OMVJF - 3 High-Dividend Large-Cap Overseas Energy Companies You're Ignoring

2024-01-18 11:30:37 ET

Summary

- OMV Aktiengesellschaft, Repsol, and Eni S.p.A. are three energy companies offering attractive yields to investors.

- OMV Aktiengesellschaft has a stable distribution payout and is trading at a low valuation.

- Repsol, S.A. has a lower yield but maintains a safe distribution payout and has a low net leverage ratio.

- Eni S.p.A. is the largest company with a hefty yield, a low distribution payout, and a reasonable net leverage ratio.

Although I have never been the kind of investor to prioritize yield, I do understand that many investors look at that above almost all else when it comes to making investment decisions. This is especially true for those in retirement or those nearing retirement, as well as others who might be saving up for something. It does make sense because distributions do provide a stream of income that can be used, plus they have the benefit of being in your pocket. If the company that you owned shares of for 20 years that never paid a distribution suddenly goes bankrupt because of alleged fraud the next day, you would have gotten nothing for all of those years. But for a company with an attractive dividend, you received money in your pocket along the way.

In this environment, there are plenty of opportunities to capture attractive cash flows. Even buying government securities can yield a decent amount of cash. On the other hand, if you want both appreciation and a yield that beats out most of what else is out there, your options do become limited. In the energy space, few of the very large players pay out anything substantive. But if you dig a bit deeper, some of the large firms that aren't necessarily amongst the largest companies in the space do offer some really great payouts. In what follows, I would dig into three of these firms and discuss their stability and price with the hopes of shedding light on whether or not anyone of them or all three of them might make for a good opportunity for anybody who might read this article.

A special note

Before I move on from here, I first need to mention that all financial results provided by these companies is in the form of EUR. Given that the vast majority of my readers are likely used to dollars, I have converted all financial data provided by management into US dollars using the most recent exchange rate available.

Betting on a name I can't pronounce

At the very top of my list is a company that I cannot pronounce the name of if my life depended on it. The firm in question is none other than OMV Aktiengesellschaft ( OMVKY ). With a market capitalization of $13.88 billion as of this writing, OMV Aktiengesellschaft is a rather sizable player in the energy market. But it's not just any energy company. It's an integrated player in the space. It might be helpful to touch on some of its operations to begin with. First and foremost, the company has a rather large Chemicals & Materials business. In fact, this unit operates as one of the largest providers of advanced and circular polyolefin solutions on the planet. In 2022, it was responsible for 5.7 million tons of this product. It also produces a wide array of other base chemicals, fertilizers, and more. It even engages in the recycling of plastics.

Next in line, we have the Refining & Marketing business. This unit was eventually renamed the Fuels & Feedstock segment. This is located through a variety of central European nations such as Germany, Hungary, Moldova, Romania, and more. Through this unit, the company has its own refineries, filling stations, and even gas-fired power plants. Its refineries alone have capacity of around 500,000 boe (barrels of oil equivalent) per day. And last in line, there is the Exploration & Production segment, which has since become known as the Energy segment, of the company, which in 2022, the most recent year for which full year data is available, produced 392,000 boe per day, equivalent to 143 million boe in all. About half of this output is natural gas, with the other half taking the form of oil and NGLs.

Author - OMV Aktiengesellschaft

{kind=link}

In recent years, the surge in energy prices that we have seen proved to be particularly bullish for the business. Revenue went from $18.07 billion in 2020 to $68 billion in 2022. With this rise in revenue came a jump in profits as well. Net income went from $1.61 billion to $5.65 billion. Other profitability metrics improved as well as the chart above illustrates. This includes operating cash flow and EBITDA. Included in this is also a measure for operating cash flow that I call adjusted operating cash flow. This is what we get when we strip out changes in working capital from the equation.

Unfortunately, high energy prices were not destined to last. In the first nine months of 2023 , revenue for the company came in at $32.11 billion. That's a sizable decline from the $52.17 billion reported one year earlier. Net profits and cash flows followed without exception. As I mentioned already, this was all largely the result of a decline in prices. Actual volumes for the company's different segments showed very little change from one year to the next. Under the Chemicals & Materials segment, for instance, the firm saw polyolefin sales dip only slightly from 4.25 million tons to 4.24 million tons. Under the Energy segment, production was lower, but only by about 4.7% year over year.

