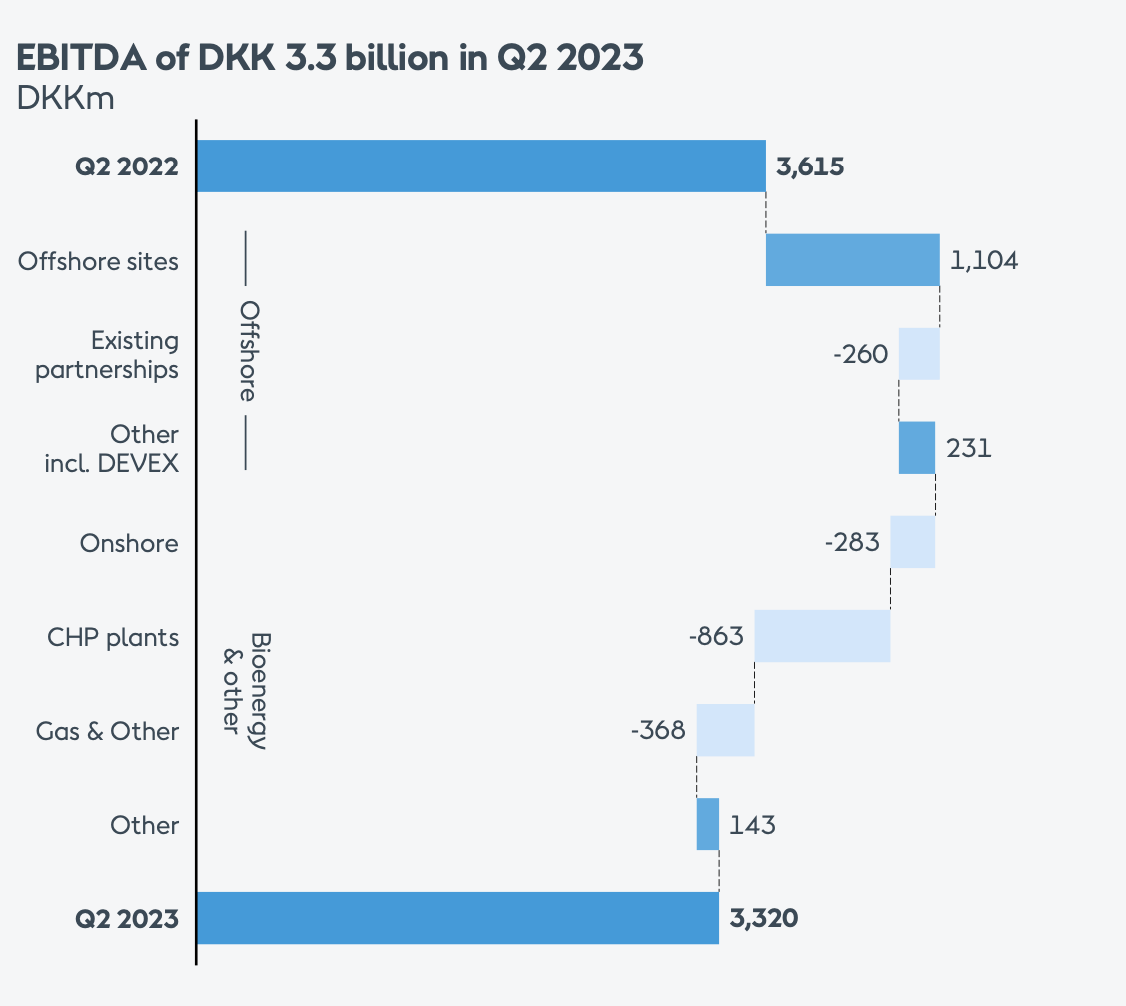

The company’s preferred profit measure, EBITDA, was also dragged down by 22% for the same reason, even as offshore wind’s profits grew (see chart below for Q2 2023 breakup). The fall was actually exaggerated due to the impact of new partnerships on last year’s number. Excluding new partnerships, the EBITDA decline actually halves.

