WGMI - 2023 Review: Building A Durable Portfolio

2023-12-18 10:32:10 ET

Summary

- Building a durable portfolio that can compound greatly over time is key to long-term capital appreciation.

- My portfolio strategy is influenced by my long-time horizon, high-risk tolerance, and willingness to stomach major drawdowns.

- I detail my investment framework, which consists of four key components: value, growth, quality, and directional bets. I also provide numerous examples of opportunities in each of these components.

Building a Durable Portfolio

I put a great deal of thought into how to build a durable portfolio, which I define as a portfolio built to compound greatly over time. Core to this approach is finding high-quality businesses that I can invest in to allow my money to compound tax-free over time. Much of this approach is defined by my extensive study of Warren Buffett, Charlie Munger, and the story of Berkshire Hathaway. The Berkshire philosophy is one of rigorous study of businesses to find those that have a durable competitive advantage, and making major moves into those businesses at fair prices.

2023 was the first year I hunkered down and became serious about portfolio management. Just before the turn of the year, I published my first article on Seeking Alpha. Since then, I've published 30+ articles and am nearing 1000 followers. A very hearty thank you goes to all those who have read and commented on my articles, and I feel immense gratitude for all the readers who decided to follow! With that, let's explore a bit of what I've learned this year and reflect on how it's impacted my portfolio.

Portfolio strategy is greatly influenced by the circumstances of our life. I am a young person with a long time horizon, high-risk tolerance, and the willingness to stomach major drawdowns. Accordingly, I've found four key themes that have naturally arisen in my approach to investing.

There are simply too many opportunities available for the market to be efficient. Efficient markets imply perfect information and rational decision-making - two things we know for certain aren't true. While 10-K's, 10-Q's, and the like provide an indispensable base of information for investors to evaluate businesses, they do not provide perfect information. Despite the increased digitization of equity markets, with computers and algorithms sloshing significant amounts of capital throughout the system, markets remain a distinctly human phenomenon. Human emotion causes violent gyrations in equity markets.

This imperfect information and volatility paired with the diversity of time horizons and risk tolerances leads to numerous opportunities for long-term capital appreciation. The sheer number of opportunities in the modern market available to retail investors makes an investment framework imperative to maximize capital appreciation. Retail investors operating without a systematic, measured approach will get eaten by whales in no time flat.

My framework has four key components: Value - Growth - Quality - Directional Bets.

Let's explore.

Value

Value is the derivative of all portfolio strategies. From a first principle perspective, investing for value is buying securities for less than they are worth. The pursuit of buying low and selling high dictates the movement of capital throughout markets. Where there is growth, where there is an arbitrage opportunity, there will be capital.

Core to this approach is the belief that all investments carry an intrinsic value, which the price will reflect over time. Purchasing stocks, bonds, options, or otherwise for less than they are worth is the key to durable long-term performance. This is what I consider my value proposition - and I evaluate stocks primarily through two value propositions: Growth and Quality.

Growth

One way to purchase more value than you pay for is to correctly predict a higher growth rate than the prevailing sentiment. If a business manages to grow quicker than the market expects, the stock price will often follow. Current stock prices reflect future growth expectations, so getting this prediction right is critical to protecting and growing capital. The growth question is evaluated through a fusion of macro and micro considerations. Are there global megatrends, like the widespread adoption of the Internet in 1980? What about industry-specific trends, like the commoditization of microelectronic components in smartphones? And what is the story of the individual business that you could buy? Are they a deeply entrenched titan, or a disruptive newcomer?

Evaluating these questions with pragmatism and lucidity is key to picking stocks whose growth will outpace both the wider market and the market's expectations for the business itself. Peeling back another layer, durable growth over time depends on one critical business characteristic: Quality.

Quality

Investing in quality requires a deep understanding of the underlying business and industry. Without extensive knowledge of a business and the wider industry outlook, long-term market-beating capital appreciation is maddeningly evasive. Many investors are burnt by chasing the crowd or value traps. Those who spend the time to develop a deep understanding can pick out long-term winners from the crowd, park their money with winners, and let compounding do the rest.

The third piece of my investment framework is an affinity for quality. Over time, quality businesses will produce market-beating returns. The quality of a business is its ability to produce market-beating returns. No method can beat the market with so much certainty as purchasing quality. Some important characteristics of quality businesses are economies of scale, consistently high margins, low ratio of SG&A expense relative to sales, consistent growth that doesn't require incremental capital, a monopolistic market position, high barriers to entry, strong brand recognition, competent management, and consistent earnings growth. This list is not exhaustive but illustrative of characteristics that investors should search for in their research. Not all quality businesses will present these characteristics, but this is a good list to guide investment decisions.

