DNNGY - Ørsted: The Impairment Overhang

2023-11-21 15:10:55 ET

Summary

- Ørsted's stock has dropped by 25% since late August and even more year-to-date due to high impairment charges and weakening financials.

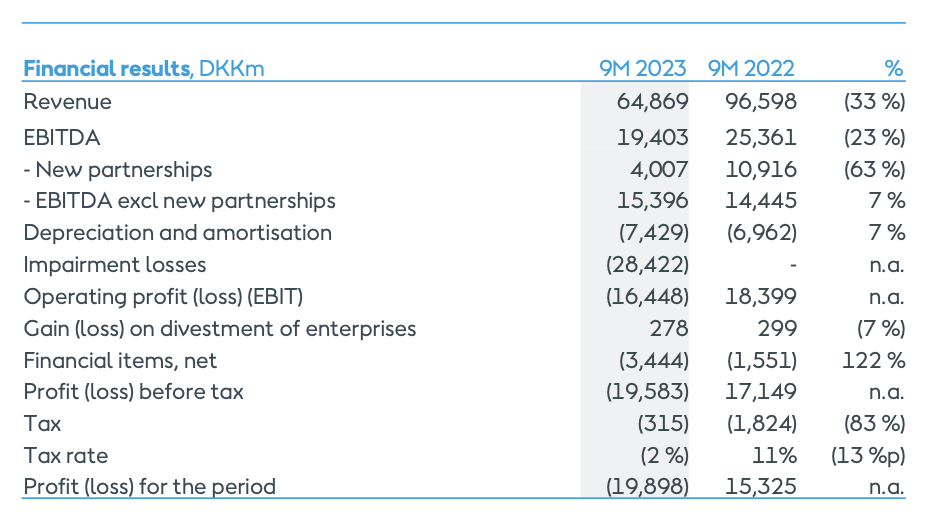

- The company reported a net loss of DKK19.9 billion for the first nine months of 2023, compared to a DKK15.3 billion profit in the same period last year.

- While Ørsted's market multiples look attractive now, the recent developments are unsettling and its likely losses in 2023 could further impact the price, not to mention its dividends.

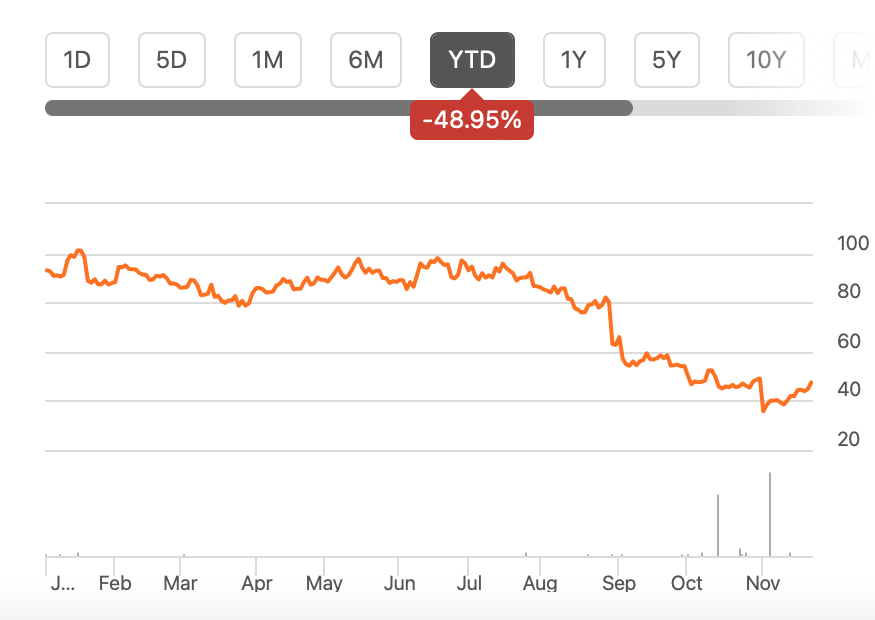

The Danish wind energy company Ørsted ( DOGEF ) has dropped by 25% since I last wrote about it in late August, and even more so year-to-date (YTD) (see chart below). Even at the time, there were signs of weakness. Its revenues had declined by 24% year-on-year (YoY) in the first half of the year (H1 2023) because of slowing energy prices.

{kind=link}

Its preferred profit measure, EBITDA, and net profits also declined for the same reason by 22% and 55%, respectively. Its forward price-to-earnings (P/E) ratio at 28.9x, based on my net profit estimates, also looked elevated compared to peers, prompting a downgrade to a hold rating on Ørsted.

Why Did The Price Drop So Much?

Even the then-elevated valuations don't justify the extent of the price drop experienced since. It is actually explained by big impairment charges that have also impacted the company's results, both of which are discussed in greater detail below.

