PRGO - 2 Fast Dividend Growers With Strong Outlooks

2023-10-25 14:46:39 ET

Summary

- Broadcom Inc. and Perrigo Company plc are two companies providing impressive dividend growth to their shareholders.

- Perrigo Company is a smaller pharmaceutical company focusing on over-the-counter healthcare products, while Broadcom is a semiconductor behemoth with a software business segment set to grow.

- Both are expecting attractive growth going forward, which could further support even more dividend growth and possibly capital appreciation in the future.

Written by Nick Ackerman.

Last month, we highlighted Primerica ( PRI ) and Comfort Systems USA ( FIX ) as two names worth investor attention. The focus was to look at faster-growing companies that have been rewarding investors through rapidly but sustainably growing dividends. These companies had positive outlooks that suggested they could keep up a healthy pace of growth as well.

Today, I wanted to carry on that mission of looking for more growthier opportunities. Names that could be added to today or to build up the watchlist for the next bear market or recession that inevitably creates buying opportunities.

I'll be using the same parameters as last time. That is, names that have grown their dividends by at least 10% for the last five years while growing their dividends for at least 10 consecutive years.

Broadcom Inc. ( AVGO )

I'm starting the list off with a familiar name, one that's actually already on my watchlist from earlier this year, but I never took the plunge to buy in. I certainly regret that, as the share price was trading around $600 when I first gave this name a look.

With a market cap of over $354 billion, there probably aren't too many people who aren't familiar with this company. That being said, Broadcom, for those who may not know, is a mostly semiconductor company at the moment.

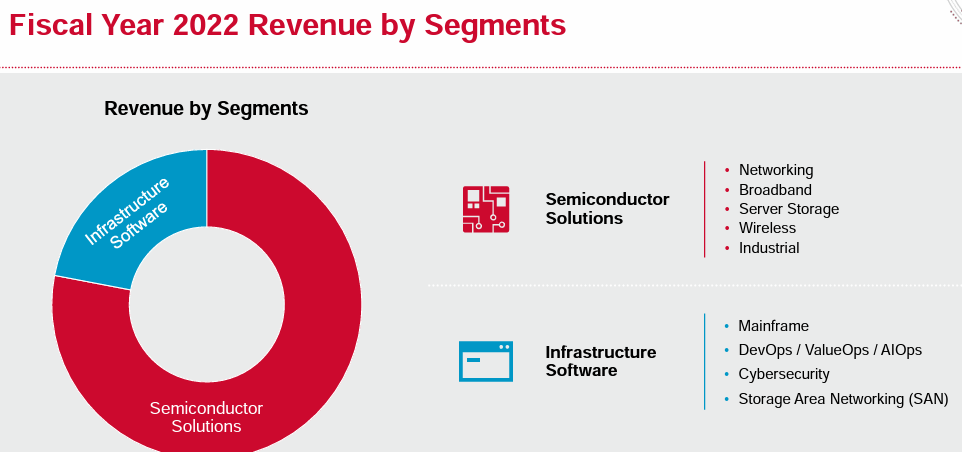

That being said, they also have a software component to their business, and they are looking to increase that with the acquisition of VMware (VMW). Here is a look at the 2022 revenue by each segment.

{kind=link}

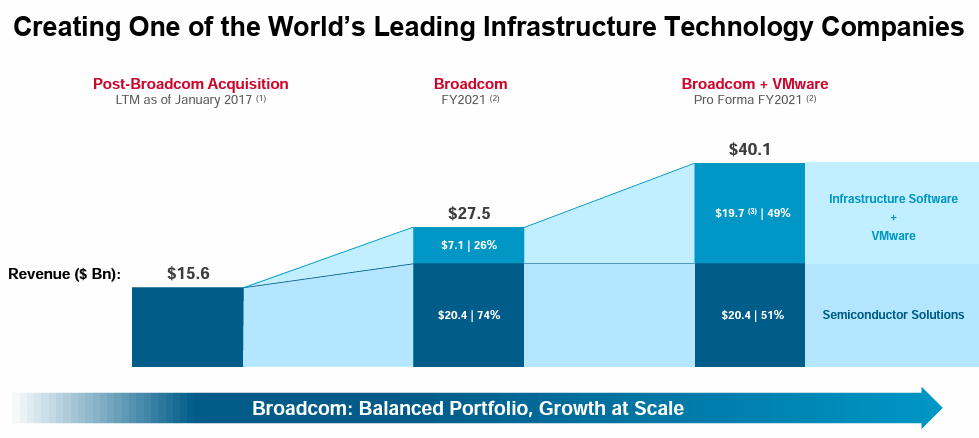

With that acquisition, they see these two segments being roughly 50/50 in terms of revenue , as VMware is a large company on its own as well. Here is a look at the hypothetically combined company in 2021.

