AGNCO - A Crude Awakening

2023-09-10 09:00:00 ET

Summary

- U.S. equity markets slumped this week as persistent inflation concerns inflamed by a "crude awakening" of global energy prices were aggravated by hawkish Federal Reserve rhetoric and revived trade tensions.

- Finishing lower for the fourth-week in the past six, the S&P 500 declined 1.3%, but losses were steeper across the other major benchmarks, with Mid-Caps and Small-Caps sliding roughly 4%.

- After leading the gains in the prior two weeks, real estate equities and other yield-sensitive segments were under pressure this week as benchmark interest rates climbed back near multi-decade highs.

- It's the best of times for some REITs, and the worst of times for others. Two REITs hiked their dividends this week - casino REIT VICI Properties and strip center REIT Phillips Edison - while West Coast-focused office REIT Hudson Pacific suspended its dividend.

- Hotel REITs rebounded as investors assessed some less troubling forecasts for several major Atlantic storms - including Hurricane Lee - that were previously expected to impact operations at several REITs' East Coast properties.

Real Estate Weekly Outlook

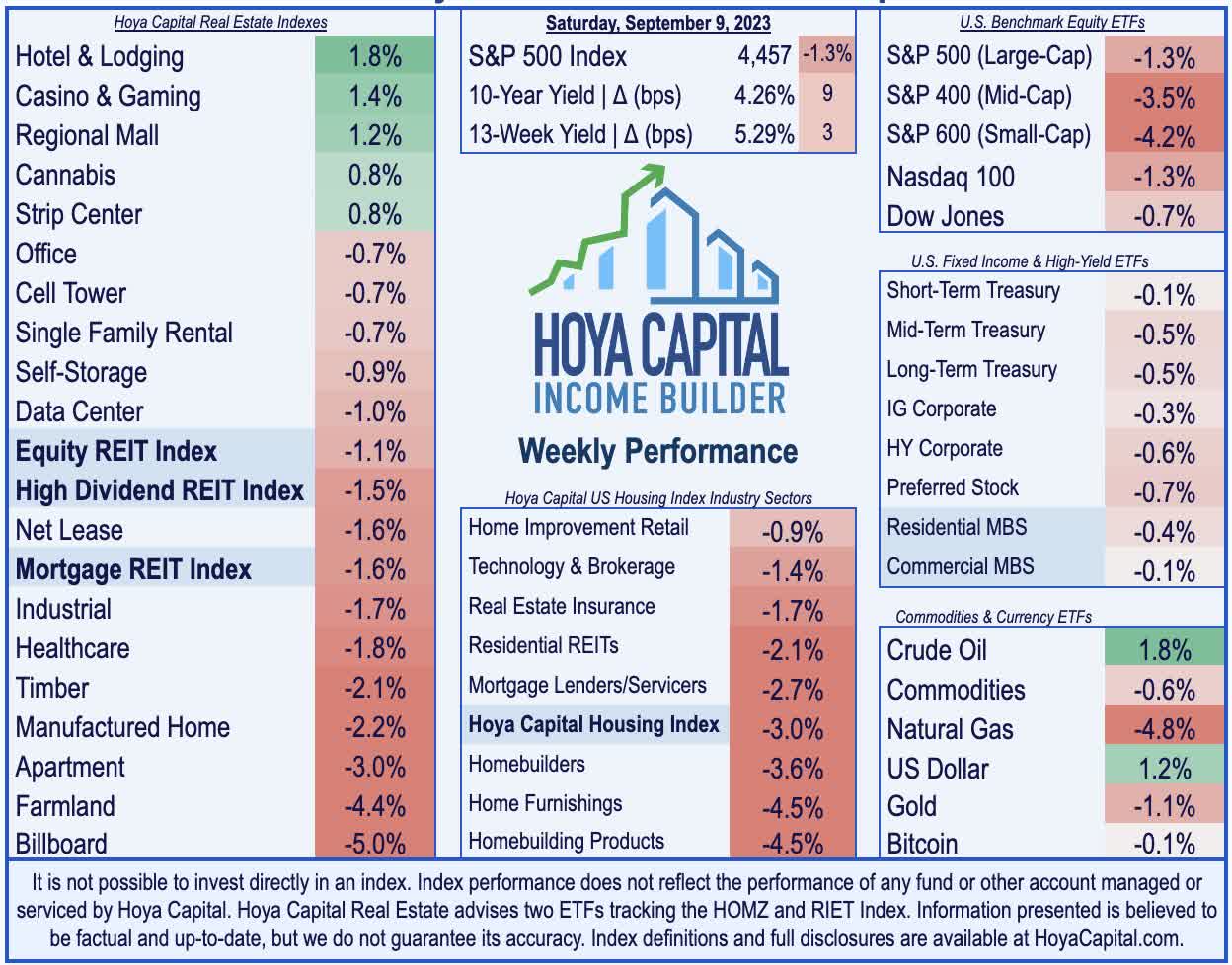

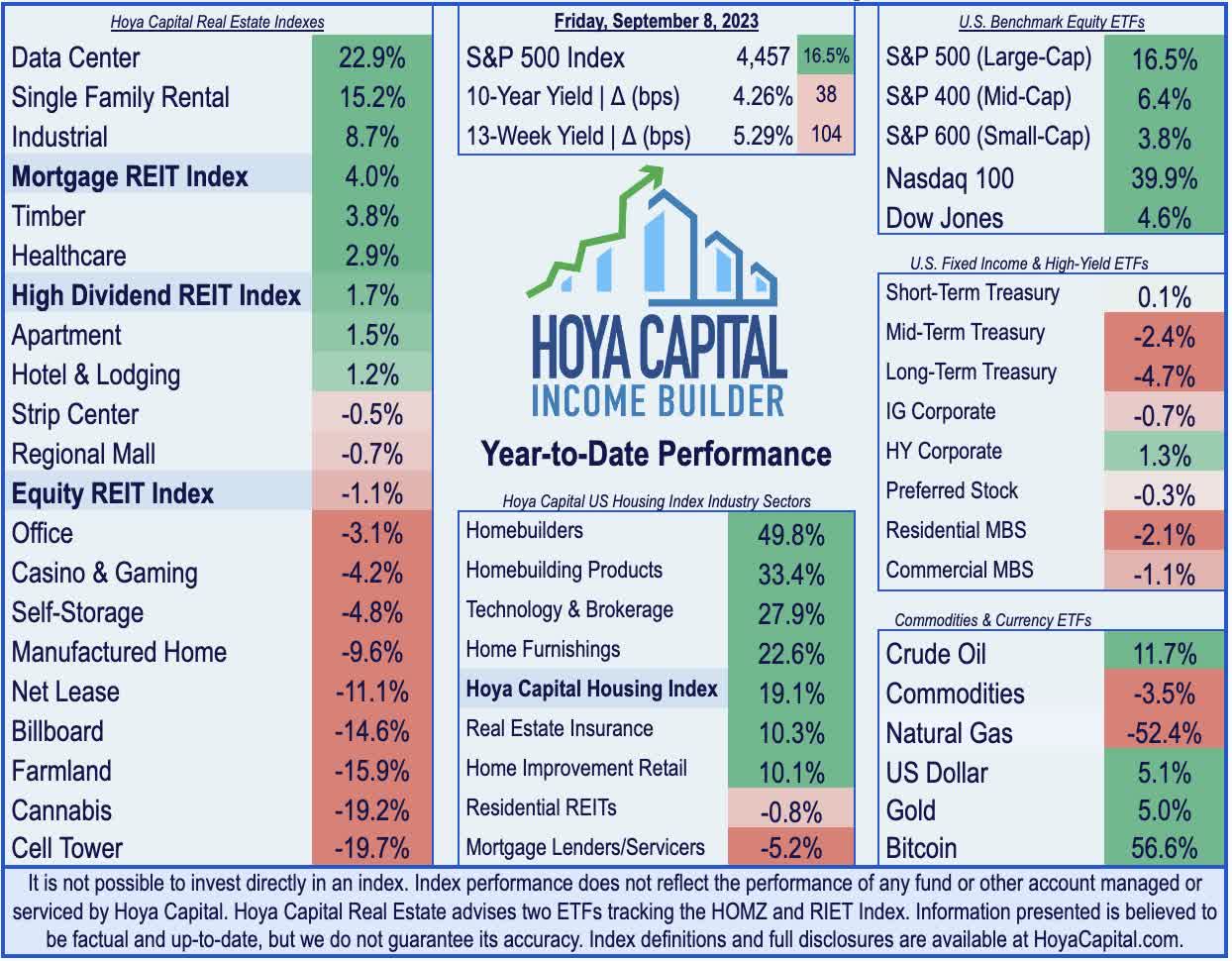

U.S. equity markets slumped this week as persistent inflation concerns inflamed by a "crude awakening" of global energy prices were aggravated by hawkish Federal Reserve rhetoric and revived trade tensions with China. Oil markets - along with the broader energy complex - remained the focus this week as Brent Crude Oil prices rose above $90 per barrel for the first time since last November after several of the largest OPEC producers announced an extension of production cuts to year-end - a move that threatens to stall or reverse the recent favorable disinflationary trends which had been largely fueled by lower energy and transportation-related prices.