Warning on impairments

My last article was published just before the company revealed that it risks high impairments on account of setbacks to three of its wind projects in the US. At the time, the estimated impairment amount was a total of DKK16 billion for three reasons:

- Delays at suppliers' ends meant that the schedule couldn't be upheld. This, in turn, meant delayed revenues and increased costs, with estimated impairments of DKK5 billion.

- It also mentioned the risk that two of the projects might not qualify for income tax credit ((ITC)), which would amount to another DKK6 billion in impairments.

- Elevated interest rates were estimated to result in DKK5 billion more impairments.

For context, these expected impairments were a shade higher than the net profits for the full-year 2022. Expectedly, when the news came in, the stock fell by 21.3%.

Losses reported for 9M 2023

The impact of the increased impairments was due to be recognised in its update for the first nine months of the year (9M 2023). When the numbers came in at the end of October, the stock saw another fall, and a bigger one this time, of 27.1%.

At first glance, it's puzzling, considering that the impact should already have been factored into DOGEF's price by the time. Except there were "further negative developments," as Ørsted puts it, with higher impairment charges now of DKK28.4 billion and ceasing in the development of two of its US projects. This impairment amount is 77.5% higher than the company's initial estimates.

Ørsted

This, of course, had an impact on the company's financials, as it fell into an operating loss, resulting in a negative return on capital employed (ROCE) of 13.7% for 9M 2023 from a positive 17% for H1 2023.

It also reported a net loss of DKK19.9 billion for the period (see table below), compared to a DKK15.3 billion profit for 9M 2022. If it weren't for the impairment cost of DKK28.4 billion, the company would have instead reported a DKK8.5 billion profit.

{kind=link}

It does need to be noted that the profit ex-impairments would have still been lower by 44.5% year-on-year (YoY) on account of a decline in revenues by 33%. The revenue contraction was a continuation from the first half (H1 2023) when they fell by 24% on falling energy prices but at an accelerated rate of 48% in the third quarter (Q3 2023). As a result, the net profit had already declined by 55% in H1 2023.

The Outlook

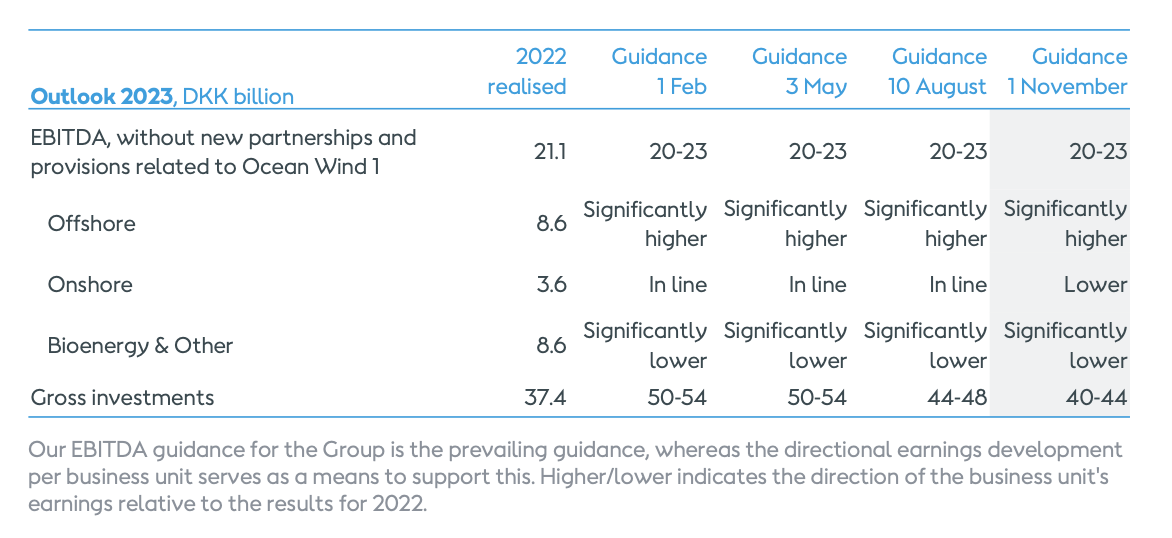

Ørsted has now decided to cease any further development in the Ocean Wind 1 and Ocean Wind 2 projects, both in the US. As a result, it has reduced its gross investments outlook to DKK40-44 billion for 2023 compared with DKK44-48 billion earlier.

It does need to be noted that even this previous guidance was lower than the DKK50-54 billion the company had expected at the start of the year (see table below), though, at that time, it mentioned it was only a matter of timing.

{kind=link}

Interestingly, however, the company's EBITDA outlook remains unchanged, as the impairment charge is a non-recurring expense. This then means that it expects EBITDA ex-new partnerships to come in at DKK20-23 billion, as earlier.

The Market Multiples

With the company likely to remain in a loss for the full-year 2023 now, the relevant market multiple for it now is EV/EBITDA. To get the forward multiple, I've made two estimates.

