DNNGY - Ørsted's Undervaluation: A Compelling Opportunity Despite Some Setbacks

2023-08-31 05:49:45 ET

Summary

- Orsted, and renewable energy producers in general, have suffered from a number of headwinds in the last few years. As a result, investors are a lot less enthusiastic.

- Orsted further complicated things by making some mistakes, including a flawed hedging strategy.

- Recent results were encouraging, with significant growth in the offshore segment.

- With its massive pipeline, competitive advantages, and excellent growth visibility, we believe DNNGY deserves a higher valuation.

It's been tough being a clean energy investor the last couple of years, following a massive run-up in share prices after Covid. The low interest-rate environment that followed, and the excitement related to massive government incentives like the Inflation Reduction Act (IRA) had a lot to do with increasing valuations in the sector. Some valuation re-adjustments were necessary in many cases, but we now believe the pendulum has swung too far in the opposite direction.

Some blue-chip companies in the sector are trading at very attractive valuations. One such example is Orsted A/S ( OTCPK:DNNGY ), the Danish company that is number one globally in off-shore wind generation. Just in the past year it has lost ~20% of its value, but the whole sector has been under pressure, as can be seen by the decrease in value of the iShares Global Clean Energy ETF ( ICLN ).

When we started covering Orsted, we thought shares were reasonably valued and that investors would benefit from an expected doubling of the EBITDA by 2027. In hindsight we were too optimistic and didn't see coming many headwinds that the company would soon be facing. These included lower than expected wind resources, rapidly increasing interest rates, and challenges with their supply chain. Unfortunately the company added additional problems, including a flawed power hedging strategy. Still, while a downward price adjustment was probably warranted given those issues, we believe the market has now become overly pessimistic resulting in a very attractive share price.

There are also signs that the operating environment can get better. For example, some competitors are showing discipline in walking away from projects that are not profitable.

Capital Markets Day

Investors interested in learning more about Orsted should take a look at the Capital Markets Day presentation . It provides a good reminder of what Orsted is about, and its numerous competitive advantages. Orsted is one of the largest green electricity producers in the world, with unique offshore wind project development capabilities and scale.

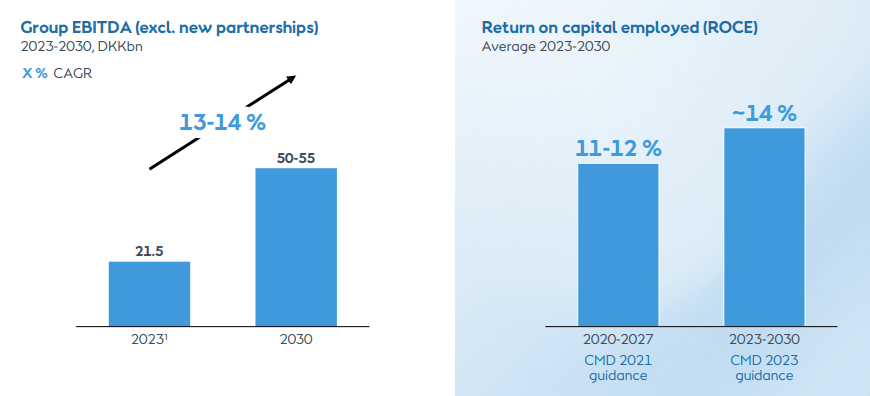

It has a massive development pipeline that undergoes strict financial hurdles to be approved in order to make sure they become value generating projects. It has an ambition to reach ~50 GW of renewable energy generation capacity by 2030. It is targeting annual operating earnings growth of 13-14% and to deliver a long-term return on capital employed (ROCE) of ~14%. It generally targets a 150 to 300 basis points spread to its weighted average cost of capital ((WACC)). During the capital markets day, the company extended its EBITDA and ROCE targets towards 2030, implying higher growth and returns compared to previous targets.