{kind=link}

Hoya Capital

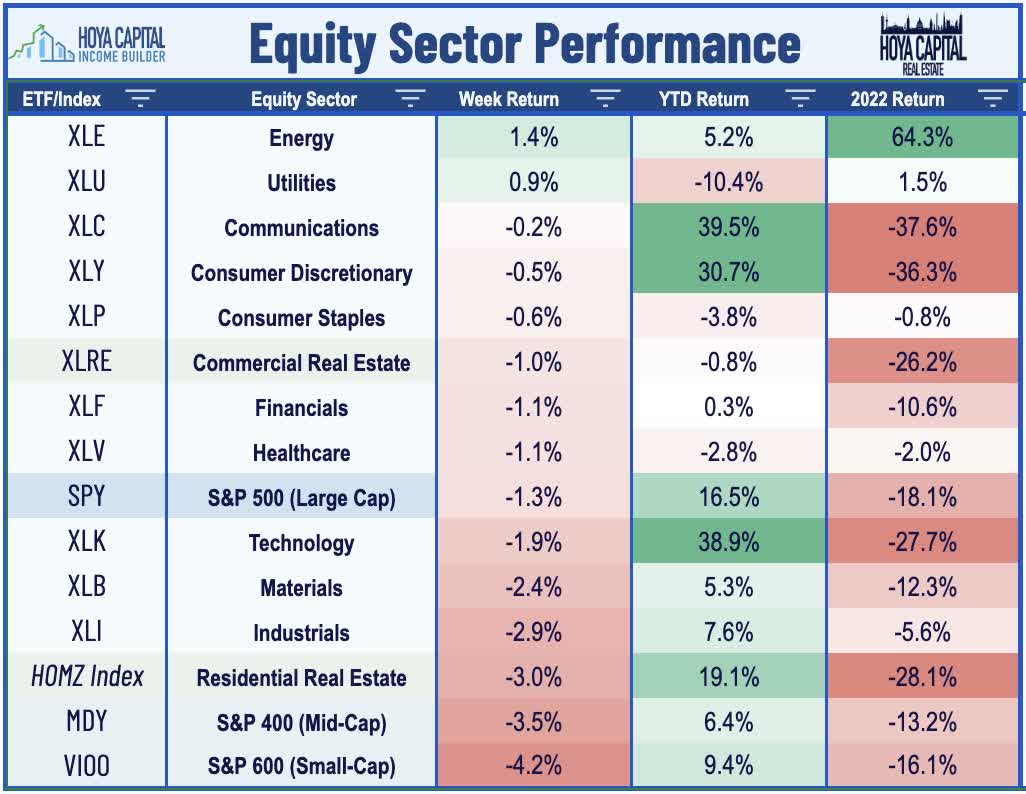

Finishing lower for the fourth week in the past six, the S&P 500 declined 1.3% this week, but the losses were steeper across the major equity benchmarks, with the Mid-Cap 400 sliding 3.5% while the Small-Cap 600 dipped by more than 4%. The Nasdaq 100 slipped 1.3% as tech-heavyweight Apple dipped over 5% after China rolled out iPhone bans for its government agencies, an escalation in the recent tit-for-tat trade disputes. After leading the gains in the prior two weeks, real estate equities and other yield-sensitive segments were under pressure this week as benchmark interest rates climbed back to the cusp of multi-decade highs. The Equity REIT Index slipped 1.3% on the week, with 13-of-18 property sectors in negative territory, while the Mortgage REIT Index slipped 1.6%. Mortgage rate concerns also pressured Homebuilders and the broader Housing Index this week.

{kind=link}

Hoya Capital

With the Federal Reserve entering its "quiet period" on Friday ahead of its FOMC meeting on September 19-20th, indications of weakening growth in Europe and Asia - combined with persistent inflation concerns stateside - lifted the U.S. Dollar to its eighth-straight weekly gain, the longest streak since 2005. WTI Crude Oil prices climbed to nine-month-highs, meanwhile, advancing another 2% this week after Saudi Arabia and Russia agreed to extend voluntary oil production cuts of 1.3M barrels per day. While oil prices remain about 25% below last year's peak levels, both domestic crude oil and consumer gasoline prices are now 30% above their 2023 lows. Further pressured by an expected wave of corporate bond issuance over the next several weeks following the slow end-of-summer pace of activity, the 10-Year Treasury Yield jumped nine basis points this week to 4.26%, while the policy-sensitive 2-Year Treasury Yield climbed by ten basis points to 4.97% - each still slightly below recent multi-decade highs. Energy ( XLE ) and Utilities ( XLU ) stocks led the gains and were the only sectors higher on the week.

