FTDS - 4 Things To Watch For In Friday's Employment Report

Summary

- Most of the monthly short leading indicators have turned down; all but one of those which remain positive are employment-related.

- All of those will be updated this week, including 3 in the jobs report on Friday.

- Along with construction, manufacturing, and short-term unemployment, aggregate nonsupervisory payrolls will be updated, and there will be important revisions to the 2022 jobs numbers.

Introduction

While the majority of long leading indicators long ago turned negative, the majority of short leading indicators only did so several months ago. Almost all of the remaining short leading indicators that would be expected to turn down before a recession actually begins are components of the monthly jobs report, which will be updated this Friday.

Overview of my current economic analysis

Most economic analysis is "skating to where the puck is," to quote Wayne Gretzky, simply projecting current trends forward. Whereas, taking into account the short leading indicators first and then looking at the coincident ones is better at "skating to where the puck will be."

So let me be transparent, and start with a synopsis of my current thinking.

Almost all of the long leading indicators had turned down by the end of Q1 of last year, meaning that Q1 of this year was the first "recession-eligible" quarter. As a result, late last spring, I went on "Recession Watch" beginning this Quarter. Many of the short leading indicators are inflation-adjusted, which means that the price of gas rocketing to $5 by June and then plummeting to $3 by December had a big effect. Despite that 2nd half tailwind, most short leading indicators had turned down by early Q4. Once that happened, I went to "Recession Warning."

With one exception, the only short leading indicators that I track and are reported monthly, that have not turned down yet are all employment-related:

- construction employment

- manufacturing employment

- number unemployed less than 5 weeks

- initial jobless claims

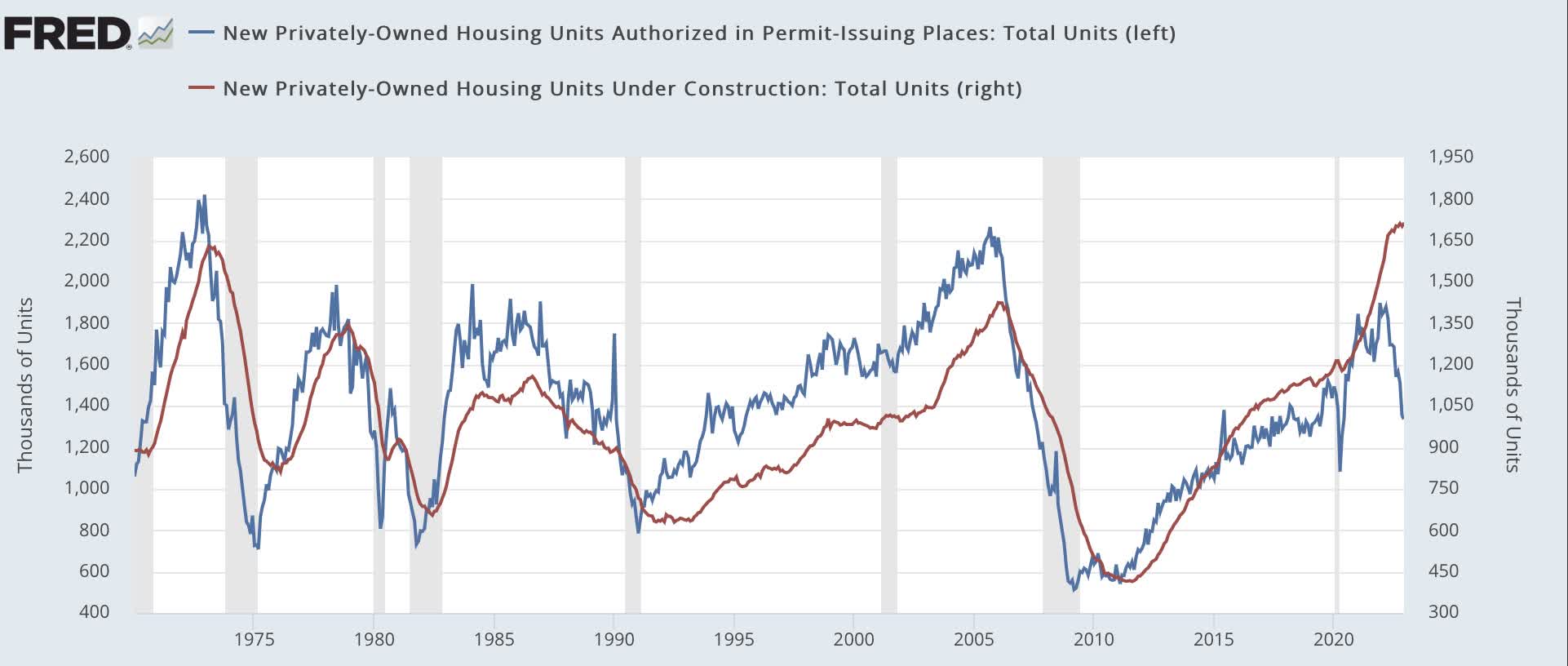

The one that is not employment-related is housing units under construction, which just made an all-time high in December.

As indicated above, since most of the short leading indicators have turned down, we look to see if the coincident indicators have followed. At this point, if they turn down, they are likely to continue down. We see that industrial production and real manufacturing and trade sales (through November) and its component real retail sales (through December) have turned down. Real personal income less transfer receipts just made a new high; but, on the other hand, is inflation-adjusted and thus heavily influenced by the price of gas.

The 4 things to watch for on Friday

Which leads us back again to employment. All of the employment-related short leading indicators will be updated by the end of this week, particularly in the jobs report. Let's review them in turn.

1. Construction employment

While housing permits and housing starts have turned down sharply, mainly due to supply bottlenecks, units under construction have not turned down yet. This is important because in the past, as shown below, they have also turned down significantly in advance of the onset of any recession:

Building permits vs. construction ((FRED))