{kind=link}

Of course, like any large acquisition, it has been quite the process of getting regulatory approval from around the globe. The latest news is that China is now reviewing the deal, but it is expected to approve it "without major changes."

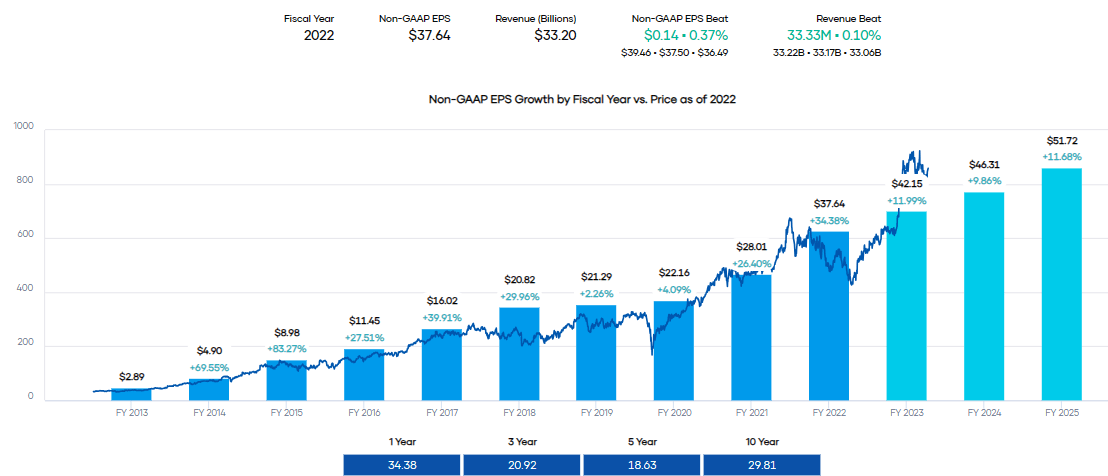

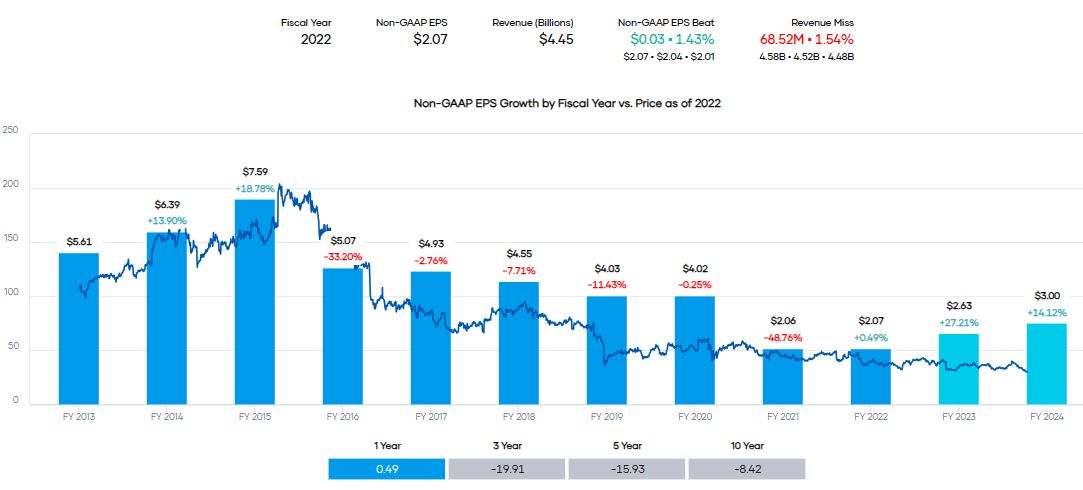

AVGO has been able to see its earnings explode higher and is expecting growth going forward. If the company hits analysts' estimates, we are looking at an annualized growth of just over 11% in the next three years.

{kind=link}

With 15 out of the last 16 quarters topping analysts' estimates on an EPS basis, the surprise has generally been to the upside, which bodes well. The revenue beats have been just as impressive, with the same upside surprises historically of 15 of the last 16.