Author - OMV Aktiengesellschaft

{kind=link}

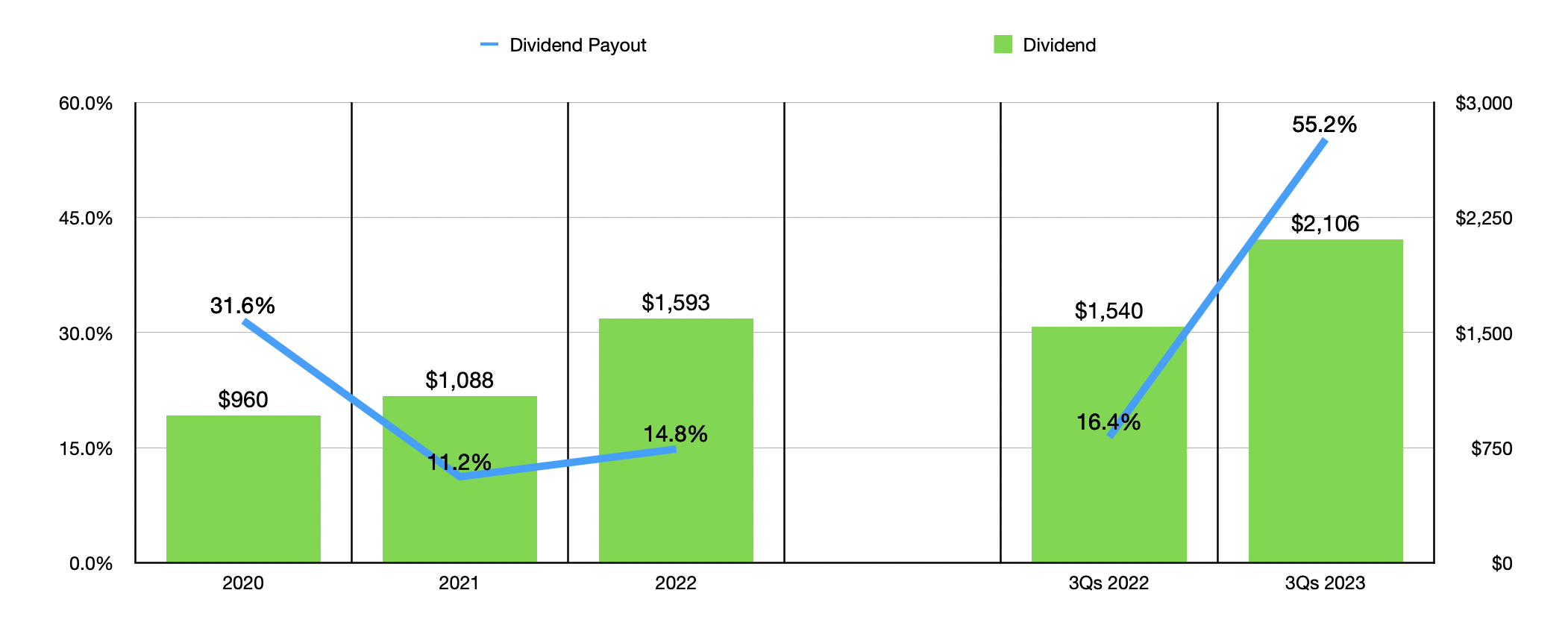

Given this drop in revenue, profits, and cash flows, you might think that the 7.07% yield currently offered to shareholders would be in jeopardy. The good news is that management has been very conservative in recent years about the payout. From 2020 through 2022, the annual distribution expanded from $960 million to $1.53 billion. Even with the drop in profitability in the first nine months of 2023, the company paid out $2.11 billion compared to the $1.54 billion paid out the same time of 2022. Despite the fact that adjusted operating cash flow plummeted from $9.40 billion in the first nine months of 2022 to $3.82 billion in the first nine months of 2023, that still translates, so far for 2023, to a distribution payout amounting to only 55.2%. Of course, any player in the energy markets, including one that's engaged in the exploration and production space, must allocate a large amount of capital toward capital expenditures. The good news is that, even after factoring those in and taking out distributions for the first nine months, the company still had $725.9 million in net cash flow to work with.

Author - OMV Aktiengesellschaft

{kind=link}

Speaking of cash, it's worth pointing out that, unlike many other players in the energy markets, OMV Aktiengesellschaft has negative net debt. As of the end of the third quarter of 2023, it had cash that exceeded debt totaling $937.7 million. That also should be weighed when considering the safety of the distribution for shareholders. A company with an absence of debt, on a net basis, is far less risky than one that is heavily leveraged. Add on top of this the fact that the company is trading at about 3.1 times adjusted operating cash flow and at about 3 times on an EV to EBITDA basis, and it makes for a solid prospect in my book.