{kind=link}

Hoya Capital

Real Estate Economic Data

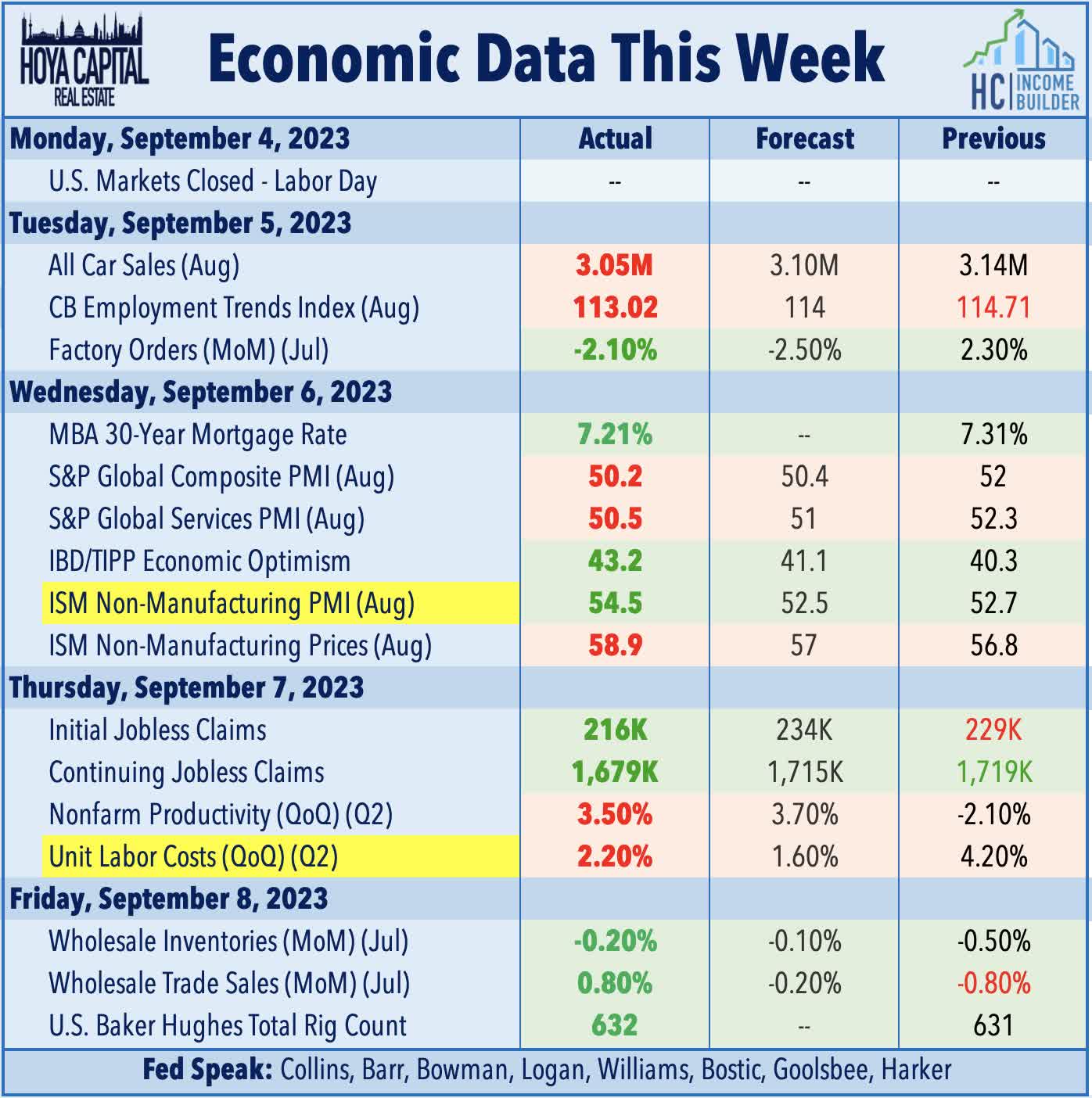

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

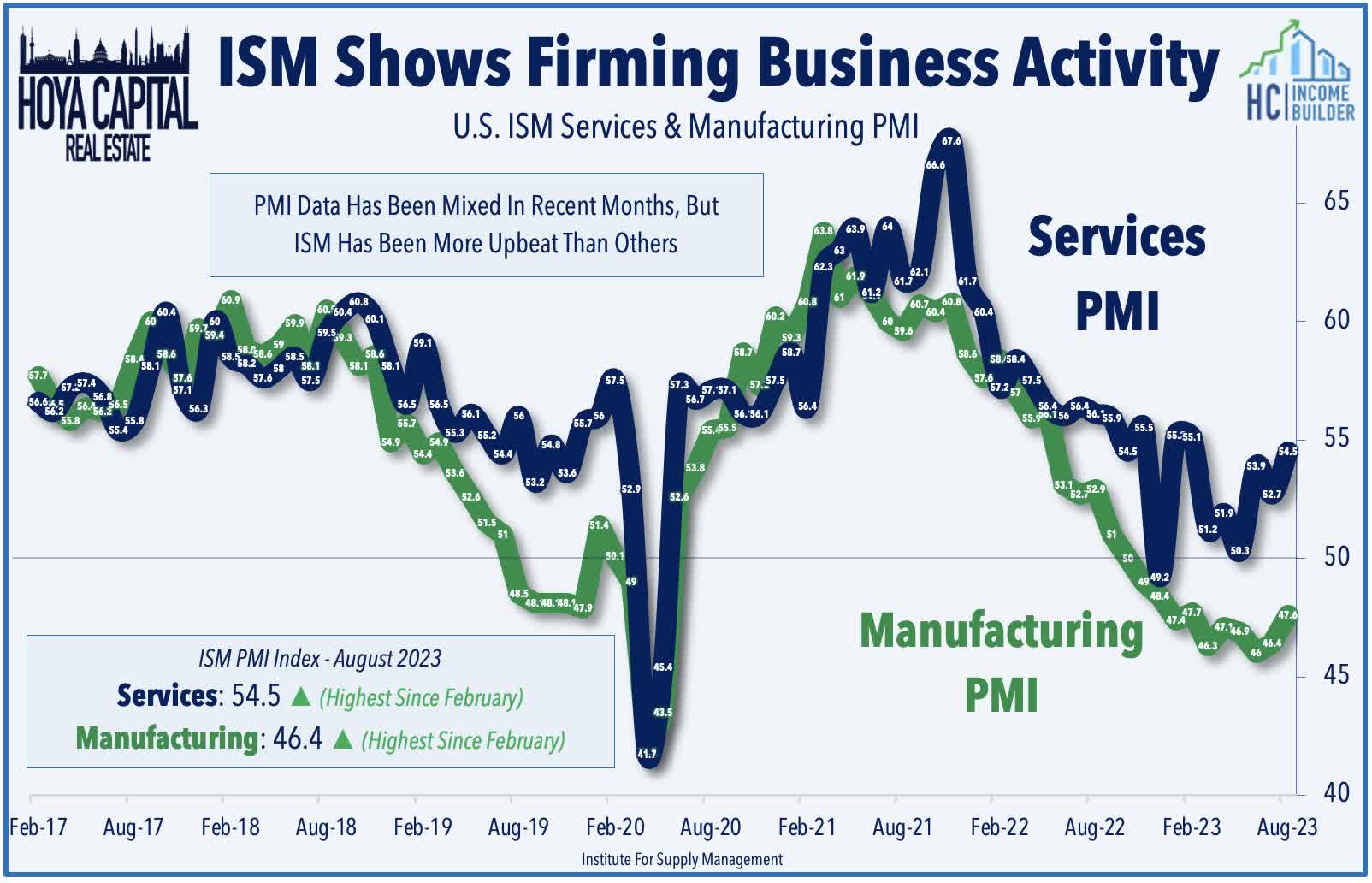

Contrasting with other economic indicators showing a stalling of economic momentum in July and August - including jobs data in the prior week - the ISM Services PMI survey this week showed that activity in services sectors rebounded to a six-month high of 54.5 in August - well above the 52.5 consensus estimate - while the employment sub-index rose to the highest since November 2021. S&P Global's PMI survey released this week was notably less upbeat, however, missing consensus estimates and showing the slowest pace of growth in seven months. Echoing the uptick seen in the ISM report, S&P's Chief Economist noted signs of continued inflationary pressures, however, citing "persistent wage growth" and "renewed upward pressure on energy, fuel and transport costs, as well as some broader firming of materials prices." The closely watched Productivity and Costs Report also showed more inflationary pressures than previously reported, with Unit Labor Costs revised higher to 2.2% in Q2, up from the initial reading of 1.6%.