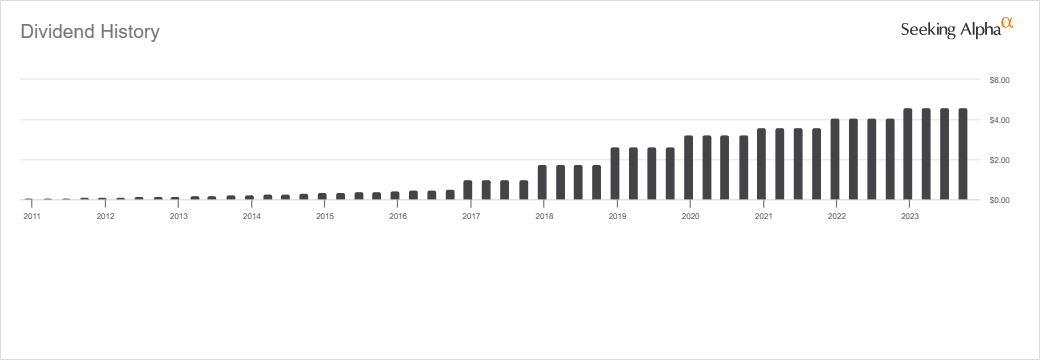

That sort of earnings trajectory has allowed AVGO the cash to reward shareholders handsomely, and that's what they've been doing with a rapidly growing dividend. The pace of that growth has slowed down to a more sustainable level, but it is still expected to be quite attractive going forward. The growth has still also outpaced their sector peers in the semiconductor space by a significant margin.

AVGO Dividend Growth Grade (Seeking Alpha)

In total, they've been growing their dividend for 12 years, which is as long as when they started to pay a dividend in the first place.

{kind=link}

The EPS payout ratio is healthy at around 44% based on forward estimates. With a similar FCF/share of $41.75 based on the $18.40 dividend, we also see a healthy free cash flow ("FCF") payout ratio of around 44% as well.

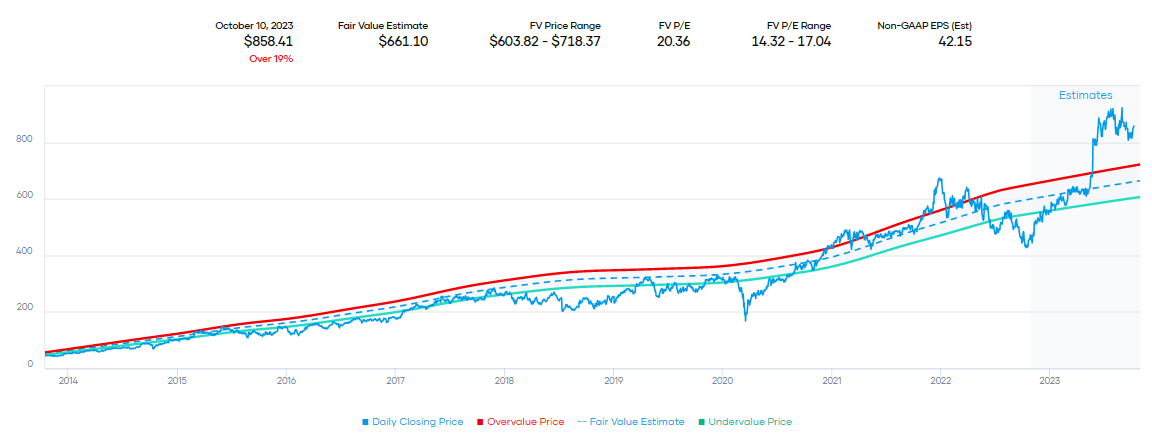

All that being said, while it was cheap earlier this year, the stock's explosion higher is likely to keep it on the watchlist for me until we get some increased volatility and the price comes down. The price is trading well above its historical P/E multiple, and that could suggest some downside going forward.

{kind=link}

While they are anticipated for some fairly quick growth going forward, the forward PEG ratio is a bit high, too, at 1.71. That further suggests that even based on expected growth going forward, we are looking at a bit of a pricey stock. However, the argument could be made that AVGO is more or less in line with the broader S&P 500 Index (SP500) - which the tech sector often trades above. So I can understand the argument for just adding to it today and dollar-cost averaging in overtime or averaging down in the next inevitable market crash.