{kind=link}

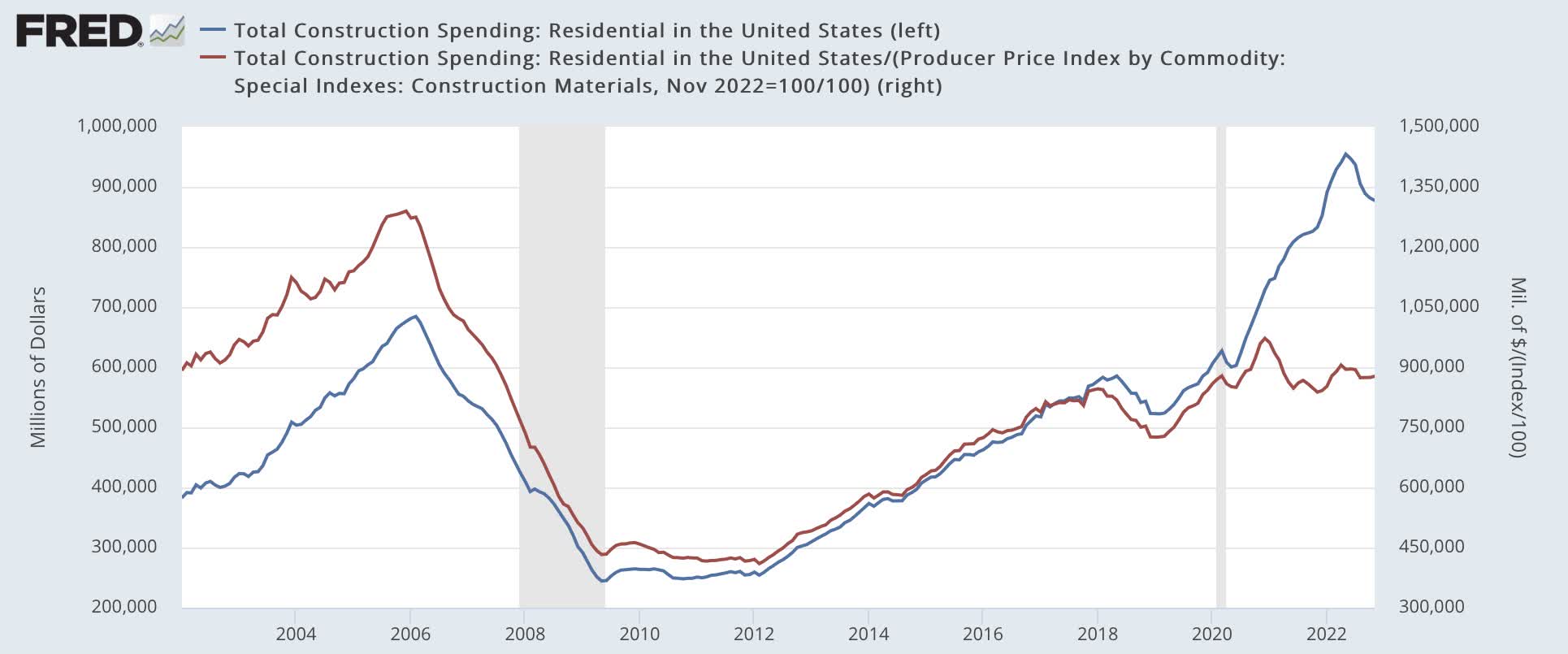

Also, while residential construction spending in nominal terms has turned down in nominal terms, if we adjust for the price of building materials, the downturn has not nearly been so dramatic:

Nominal vs. real residential construction spending ((FRED))

{kind=link}

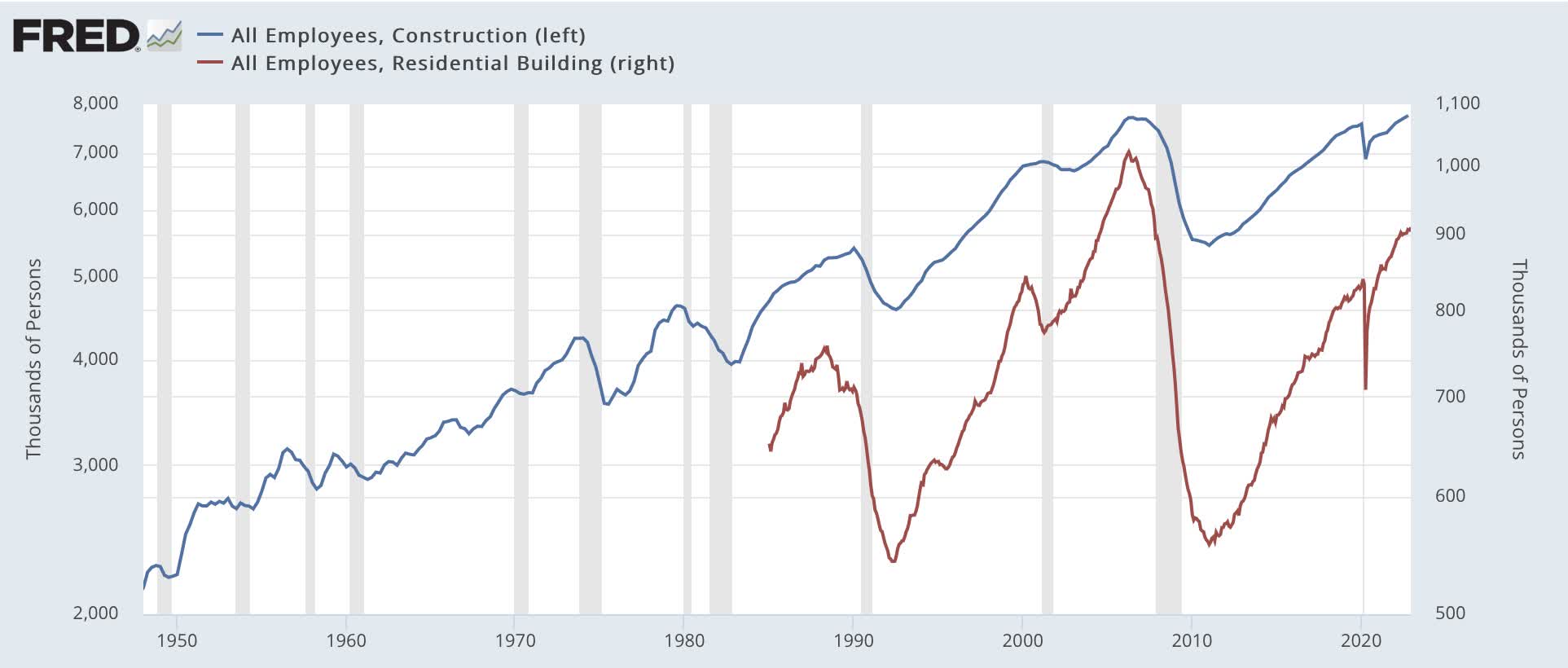

With record construction still occurring, residential construction employment (red in the graph below) has continued to increase. In the past, it has turned down significantly before a recession has begun. The more general category of all construction employment (blue) has either turned down or at least remained flat for several quarters before a recession has begun:

Residential and total construction employment ((FRED))

{kind=link}

Neither measure of construction employment had turned down as of December.