{kind=link}

Hoya Capital

Equity REIT Week In Review

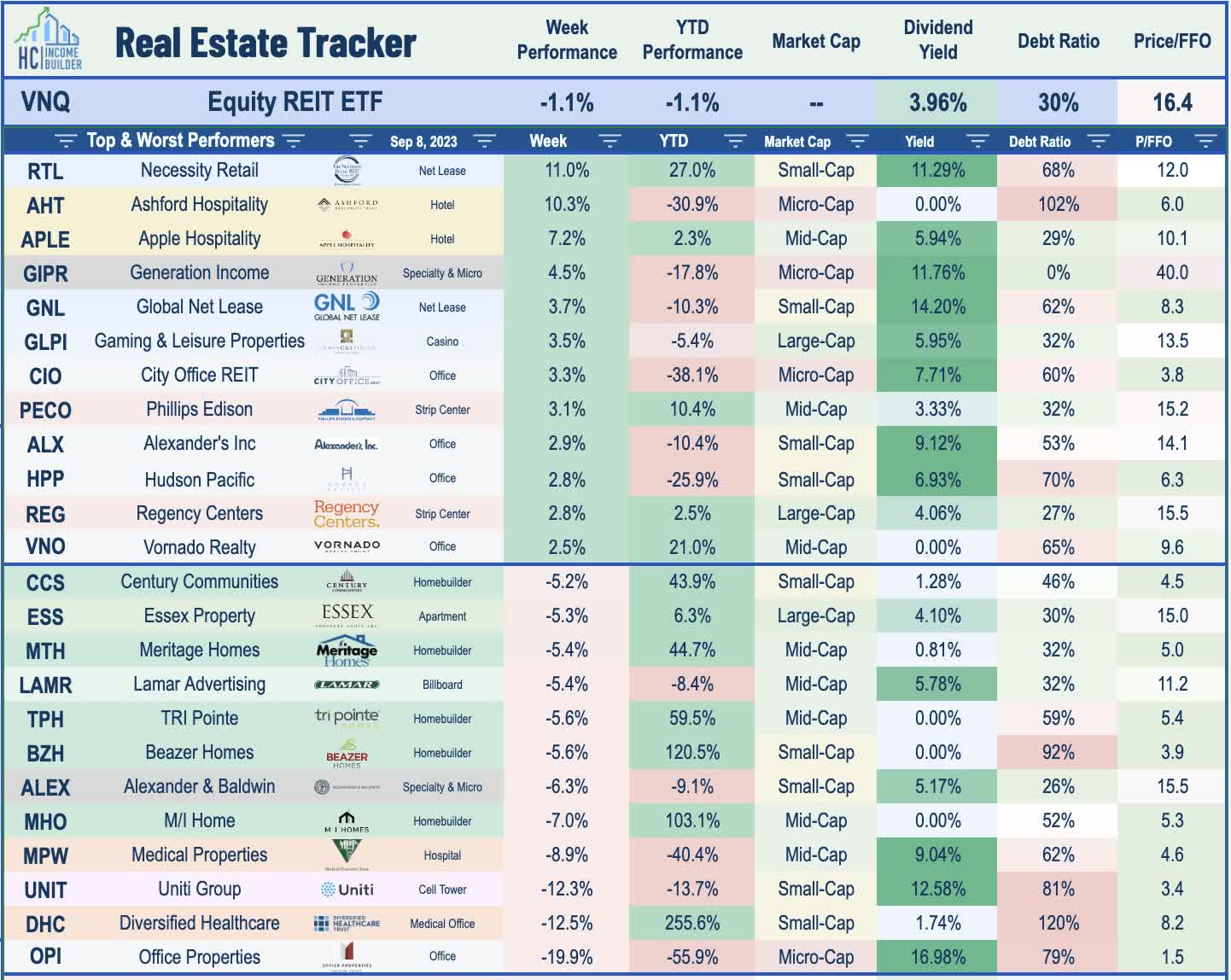

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

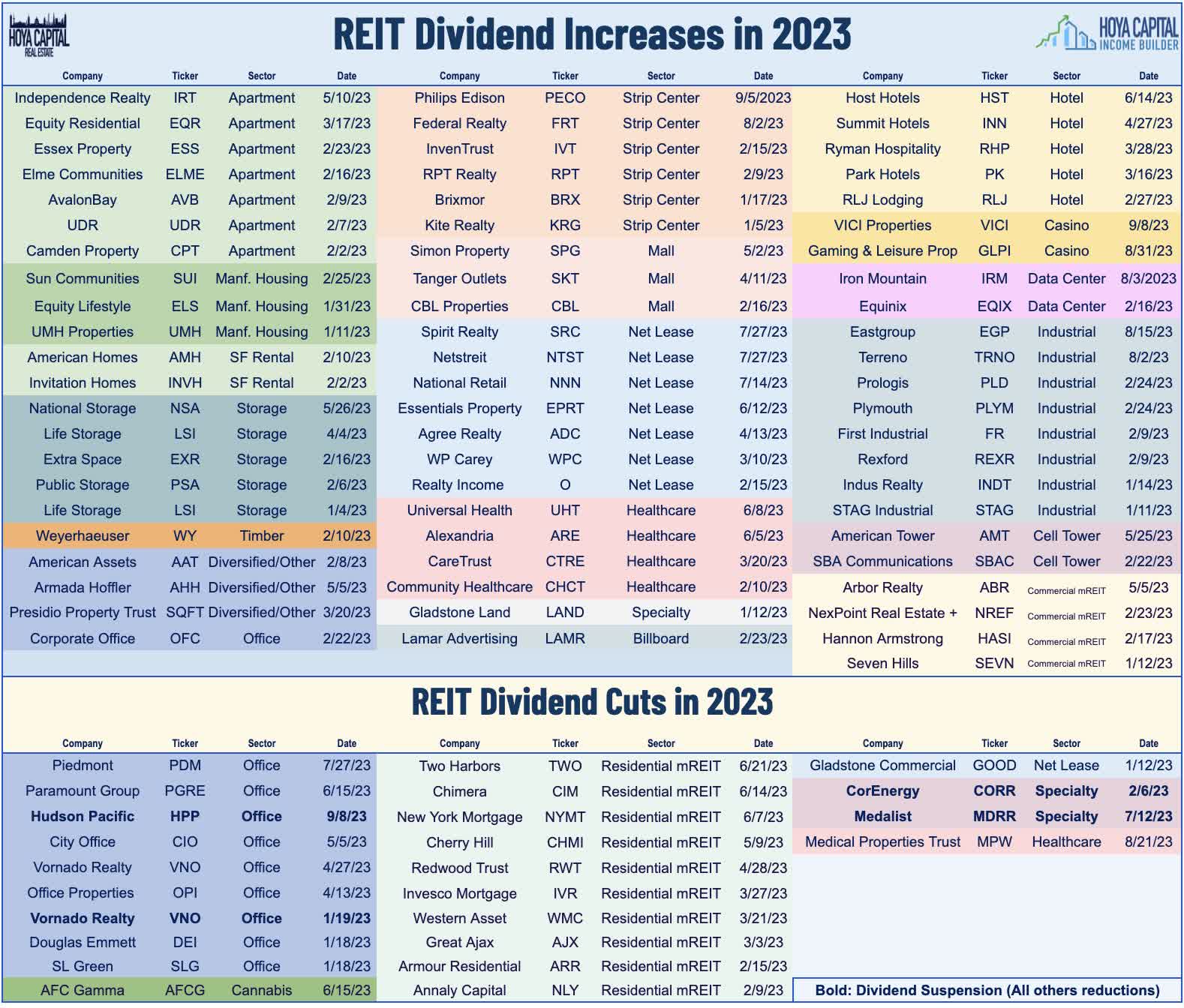

It's the best of times for some REITs, and the worst of times for others. Casino REIT VICI Properties ( VICI ) - which we own in the Dividend Growth Portfolio - was among the better performers this week after it hiked its dividend by 6% to $0.415/share (5.3% dividend yield). Strip center REIT Phillips Edison ( PECO ) rallied 3% after it raised its monthly dividend by 4.5% to $0.0975/share (3.4% dividend yield). On the downside, West Coast-focused office REIT Hudson Pacific ( HPP ) managed to finish higher by 3% on the week despite suspending its dividend on its common stock, citing the impact of the ongoing Hollywood strike on its studio portfolio, which represents about 10% of its average annual NOI. HPP had slashed its dividend by 50% in the prior quarter, but noted that the outright suspension is the "prudent decision" as it seeks to pay down variable rate debt. HPP is among the largest owners of Hollywood studio space, the majority of which are operated under usage-based revenue models rather than long-term leases. We've now seen 67 REITs increase their dividends this year, while 24 REITs have reduced their payouts.

