BRW - 5 Closed-End Fund Buys In The Month Of December 2023 (Plus 1 Sell)

2024-01-16 05:02:15 ET

Summary

- Equity and fixed-income markets had another strong month in December, driven by continuing retreating risk-free Treasury rates.

- We even saw an improvement in the breadth of the overall market, with broader participation lifting some of the beaten-down sectors for the year.

- That said, closed-end fund discounts remain historically wide, and that continues to drive opportunity in the CEF wrapper.

December turned out to be another strong month for equity and fixed-income markets once again, carrying over the momentum in November. The driving factor was risk-free Treasury Rates continuing to recede.

Across the board, equities rallied over the last month, but it was more tilted toward those companies that are relatively smaller. The large and mega-caps did participate in the upside and put in a really strong 2023 overall.

U.S. Equity Performance 12/31/2023 (Seeking Alpha)

A good portion of those gains was attributed to a relatively narrow basket of names, the Magnificent 7, but broader participation picked up at the end of the year. We can see that reflected if we compare the SPDR S&P 500 ( SPY ) and Invesco S&P 500 Equal Weight ETF ( RSP ).

I believe that RSP is a better representation to illustrate equity performance as it applies more weight outside of just the select few names. Being up nearly 12%, RSP certainly did well - even more if factoring in dividends for a total return. However, that's less than half of what SPY put up for performance.

Ycharts

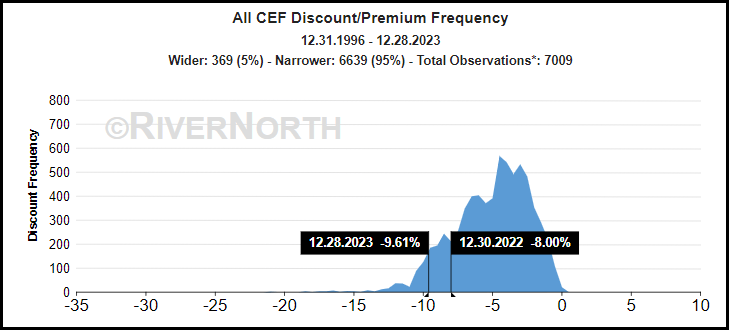

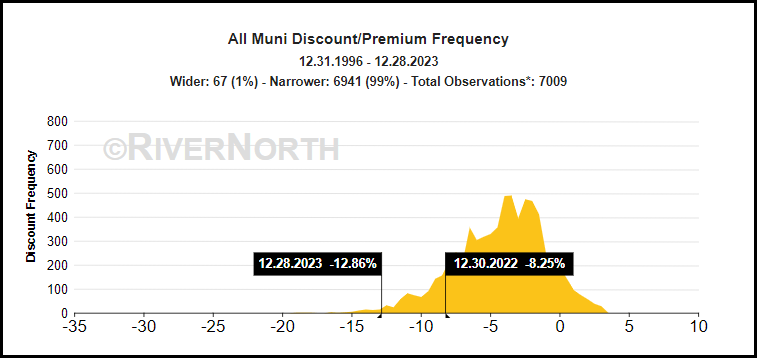

Despite that being the case, discounts overall in the closed-end fund space didn't see a significant change in the last month. That's kept them at some of the historically widest discounts in history. In fact, if we are being picky, last month when I put together this article, the overall discounts for CEFs came to -9.47%, so we've seen discounts even widen a touch. That means there are still great bargains to be had in this investment wrapper. In particular, municipal bond CEFs are at the deepest absolute and relative discounts.

{kind=link}

Over time, I look at my closed-end fund portfolio to grow my monthly cash flow. This works through putting new capital to work and reinvesting the steady cash that comes in monthly as well. This has a compounding snowball effect over time. The more capital that is put to work, the larger the ball of monthly cash becomes.

I picked up or added to 5 different closed-end fund positions throughout December. However, I also sold out of BlackRock Floating Rate Income Strategies Fund ( FRA ) , which I discuss further below.

Nuveen AMT-Free Municipal Value Fund ( NUW )

Speaking of municipal bond CEFs, NUW was the first purchase of the month. For those who have been following along with this monthly series of articles, you'll already know this was a position for me, and I've been accumulating it throughout the majority of this year. The reason is quite simple: as rates are and have come down, NUW should perform well - clawing back some of the significant drops from when rates ramped up significantly.

At the same time, it's a very low leveraged fund, currently around a 1% leverage ratio, but allows for only up to 10% leverage. That helps keep risks even more minimal for an already low-risk muni exposure. The discount is a cherry on top, and as mentioned above, muni discounts are basically the widest discounts they've ever been since going back to 1996.

{kind=link}

NUW's discount reflects this as well and is one that is pushing its all-time low discount level, excluding the Covid panic.

Ycharts

Finally, the worst-case scenario is rates start heading higher once again, making the price drop precipitously, and I'm stuck with a ~4% tax-free cash flow. I can think of worse things than collecting tax-free income, even at a 'mediocre' rate.

Special Opportunities Fund ( SPE )

SPE is a fairly unique fund that attempts to capture the prowess of Bulldog Investor and Phillip Goldstein. Though they aren't really quite as active as Boaz Weinsteins Saba Capital group, they can sometimes be an 'accomplice.' Some of the funds you see Saba Capital building a position in can overlap with Bulldog Investors. In that way, they can help each other in terms of getting further control of the fund and both benefit from whatever potential outcome is to be had.

Saba Capital offers its own CEF with Saba Capital Income & Opportunities Fund ( BRW ), which is ironically a fund that they took over entirely, similar to Bulldog and how we got SPE today. SPE was previously a municipal-focused fund under a different name, but Bulldog took over in late 2009. However, while I own BRW also, the discount for SPE is pretty spectacular. It made it a no-brainer as to which 'activist' fund I was looking at picking up more exposure to. Also, it's a little ironic as it would be a target for an activist group with such a wide discount.

