SAFE - 2 REITs That Could Soar In 2024

2023-12-27 08:05:00 ET

Summary

- REITs doubled after the 2020 crash.

- Valuations are today comparable, and some REITs could double again in the coming years.

- Here are two REITs that we are buying ahead of their recovery.

Today, some REITs are so cheap that they could double in 2024.

Before you tell me that I am getting ahead of myself just consider that the last two times, REITs were this cheap, they more than doubled in value shortly after.

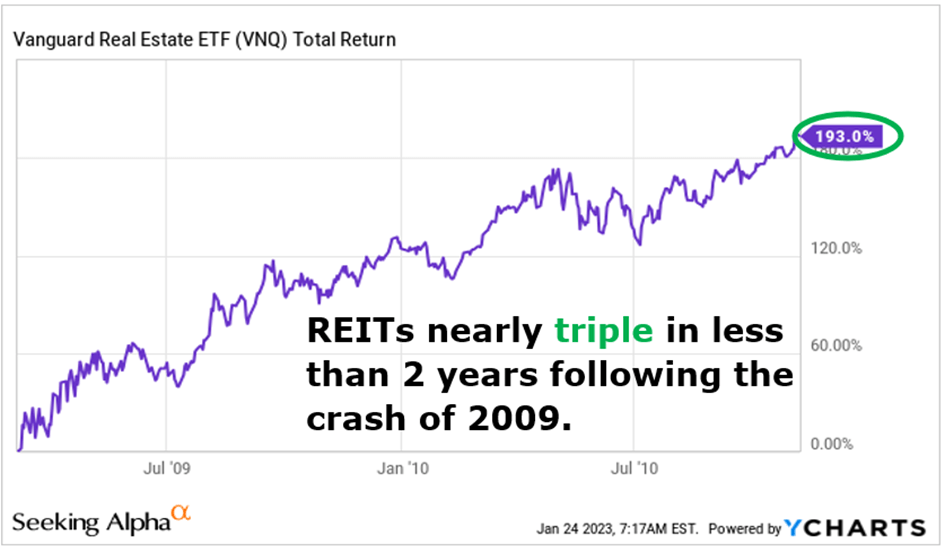

Following the crash of the great financial crisis, REITs nearly tripled in just two years:

{kind=link}

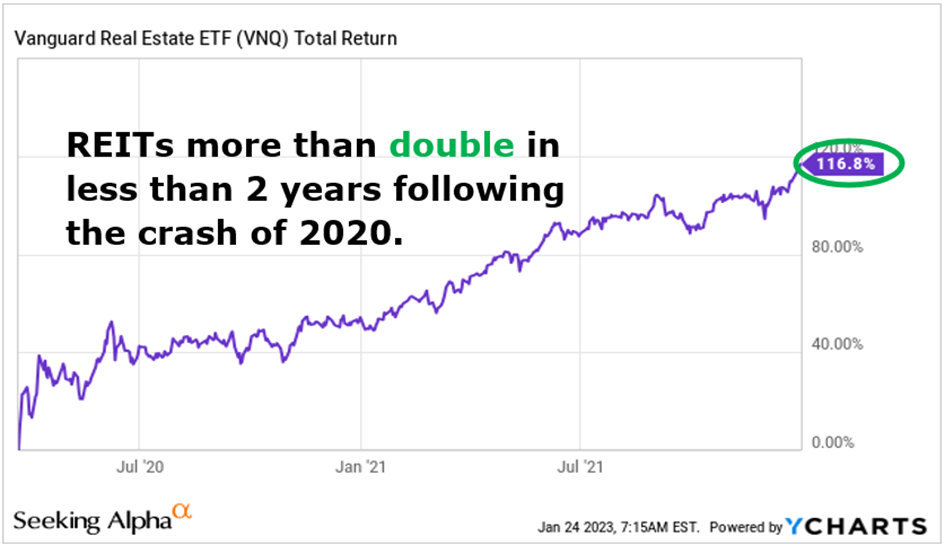

And following the crash of the pandemic, REITs more than doubled in just over one year:

{kind=link}

There's this famous saying that:

"History doesn't repeat itself, but it often rhymes"

And today, REITs are priced at comparable valuations as during the pandemic.