Q2 2023 Results

Orsted had a fairly negative wind impact in its Q2 results . The company delivered EBITDA of DKK 3.3 billion (~$481 million). Orsted experienced lower earnings from its combined heat and power plants, partially compensated by the offshore division. There was also some positive farm down related income.

Despite lower average wind speeds across its portfolio, the company managed to grow its offshore earnings thanks in part to the ramp-up of Greater Changhua 1 and 2a. It is worth remembering also that last year the company had a negative impact from being over hedged.

The company ended the quarter with net interest-bearing debt of DKK 43.9 billion (~$6.4 billion), an increase of DKK 8.6 billion (~$1.3 billion during the quarter). The increase in net debt is mostly the result of planned capex and acquisitions. We are not too worried about the amount of debt the company has, as it is basically just following its business plan and remains committed to maintaining an investment grade rating of BBB+/Baa1. Orsted believes no new equity needs to be raised to deliver on its business plan.

Orsted Investor Presentation

Growth

One of the things we like the most about Orsted is its massive renewables pipeline of more than 100 GW. Having so many potential projects to develop helps it stay disciplined in its bidding for new tenders, and select the most value creating opportunities.

Orsted has a fully self-funded plan to reach ~50 GW of installed renewable capacity by the year 2030.

Orsted Investor Presentation

This massive growth in energy generation capacity should, in turn, deliver higher operating earnings and returns. As can be seen below, the company believes it can more than double group EBITDA by 2030.

{kind=link}

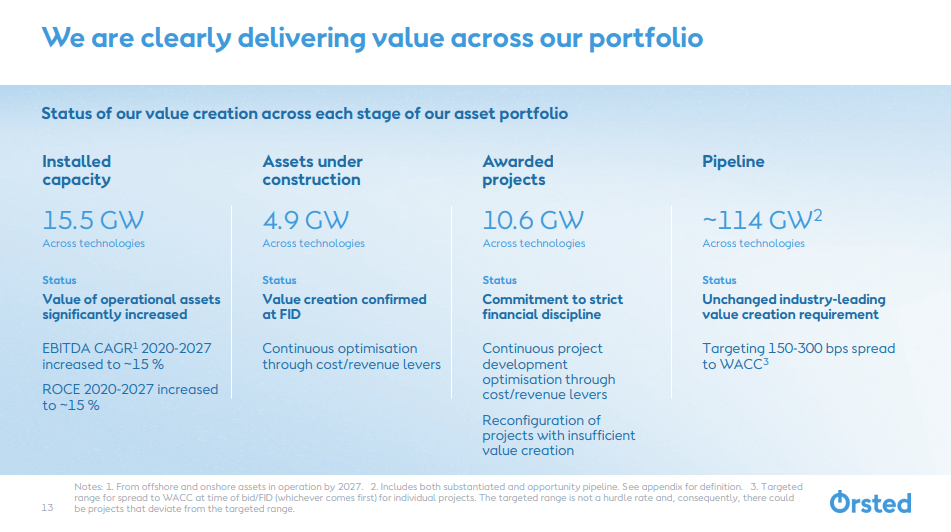

At the moment the company has roughly 15.5 GW of installed capacity, 4.9 GW of assets under construction, and close to 10.6 GW of awarded projects. With its massive pipeline of more than 100 GW, the company has a long growth runway.