Hola

Next in line, we have Repsol, S.A. ( REPYY ), which is based out of Madrid, Spain. With a market capitalization of $18.15 billion, Repsol, S.A. is a bit larger than the first company in this article. However, its yield comes in a bit lower at about 6.11% as of this writing. That's still a fantastic payout to lock in, if it's stable. But before we get to that topic, it would be helpful to dig into what the company is and what it does.

According to the management team at Repsol, S.A., the enterprise consists of three primary segments. The first of these is the Upstream segment which, as you can imagine, engages in the exploration, development, and production of certain natural resources. Namely, we're talking about oil and natural gas. About 70% of the $1.916 billion of proven reserves under this segment is in the form of natural gas. But even with those massive reserves, the company produces around 572,000 barrels of crude each day.

Next in line, we have the Industrial segment, which focuses on refining activities, the production of petrochemicals, the trading and transportation of crude oil and oil products, and even the sale, transportation, and regasification of not only natural gas, but also liquefied natural gas. In all, the company has over 1 million barrels per day worth of refining capacity, making it a major player in this regard. And lastly, there's the Commercial and Renewables segment. This touches on a variety of activities such as the company's low carbon power generation strategy, renewable energy sources, the sale of gas and power to customers, mobility activities and the sale of oil products, and everything not mentioned already that involves liquefied petroleum gas.