The entire philosophy of quality investing is illustrated perfectly in Warren Buffett's words (a belief he largely credits his long-time partner Charlie Munger with instilling in him): "I would rather buy a wonderful business at a fair price than a fair business at a wonderful price".

Buying and holding quality is the surest way to beat the market. However, many investors are still nagged with the timeless issue: not enough cash! How then can we round out a strategy to build a durable portfolio over time? Short-term cash generation can be achieved with high-conviction directional bets. If these directional bets pay off, usually in a big way, it can provide us with a lot of capital now to park in long-term quality. Small directional bets can reward investors while limiting the loss of principal.

Directional Bets

Bets are high-risk high-reward by definition. Feeble investor sentiment creates drastic volatility in markets that patient investors can abuse to generate significant short-term capital appreciation. These decisions require the most conviction and carry the highest risk. My directional bets, mostly options, are time-sensitive and highly uncertain. Buying calls on a stock puts a depreciating asset in the hands of an investor. Without accurate prediction of underlying asset behavior, this asset will fade to worthlessness over its lifetime. But these assets also offer nearly unlimited upside with very little upfront cost.

2023 in Reflection: This Framework in Action

Now that I've detailed my approach to picking stocks, let's dive into my portfolio and how this framework has manifested itself in my allocation decisions.

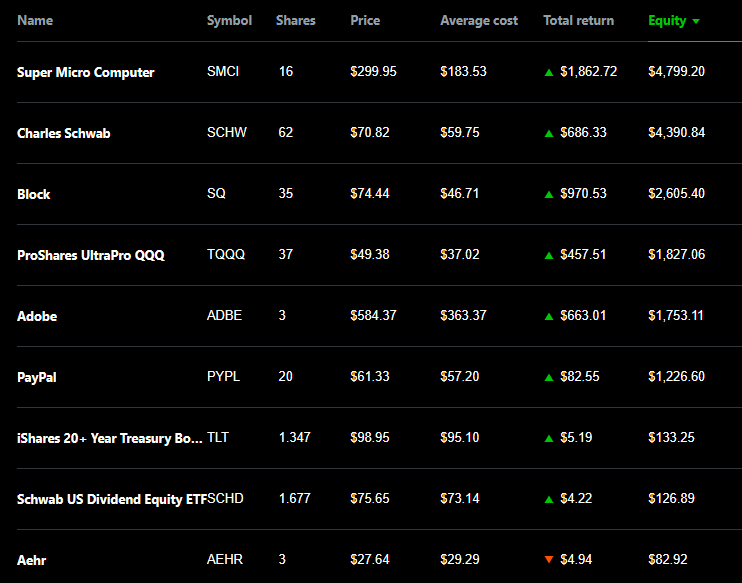

Taxable Brokerage

Author's Creation, Taxable Brokerage

{kind=link}

I've accumulated these positions throughout this year. The starting value of my portfolio was roughly $2,000. At the time of writing, this portfolio (including options, which are not included in the above pictures), is worth $17,713.53. This growth is from a combination of capital appreciation and principal contributions of about $9,797.99 this year.

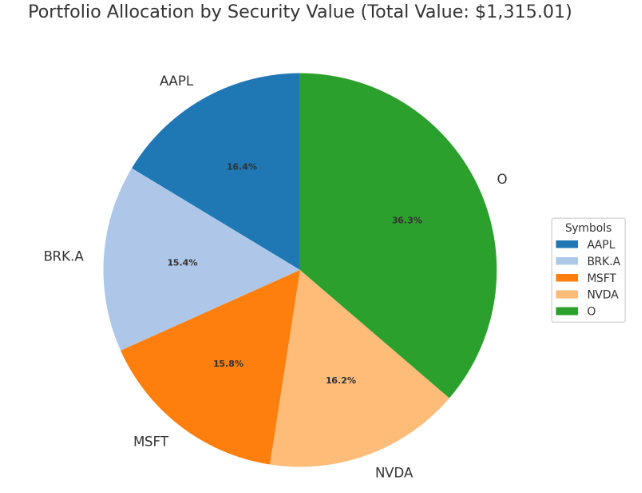

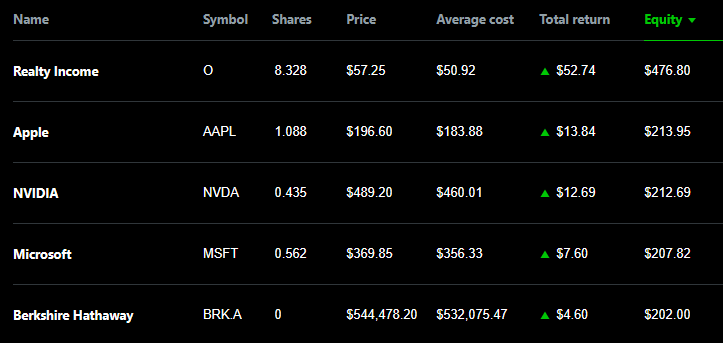

Roth IRA

{kind=link}

{kind=link}

Utilizing a Roth IRA is a recent component of my portfolio strategy. Most of this was driven by Robinhood's offer of a 3% cash match of Roth IRA contributions. The opportunity to immediately compound 3% in a tax-advantaged account is too good to pass up. In my Roth, I hold yield and quality. These are stocks that will benefit from a Roth tax structure by decreasing tax incidence on dividends or stocks that I intend to hold indefinitely to compound over time.