{kind=link}

Competitive Advantages

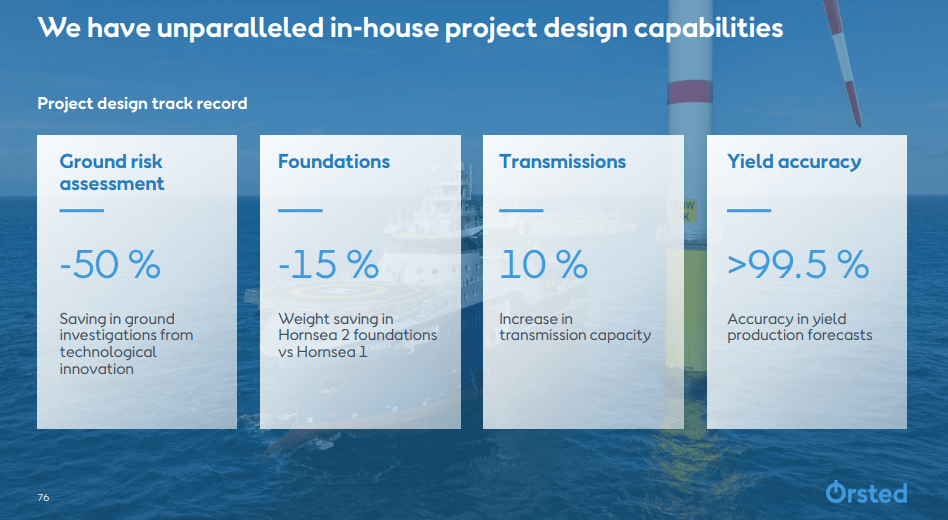

Growth by itself would not be that beneficial to investors if the company cannot generate good profit margins. And good profit margins usually require some type of competitive advantage. In Orsted's case their competitive moat comes mostly from scale and its fine-tuned in-house project design capabilities. Its scale gives it great negotiating power with suppliers and increased efficiency in many respects. Its experience designing projects in-house has created significant proprietary knowledge that results in lower costs and better estimates of project performance.

Orsted works hard to get the maximum output out of any given wind farm, achieving increased yields as they both operate and maintain their wind farms.

{kind=link}

Financial Visibility

Something we believe is under appreciated by investors is just how much visibility there is to the future financial results the company is expected to deliver in the coming years. Orsted recently boasted that ~90 % of its 2027 EBITDA is already in operation, under construction, or awarded.

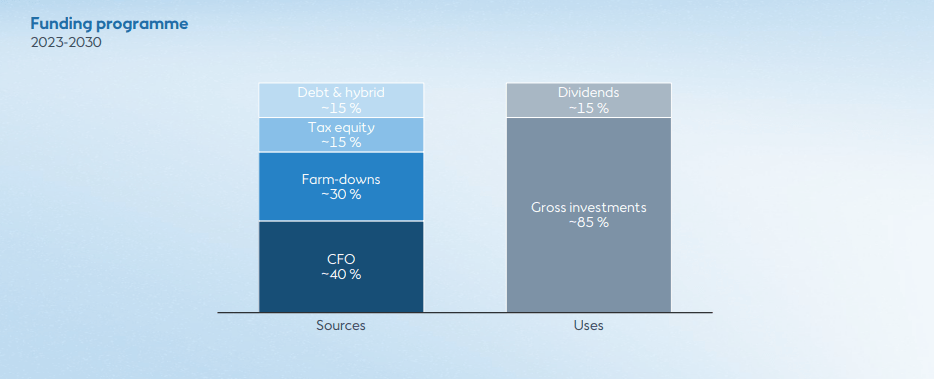

The company also has a very clear funding program for its growth capex, with most of the required capital coming from cash flow from operations, farm downs, and tax equity.

