JEPI - 5 Impressive High Yield Ideas For A Healthy Retirement

2024-01-08 21:10:55 ET

Summary

- Public Storage is a favored REIT due to its strong traditional free cash flow, excellent free-cash-flow coverage of its payout, and attractive self-storage sector dynamics.

- Altria Group offers a high dividend yield that is covered by traditional free cash flow, making it a potentially strong option for income investors.

- Dividend Aristocrat Enterprise Products Partners boasts attractive investment-grade credit ratings that back its dividend payout.

- Derivative income ETFs have changed the game for income investors. The JEPI and JEPQ should be on all income investors' radars.

By Brian Nelson, CFA

The financial industry has continued to innovate and now offers high dividend income ideas that do not necessarily depend on a company's healthy levels of free cash flow to cover the payout. Unique derivative income strategies that can be purchased via exchange traded funds [ETFs] have largely replaced the need for many investors to hold risky high dividend paying stocks, which are more susceptible to dividend cuts given their net debt heavy balance sheets and meager ability to generate free cash flow to sustainably pay dividends.

When it comes to corporate equities, we tend to like companies that are overflowing with cash-based sources of intrinsic value: net cash on the balance sheet and future expectations of free cash flow. Many companies with these attributes, however, don't necessarily generate lofty dividend yields. It's usually the worst of companies that have the highest of yields. In the past, we often pondered how investors could gain access to great free-cash-flow rich companies, but with a fantastic high yield income stream to boot. Today, derivative income ETFs do just that, holding some of the strongest companies while selling covered calls on these same companies or a representative index to generate a nice income stream.

In the past, we've written about how investors should avoid a couple Dividend Aristocrats such as Walgreens ( WBA ), which recently cut its payout, in this article , and while we still like many corporate equity yielders that generate free cash flow in excess of cash dividends paid, the case for many derivative income ETFs in an income portfolio has perhaps never been stronger. In many ways, we've never been more excited about income ideas that seek to capture the best of both worlds: capital appreciation potential with income generation, as many high yielding corporate equities have been lacking in this regard. Many high dividend yielding stocks just erode away with each dividend payment, " Don't Destroy Wealth One Dividend At a Time ."

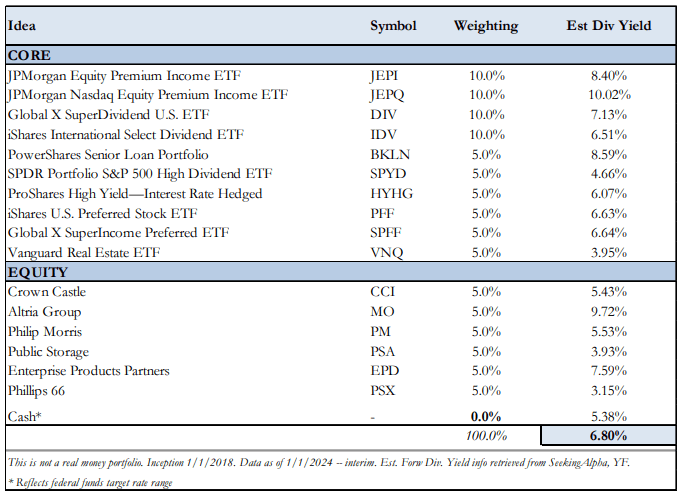

In this article, we'll examine three of our favorite corporate equity income ideas, and two of our favorite derivative income ideas. We think these ideas are far better than corporates or other equity ideas that have lofty net debt positions and/or fail to generate sufficient free cash flow to cover their payouts. These five ideas are also included in our simulated High Yield Dividend Newsletter portfolio that we make available each month to members of our service. That simulated High Yield Dividend Newsletter portfolio can be found below.

{kind=link}

Valuentum's High Yield Dividend Newsletter portfolio. (Valuentum)

Public Storage ( PSA )

Public Storage reported better-than-expected third-quarter performance on October 30 and upped its outlook for core funds from operations (FFO) for 2023 to the range of $16.60-$16.85 from $16.40-$16.80 per share. Among the REIT sub-sectors, we continue to like the self-storage space mostly because of its traditional free cash flow dynamics, as measured by cash flow from operations less all capital spending, are much more attractive.

For the first nine months of 2023 , Public Storage generated $2.45 billion in operating cash flow and shelled out $572 million in capital expenditures and outlays to develop and expand real estate facilities, resulting in free cash flow of ~$1.88 billion, better than the distributions paid to common shareholders and noncontrolling interests over the same time period. Many REITs fail to cover their dividends with traditional free cash flow, but Public Storage has shown a unique ability to do so.

Self-storage REITs can also be viewed as generally recession-resistant, and offer high operating margins and generally lower maintenance capital requirements. Public Storage is one of our favorite REIT ideas and yields ~5% at the time of this writing. Shares of PSA haven't done as well as the broader market as it has been lumped in with most equity REITs during the past several years, and while we expect a challenging market environment for equity REITs for the foreseeable future (given rising interest rates), we view Public Storage as the best long-term idea in the attractive area of self-storage.