2. Manufacturing employment

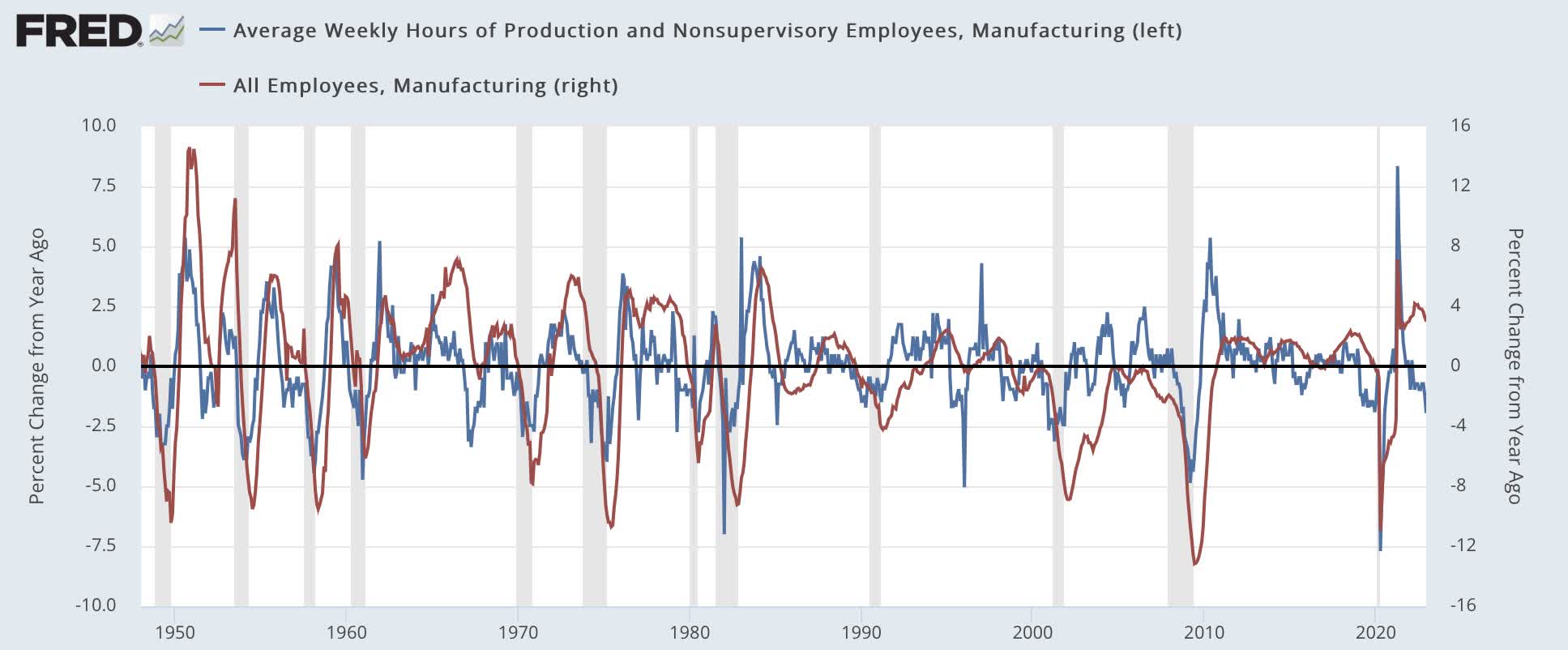

Manufacturing employment sustained a big structural downturn from 1980 through 2012, so its cyclical trend is obscured by that measure. Its cyclical component is best viewed YoY.