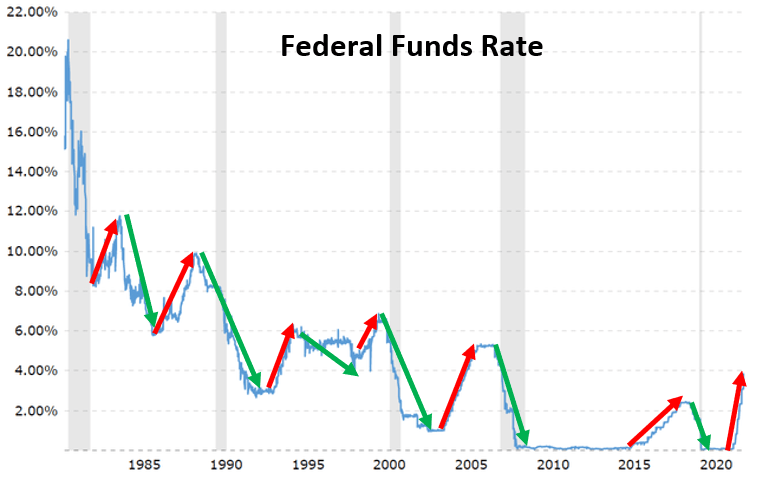

The reason why they are so heavily discounted is that the market is scared of the recent surge in interest rates, but I have some very good news for you: it appears more and more likely that interest rates will be cut in 2024 and this should fuel an epic rally in the REIT sector.

Morgan Stanley ( MS ), UBS ( UBS ), Deutsche Bank ( DB ), Bank of America ( BAC ), Goldman Sachs ( GS ), Bill Ackman, and many others are predicting very significant cuts because inflation is back to normal, the economy is weakening, and the Fed wants a soft landing. Historically, every single rate hiking cycling has been followed by sharp rate cuts shortly after...

Will "this time be different"? I don't think so.

{kind=link}

I don't think that every REIT will double this time, at least not in such a short period.

But there are quite a few of them that present 100%+ upside potential and we are going to highlight two of them that I am accumulating at the moment:

Helios (HTWSF)[LON:HTWS]

Lately, we have invested a lot in cell towers by purchasing shares of Crown Castle (CCI).

The whole REIT market (VNQ) is today out of favor, but cell tower REITs are especially cheap, dropping even more than the rest because they are expected to suffer a couple of years of slower-than-usual growth:

YCHARTS

As a result, Crown Castle (CCI) is now priced at near its lowest valuation and its highest dividend yield ever:

| Historic Valuation |

| Today's Valuation |

| P/FFO |

| 22-25x FFO |

| 14.5x FFO |

| Dividend yield |

| ~3% |

| ~5.5% |

It just shows you that there is no appetite for cell tower REITs in today's market.

I would add that CCI is a US-based mega-cap blue-chip cell tower REIT that has an investment-grade rated balance sheet and a long track record of significant outperformance.

So you can just imagine how the market would then price an African-based small-cap cell tower company that pays no dividend and lacks a lengthy track record...

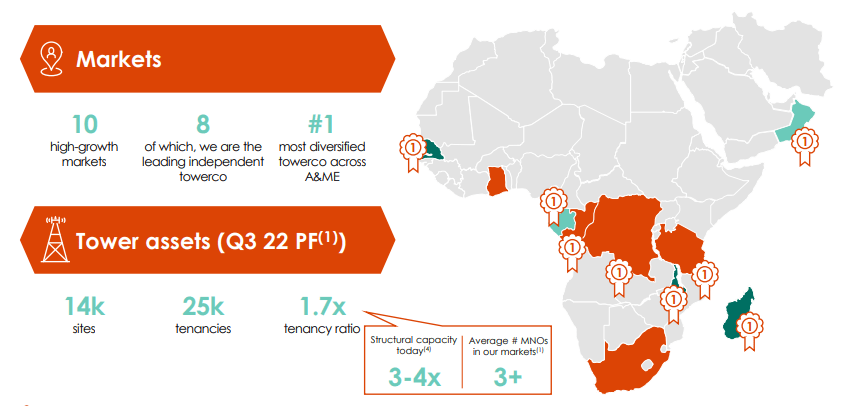

This brings us to Helios Towers, which is a REIT-like entity that's investing in cell towers across Africa and the Middle East.

