RCA - 8 Income Picks For Any Taste With Yields From 5 To 10+%

2023-05-22 17:15:28 ET

Summary

- A brief review of some of the positions we like at the moment.

- Yields ranging from 5% to 10+% in relation to embedded risks.

- In the article, one can find a pick with some "Alpha" for almost any credit rating or duration.

We usually post our articles to members of our service 1 week before we publish them to the public.

At this point, we are four and a half months into 2023, and we have seen quite a bit of action in the markets as a whole and in our small fixed-income universe in particular for this short period of time. The "January effect" started a wild rally in our products, and we witnessed how BBB- and lower-rated perpetuities such as JPM-M, BAC-O, and WFC-D, to name a few, trade at yields well below 5.5%. At the same time, risk-free 30-year Treasury bonds were trading at 3.6%.

In times of an increasing Fed funds rate and markets that were teeming with uncertainty, this trading behavior seemed pretty strange to us. Then March 2023 came out swinging with bank insolvencies and a crisis in the whole banking sector that continues to this moment. Some of the fixed-income products we have loved and cherished through the years are no more and others are struggling to survive. On the other hand, we have products that trade as if they are rated a couple of notches higher and mispriced investment opportunities that are just lagging behind their cousins.

The current market conditions might seem hard for making fixed-income investment choices, but as the sophisticated investor surely knows, it always comes down to juggling the credit risk, duration risk, and position size. As we monitor all of the exchange-traded fixed-income products, we will try to point out which are our best picks, with suitable hedging reactions where needed. The fixed-income issues we will draw your attention to carry credit and duration risks across the spectrum, so we believe investors with different risk tolerances can find among them suitable additions for their portfolios. So let's check them out.

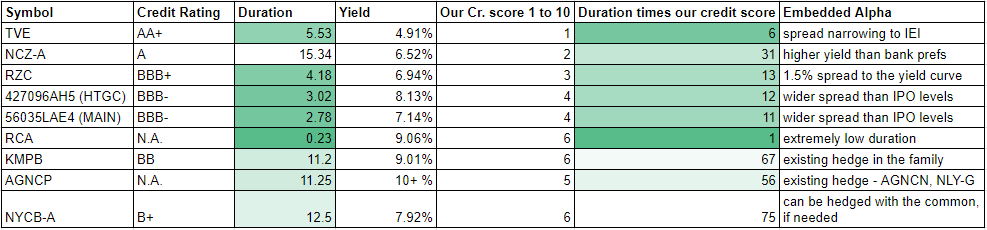

1. TVE, Credit rating: AA+ (S&P), Duration: 5.53, Yield 4.91%

(TVE) and its brother (TVC) are exchange-traded bonds from the federally-owned utility company Tennessee Valley Authority ("TVA").

TVE and TVC data (proprietary software)

{kind=link}

These are among the safest products that trade on the exchange, as they carry almost the same credit risk as the USA itself. We analyze them in more detail in our article , "TVE And TVC The Safest Part Of Our Portfolio." TVE is one of our favorite fixed-income exchange-traded vehicles, and we deem it an "excellent buy" any time its YTM is 1% or higher than its corresponding benchmark treasury bonds. As of the moment of writing this article, TVE's YTM is 4.91% and the 5-year treasury bonds yield is 3.45%. With 6 years left to maturity, TVE has a very limited duration risk. We strongly believe that TVE and TVC are among the best picks for risk-averse investors.

2. NCZ-A, Credit rating: A (Fitch), Duration: 15.34, Yield 6.52%

(NCZ.PA) is a closed-end fund - from Virtus Convertible & Income Fund II ( NCZ ) - issued preferred stock and the regulatory leverage restrictions for the CEFs make it relatively safe from a credit risk perspective.

NCZ-A data (proprietary software)

{kind=link}

NCZ-A was examined in depth in our article " NCZ-A Has Always Been Mistreated. " NCZ-A has a history of being mispriced and the case at the moment is no different. It seems that the market does not fully appreciate the 6.52% CY from a fixed-income vehicle that has way lower credit risk than the bank preferreds, for example. At the time of writing this article, the 30-year Treasury yield was 3.78%, giving NCZ-A a spread of 2.8%.