{kind=link}

Hoya Capital

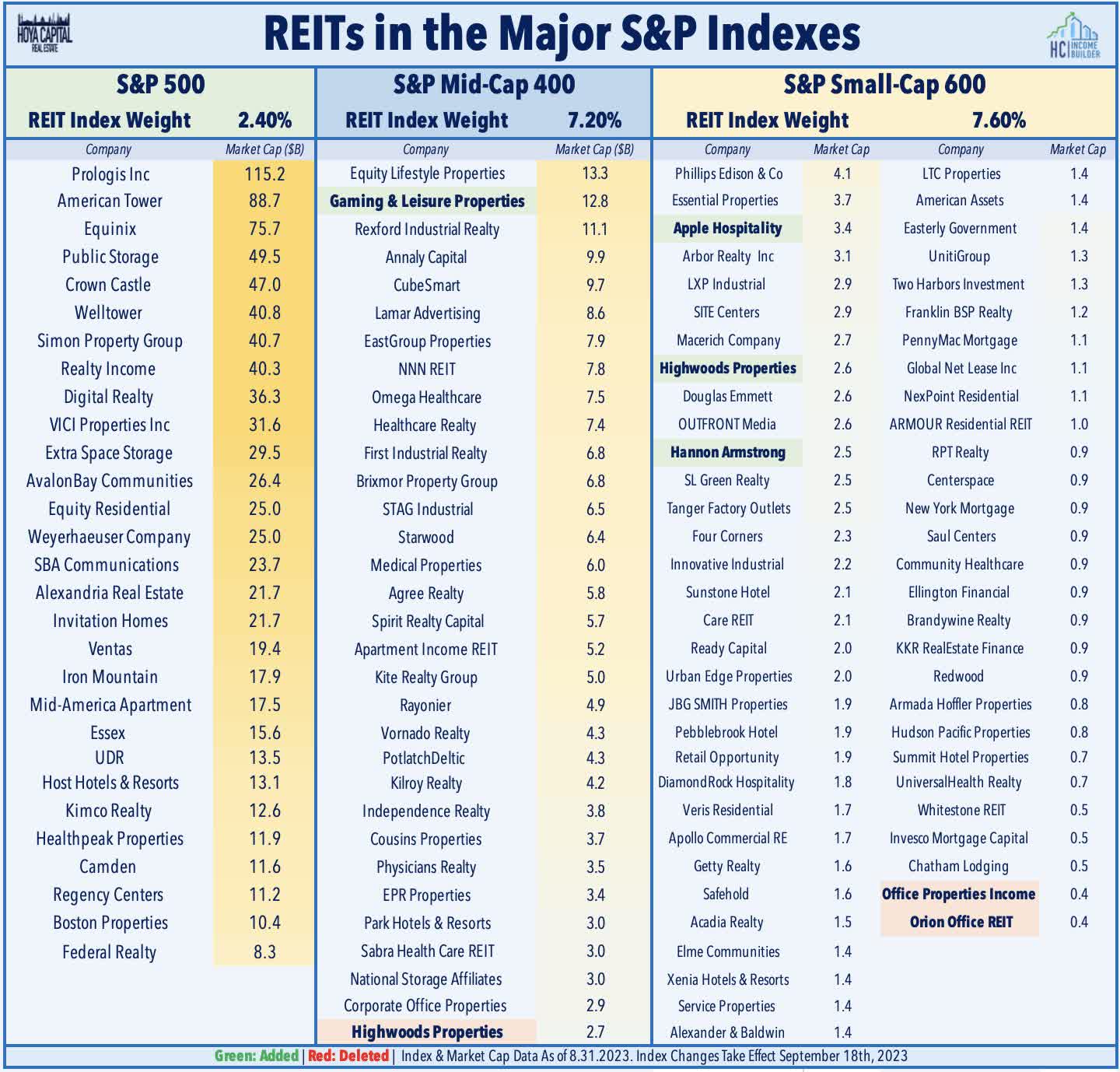

One of a handful of S&P index changes impacting the REIT space, Apple Hospitality ( APLE ) - which has been one of our three Best Ideas in Real Estate - rallied 7% this week after S&P announced that it will be added to the S&P Small-Cap 600 upon the next rebalancing on September 18th alongside mortgage REIT Hannon Armstrong ( HASI ). The pair will effectively replace two REITs that will depart from the benchmark: Office Income Properties ( OPI ) dipped 20% after being dropped from the index, while Orion Office ( ONL ) dipped more than 6%. Casino REIT Gaming and Leisure Properties ( GLPI ) was also among the leaders this week after being added to the S&P Mid-Cap 400 - one of 31 REITs in the mid-cap benchmark. Office REIT Highwoods ( HIW ) was little changed after being swapped into the Small-Cap 600 from the Mid-Cap 400. REITs are relatively well represented in the Small-and Mid-Cap indexes with roughly 7% weighting in each benchmark, but are underrepresented in the S&P 500 with a combined weight of barely over 2%.

{kind=link}

Hoya Capital

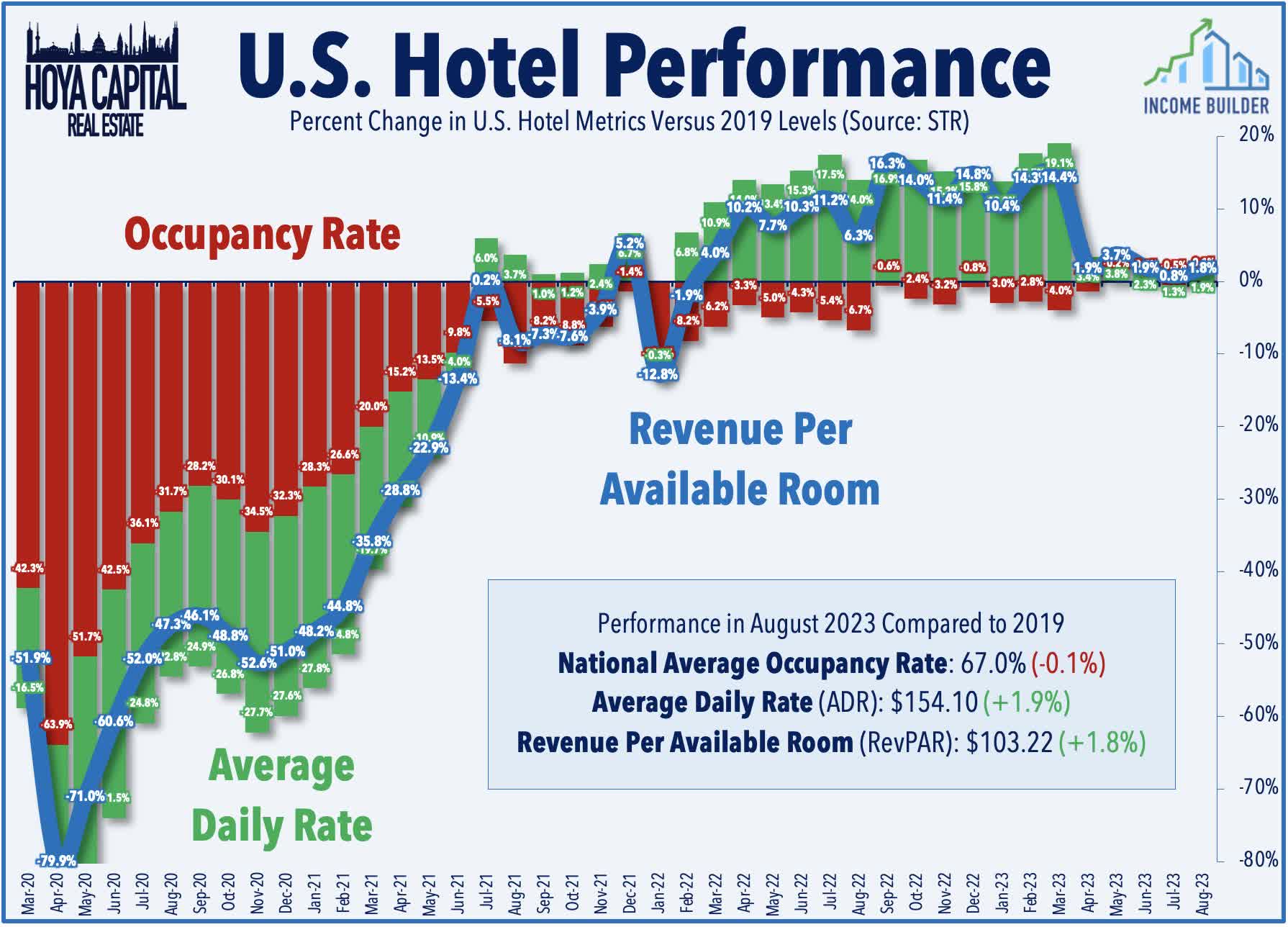

Hotel : Ending the week as the leading property sector, hotel REITs rebounded as investors assessed some less troubling forecasts for several major Atlantic storms - including Hurricane Lee - that were previously expected to impact operations at several REITs' East Coast properties. As of Saturday morning, most Hurricane Lee: Latest spaghetti models, track now forecast the storm - the most powerful storm of the season thus far - to avoid a direct U.S. landfall. The most damaging storm so far this season has been Hurricane Idalia, which impacted the Florida Gulf Coast but did not materially impact any REIT. Earlier this week, Host Hotels ( HST ) provided an update regarding the impact of the Maui wildfires and other recent weather events, noting that there has not been any reported property damage to its hotels or golf courses on Maui, and all its hotels remained open and operational through the wildfires. HST estimated that impact to its net income and hotel EBITDA totaled approximately $5M in August due to cancellations but noted that it is not otherwise updating its guidance provided in August, as it is "too early in the quarter to provide a comprehensive update."

