DNNGY - Ørsted: Solid Renewables Company Undervalued With Strong Pipeline

2023-06-12 21:40:19 ET

Summary

- Ørsted is a solid renewables company and a market leader in the wind energy sector, with a well-filled pipeline and conservative financing.

- The company is currently undervalued, making it a good time to buy shares or write options, but investors should be cautious of its volatility and meager dividend yield.

- The long-term growth potential of Ørsted is attractive, but investors should be patient and focus on capital gains and dividends over time.

Dear readers/followers,

I've been covering Ørsted ( DNNGY ) (DOGEF) for about a year at this point, usually holding a fairly positive stance on the company. Overall, this has been a successful stance to have, and my small common share position is a plus. Mostly, I'm using the native Ørsted ticker to play the options game for the company. This means that I'm selling 30-45 day expiration put options with the lowest possible strike price I can find that allows me a 5-12% RoR, and I try to do this during days when the company's share price is down - such days lend themselves to obviously getting some higher premiums for those options.

From that perspective, the returns you see below are only for the common - my option returns annualized for this business for the year are actually higher.

Seeking Alpha Article (Seeking Alpha)

I thought this would be a good time to look closer at some of the trends we've been seeing to perhaps buy more of the common share - or write some more options.

Let's take a look at what we have here.

Ørsted - still a lot to like, but the market is uncertain short-term

When I invest, I usually talk about short-term relative to long-term investments. I most often only go for the longer-term ones. Regardless if you consider Ørsted a long-term or a short-term investment, it's good to know the facts about the company, meaning that you're investing in a world-leading renewables company. This alone is attractive to some investors.