One long-time component of the Index of Leading Indicators is the manufacturing work week (blue in the graph below). Employers typically only cut manufacturing jobs (red) after hours have already been cut back, as shown in the YoY graph below. Put another way, manufacturing hours lead manufacturing jobs:

YoY Manufacturing workweek vs. employment ((FRED))

{kind=link}

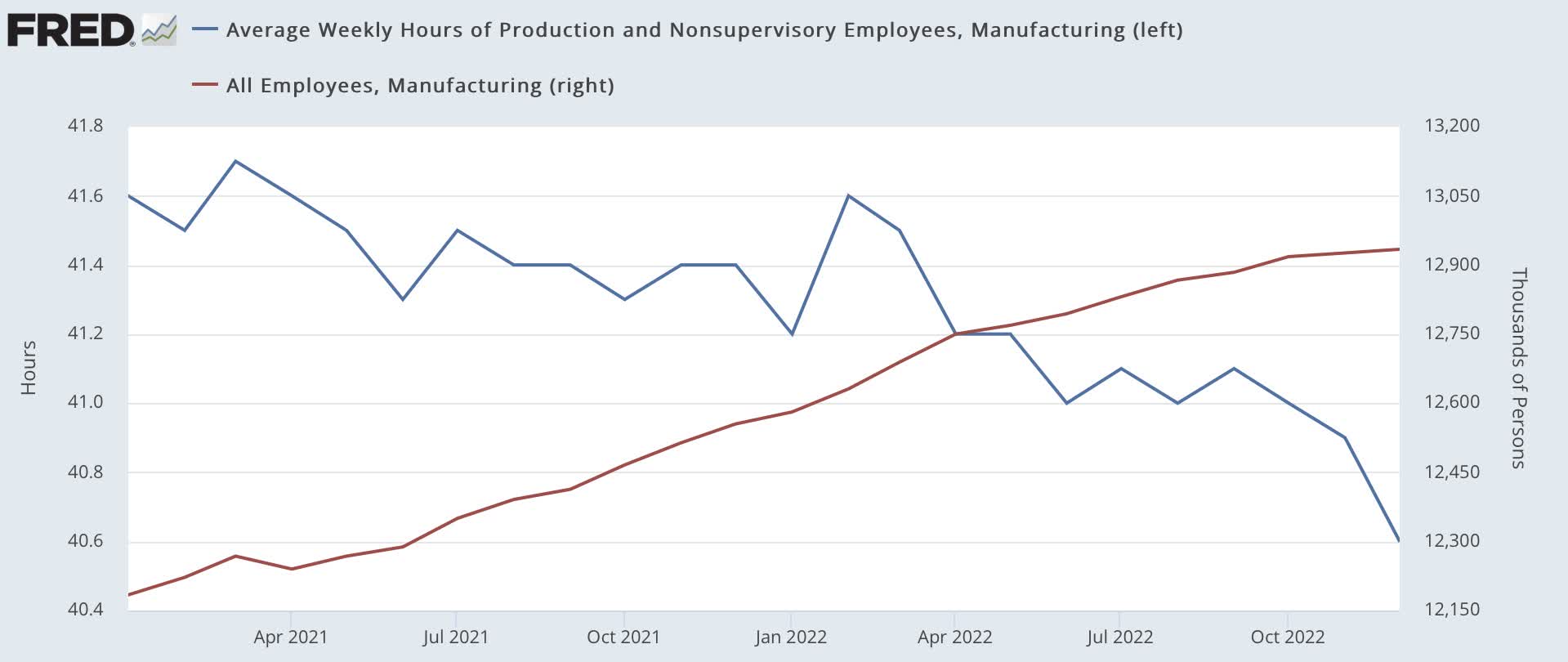

Zooming in on the past year in absolute terms, the manufacturing work week is already in plain recessionary territory. But manufacturing employment through December was still increasing slightly, although at a much slower rate:

2022 manufacturing work week vs. employment ((FRED))

{kind=link}

3. Short-term unemployment

The number of persons unemployed for less than 5 weeks (blue in the graph below) is a self-explanatory metric, noisier than but similar to the measure of initial jobless claims (red):

Short-term unemployment vs. initial claims ((FRED))