{kind=link}

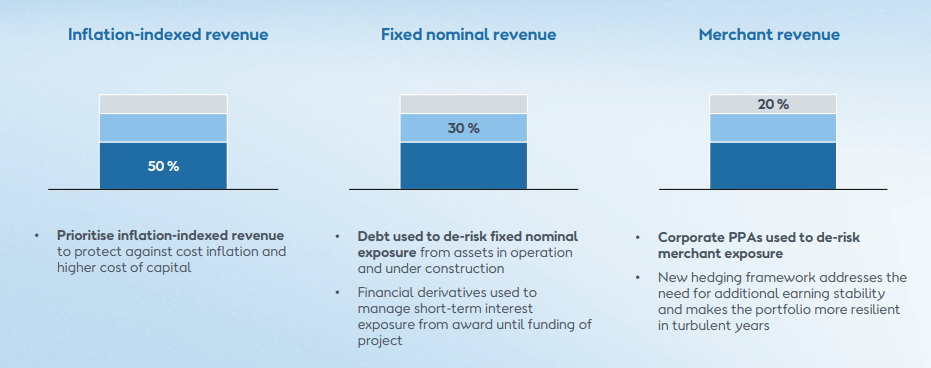

Further improving financial visibility and stability, the company has roughly half of its revenue indexed to inflation. The use of debt de-risks fixed nominal revenue exposure, while corporate PPAs are used to re-risk merchant revenue exposure.

{kind=link}

Farm downs

Investors should pay close attention to farm down transactions, as they are a critical component of the business plan. Through farm downs the company is able to recycle capital from mature and de-risked projects into new developments. They also give an idea of the value of the assets the company owns, and the value creation that is taking place.

During the Q&A session of the most recent earnings call , CFO Daniel Lerup provided interesting commentary regarding farm downs, and the current demand for the type of offshore assets that the company owns.

Yes. Thanks a lot, Mark. And yes, I very much agree it was a good transaction that we made on London Array, and it's good to see that there is a lot of demand out there for offshore assets and also at very competitive prices. We are, as always, in the market with a number of transactions and both in the U.S. and APAC and Germany, and we continue to see demand on the various assets that we are looking to farm down. When it comes to your question around the opportunistic farm down below the 50%. London Array was a good example of that. We don't have, at the moment, more like that, but we can end up in situations where it might make sense due to partner considerations to go below 50%. We saw that in the partnership that we had in Japan. There is other countries where our partners would very much like project financing, which we normally don't do where it might make sense to do further farm down. So it's very much a case-by-case assessment that we do. But the assets that we are focusing on right now is more of a classical down to 50% farm down.

Valuation

Orsted is trading with an enterprise value of ~$39 billion, and guided for full year 2023 EBITDA of DKK 20 billion (~$2.9 billion) to DKK 23 billion (~$3.3 billion). That puts the EV/EBITDA multiple at ~12.5x. Its price to cash flow is even lower at ~10.8x. We would argue these are cheap multiples for a company with the growth visibility and strong competitive position that Orsted has in the renewable energy space.

Another way to visualize the current undervaluation in the shares is looking at the EV/Revenues multiple. Historically it has averaged ~5.2x, and at current prices it is almost at half that multiple, or roughly 2.6x.

The company pays a relatively small dividend, but at current prices it is becoming significant, with shares yielding ~2.4%. The company has committed to growing the dividend by a high single-digit percentage towards 2025, and mid single-digit percentage growth from 2026 to 2030.

Risks

There are several risks investors should consider, including the fact that the weather and average wind speeds can affect financial results. The company is also exposed to often changing governmental regulation and incentives, as well as to commodity prices. Higher interest rates also make financing new projects more expensive, and stocks less attractive compared to other investment options. Still, the biggest risk we see is that of competitors behaving irrationally and bidding at prices that make value creation difficult or impossible for new developments. This risk is partially mitigated by Orsted's scale and competitive advantages that allows the company to offer competitive prices while creating value with its development of new renewable energy generation projects.

Conclusion

Orsted and renewable energy producers in general have suffered from a number of headwinds the last few years. As a result investors are a lot less enthusiastic, and valuations in the sector have come down significantly. Orsted further complicated things by making some mistakes, including a flawed hedging strategy. That said, there are signs that things are improving, competitors becoming more rational when bidding, and several governments making good on their promise to support more green energy generation. With its massive pipeline, competitive advantages, and excellent growth visibility, we believe Orsted deserves a higher valuation. As a result, we are upgrading our rating to 'Strong Buy', as we believe shares to be significantly undervalued.

For further details see:

Ørsted's Undervaluation: A Compelling Opportunity Despite Some Setbacks