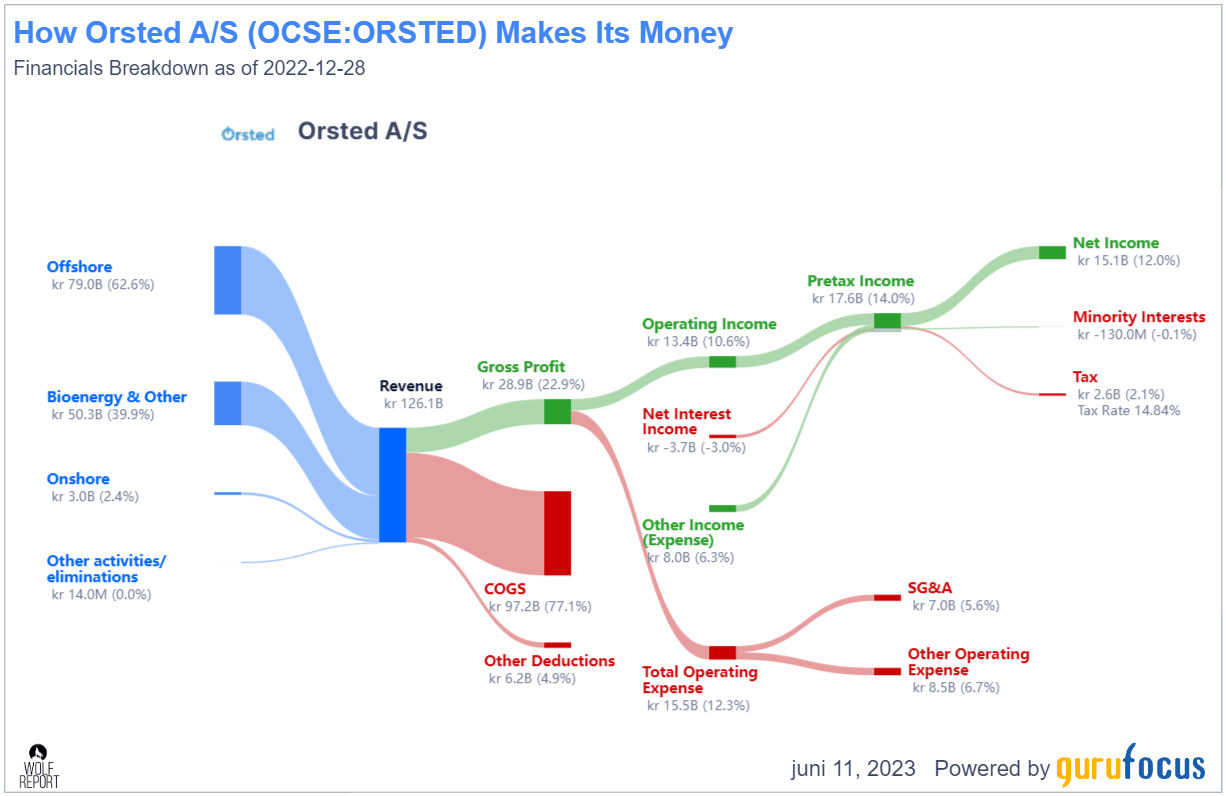

It's also fairly easy to understand why many investors consider Ørsted to be an attractive business. The company's margins are solid, their growth rate - current challenges notwithstanding - is superb, and they have some very attractive fundamentals overall. Profitability is good if somewhat impacted by current trends. The company has a comparatively high COGS, but it also provides some of the most innovative solutions on earth, being the global leader in offshore wind farms, top 10 onshore, and a global leader in renewable fuels of various kinds. This is a big change from what the company "used to" be, which was predominantly legacy-focused and Danish oil business.

Orsted revenue/net (GuruFocus)

{kind=link}

The majority shareholding by the Danish government is something I view as fairly positive, altogether (50.1% of votes). Dividends will likely never be high or grow massively because the focus of this business is to retain low debt while growing its already-sizeable portfolio.

So know this going in - you won't get a lot of dividends, and that's unlikely to change at any time in the future. A suitable investor in this company, as I see it, is someone with the patience of letting this business run through thick and thin, developing its world-leading portfolio of renewable assets.

The last few years have been challenging for the company. While revenue has been hitting the roof, especially in 2022, the company has seen difficulties in translating this to net profit, and debt has been going up since about 2019. Many investors often ask why a company goes this way or that way in terms of share price.

Sometimes it's based on irrational fears regarding a singular event, but most often, there is actually some fundamental reason to it. With Ørsted, I would simply answer such a question with the fact that the company's debt, coupled with top-line growth but not corresponding bottom line growth, coupled with lower profitability in terms of new investments due to a mix of higher NIC (Net interest costs) due to higher debt, inflation, and other cost increases.

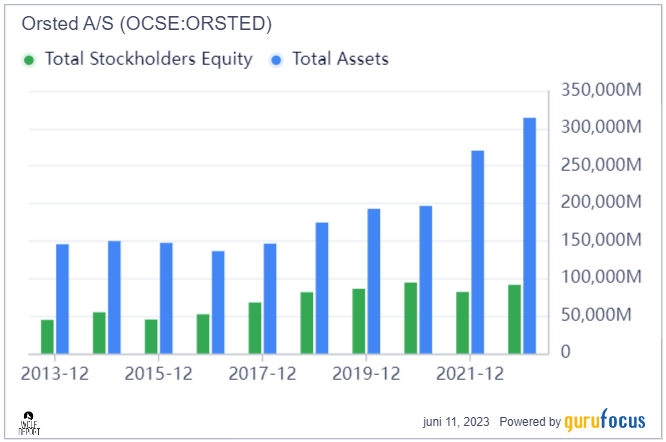

That makes it a not-so-strange trend to see here, that the company is actually declining. Shareholder equity as a percentage of assets has been declining for several years now, and currently looks like this.

{kind=link}

Very basic trends, as you can see. The company fairly recently revised its growth estimates, and as a result of this, the share price level has been crashing for about 5-6 months at this point from overvalued highs of close to 1300-1400 DKK. Today, you can pick up the company for 660 DKK native, and I've written options as low as 530-540 DKK, and profited off them.

There's plenty to like about the company at prices that low, provided you hold any sort of conviction in the long-term growth of the company.

1Q23 is in, and some positives can be noted. The company delivered high earnings in several offshore sites, with final investment decisions on several projects, as well as new submissions for projects being finished, one of them a large 884 MW farm in Rhode Island with the JV, Eversource.

New awards for contracts were also confirmed. The company was awarded 100 MW floating wind leases for the Scottish Salamander Projects, and a purchase agreement with Google regarding an onshore project in the USA. The company also acquired 160 MW worth of solar in Ireland, and the first submission of a bid to the Danish Energy Agency for carbon capture and Kalundborg hub has been submitted. When you're a company with a majority shareholder stake from the government, I would say that it's fair to say you have a bit of an advantage in public tenders and bidding.

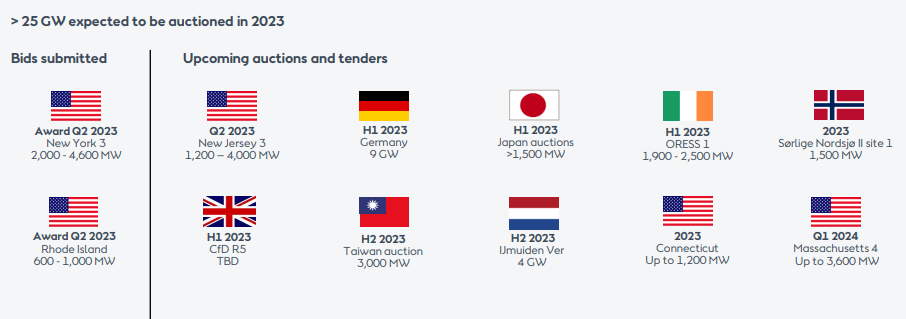

The annual tendering for offshore wind is accelerating, which is a net positive for the company.