In terms of my framework, here is my current breakdown of my positions across both accounts:

Value

PayPal ( PYPL )

PayPal, like most fintechs this year, has been beaten to a pulp by the market. The prevailing narrative is that increasing competition, margin erosion, and active user attrition will severely limit PayPal's long-term growth and profitability. This has led to PayPal becoming severely mispriced. I have been accumulating a position in PayPal since October 25th, and plan to continue this accumulation until the price begins to recover. Increasing competition should be a concern, but the numbers don't lie - PayPal is still a dominant player in digital payments and is one of the most trusted brands worldwide. Margin erosion is not being caused by a price war or shrinking market share - it's being caused by rapid growth in the lower-margin unbranded segment. The branded segment is still growing, just not as fast. Finally, there has been some erosion of total active users, but management has been focusing on its high-quality users, so revenue per user is increasing while the total user count is shrinking. While PayPal has some issues, they aren't as severe as the market believes.

Charles Schwab Corporation ( SCHW )

At its core, Schwab is an asset management and wealth advisory firm. The unique business structure that Schwab employs though has led to quite a volatile year for the stock. Rising rates are bad for wealth advisors to begin with - equities fall as the risk-free rate rises, trading volumes decrease, and rising yields devalue the back-book of loans that are held for sale. These issues were pressuring Schwab's stock already when the dramatic fall of Silicon Valley Bank in March of 2023 rocked the entire financial industry. Any institution that depends on cash sweep for revenue saw its market cap crater overnight. Although Schwab is not a bank or traditional depository institution, their revenue structure resembles one. Schwab takes the client's uninvested cash and sweeps it into Charles Schwab Bank to begin earning interest income on it. When SVB fell victim to a bank run, investor sentiment crushed Schwab on fears of a similar issue occurring. This led to a significant mispricing of this goliath, while Schwab faced no existential threat to its business. I explored this in more detail in my Strong Buy rated article on Schwab titled Charles Schwab: A Discounted Behemoth, Buy The Earnings Contraction.

Realty Income Group ( O )

As rates were on their uninterrupted march upward during 2022, rate-sensitive stocks got crushed. Equities are rate sensitive, to begin with as most valuation models use a risk-free rate in their calculations, so as this rate increases value decreases. Equities sell-off. Fears of a looming recession, high inflation, and a deeply inverted yield curve scared many investors further away and toward safer investment vehicles. There was little appetite for equities, especially not acutely rate-sensitive equities like REITs. Realty income group fell victim to this pessimism and the stock price was impacted accordingly. This was not because of fundamental weakness, but because of widespread fear in markets. I have been dollar-cost-averaging weekly into O since the yield was above 6%. I plan to continue this at least until the yield falls below 5%. This is both a value and long-term accumulation play. I will be reinvesting dividends in my Roth IRA indefinitely.

Growth

Aehr Test Systems ( AEHR )

Aehr is a microcap with a strong competitive offering in the semiconductor manufacturing equipment market. You can read more about their competitive advantage and the business in my article titled Aehr: A Microcap With A Strong Competitive Advantage.

Super Micro Computer ( SMCI )

Super Micro Computer is one of the leading AI trades from 2023. As a provider of high-performance IT solutions, they have experienced strong growth throughout this whole year. This growth looks almost certain to continue through 2024, as they are increasing manufacturing capacity and supply shortages have eased. I wrote on SMCI most recently in an article exploring the server industry and before that in an article discussing their business model.

NVIDIA ( NVDA )

NVIDIA needs no introduction. The AI hype is real and the commercialization of AI throughout end markets will provide strong growth for years to come. Valuation aside, this is a business that is certain to grow top and bottom line for at least the next five years. Barring any cataclysmic events like a conflict in Taiwan, a major recession, or accounting fraud, NVIDIA will continue its strong upward trajectory over the medium term. I wrote on Nvidia most recently after the Q3 2023 earnings release .

Block ( SQ )

Block, like other fintechs, has cratered since the COVID bubble burst. The story here is similar to the PayPal story. Rates, recession fears, and increasing competition have led to this stock becoming severely mispriced. This is a fusion of value and growth and will reward patient investors over time. I wrote on Block's numerous tailwinds recently and expressed why this is one of my high-conviction stocks going into 2024.