{kind=link}

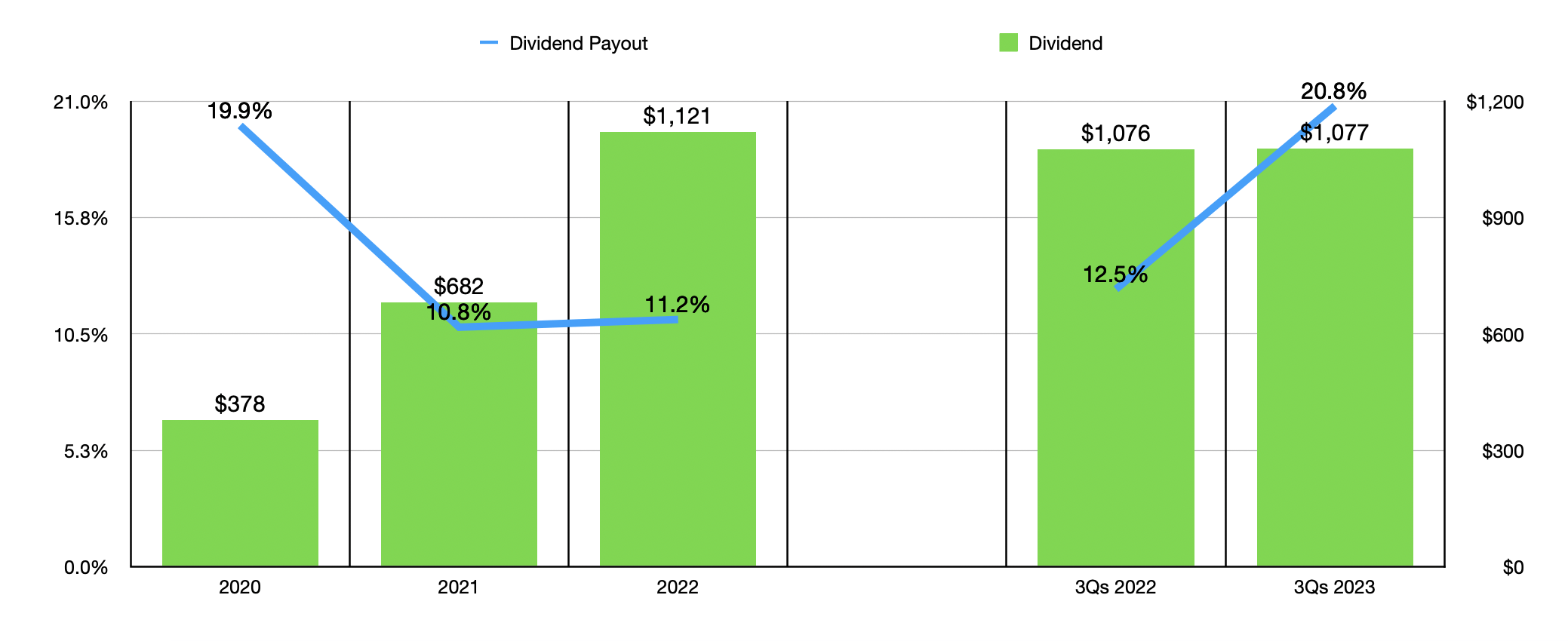

Just like our prior prospect, Repsol, S.A. has done really well to grow in recent years. Revenue with the business expanded from $35.98 billion in 2020 to $81.68 billion in 2022. As you can see in the chart above, profits and cash flows followed suit. And as the chart below illustrates, financial performance has weakened for 2023 relative to 2022. Despite this weakening, management has always been mindful not to allocate too much in the form of distributions for fear of having to pull them back again. In 2020, for instance, the company spent only $378 million on dividends. That was against $1.90 billion of adjusted operating cash flow. Even when you cover the first nine months of 2023, the distribution for the company was virtually flat year over year at about $1.08 billion. To put this in perspective, adjusted operating cash flow for the same window of time was $5.18 billion. This implies a dividend payout of 20.8%, even during what was undoubtedly not a great year in the energy space.

{kind=link}

Speaking of the distribution, it does appear to me that it's safe from the perspective of leverage as well. Net debt on the company's books is about $2.02 billion. When you consider that annualized EBITDA for 2023 should be around $8.15 billion, that implies a net leverage ratio of only 0.25. It would be astounding if the company has to cut the distribution absent a plunge in energy prices. Also, just like the first company that I covered in this article, shares of the business are quite cheap. Based on my estimates, the company is trading at about three times adjusted operating cash flow and 2.2 times on an EV to EBITDA basis.

{kind=link}

The big boy in the room

Of the three companies that I'm diving into, the largest, by far, is Italian firm Eni S.p.A. ( E ). With a market capitalization of $52.95 billion as of this writing, it truly is a major integrated energy business. It also boasts a yield of 6.05% as of this writing, which is a rather hefty payout for a company of its magnitude. Operationally speaking, it has four different segments if we exclude its corporate and other activities operations. The largest of these has been its Exploration & Production unit which, like every other company engaged in that activity, has benefited tremendously from rising energy prices over the past few years.

Spread across multiple countries, the Exploration & Production part of the company is a true behemoth. In 2022, it was responsible for 1.61 million boe per day of output. This actually represents A consistent decline year after year that started in 2019 when the unit was responsible for 1.87 million boe per day. Despite this drop, the segment is still in control of 6.61 billion boe of net proved reserves. That's over 11 years worth of output if the picture remains unchanged from what it was back in 2022. As I mentioned already, the segment is responsible for operations spread across different countries. This includes Italy, various parts of Europe, North Africa, Egypt, sub-Saharan Africa, Kazakhstan, various other parts of Asia, the Americas, Australia, and parts of what is known as Oceania. When it comes to oil and natural gas production, as of the first three quarters of 2023 , its largest exposure was to Egypt, from which the company extracted 323,000 boe per day of its 1.64 million boe per day.

Next in line, we have the Global Gas & LNG Portfolio segment, which is engaged in the wholesaling of natural gas using pipelines and is also engaged in the production and sale of the liquefied natural gas. A little under half of the gas sold through this segment is sold directly in Italy, with the rest sold to other countries. Of the gas sales in Italy, the company consumes about 17.7% on its own. But the largest chunk, about 39.8%, is made available on a wholesale basis to customers. This gas comes from multiple countries, including the Netherlands, Norway, Qatar, Egypt, Libya, and others.

The third segment is the Refining & Marketing and Chemicals segment, which, as you can imagine, is engaged in refining activities, particularly in processing feedstock into more advanced chemicals for various industrial uses. Truthfully, a standalone article could be written about any one of these segments. So I know I can't touch on everything. But this unit is particularly complex given its various assets. For instance, the unit even has biorefinery capacity and it boasts a network of more than 5,000 service stations throughout Europe, with around 80% of these located in Italy. And lastly, there's the Plenitude & Power segment, which focus is on the marketing of gas, power, and services for end customers in the regions in which it operates. This includes power produced by thermoelectric plants and from renewable sources as well. It also boasts an electric mobility business, as well as trading activities for carbon dioxide emission certificates and other miscellaneous things. As of the end of the 2022 fiscal year, the segment also had over 13,000 electric vehicle charging points in its home country.

