DNNGY - Ørsted: Hedges Negatively Hit Strong Power Price Development

Summary

- Ørsted had a decent showing for FY 2022 with strong growth in new PPAs, and tailwinds from high prices of electricity.

- It would have been even better if not for poorly placed hedges that nullified some of these positive effects, whose negative results have been frontloaded into current earnings.

- While delays continue in the construction of Changhua 1, and impairments hit the very bottom line, the assets should hold longer-term value.

- But investors should acknowledge that the economics of offshore depend on continued government support and are among the most expensive renewable solutions.

- Indeed, impairments are coming from massive increases in CAPEX and OPEX associated with some developments.

Ørsted ( OTCPK:DNNGY ) is one of the more well-known renewable companies that trade on public markets, whose profile has been elevated by being a leader in offshore wind development which is a relatively new idea. The economics of their development activities have been great in the pre-inflation environment, and with support to the green agenda proving relatively market agnostic, valuations should hold better for these sorts of assets than most. While asset values are a point of question on the cost side for developments, the fundamental performance of their cash generating assets continues to be good, making strides in organic growth despite headwinds from hedging. This quarter, despite EBITDA growth, was an underperformance, and while we aren't buyers of Ørsted, we do suspect that their performance is going to improve going forward.

A Look at the Q4

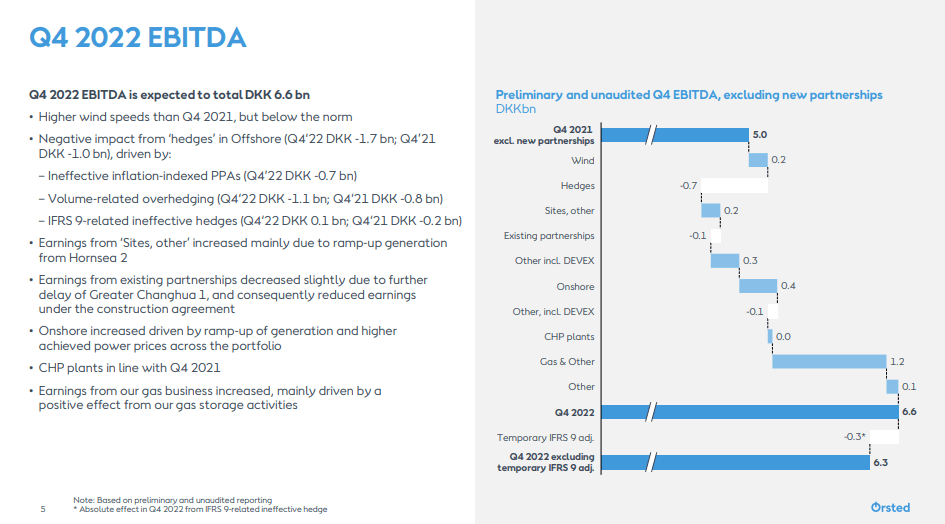

The Q4 is a little peculiar , but it can be explained through the EBITDA waterfall.