{kind=link}

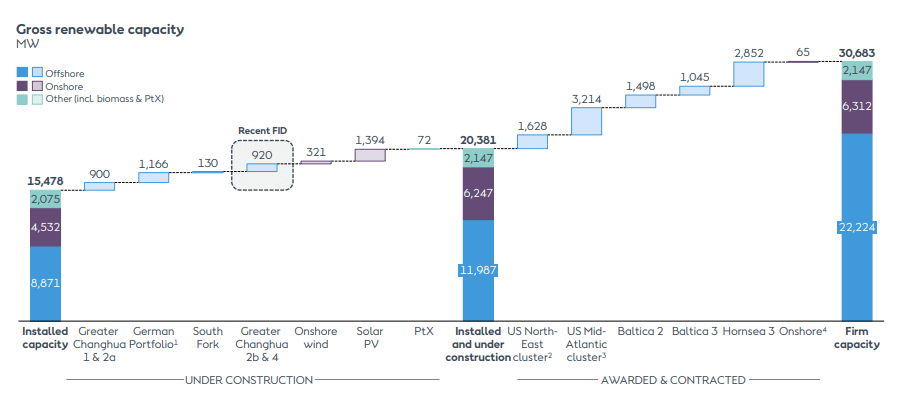

And its current construction pipeline is impressive.

{kind=link}

However, top-line volume growth is only one part of the equation, and the bottom line isn't improving all that much even as of the latest quarter. Net profit is down - significantly, with lower EBITDA and higher depreciation from assets, as well as increased expenses due to chronically unfavorable FX. ROCE is down almost 6% due to lower pre-tax earnings, and higher amount of employed capital, and the company has massively impacted its own estimates for ROCE, from 19% in 2022, to between 11-12% on a forward average basis until 2027. All of this dictates how we should, or shouldn't value this company.

Equity stands strong. The company has equity of well over 100B DK, and hedge costs/reserves are down, at the very least, due to lower forward power prices and hedge run-offs.

Debt is so-so. It's low, but the company also hasn't been cutting or reducing it. The company's adjusted debt numbers are at 38% in terms of FFO/net debt on an adjusted basis, and net-interest bearing debt of 35.3B DKK with a naturally rising interest cost as these debts are refinanced and mature.

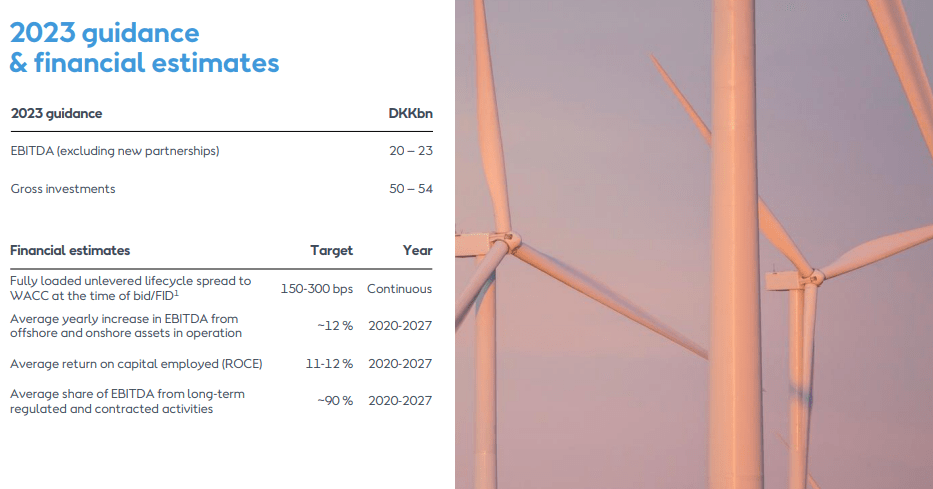

Guidance is...so-so.

{kind=link}

It's not great, but it's also somewhat better than I expected. Part of my bearish thesis involved ROCE trending close to 10%, and it doesn't. EBITDA isn't great, and gross investments are a bit higher than expected, but it's all within the framework of my forecasts, which I used to set my previous price targets for this company.

