TCN - 2 REITs That Could Be Takeover Targets

2023-10-23 08:05:00 ET

Summary

- REITs offer an opportunity to buy real estate at a discount.

- Private equity players are already taking advantage of this.

- We highlight 2 likely buyout candidates.

Over the past year, Blackstone Inc. ( BX ) bought out $30 billion worth of real estate investment trusts ("REITs").

This includes:

- American Campus Communities for $12.8 billion (from which we profited)

- PS Business Parks for $7.6 billion (from which we also profited)

- Preferred Apartment Communities for $5.8 billion

- Resource REIT for $3.7 billion.

... And I think that their buying spree is just getting started.

{kind=link}

They recently had a bit of a break in their REIT buyouts because they were dealing with redemptions themselves, but as they scale back up their capital-raising activities, they will likely put a lot of that capital to work in REITs.

Here's the reason why:

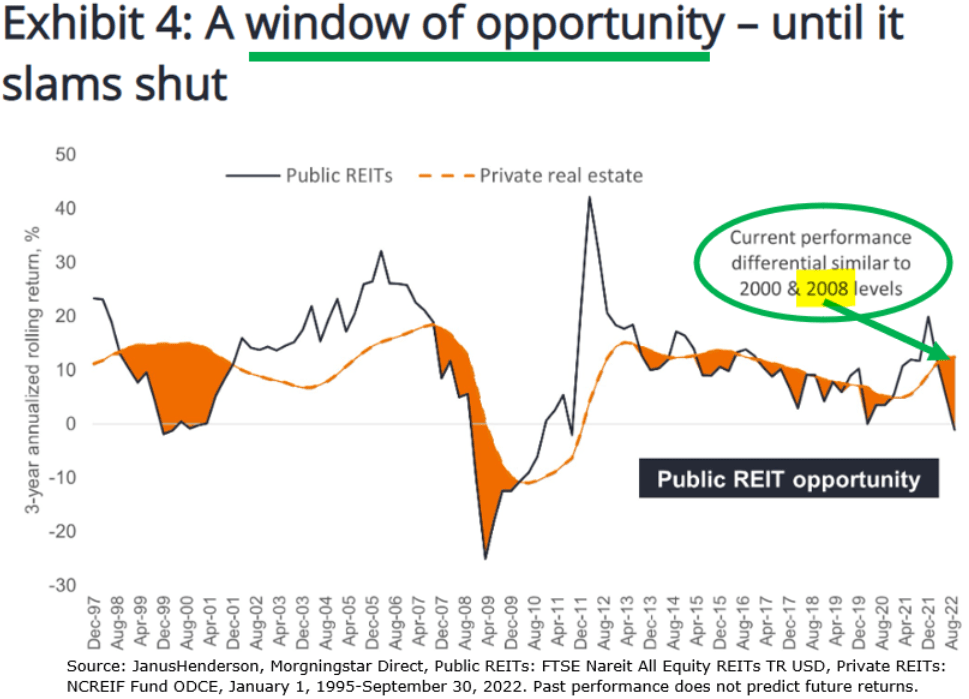

REITs today allow you to buy real estate at a steep discount to its fair value. Their share prices have crashed over the past year even as the value of their real estate remained stable for the most part.

As a result, most REITs are today priced at a large discount relative to their net asset values. According to a one-year-old study by investment firm Janus & Henderson, the average discount was around 30%, the largest since the great financial crisis. Since then, share prices have dropped even further:

{kind=link}

And that's just the average.

There are lots of smaller and lesser-known REITs that trade at even larger discounts and that's despite owning very desirable assets.

They make very compelling buyout targets for private equity players like Blackstone because who doesn't like buying good real estate at 50-70 cents on the dollar?

In what follows, we highlight two small REITs that could become takeover targets in the coming quarters:

UMH Properties ( UMH )

UMH Properties, Inc. ( UMH ) is the smallest of just three REITs that specialize in manufactured housing communities:

- UMH Properties: $920 million market cap

- Equity LifeStyle Properties ( ELS ): $12 billion market cap

- Sun Communities (SUI): $13 billion market cap.

UMH Properties

This is a popular property sector among investors because it enjoys recession-resistant cash flow, steady rent growth, and low capex.

Typically, the investor only owns the land and the tenant then rents the lot and brings his/her own home on it. It makes them highly unlikely to miss their rent payments because the rent is typically very affordable, the next alternative is a lot more expensive, and if they fail to pay, the landlord may end up taking possession of their home.