The first estimate assumes that the EBITDA from new partnerships stays static at that for 9M 2023, and the EBITDA ex-new partnerships comes in at the midpoint of the target range provided by Ørsted. This results in a total EBITDA of DKK25.5 billion and a forward EV/EBITDA for 2023 at 6.9x.

The second estimate assumes that the EBITDA from new partnerships for 2023 comes in at 26% of the full-year EBITDA ex-partnerships. This is the same proportion as seen for 9M 2023. The EBITDA ex-new partnerships is once again assumed to come in at the midpoint of the range provided. This results in a total EBITDA of DKK27.1 billion and a forward EV/EBITDA of 6.5x.

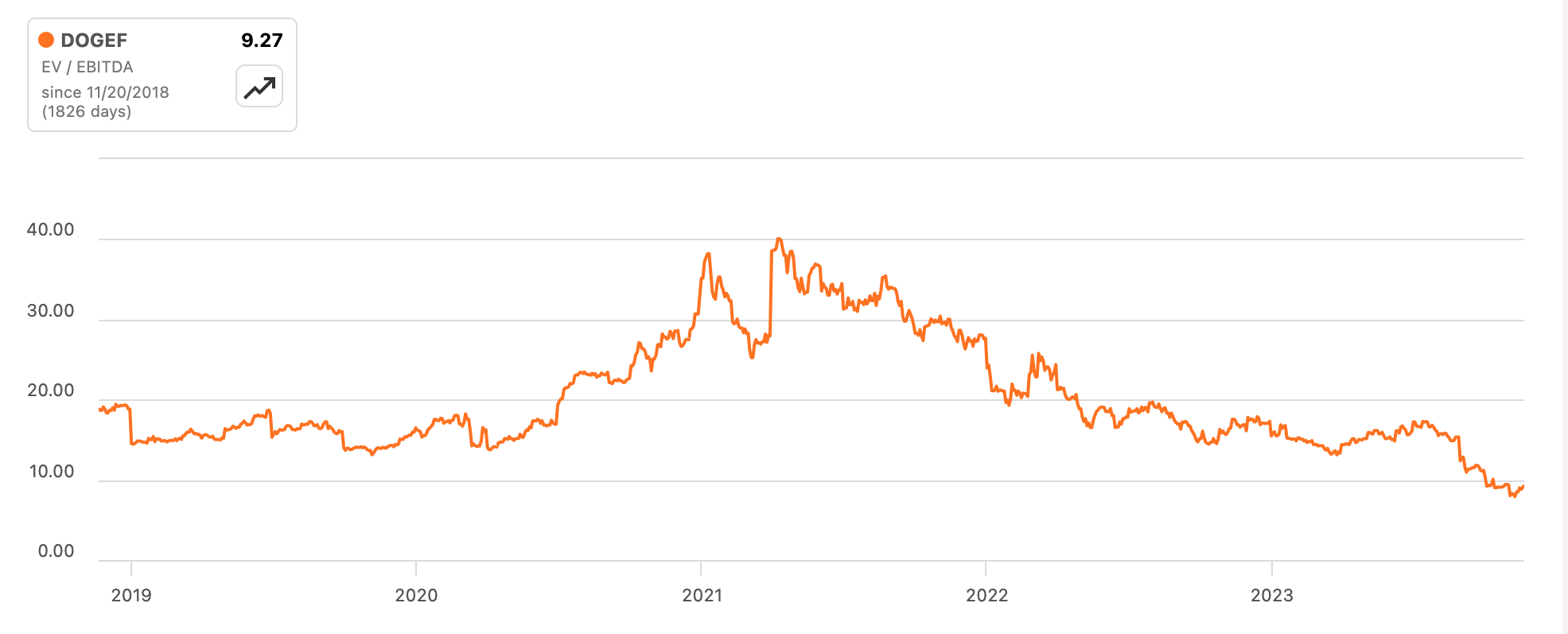

Both the forward EV/EBITDA estimates are lower than both the five-year average for DOGEF at 15.4x and the trailing twelve months ((TTM)) EV/EBITDA at 9.27x. Further, the TTM EV/EBITDA itself is at five-year lows (see chart below).

{kind=link}

What Next?

The market multiples indicate that there's indeed an upside to DOGEF for now. Its TTM dividend yield of 4% certainly makes it more attractive. However, for now, I'd hold back from buying it. Firstly, because of its likely losses in the foreseeable future. Next, a net loss can affect its dividend payouts and its price further.

Also, the recent developments on impairments for the US projects are unsettling. I'd wait for at least another quarter's update before taking a call on Ørsted for two reasons. First, to avoid being impacted by a further price fall if any other nasty surprises come up. And second, to assess what the company's outlook for 2024 is when it announces its full-year results in February next year. I'm retaining a hold rating.

For further details see:

Ørsted: The Impairment Overhang