{kind=link}

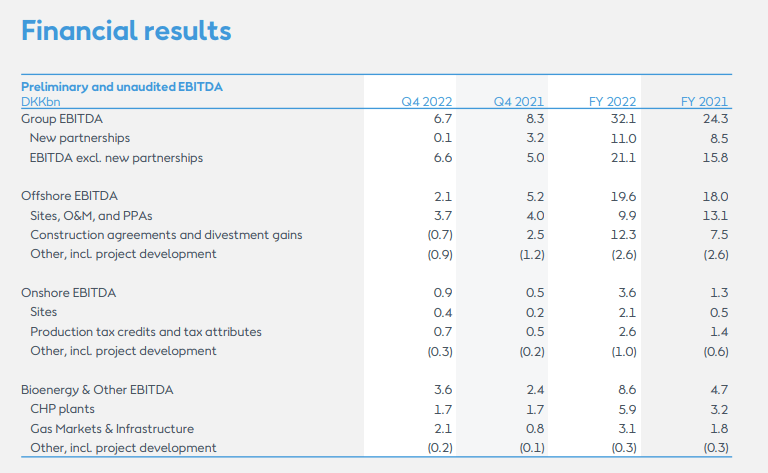

Wind activity, still below averages, were up, and power prices were up too. Onshore sites did well, and the big positive came from the gas trading business thanks to volatility in the gas markets in 2022 . This last effect is likely not to be repeated, and a deflation in electricity prices similarly will hurt EBITDA from existing partnerships. Note that the figures in the waterfall do not include the new contributions from newly established offtaking deals.

On the other hand, the negatives were coming from the hedges that they had in place. PPA indexation and other hedges in place were not helpful, and some of the hedges have become technically useless, and therefore have warranted basically an upfront impairment of the cash committed to those hedges under IFRS. The negative hedging effects in this quarter are all upfronted negative effects, that due to accounting thresholds have assumed the worst possible payout and value. While these are likely to be accurate, it is important to understand that the poor and ineffective hedging in place are not going to be haunting results any further. Hedges will be positive in 2023 according to management guidance.

The sites, other line didn't do as well as it could have. This EBITDA contribution comes from construction activity related to early stage projects like Changhua 1, which stalled due to difficulties in commissioning turbines - it hasn't happened yet. This is slowing down the cash flow forecasts, and of course affects valuation of the project together with the higher costs of capital due to higher debt costs. The only growth in this segment came from positive Hornsea developments.

We should mention at this point that there have been some impairments.

{kind=link}

The return profile of Ørsted, which relies on ROI from developments, is being impacted by Sunrise Wind, which due to the structural costliness of offshore wind, had to be impaired substantially on account of inflation, in particular of services related to constructing the offshore installations. This impairment represents about 2.5% of assets, which thankfully is low. However, costs in development could be an enduring problem for how these assets become valued even if inflation subsides because it will slow down the speed of development and the rotation of the assets in their typical farm-down model . Sunrise is the only asset with an impairment because it is the most recent one and was most levered to the inflation of these years which affects a large change on the assumptions of development costs for the asset. More mature developments are less problematic, and mark-to-market there is going to be value creation, but maybe not to the extent of assets in past years, where development IRR was high around 35%. It will be closer to WACC now as OPEX, CAPEX assumptions and capital markets - so no more impairments with apparently a 90% certainty on CAPEX for NEP and Ocean Wind, so short term developments.

Moreover, analysts were really probing management to understand how the economics of the developments would end up being in light of at least one impairment. Management has indicated vaguely that there are discussions with stakeholders that will improve value creation in light of the radically different market environment. There shouldn't be more delays on Sunrise at least.

Bottom Line

How profitable the developments become depend on how the offtaking deals associated with them are negotiated. Since costs are rising, stakeholders need to be dealt with in order for economics to improve. Thankfully, support for the renewable agenda very much favours Ørsted in its incremental ROI. Otherwise, current deals and new deal development are doing a lot to improve EBITDA on a FY basis.

{kind=link}

Ørsted's valuation is heavily dependent on the incremental ROI on their developments. News of improved deals with stakeholders will be important, but most of the developments shouldn't have their value creation too affected by delays and revised OPEX and CAPEX assumptions. Nonetheless, markets are right to question whether Ørsted is getting bang for their buck. Still, when they farm down, the multiple should be safe since we expect a recovery in market sentiment and infrastructure funding in the next year. Moreover, costs increases are unlikely to persist into the later years of the developments, some not producing cash flow till 2025. While they will have made a permanent rise this year to a meaningful extent, the lack of perpetuation is important. It's hard to know their capacity to value creation so we're not buyers, but we think that the worst is likely to be behind Ørsted, and as cost and financing conditions improve, as well as progress in the green agenda, things could start looking good again in terms of stock price.

For further details see:

Ørsted: Hedges Negatively Hit Strong Power Price Development