{kind=link}

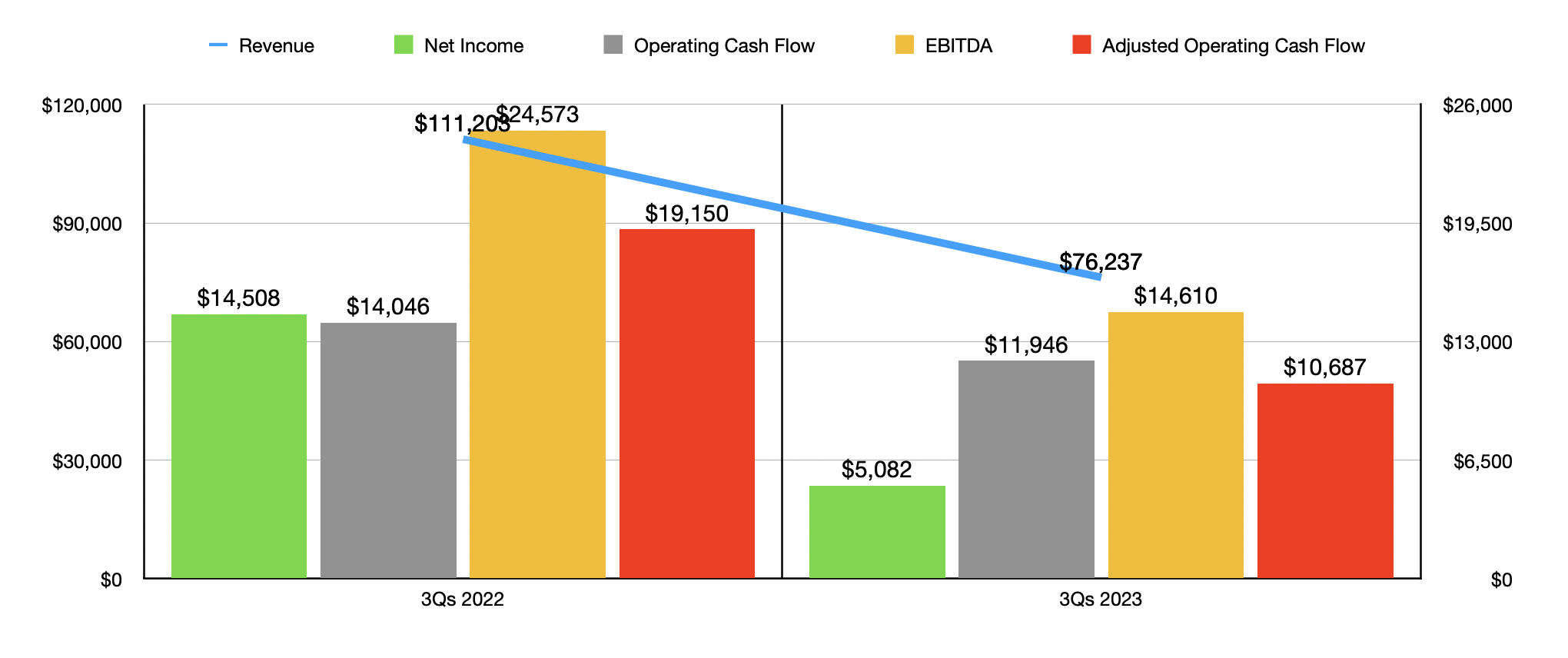

As the largest player covered in this article, it stands to reason that the financial footprint of the firm would also be massive. From 2020 through 2022, thanks in large part to a surge in energy prices, revenue skyrocketed from $48.02 billion to $144.35 billion. Profits and the cash flows rose nicely as well. For context, in 2022, adjusted operating cash flow for the company came in strong at $20.45 billion. That dwarfs the $5.28 billion reported one year earlier. But just like every other firm in this space, 2023 was a year of weakness. Revenue of $76.24 billion in the first nine months was substantially lower than the $111.20 billion reported the same time of 2022. Net profits were slashed by almost two-thirds from $14.51 billion to $5.08 billion. Cash flow figures were not as impacted, with some of them falling by less than 50%. But they did see declines all the same.