To get an idea of how much embedded "Alpha" there is in NCZ-A, one may consider comparing it to JPM-D. JPM-D has a CY of 5.87% and stands a couple of notches lower than NCZ-A regarding credit risk. Moreover, being a security of the bank sector, at the moment it is subject to even increased credit risk in regard to the crisis in the whole sector (USB-P was our other hedging choice and it has worked out already). This simple comparison, which should be easily noticeable, gives us a fair idea of how mispriced NCZ-A is. As a perpetuity, NCZ-A carries some duration risks that have to be noted. A thoughtful investor should keep in mind that NCZ-A is a fixed-income vehicle with one of the highest qualities. That fact gives us a lot of reaction to hedge the duration risk among the rest of the exchange-traded perpetuities. Each consideration we made for NCZ-A is also valid for its cousins NCV-A and RIV-A. These three securities carry the same risks and at the moment they trade at similar current yields. They are among our favorite investment picks.

3. RZC, Credit rating: BBB+ (S&P), Duration: 4.18 *, Yield 6.94%

The next product we would like to turn your attention to is a baby bond issued by Reinsurance Group of America, Incorporated ( RGA ) and trading under the symbol (RZC).

RZC data (proprietary software)

{kind=link}

RGA is a prime issuer of debt that we find unlikely to pay the US 5-year treasury rate plus 3.46% on its subordinated debentures. According to us, there is a very high probability that RZC will be redeemed on its call date. The fact that RZC had a brother, RZA (LIBOR + 4.37%), that got called at the end of 2022 gives us additional confidence that RZC should be evaluated based on its yield to call. The combination of 6.94% YTC in 5 years and a BBB+ credit rating from S&P makes RZC a bargain on a relative basis.

RZC has one important merit that our previous pick lacked: it has a very limited duration-induced downside risk. The more the Fed funds rate rises, the more the redemption probability for RZC also increases. That, in our opinion, makes this stock pretty unlikely to trade below par. So we have our hands on an investment product that is offering us an attractive yield for five years, above-average credit safety, and very limited downside potential due to interest rate increases. In our book, we call this a good bargain.

* RZC duration is calculated based on its redemption date(high probability event)

4. HTGC and MAIN OTC bonds, Credit rating: BBB- (Fitch), Duration: 3, Yields 8% and 7%

The next investment opportunity in our focus today is the Sep16'26 HTGC 2.625% bond of the BDC Hercules Capital, Inc. ( HTGC ), with a CUSIP 427096AH5.

interactive brokers

This is a regular bond that does not trade on the exchange but on the bond market and can easily be found by its CUSIP number. Last year we made a full analysis of this bond and if someone is interested in the detailed review, it can be read here : "HTGC - 7% From The Investment Grade Bonds With 4 Years To Maturity." With an 8.13% yield to maturity and an investment-grade credit rating, we have at our disposal a rather attractive investment opportunity. Having left a little more than three years to the maturity date, this product will be exposed to very moderate duration risk.

Somewhat similar to the HTGC bong described above is the Jul14'26 MAIN 3%, one of the business development Company ("BDC") Main Street Capital ( MAIN issues) trading at 7.14% YTM. The Cusip is 56035LAE4.

interactive brokers

Again, this is a regular bond that trades at the bond market rather than the exchange, and one has to work with a broker that allows trading it. Our detailed review from last year can be found here : "The Real Value In MAIN Is In Its Bonds." This investment opportunity is rated BBB- by S&P and its YTM is 7.14% over 3 years. As with the HTGC bond described above, this one presents itself with small downside potential due to its low duration.

5. RCA, Credit rating: N.A., Duration: 0.23, Yield 9.06% (annualized)

(RCA) is a convertible senior note issued by Ready Capital Corporation ( RC ). At the moment of writing this article, it has a YTM of 9.06% over 3 months.

RCA data (proprietary software)

{kind=link}

The baby bond is not rated, but its extremely low duration makes it, in our opinion, an excellent short-term investment opportunity. As long as RC does not default before August 15th this year, we are in a great position to collect one last dividend from RCA. At the moment RC looks healthy enough and we have our share of money invested in their product.