Altria Group ( MO )

We recently wrote the following about Altria on our website:

Altria Group’s forward estimated (9.5%) dividend yield is too hard to pass up as it is comfortably covered by traditional free cash flow. The tobacco giant reported third-quarter 2023 results on October 26 that showcased how its asset-light business model continues to throw off tons of cash. Traditional free cash flow generation came in at ~$5.9 billion during the first nine months of 2023 , while cash dividends paid came in at ~$5 billion, resulting in a very nice free cash flow cushion on a ~10%-yielding stock.

Though revenue growth at Altria remains under pressure, gross profit continues to move in the right direction. Altria has raised its dividend 58 times during the past 54 years, and the firm continues to target mid-single-digit dividend growth annually. For income investors that aren’t worried about ESG-related criteria, Altria could make for a great diversifier in a high-yield dividend income portfolio. Our fair value estimate stands north of $60 per share (shares are trading under $40 at the time of this writing).

Altria's shares have continued to languish as investors remain concerned about the longevity of its combustible tobacco portfolio, but we think shares offer a nice risk/reward for income investors. A company that is generating sufficient free cash flow to cover its payout and also has financial flexibility through the partial ownership of AB InBev ( BUD ) and Cronos Group ( CRON ) is in much better shape than its dividend yield suggests. Altria is not without troubles, but for a 9%+ dividend yield, we think the stock is definitely worth considering for income investors.

Enterprise Products Partners ( EPD )

The following from our website explains the case for Enterprise Products Partners:

Though, in general, we’re not too excited by the midstream pipeline space given their capital-intensive nature and hefty net debt positions, Enterprise Products Partners has a lot of things going for it. The company boasts investment-grade credit ratings (A-/A-/A3), has strong and consistent returns on invested capital, and has put up 25 years of consecutive distribution increases.

In addition to growing its payout in each year for more than two decades, management has done a great job reducing its leverage ratio (net debt adjusted for equity credit in its junior subordinated notes divided by adjusted EBITDA). For the trailing twelve months ended in the third quarter, its leverage ratio has fallen to 3.0x from 4.1x in 2017.

All told, we think Enterprise Products Partners’ growth initiatives will help to solve revenue pressures, and we expect the company to continue to drive distribution growth in the coming years as it keeps its leverage in check.

Years ago, midstream pipeline companies were spending like mad, driving traditional measures of free cash flow to levels below that of their dividends and distributions. A lot has changed since the middle of last decade, and many midstream equities are now covering their dividends and distributions with traditional free cash flow. Enterprise Products Partners has a hefty investment program in the coming years, but we would expect the firm's focus on generating value for shareholders to translate into future dividend increases. The Dividend Aristocrat yields ~7.5% at the time of this writing.

JPMorgan Equity Premium Income ETF ( JEPI )

Derivative income ETFs are probably the best innovation in modern finance over the past decade, even better than proliferation of Bitcoin and the blockchain, in our view. The JPMorgan Equity Premium Income ETF pursues a fundamentally-based active strategy investing in U.S. large cap stocks, while writing out-of-the-money S&P 500 Index call options to generate monthly income, along with the dividends it collects on its long positions.

Based on the last check on its website, the firm has provided a 12-month rolling dividend yield of ~9.82%, a hefty level, which it has been able to achieve while holding exposure to some of the strongest fundamental names, including Microsoft ( MSFT ), Amazon ( AMZN ), and Visa ( V ). It's truly remarkable that investors can get such a high income stream with exposure to some of the strongest cash-rich names on the market, and for this, the JPMorgan Equity Premium Income ETF is one of our favorite income ideas.

JPMorgan Nasdaq Equity Premium Income ETF ( JEPQ )

The JP Morgan Nasdaq Equity Premium Income ETF is similar to the JEPI above in the sense that it is a derivative income ETF, but there are some important differences. The ETF focuses on stocks in the Nasdaq 100, as it writes out-of-the-money call options on the NASDAQ 100 Index. Including such names as Microsoft ( MSFT ), Apple ( AAPL ), and Alphabet ( GOOG ) in its top holdings, the ETF is still able to drive a 12-month rolling dividend yield of ~12.51%.

The big drawback of the JEPI and JEPQ is that during periods of rapid market increases, the capital appreciation potential may not be as large as that of their underlying, U.S. large cap stocks and the Nasdaq-100, respectively, but this may be worthwhile given just how lofty the dividend yields are on these financial instruments. We're very excited about derivative income ETFs for income, and based on how fast these ETFs have been attracting assets, many other investors are, too.

Concluding Thoughts

Derivative income ETFs have changed the game when it comes to income-oriented ideas. The JEPI and JEPQ have excellent bottom-up focused processes that lead to some of the strongest, net-cash-rich entities to grace their top holdings, while the portfolio managers are able to write out-of-the-money calls on the S&P 500 and NASDAQ-100 indices, respectively. We think the JEPI and JEPQ are game-changers for many income investors.

We've also profiled three equity income ideas. Public Storage is a rare REIT that generates positive free cash flow in excess of its cash dividends paid, while the risk-reward regarding Altria's dividend is tilted strongly in investors' favor. Finally, Enterprise Products Partners boasts some of the most attractive attributes in the midstream energy pipeline space, while it holds onto the coveted label of Dividend Aristocrat. We hope you have enjoyed this article, and thank you!

For further details see:

5 Impressive High Yield Ideas For A Healthy Retirement