SLRC - 2 Magnificent +9% Yields You Don't Want To Miss

2023-11-29 07:35:00 ET

Summary

- Business development companies are earning massive revenue today, and the future continues to look bright.

- The best time to buy is when others are selling or hesitant.

- Don't miss opportunities because of irrational worries. Dig deeper.

Co-authored by Treading Softly.

Most of us can remember various aspects of 2020 or the COVID pandemic that radically altered how we lived. 2019 was a very normal standard year. 2020 through 2022 felt like an entirely different world. Moving into 2023 and the tail end of 2022, things started to normalize again across most of the country and across most of the globe. At times, I'll talk to my family or my friends about different things that we experienced during the COVID pandemic, and it feels like I'm almost talking about a completely different lifetime. I can only imagine when I teach my children about that period of time, which, many of them were too young to be able to remember, how weird it will sound to them and how unusual they will consider it.

When it comes to the market, many investors experienced a great deal of panic and consternation, watching the market swing wildly as investors tried to grapple with the new reality of this pandemic. Yet our long-term members look back and reminisce about how they wish they had more money or bought more of the opportunities that were presented, but that they missed them either because they ran out of cash investing in so many other opportunities or because they were too afraid. Some of our newer members, who were not part of our community at the time, will talk about how they wish they had been and were able to enjoy some of the great yields that we were able to lock in and still enjoy the great dividends from them to this day.

While I hope we never have to deal with another pandemic, I do remind investors that there will always be another drop on the horizon to be able to take advantage of. Those who learn to embrace our Income Method and use it to their advantage will be the ones who are able to buy massive yields and lock in those income streams for decades to come. I'm a net buyer of the market. I don't try to time it. I don't try to game it. I buy it, and it pays me to do so.

Today I want to look at two outstanding opportunities that I think are well worth buying and if you don't, you may very well look back at them in the future and wish you had bought them.

Let's dive in!

Pick #1: SLRC – Yield 10.9%

Let's face reality: when you are seeking a high current income, you are looking at stocks that aren't currently in favor with the market. They are often stocks that are unpopular for one reason or another. Yields get high because prices are low. Investing for above-average yields often means identifying opportunities that others in the market is avoiding. One common reason a dividend stock might be trading at a low price is that the market fears a dividend cut. If a dividend isn't covered by cash flow, the price will usually decline and it will trade at an above-average yield.

This was the case with SLR Investment Corp. ( SLRC ), which was failing to cover its dividend after COVID. The "problem" that SLRC had was its leverage was too low and it took time to deploy capital and leverage back up. As a result, the dividend was not covered by net investment income.

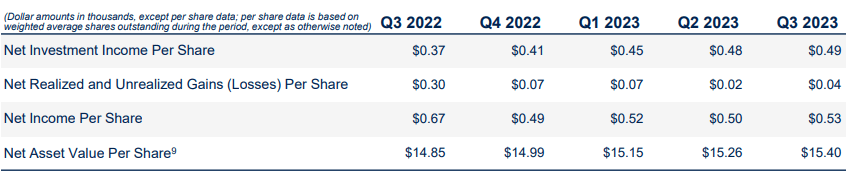

In Q1 of 2022, SLRC's NII (net investment income) was only $0.32. It was falling well short of its dividend. By Q1 of 2023, NII had risen to $0.41, just barely covering the dividend. For Q2, SLRC had an NII of $0.42, covering the dividend with a little room to spare. In Q3 SLRC reported NII of $0.43, adding a little more cushion for the dividend. Management laid out a clear plan, and they are executing it. The trend is definitely in the right direction and leverage is up to 1.21x debt/equity.

Since NII is now covering the dividend, SLRC saw its book value tick up to $18.06, up from $17.98 the prior quarter.