6. KMPB, Credit rating: BB (S&P), Duration: 11.2, Current Yield 8.5%, YTM - 9%, Capital appreciation potential in 1 year - 10%

The logic of (KMPB) is that it has widened its spread in comparison to the higher-rated KMPR bonds. KMPB was issued in March 2022 at a fixed rate of 5.875% which later resets every 5 years at the 5-yr + 4.14%. Just 2 weeks before KMPB, KMPR issued a 10-year bond which is 2 notches higher in credit rating at 3.8%:

{kind=link}

The spread at the time was very close to 2%. Since then KMPR has seen its credit rating downgraded from BBB to BBB- and from BB+ to BB respectively for the 2 securities. And It is kind of normal for credit spreads to widen when credit quality worsens. What is also important to point out is that KMPB is expected to reset at quite a higher rate compared to its nominal yield at first. The 5-yr treasury projection is around 3.4% on the date KMPB resets its nominal rate. This would make the yield spread quite abnormal for KMPB. We believe that the recent selling has been mostly correlated to the general sell-off in exchange-traded fixed-income instruments.

7. AGNCP, Credit rating: N.A., Duration: 11.25 **, Current Yield 7.6%, Capital appreciation potential - 15%.

The next fixed-income product we would like to bring to your attention is (AGNCP) - fixed-to-floating preferred stock issued from AGNC Investment Corp. ( AGNC ).

AGNCP info (proprietary software)

{kind=link}

In our latest Seeking Alpha article , "Annaly And AGNC Preferred Stocks - Crazy Mispricings Create An Opportunity," we made an in-depth analysis of the exchange-traded LIBOR-based fixed-to-floating preferred stocks of two mREITs, AGNC and Annaly Capital Management, Inc. ( NLY ), in an attempt to find mispricing amongst them. Everyone who is interested in the model we used should feel free to check out the article. To cut a long story short, we calculated that AGNCP is deeply undervalued compared to NLY-G, giving potential investors a good capital appreciation opportunity with a decent hedging reaction. AGNCP has the potential for 15% price appreciation in order to trade in line with its cousin NLY-G. At the moment this is one of our largest positions. AGNCO is equally mispriced as AGNCP, but we deem the latter a better buy as it trades at a lower price.

** AGNCP duration is calculated using (USDSB3L30Y=) swap rate. According to many investors, the duration of a floating-rate instrument is equal to the period between two distributions. Calculated in such a way, the duration of AGNCP will be approximately 2. We try to be more practical and give it a duration based on the probability of the yield curve normalizing in which the 10+ year yields are moving way higher than the expected short-term rates.

8. NYCB-A, Credit rating: B+ (S&P), Duration: 12.5 ***, Current yield 7.92%, Capital appreciation potential - 8%.

With all the turmoil in the banking sector, there are a lot of opportunities, riskier than those discussed so far, that are opening up to investors. It will only be fair for us to show you the one we like the most at the moment. The security under consideration is the New York Community Bancorp, Inc. ( NYCB ) fixed-to-floating preferred stock (NYCB.PA).

NYCB-A data (proprietary software)

{kind=link}

NYCB-A made a sympathy fall in price, along with most of the equity and debt in the sector, when the banking system crisis began in March 2023. At the moment it trades at 7.92% CY. That may not seem much for an S&P B+ rated security in a troubled sector, but there is additional information that should be taken into consideration. Since the initial instability, the common stock of NYCB has shown strength and regained its position as of February 2023. As long as the market prices NYCB as if there is no sector risk for it, there should be no such risk for its preferred stock too. This gives potential investors in NYCB-A a hedging reaction in its common stock. This, in our opinion, is still a highly speculative investment opportunity, and the position size should be carefully considered if one decides to engage in it.

*** Same type of swap calculation, as for AGNCP above. If calculated for a floating-rate instrument, the duration of NYCB-A will be approximately 4.

Summary

article summary (personal calculations)

{kind=link}

These are some of our top picks at the moment. The yields are not spectacular as absolute values but do present some "Alpha" when compared to alternatives. What is your best pick?

For further details see:

8 Income Picks For Any Taste With Yields From 5 To 10+%