{kind=link}

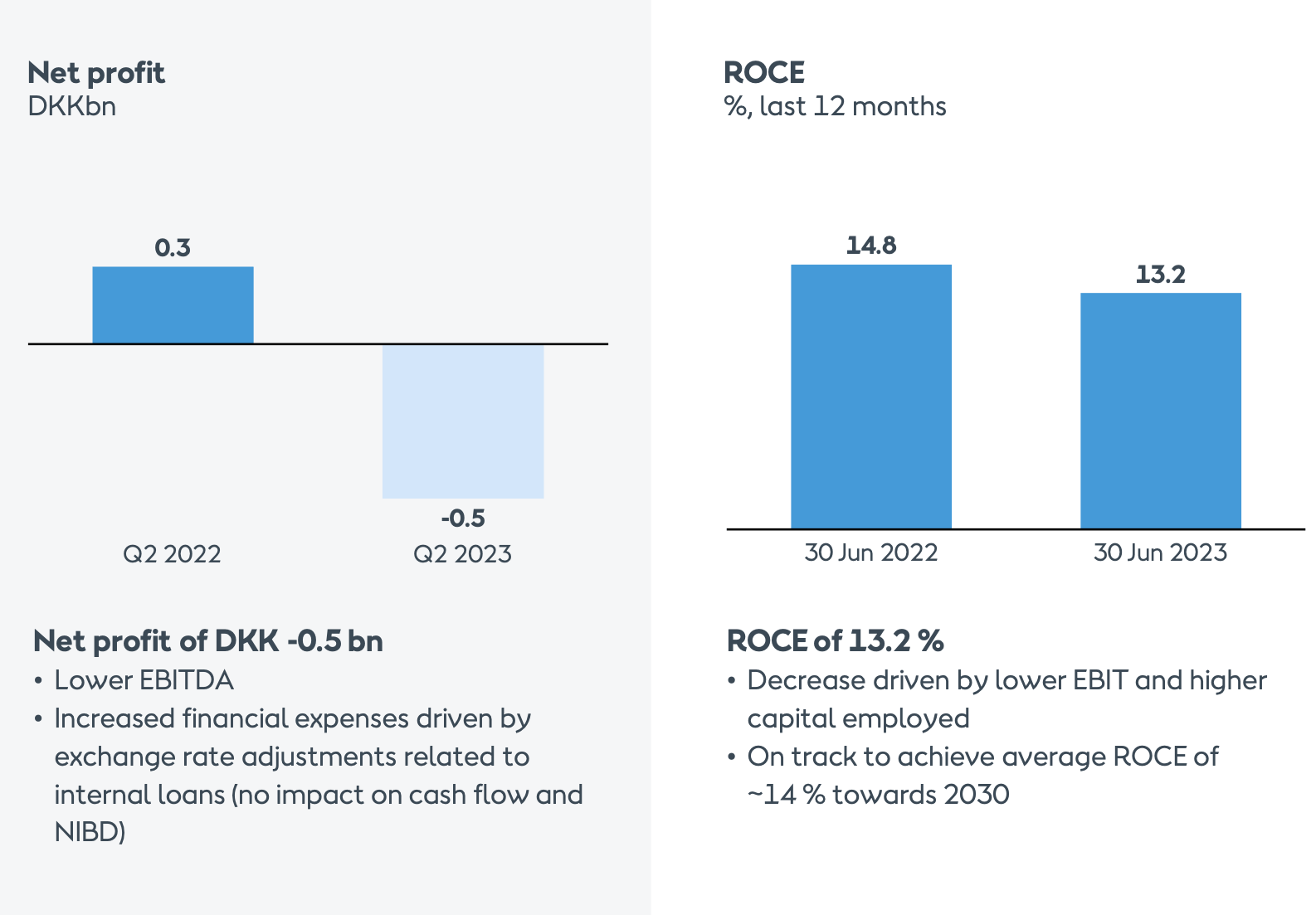

Interestingly, the EBITDA margin actually expanded to 22.3% in H1 2023 from 19% for EBITDA ex-new partnerships last year on a notable 27% YoY reduction in the cost of sales. The other profit measures didn’t show a similar rise, however. Both the operating and net margins dropped to 11.6% (H1 2022: 14.3%) and 5.8% (H1 2022: 9.9%) respectively. While operating profits were impacted negatively by higher depreciation, net profits saw a drag from higher financial expenses as well, which actually resulted in a net loss in Q2 2023 (see chart below).

{kind=link}

However, it bears mentioning that, unlike the EBITDA, the numbers sans the impact of new partnerships aren’t available for operating and net profits. Factoring it in indicates that the operating profit margin is essentially unchanged, while the net profit margin has still declined from 7.3% in H1 2022.

A fall in profits of course impacted Ørsted’s ROCE, which dropped to 13.2% from 14.8% in H1 2022 as the capital employed at the end of June at DKK 147.5 billion rose by 17% YoY (see chart above).

Small change to outlook

The company has also slightly changed its guidance for 2023. It now expects EBITDA to come in the range of DKK 20-23 billion, as opposed to DKK 21.1 billion earlier. This follows the better than expected earnings from offshore wind and lower earnings expectations from CHP plants, which use either fossil fuels or bioenergy in H1 2023.

The change in outlook can be either good or bad, depending on where in the range the final figure lands up. But if it comes in at the midpoint, EBITDA would inch up only to DKK 21.5 billion in 2023, a 1.9% rise over the previous guidance. There is something to be said for the fact that even as per the earlier guidance EBITDA was expected to remain unchanged (ex-new partnerships) from 2022, which was a far better year for the company, clearly driven by lower costs as we’ve seen in H1 2023.

Estimating net profits for 2023

The net profit to EBITDA ratio during the first half was 26%, which is particularly low. The ratio was at 47% in H1 2022 and 46% for the full year 2022. Net profits in H1 2023, as was noted above, were negatively impacted by financial costs, particularly as they relate to exchange rates. The same trend might or might not be at play in H2 2023.

Assuming that the H2 2023 number averages between the full-year figure and that in H1 2023, the company’s net profit is projected to be DKK 7.8 billion in 2023. This translates into a forward P/E of 28.9x, which is lower than the available current forward estimates indicate at 35.1x.

That said, the fact remains, that the ratio is still higher than for peers like Consolidated Edison ( ED ) or NextEra Energy ( NEE ) at 12.4x and 21.4x respectively. Ørsted’s forward ratio is also double that of the utilities sector. The point is, no matter how I look at it, it does look overvalued for right now.

What next?

I still like it as a long-term stock to hold in the portfolio. The company has a bright future as an established wind energy producer at a time when renewables are gaining ground.

But it’s also vulnerable to fluctuations in energy prices, and not in a small way, as both last year’s and this year’s numbers show. So even though fundamentally nothing has changed about the company, its financials have seen a temporary drop, which is reflected in its share price movements and market valuations too.

Despite weakening in price, however, it still looks pricey. Still, its H2 2023 numbers might just look better on a base effect as energy prices had started coming off in the second half of last year. I reckon its net profit could surprise the upside too after showing a weak performance in the first half. In the meantime, though, I expect its price to correct some more. I’m downgrading Ørsted to Hold, but the rating could change on improved Q3 2023 results.

For further details see:

Ørsted: Beaten Down By Lower Energy Prices (Downgrade)