{kind=link}

It is getting no interest from the market and as a result, it is today priced at just ~7.5x its free cash flow, or put differently, a ~13% free cash flow yield.

That would imply that the company is going through some severe challenges, but in reality, it is actually doing very well.

They just hiked their guidance for 2023 and said that their results were " very strong ".

They are guiding for 13% organic growth and noted that their organic growth is " the best it has ever been ".

And their leverage came down another 0.3x and is now back below 5x Debt-to-EBITDA, which is in line with US peers, and they expect to be below 4.5x by the end of the year.

The nice thing about Helios is that it is experiencing rapid organic growth so its leverage is coming down by itself, and then on top of that, since it is not "officially" structured as a REIT, it is able to retain 100% of its cash flow to reinvest in growth, which results in additional deleveraging and makes them less dependent on public capital markets.

Their goal is to get below ~4x Debt-to-EBITDA by the end of 2024 and after that, they will consider some share buybacks if they are still trading at such a low valuation. Here is what the management said on the recent conference call:

"Buybacks at the current share price do actually make sense. So we're certainly kind of reviewing that option. We think it's highly undervalued. So we will be monitoring that over the short-term period."

Beyond that, they are now also starting to talk about initiating a dividend:

"It's our desire to pay a dividend in the short to medium term as well. So as long as we continue to de-lever within our desired range... then we would actually start to look at some kind of shareholder disbursements if not a little bit sooner."

They once more reaffirmed their intention for both, buybacks and a dividend, a bit later in the call:

"For sure getting to be a dividend payer and/or doing a share buyback is clearly where the business is heading. And we'll continue to monitor that as we move forward both looking at external opportunities as well and winding that up, but certainly becoming a dividend payer is where we want to get to. And on this trend we got there reasonably soon in the more short to medium term."

I think that this would be a very strong catalyst for the stock.

I think that the combination of having a stronger balance sheet, initiating buybacks, and instating a dividend could push the stock a lot higher because it would create a lot more appetite for the stock.

Today, it is tough to convince anyone to invest because many fear that the leverage is a bit high for an African real estate investment firm and the lack of dividends/buybacks makes it difficult to be patient.

But in just a year from now, they should have their leverage back below 4x, which is quite conservative, and assuming that they grow by another 10% in 2024, and then initiate a dividend at a 75% payout ratio, that would result in a near 10% dividend yield.

Suddenly, the market sentiment could become a lot more positive because how many REIT-like entities do you know that offer:

- ~10% dividend yield

- >10% organic growth

- With a lot <4x Debt-to-EBITDA

- With strong secular growth prospects

- And potential buybacks to supplement that?

I don't know any other so it sure would get my attention and likely that of many other investors.

Some of you may argue that... it is an African real estate investment and so it deserves to trade at a low valuation to reflect its higher risk... and to an extent, you would be right, but I would like to remind you that Helios is a lot safer than a typical African real estate investment because:

- Africa's demand for mobile data is set to explode.

- Its current assets enjoy significant lease-up potential.

- Its leases enjoy superior organic rent growth.

- It is diversified across various African countries to mitigate risks.

- It earns most of its rent from multinational companies in hard currencies.

Therefore, it is not like investing in a portfolio of office buildings or strip centers in a single country and earning rents in local currency.

It is far safer than that.

The African continent is of course riskier, but the risks are well-mitigated here, and an argument could be made that Helios deserves to trade at a premium valuation because its growth prospects are superior to those of most other REITs.