{kind=link}

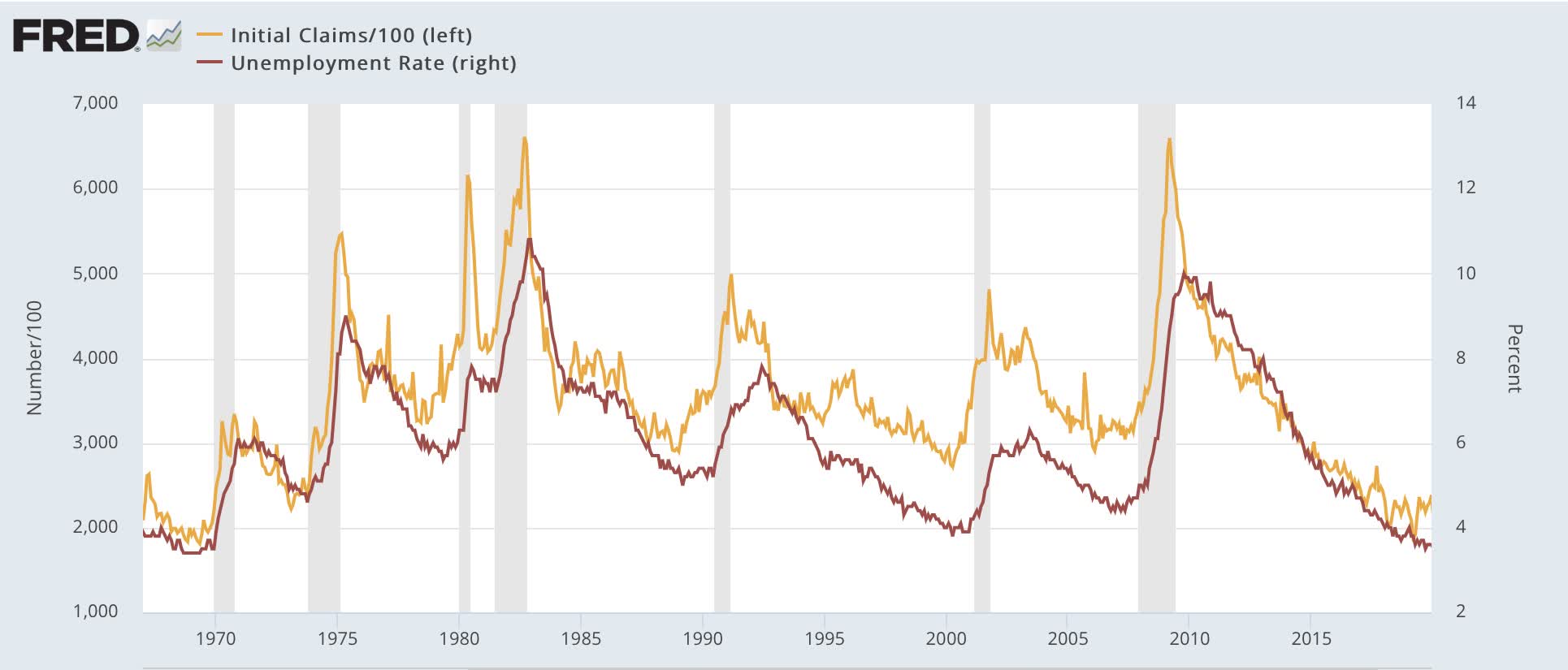

Further, initial jobless claims have a long-standing short leading relationship to the unemployment rate:

Initial claims vs. unemployment rate ((FRED))