Perrigo Company plc ( PRGO )

PRGO is a much smaller company relative to AVGO and would fall in the mid-cap category with around a $4.1 billion market cap. Similar to PRI and FIX, and that's generally where you can find more growth potential - but it also comes with more uncertainty as smaller companies tend to be more volatile relative to their large-cap peers.

That being said, PRGO is an interesting name nonetheless, even as a more speculative name. The company is headquartered in Ireland but has business around the globe. They are a "global consumer-focused self-care company" falling within the pharmaceuticals industry. However, they focus on over-the-counter healthcare products. They sold off their prescription pharma business in 2021.

That can help explain why we saw a significant drop in earnings during that year, as that was a sizeable portion of their business. However, they appeared to be struggling even before that as well.

{kind=link}

The company itself was up for speculation that it was going to be acquired at one point , and Mylan (now Viatris ( VTRS ) after merging with Upjohn) had attempted to acquire PRGO before that. Outside of that, there have been a number of acquisitions that PRGO has been involved with over the years. So, we have a lot of moving parts and history for this company.

That being said, one thing that has been maintained has been the dividend for going on 19 years of consecutive increases .

{kind=link}

This growth has mostly outpaced peers, and it remains at fairly healthy levels, especially if the company can deliver the anticipated growth going forward. That's always a big if, but it's always the question of where things are moving forward rather than simply where they've come from in the past.

PRGO Dividend Growth Grade (Seeking Alpha)

The EPS payout ratio comes in at 44.60% based on next year's estimated earnings. Based on FCF, the payout ratio comes to around 58%. However, FCF has been trending higher over the last couple of years. Similar to the same trajectory of the EPS, they saw this decline significantly after the spin and had a general trend of seeing lower FCF/share.

Earnings are anticipated to grow at nearly 18% on average for the next three years, with most of that growth coming in the current fiscal year. In this case, PRGO has been more of a mixed bag when it comes to earnings surprises . It is split 50/50, with 8 of the last 16 quarters showing they missed estimates and leaving 8 quarters where they exceeded.

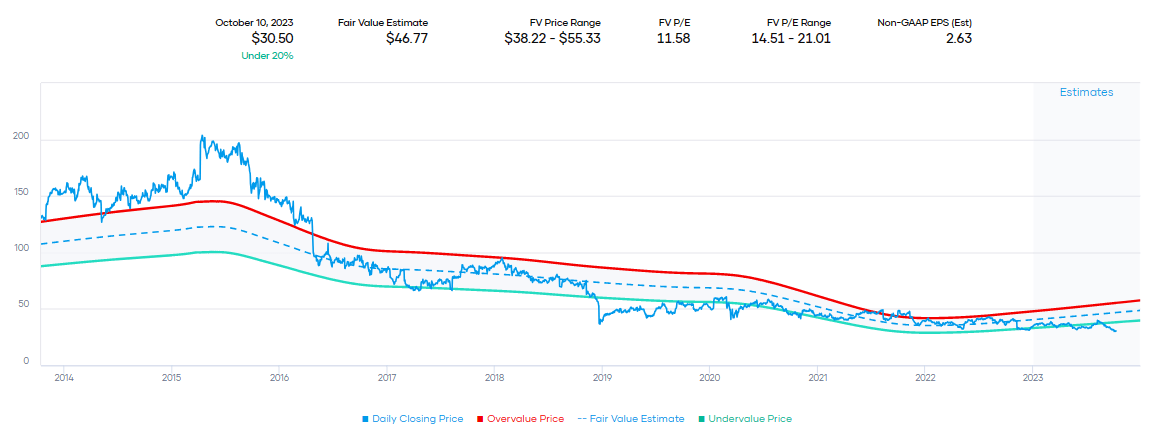

I believe that the valuation reflects a fairly pessimistic outlook. The stock is trading below its estimated fair value range.

{kind=link}

This suggests that there could be some potential upside with not only earnings growth on the horizon (if they can return to growth) but also some multiple expansions. If they are able to get back on the growth train, which is admittedly shaky historically, that could get some investors' attention to start pushing it higher.

For all these reasons, I'd be a bit more cautious about the optimistic outlook for Perrigo Company, but it still creates a situation where the dividend is well covered. Additionally, even if they miss by half, we are still talking about some decent growth.

For further details see:

2 Fast Dividend Growers With Strong Outlooks