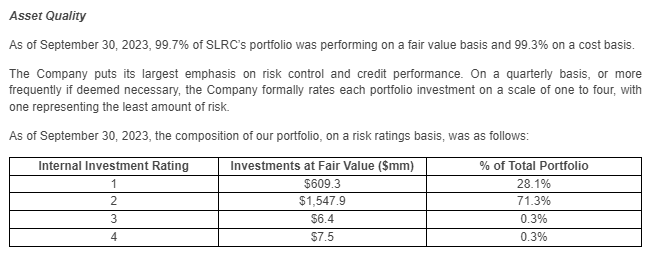

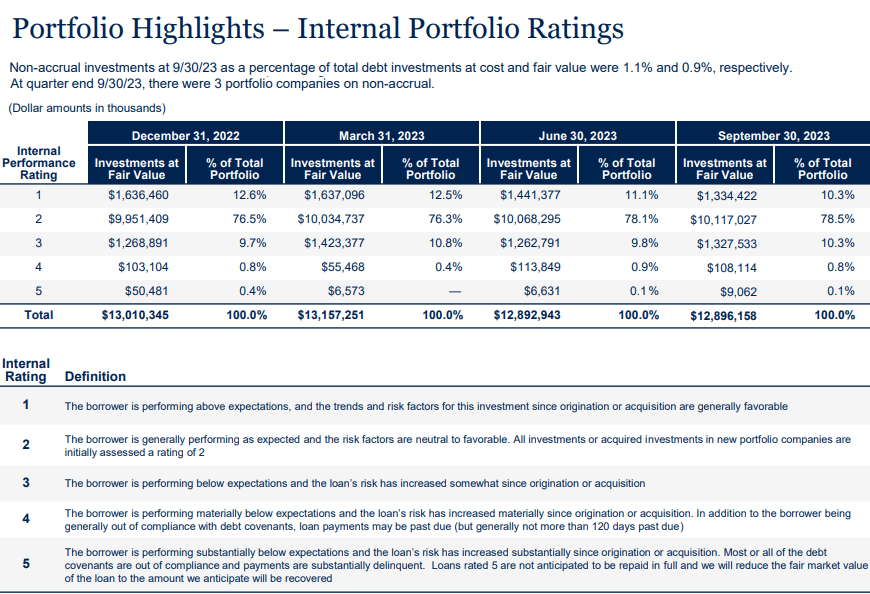

SLRC's asset quality has consistently been strong. Their preference for making loans that are secured by assets and physical equipment has led to low levels of defaults and high recoveries. 99.7% of SLRC's portfolio is currently performing, with 99.4% of the portfolio in the two highest investment ratings. Source .

{kind=link}

SLRC had a stated goal, and they have achieved it. The dividend is now covered with a comfortable cushion and book value is rising. The share price is still trading at a 15%+ discount to book value, and we are happy to add more shares before the market realizes how much SLRC has improved.

Pick #2: OBDC – Yield 9.4%

Blue Owl Capital Corporation ( OBDC ) is a BDC (Business Development Company) that was failing to cover its distribution when we first bought it. Fast forward a few years later and OBDC achieved dividend coverage, then started increasing its dividend, then started paying a supplement, and today is increasing both its regular dividend and its supplement!

The "regular" dividend, which is what management believes is sustainable even if interest rates decline and business slows down, was raised from $0.33 to $0.35 (ex-dividend Dec. 28). The supplemental dividend, which is designed to reflect the current beneficial interest rate environment for the business, was increased from $0.07 to $0.08 (ex-dividend Nov. 29). We expect that supplement will decline when interest rates decline, but we are happy to collect it in the meantime!

Despite all of OBDC's dividend raises, net investment income continues to exceed the dividends paid. In Q3, OBDC had $0.49 in NII, covering the new dividend and the supplement by 113%. We love it when a company "struggles" to raise its dividend faster than earnings are rising!

At 1.13x debt to equity, OBDC is operating with a modest amount of leverage and well within its target range of 0.90x-1.25x.

Over the past year, OBDC's operating results have been very strong, with a positive trend. NII and NAV have both increased every quarter. Source .

{kind=link}

We've been stating for years that we believe OBDC is a high-quality BDC that deserves to trade at a premium to par. The market has disagreed, and OBDC has consistently traded at a discount. Even today, OBDC is trading at a 5% discount to NAV.

The market's loss is our gain, as we love the opportunity to collect more dividends at a lower price.

OBDC focuses on the "upper middle market," its portfolio companies have an average EBITDA of $196 million/year. So while these are "small" companies compared to public companies that might measure EBITDA in the billions, they are companies with significant cash flow.

This segment of the middle market historically has less credit risk than smaller companies, and OBDC has only 1.1% of borrowers at costs that are non-accrual. 88.5% of borrowers are performing as expected or better than expected at the time of underwriting. This is despite the rapid increase in interest rates that has put pressure on a lot of companies. Source .

{kind=link}

OBDC is firing on all cylinders, and we are happy to sit back and collect our frequent and growing dividends.

Conclusion

With SLRC and OBDC, we can enjoy large yields that are well-covered and growing their payouts. It is a prime time for BDCs to benefit as interest rates rose rapidly. While many have low fixed interest costs, they are earning high variable rate interest from their loans. Many investors are still hesitant to buy into BDCs because they're worried about a climbing rate of defaults, which is a valid concern. Default rates typically rise as recessions occur because the economy is straining under various conditions. In this case, it would be high interest rates and slowing economic output.

Yet, well-established BDCs are going to have portfolios that see fewer defaults than the average, simply because they have supported and enabled their portfolios to hold quality companies. Once interest rates have bottomed again, they will begin to climb, as is the cycle, and BDCs will once again start seeing higher degrees of earnings all over again. There are some companies worth holding through their entire cycles, simply because the income that they output is steady and stable.

When it comes to retirement, the last thing you want to do is have to worry about what companies to juggle in your portfolio every time a macroeconomic shift occurs. In our Model Portfolio, we have over 80 picks that provide us yields above 9%. We also have weekly market outlooks that provide an eagle-eye view of the macroeconomic situation and help investors be prepared for what's on the horizon while still collecting outstanding income today.

Half the battle of being an investor is knowing where you are and where you want to be and adjusting ahead of time. This way, your retirement is less stressful because you're not panicking at the last moment, trying to flip the switches or turn the knobs to make your retirement successful. Instead, you know where you're going, you're collecting outstanding income, and then you can do whatever you want the rest of the time – take up golf, go on a cruise, or sit by a fire with your spouse. The ultimate goal of our Income Method is: to make it so you can have powerful income from the market and be able to have a wonderful, affordable retirement.

That's the beauty of my Income Method. That's the beauty of income investing.

For further details see:

2 Magnificent +9% Yields You Don't Want To Miss