{kind=link}

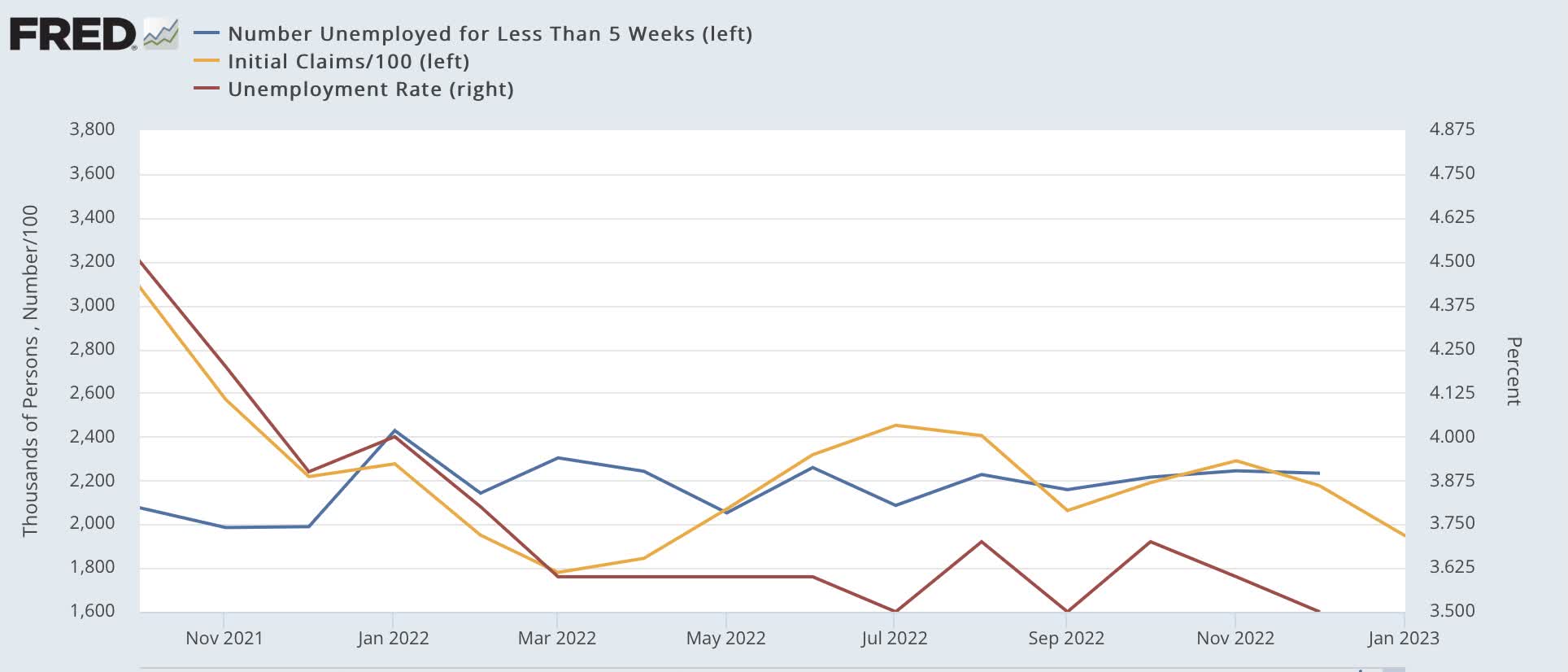

A close-up on the past year+ shows that short-term unemployment made a low in autumn 2021, but has not turned up more significantly in about 9 months. Meanwhile, new jobless claims rose slightly into the summer and autumn, but in recent weeks turned down again (possibly an artifact of seasonality, as less Christmas hiring means less January firing):

2022 initial claims, short-term unemployment, and unemployment rate ((FRED))