{kind=link}

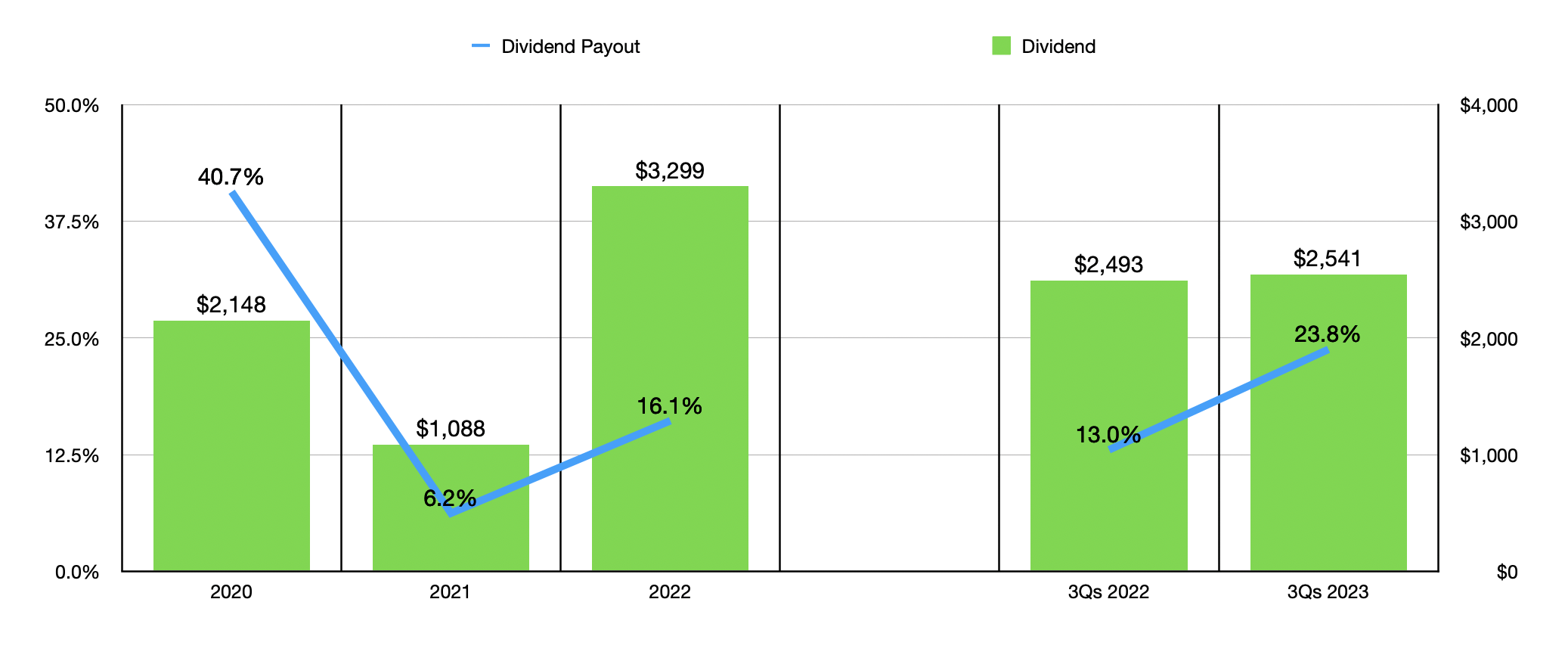

The good news for shareholders is that, even with a hefty yield, the distribution payout in the first nine months of 2023 totaled only 23.8% of the adjusted operating cash flow that the company produced during that same window of time. Unlike its peers, Eni S.p.A. it does have a bit more debt, coming in at $19.28 billion. But that still translates to a net leverage ratio, if we annualize EBITDA for 2023, of 0.99. That's far from bad. Shares also are a bit more expensive relative to the other two companies, with a forward price to adjusted operating cash flow multiple of 4.6 and an EV to EBITDA multiple of 4.4. Compared to the market more broadly, that's quite cheap. But for a company that has a large portion of its operations dedicated to the exploration and production market, it does not seem to be out of the range of what one would expect.

{kind=link}

Takeaway

If your goal as an investor is to buy large, stable companies in the energy space, while simultaneously capturing attractive distributions, the three companies that I covered here are definitely prospects to be considered. No, they don't have the same kind of stability and consistency that standalone pipeline operators might. But they do bring with them diversification in terms of the activities that they engage in. All three firms have debt levels at are well below what I would have anticipated and they easily cover their distributions. Shares are also attractively priced. So these are definitely prospects that are worthy of consideration.

For further details see:

3 High-Dividend Large-Cap Overseas Energy Companies You're Ignoring