Ycharts

SPE is leveraged, and I've been mostly avoiding adding too much in the way of leverage throughout 2023 due to the higher rate environment; this is a fixed-rate leverage. It comes in the form of a publicly traded convertible preferred offering ( SPE.PR.C ) at what can only be one of the most envious rates we can see in the space, paying a dividend rate of 2.75%. It comes with future dilution that will dilute the NAV, but at this cost, it should easily be negated by what should be better performance.

SPE NAV at time of writing (Special Opportunities Fund)

OFS Credit Company ( OCCI )

To reiterate, I had mostly been taking 2023 as a way to reduce risk and de-leverage my overall portfolio. That said, when OCCI switched to a monthly distribution policy and is trading at a massive discount relative to its peers, I did have to jump in and take a speculative position. All NAV estimates listed below are as of November 30, 2023.

| CLO CEFs |

| Ticker |

| Notes |

| Price |

| Nav |

| %Change |

| Yield |

| P/D |

| ECC |

| ~100% CLO equity |

| $9.50 |

| $8.88 |

| -0.73% |

| 17.55% |

| 6.98% |

| OXLC |

| ~100% CLO equity |

| $4.94 |

| $4.75 |

| 0.00% |

| 19.43% |

| 4.00% |

| OCCI |

| ~100% CLO equity |

| $6.46 |

| $7.63 |

| -0.46% |

| 18.58% |

| -15.33% |

| CCIF |

| ~100% CLO equity |

| $7.95 |

| $8.04 |

| 0.89% |

| 15.00% |

| -1.12% |

A discount for OCCI is likely due to the relatively weaker performance. That said, given that the fund has gone to a large discount, that is working against the fund's share price results. So that's a bit of a vicious cycle; a wider discount makes it appear an even worse performer, relatively speaking, which could cause more and more investors to sell. ECC and OXLC are still trading at premiums, albeit their premiums have even come down from the levels we've historically seen them.

Ycharts

The fund had also been running with a quarterly distribution policy for a number of years when its equity CLO peers paid monthly. It had also been a more unusual policy of part cash but mostly additional stock. I believe that the new monthly all-cash distribution policy is more appealing, and that could see investors' interest perk up.

Worth noting the leverage here is also fixed-rate through various preferred stock issuances. That's similar to SPE, but not as envious of rates. That keeps it at one less moving variable part to consider for this fund.

It also wasn't directly related, but shortly after picking up a position in OCCI, I sold my position in BlackRock Floating Rate Income Strategies Fund ( FRA ) . I also held that fund in my tactical portfolio to hedge the higher rate environment, picking up shares through mid-2022. With rates looking set to move lower, its job is done. I was able to cash out on the ex-distribution date and at a profit. The discount for the fund also wasn't particularly attractive at only around 5%, which made it even easier to let go.

That said, I also realize that OCCI should perform better in terms of income generation during a higher-rate environment, so that was essentially a wash from that angle. Still, the idea would be to see if OCCI can get itself to a higher premium than its admittedly stronger peers enjoy.

BlackRock Health Sciences Term Trust ( BMEZ ) and abrdn Healthcare Investors ( HQH )

I'll lump these two together because they were picked up for the exact same reasons. I added to my position in BMEZ, and then a few days later, I finally capitulated and purchased HQH. Similar to OCCI, despite wanting to limit adding any further names to my portfolio to have to keep track of, sometimes the price is just too right.

I've also covered both of these funds quite recently; for those interested in either BMEZ or HQH , those could be worth reading through. Neither of these funds employs leverage in the form of borrowings, but BMEZ does have a covered call-writing component.

HQH is a 'new' name to my portfolio, but not entirely new; I owned it in the past. I sold it when the discount narrowed in August 2021. In fact, the specific day was August 10, 2021, which CEFConnect says the discount was a meager -1.32%. I missed out on selling a week or so later when it touched a premium, but that happens sometimes.

Ycharts

Overall, BMEZ is in the same boat with a massive discount. It's a much newer fund, but similar to HQH, it places a heavy emphasis on biotech exposure.

Ycharts

The biotech exposure sets these funds apart from their healthcare-related peers. Healthcare is often associated with a more defensive sector. Instead, just like the technology sector, the bio technology sector can get a bit wild with significantly more volatility. Below is a look back at the last 3 years between the SPDR Biotech ETF ( XBI ) and the Health Care Select Sector SPDR ETF ( XLV ).

Ycharts

The sector has been out of favor for a few years now; in 2021 and 2022, the sector was beaten down massively. In 2023, it actually performed better with at least positive results. That said, it is still far from making any sort of full recovery from the beatings it took in the prior two years. The 3-year annualized returns for XBI come to around -14% for some further perspective. While the traditional healthcare names have performed significantly better in this period, even those names have been moving sideways. In 2023, XLV is essentially flat for the year.

With any potential recovery in biotech, BMEZ and HQH should perform well. BMEZ has around 45% of its portfolio in biotech, and HQH has 60.5% of its portfolio exposure in the space. That leaves the rest of their portfolios in the more traditional healthcare names that I also believe can do well after the sideways moves throughout the last year.

Further, when/if biotech comes back into favor, it will likely see the fund's discounts narrow. While waiting, both pay out a distribution to investors. BMEZ's is based on a 6% NAV managed plan that is paid monthly, and HQH pays a quarterly distribution based on an 8% NAV policy.

For further details see:

5 Closed-End Fund Buys In The Month Of December 2023 (Plus 1 Sell)