For these reasons, there are always a lot of investors who are seeking to buy manufactured housing communities, but there aren't many for sale.

It is very tough to get permits to build new ones because no one wants a manufactured housing community in their backyards and existing owners are rarely willing to sell.

This makes UMH particularly appealing as a buyout target because it owns a portfolio of 135 communities, and yet, its share price is today heavily discounted.

Following the recent crash, the management estimates that they are now trading at $45,000 per lot - representing a ~30% discount to private market values.

Moreover, I would point out that the same management team that takes care of UMH used to also manage another REIT called MNR Real Estate, and just recently, they sold it to another REIT called Industrial Logistics Properties Trust ( ILPT ).

This shows you that they are willing to sell if they are presented with the right offer. Today, the chairman and founder of these two REITs, Eugene Landy, is approaching 90 years old, and I suspect that he wouldn't mind selling to come full circle on this venture.

UMH also recently entered a new venture with Nuveen Real Estate, which is one of the biggest real estate owners on the planet. They have been working together to help them build their own portfolio of manufactured housing communities, but given how discounted UMH has gotten, why not just buy them out?

Nuveen Real Estate

It wouldn't surprise me if these discussions were already happening.

In case of a buyout, I think that investors could earn up to 50% upside from today's level and while you wait, you also earn a 6% dividend yield.

That's quite attractive coming from such a desirable asset class.

Tricon Residential Inc. (TCN)

Tricon is not officially structured as a REIT, but it essentially functions as if it were one. It is the smallest of three REIT-like entities that specialize in single-family rentals:

- Tricon Residential: $1.9 billion market cap

- Invitation Homes (INVH): $20 billion market cap

- American Homes 4 Rent ( AMH ): $14.4 billion market cap.

Tricon Residential

Single-family rentals, just like manufactured housing communities, have been attracting a lot of institutional capital in recent years with the likes of Blackstone and BlackRock ( BLK ) even building their own portfolios.

But with high home prices and few transactions happening today, Tricon could become the perfect buyout target, especially given how heavily discounted it has become after the recent crash of its share price:

- Tricon Residential: ~40% discount to NAV

- Invitation Homes: ~10% discount to NAV

- American Homes 4 Rent: ~10% discount to NAV.

Why is it so heavily discounted relative to its peers?

Is it because it owns undesirable assets? No. Most of its properties are located in rapidly growing sunbelt markets, which is precisely where the likes of Blackstone are today investing.

Is it overleveraged? No. Its LTV is today at around 50%, which is below average for single-family homes. Private equity investors commonly use closer to 60% in most cases.

Is it poorly managed? Again, no. The management has done a good job since going public and they have a lot of skin in the game.

Instead, it appears that TCN is so heavily discounted because of two reasons that have little to do with the quality of its assets:

Firstly, it is primarily structured in Canada and Canadian investors simply may not have the same appetite for single-family rentals as U.S.-based investors.

And secondly, TCN is also running an asset management business, managing capital for others and earning fees in exchange for it. It will typically structure JVs to buy single-family homes and it will only put a portion of the capital itself. The rest is coming from other investors who want to participate in the opportunity.

The public market appears to dislike this model and prefers the simplicity of a traditional REIT that owns a 100% interest in all of its properties.

However, this unique JV approach could be very appealing to private equity groups because they are themselves in the business of earning fees for managing capital for others.

In that sense, they would get two things by buying out Tricon...

- The discounted equity in its properties

- The growing asset management platform.

... And priced at a 40% discount to NAV, this seems like a very compelling proposition to a lot of private equity groups.

In a future buyout, the upside potential could be up to 50% and the buyer would still get it at a nice discount. While you wait, you earn a 4% dividend yield.

Closing Note

In a recent interview, legendary billionaire investor Barry Sternlicht said the following:

"There are some unbelievable bargains in REITs. We did the same thing during the pandemic. We bought a dozen stocks all over the world and we had a 70% IRR on that stuff. We are already buying some stuff in the public market..." Barry Sternlicht, CEO/Chairman, Starwood Q3 2023 CNBC Interview.

He runs the private equity group Starwood, which manages $115 billion of assets. Their latest 13F filing revealed that they had recently built a position in an apartment REIT called Camden Property Trust ( CPT ).

By all accounts, it seems that we will have many more REIT buyouts over the coming quarters. Valuations are just too low relative to private markets and we are positioning our portfolio to profit from this opportunity.

For further details see:

2 REITs That Could Be Takeover Targets