3x Leveraged Nasdaq ETF ( TQQQ )

My strategy here is quite simple. Buy shares when this dips 5% or more and sell some shares when the Nasdaq hits an all-time high. I am bullish on America and its tech sector and therefore feel comfortable utilizing leverage to boost returns over time.

Quality

Apple ( AAPL )

Apple is a prime example of a quality investment. It's hard to justify a $3T market cap. It's hard to buy when valuations are at historical highs. But it's also hard to imagine any company disrupting the global smartphone oligopoly. Apple has a strong product ecosystem and will maintain its dominance because of superior product quality .

Microsoft ( MSFT )

It's hard not to love what Microsoft is doing. They have two durable monopolistic products with the Windows OS and Microsoft Office. They own the leading professional social network with LinkedIn. They own one of the few major players in gaming with Xbox. And now the exceptional management of Satya Nadella has placed them securely in the lead in the AI race with a major OpenAI investment and a market-leading AI offering with Bing's Copilot.

Adobe ( ADBE )

Adobe has a monopoly in creative software because of its product breadth and superior quality. There is simply no viable alternative to Adobe for creative professionals. Some individual software programs may have strong competitors, but there doesn't exist a company other than Adobe with the breadth of high-quality software programs for creative professionals. Mixed with an incredible margin profile a generous share buyback program, and strong AI offerings , Adobe is a sure winner over time.

Berkshire Hathaway ( BRK.A ) / ( BRK.B )

I would be doing a disservice to Berkshire by even attempting to explain why this is a quality investment. Warren Buffett and Charlie Munger have created the most comprehensive collection of quality businesses in history. It will be difficult for Greg Abel to fail so immensely that Berkshire doesn't continue delivering shareholder value over time.

ASML ( ASML )

ASML enjoys a pure monopoly at the heart of one of the largest and most important global industries. Semiconductor manufacturing involves a few deeply entrenched behemoths, and all those behemoths are singularly dependent on ASML to operate their business and maintain their competitive position. Until a viable alternative to EUV lithography is commercialized at the leading edge, ASML will continue to be one of the highest-quality businesses globally.

Schwab US Dividend Equity ETF ( SCHD )

There's not much to say here other than SCHD is a SWAN investment that should continue winning over time. The historical track record is strong and, while currently trailing the S&P due to a weak year, is a collection of very high-quality businesses.

Directional Bets

Bitcoin Miners ETF Call ( WGMI ) -

This is just a gamble on a Bitcoin bull run. This could pay off significantly but also could be a nothing-burger. This is a very short-term call contract that I will look to exit as my expiry date approaches to protect my principal if there is insufficient price appreciation. I am currently up 5%.

SQ & PYPL Calls

As noted earlier, both SQ and PYPL are my highest conviction bets right now. As such, I have a position in two long-dated call contracts that require roughly a doubling of the stock price from the time I purchased the contracts. I am currently up 39% on my $95 PYPL call with an expiry of 1/17/2025 and up 250% on my $110 SQ call with an expiry of 1/17/2025.

TQQQ Put sale

I sold two cash-secured TQQQ contracts near the end of November. I did this because I believed we were securely in a bull market. The market is emerging from a deep two-year bear market and the Fed is hinting at a looming pivot. Selling puts also benefits from the time-decaying nature of options. I am currently up 33%.

Long-bond ETF ( TLT )

Although I haven't initiated an options position in TLT, I still consider this a directional bet. This is simply a bet on Fed cuts, as TLT price will increase as a step-function relationship with rate cuts. Although this position is small for now, I am purchasing TLT regularly and will sell once rates plateau.

Additionally, here is a breakdown of my current watchlist based on this framework. I will not be breaking these down as I did for my other positions as I haven't done sufficient research to make claims yet on these businesses (also why I don't hold positions!).

Value

Alibaba ( BABA )

Pfizer ( PFE )

Growth

Tesla ( TSLA )

SoFi ( SOFI )

Palantir ( PLTR )

Onsemi ( ON )

Celsius ( CELH )

Quality

Synopsys ( SNPS )

Applied Materials ( AMAT )

Lululemon ( LULU )

Lowe's ( LOW )

Broadcom ( AVGO )

Directional Bets

Given the nature of directional bets, it's difficult to maintain a watchlist of potential opportunities. They are highly uncertain and seldom have a lot of lead time. They require high conviction and rapid decision-making.

Conclusion

2023 was quite an interesting year for investors. This year taught us that, no matter the prevailing sentiment in January, markets can always surprise us. Investors that fell victim to fear missed out on quite substantial returns this year. I am pleased with my current 50% YTD return, outpacing the S&P, and feel confident in the durability of my portfolio.

For further details see:

2023 Review: Building A Durable Portfolio