It means that all things considered, those targets are still relevant.

Let's look at the company valuation and forecasts, and see where this puts us.

Ørsted - The valuation is good, but don't expect wonders from this company

The company has been through a quite ridiculous analyst price target adjustment over the past 18 months, which really illustrates just how broken these targets and estimates can sometimes be, as well as how short-term some of these analysts tend to target their own assumptions.

At one point, the highest analyst target for the company was 1,500 DKK - that was less than 2 years ago. Now the highest target is 975 DKK. It's not that the company is suddenly worth 30% less, is that these analysts have grandiose expectations based on unrealistic perspectives on macro as well as the stock market as a whole - or the company.

When the company traded at over 1000 DKK I treated it like a hot potato. Now though, when it's trading below 700 DKK, that's a different story altogether.

The average PT at this time is around 740 DKK. If you follow my articles, you'll know that this is a target that I can get on board with. The range at this time goes from 475 DKK to 975 DKK, with 24 analysts following the business. Out of those 24, 15 are at a "BUY" or equivalent. I mostly agree with this as well, and the picture this implies.

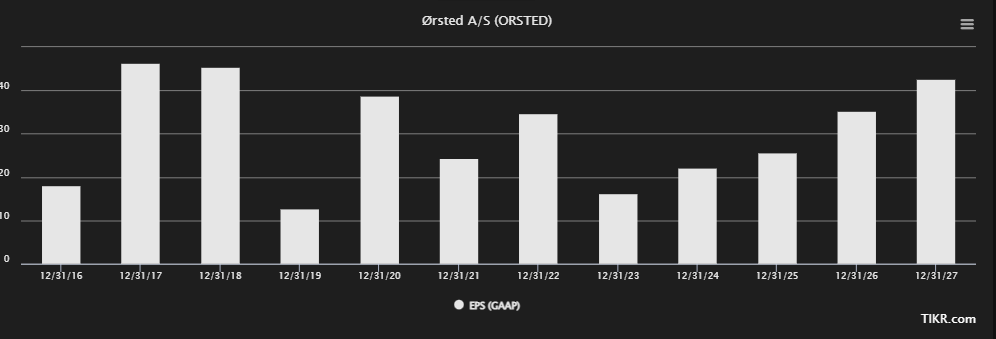

I do want to tell you though, that I don't see a quick or immediate ramp-up in the company's bottom line. That means that the trend being forecasted here by S&P Global in terms of GAAP EPS...

Orsted EPS forecast (TIKR.com)

{kind=link}

...i consider that to be far too positive/exuberant. If you take even just a glance at the historicals, you'll realize that profits bounce up and down like a JoJo. For them to suddenly go a nice, smooth stair-stepping positive trend, that would require macro stability including inflation, FX and other concerns, which I do not currently see - not even close, as a matter of fact.

So I would take these estimates with more than a spoonful of salt. Expect continued volatility. But at the price you're paying here, you're getting the company at a decent valuation. Some would even say that the valuation is great, and the company is massively undervalued. Some valuation models that include earning power, NAV, tangibles, and projections as well as including Graham numbers put the company's value on a per-share basis at almost 1,700 DKK (Source: GuruFocus). However, I view such estimates as way too exuberant, and in this case, "mechanized" in a way that this company doesn't lend itself well to.

You really need to understand how volatile this business can sometimes be. The same thing is true for a company like Yara (YARIY). For years, the company was treated like dirt, trading at below 200 NOK. That was when I started buying, recognizing the quality of the assets and the potential when the cycle changes. Now I've harvested Yara dividends for years, and I'm at a 130%+ RoR and profit, with over 24% of my profit in my position in received dividends.

This company, while lacking dividend potential, should be approached the same way. Now is the time to add to this business, not when the company spikes at over 1400 per share - as some analysts actually were beating the drum for.

I still have some nice options running for this company, and I may write more. I'll wait until 2Q to see if I add more common shares, but this makes the thesis for the company as follows.

Thesis

- Ørsted is a solid renewables company and one of the relevant market leaders in the entire segment. It is, in fact, a market leader in Wind. It's also state-owned, has a well-filled pipeline, and is one of the most conservative financing pipelines and maturities when it comes to utilities. This makes it a class-A business.

- However, a meager yield and premiums make valuation important - and I would only buy the company as long as it stays within its range. At current numbers, I would not buy it above 800 DKK per share.

- That means that as of right now, Ørsted is a "BUY" for me.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company does still fulfill all of my criteria, and that makes it a positive "BUY".

For further details see:

Ørsted: Solid Renewables Company, Undervalued With Strong Pipeline