{kind=link}

4. Real aggregate payrolls for nonsupervisory employees

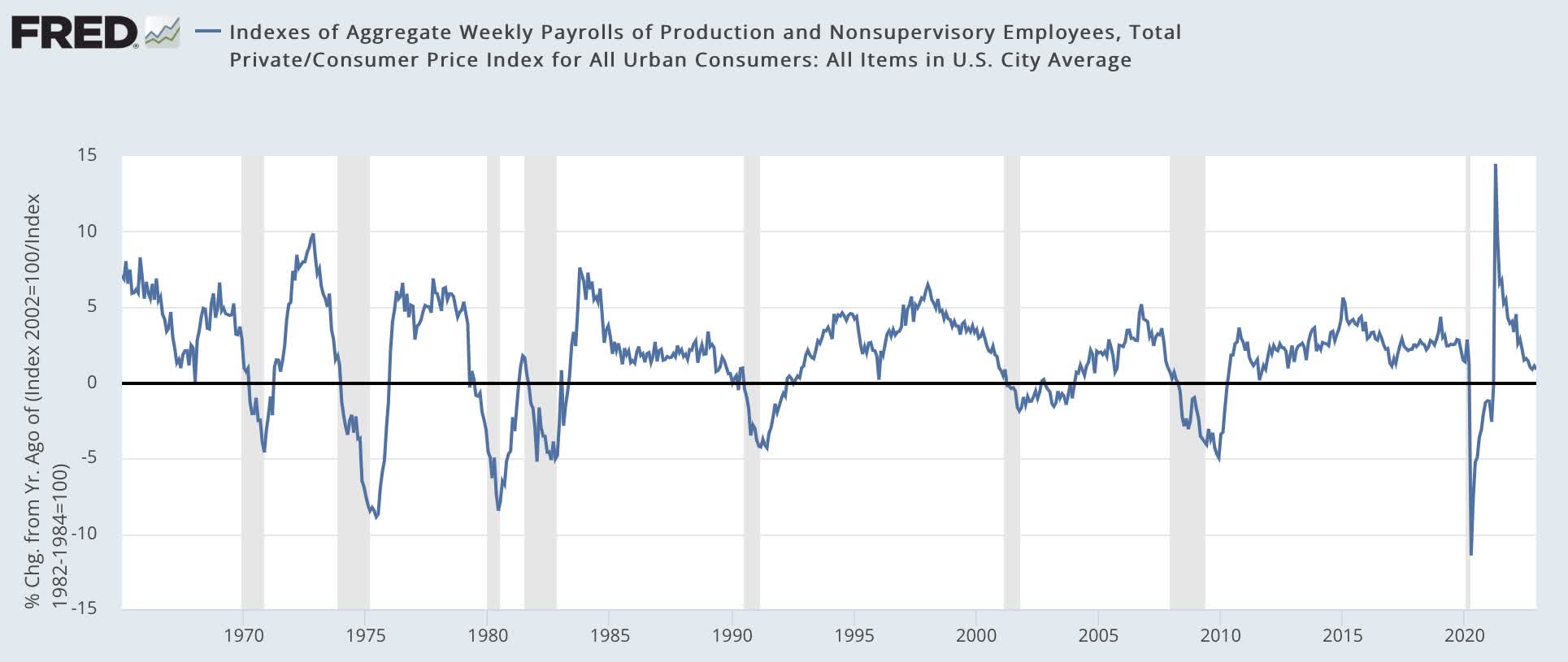

As noted above, once short leading indicators have turned down, we look to the performance of coincident indicators. And there is one element of the employment report which has been an excellent coincident indicator for recession: whether YoY real aggregate nonsupervisory payrolls have turned negative:

Real aggregate nonsupervisory payrolls ((FRED))

{kind=link}

This indicator also has the advantage of being grounded in the fundamentals. If average Americans, in the aggregate, have less in real terms to spend, they can be expected to cut back their spending. And since that spending is 70% of the entire economy, a cutback in that spending ought to be a marker of recession. And as shown above, indeed it is.

Also, as shown above, after declining sharply for the past several months, real aggregate payrolls have hovered at just below +1% YoY. Friday won't give us the inflation rate, but it will tell us what the nominal YoY number is. In January last year, aggregate payrolls went up +0.6%, as did inflation. Any nominal number below that means that inflation must be similarly lower, or the YoY comparison will worsen.

Plus, Revisions!

Although not a component of leading or coincident indicators, be aware that this Friday the BLS will revise its job numbers for the past 3 years. There could be some real surprises, as the comprehensive QCEW, which measures 95% of all employers' reports, rather than just a sample, indicated stronger growth in 2021 and Q1 2022 than the payrolls report, but sharply lower growth in Q2 2022 (the data last reported). If the BLS adjusts to harmonize with the QCEW data, then 2022 employment may look very different after Friday than it has looked up until now.

Conclusion

To summarize, there are 4 components of the jobs report that will give us important updates as to whether a recession might be beginning now, or remains some months away - or even, possibly, that there will be the much-hoped-for "soft landing."

So this Friday look to see whether construction and manufacturing employment have turned down, and also if the number of short-term unemployed has turned significantly higher. Also pay attention to aggregate payrolls for nonsupervisory workers, keeping in mind that in view of the $0.40 rise in the price of gas during January, the inflation adjustment may be significant. And keep in mind that these values may all be affected by some significant adjustments to the 2022 data.

For further details see:

4 Things To Watch For In Friday's Employment Report