In any case, you would probably agree that ~7.5x FCF is too low and that over time, multiple is likely to expand. To close the gap with US peers, which are also heavily discounted, it would need to rise by about 100%, and that's despite having a stronger balance sheet and faster growth prospects.

I would also remind you that a buyout is quite likely.

The CEO of Vertical Bridge [part of DigitalBridge (DBRG)] recently said that "there is a scarcity of towers for acquisition and potential acquirers have dry powder (capital) to deploy" to explain why the prices of towers remain at an all-time high in the private market.

InsideTowers

Meanwhile, Helios is priced at a double-digit free cash flow yield.

An acquisition by a global REIT like American Tower (AMT) or even a private equity player like Blackstone (BX) could lead to rapid upside realization.

For all these reasons, we think that Helios is the most compelling opportunity in Africa. We think that when we look back 5 years from now, we will likely wish that we had bought even more. There are clear risks, but the risk-to-reward seems very compelling given how the risks are mitigated and the many potential catalysts to unlock value within the coming years.

Safehold (SAFE)

We have previously described Safehold (SAFE) as the king of all bets on lower interest rates.

That's because it is the only REIT that specializes in ground lease investments.

In case you are not familiar with ground leases, you should take a moment to study their website . In short, they are land investments that are leased to a tenant for up to 99 years, allowing them to control the land and build a property on top of it. It can be a win-win for both parties as the landlord gets an income stream that's highly secure and once the lease expires, the ownership of the property reverts back to the landlord at no cost. The tenant, on the other hand, gets to build and control a property without having to buy the land, reducing its capital requirements.

But the big downside of 99-year-long leases with pre-set rents is that they are extremely sensitive to movements in interest rates.

When rates declined in 2020 and 2021, the value of their ground leases surged given the ultra-long-duration of the cash flow. That explains why Safehold was our best-performing investment back in 2021. At one point, it had more than doubled our initial basis:

YCHARTS

(Note that we used to hold Safehold via iStar, which does not exist anymore)

But when interest rates surged, its value collapsed and that's how Safehold turned from one of our best investments into our worst in less than two years.

The recent surge in interest rates, which resulted from two black swans, was unprecedented and caught all of us by surprise.

But now it seems that the trend will reverse again and interest rates will return to lower levels. The company's CEO agrees and made the following note on their recent conference call:

Jay Sugarman appears to agree:

"By some measures, this has been the worst market for fixed income investments on record and long-dated cash flows are obviously some of the most impacted when rates rise. But cycles end and we believe we have been through 90%, 95% rate moves in this cycle."

This means that the narrative is likely to change soon.

The market sentiment for Safehold has been very low over the past year because the Fed was guiding for higher rates and investors feared that this would lead to a lower share price.

But as interest rate hikes are now put on pause, the sentiment for the stock should start to improve, and eventually, if and when rates come back down, Safehold could recover just as fast as it dropped. This could lead to a 100% or even 200% upside in short order. So if you agree that interest rates are headed lower, Safehold is arguably the best REIT that you could buy today.

And best of all, Safehold is in no rush because its weighted average debt maturity is 23 years with big pieces of that debt coming due in 30 to 50 years from now. Moreover, its rents are rising steadily by ~2% per year, and they have additional CPI-lookback adjustments that could bump its rent growth to ~3% annually.

So even if our timing is off, and it takes a few more years before rates are cut, SAFE should be just fine. This explains why Moody's just recently upgraded SAFE to an A3 credit rating, which is one of the strong ratings of all REITs.

The company's CEO is one of the biggest shareholders, owning about $40 million, worth of stock, and he keeps buying more at these levels.

He made several ~$30,000 purchases when the shares traded at $~27 per share.

He then doubled down and made a ~$250,000 purchase when it dropped to $24 per share.

And more recently, he again increased the size of his investments and bought another ~$1,400,000 worth of shares after it dropped to $21.40 per share.

{kind=link}

Today, you still have the chance to buy shares at the same level.

A year from now, it could be double if rates return to lower levels.

For further details see:

2 REITs That Could Soar In 2024