{kind=link}

Hoya Capital

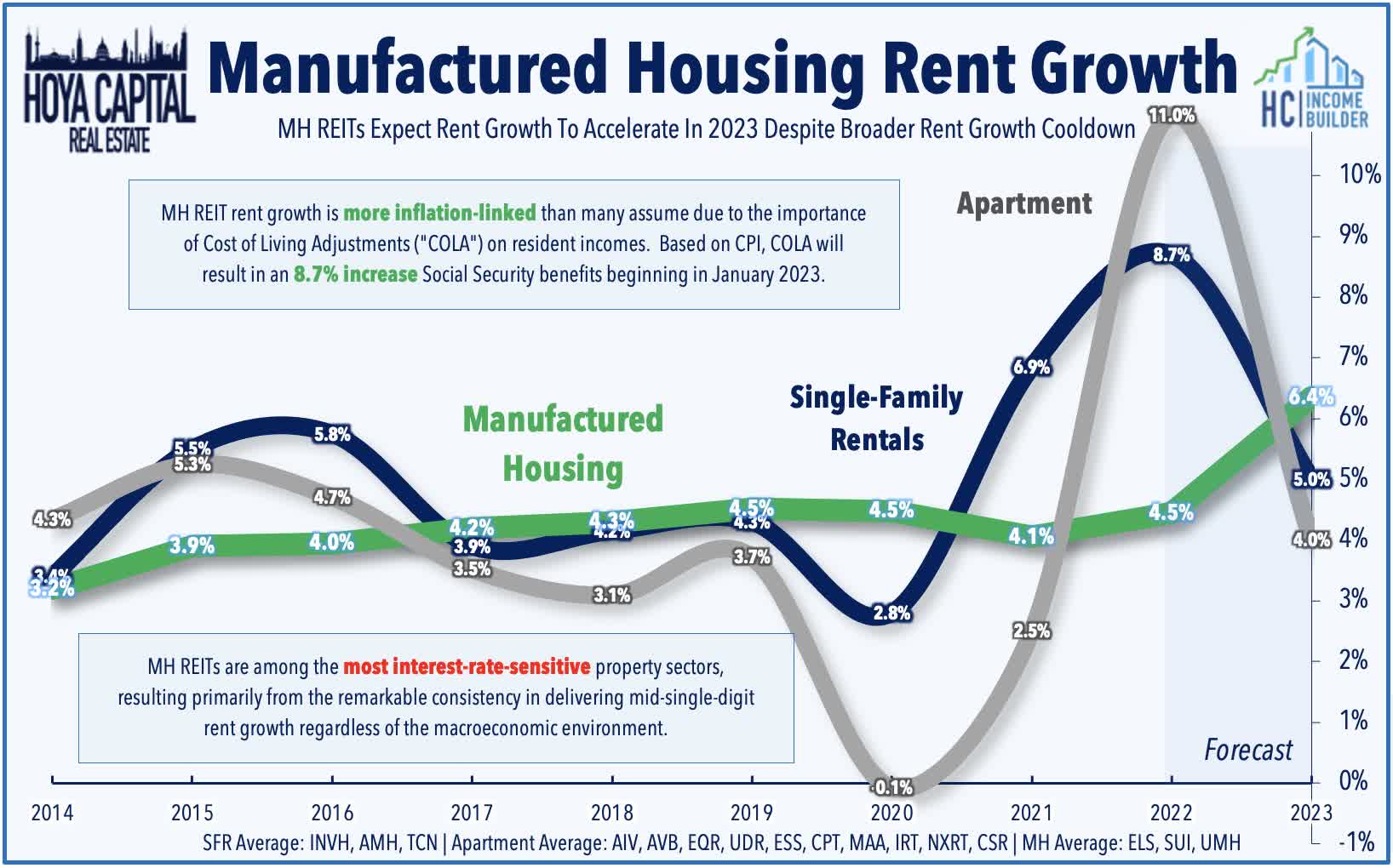

Manufactured Housing : The other property sector that deals with the annual threat from Atlantic Hurricane season each year, manufactured housing REITs - along with other more-interest-rate-sensitive property sectors - were among the laggards this week. UMH Properties ( UMH ) was little changed after it provided a business that included operating metrics through the end of August. UMH commented that "demand throughout our portfolio remains strong as evidenced by our monthly rent roll and occupancy growth" and noted that its overall occupancy has increased by 167 units quarter-to-date. UMH also noted that its monthly revenues have increased by $377K thus far in Q3 compared to the prior quarter. As discussed in our Manufactured Housing update last month, following nine straight years of outperformance over the REIT Index, MH REITs have uncharacteristically stumbled over the past year, pressured by the direct and secondary effects of higher interest rates. Interest rate-related risks have been compounded by concerns over "climate risk" exposure and the effects of a post-COVID demand normalization in the recreational vehicle and marina business segments. Domestically, fundamentals within these REITs' core manufactured housing segment are as strong as ever. Propelled by COLA effects, rent growth has accelerated this year even as broader residential rents have moderated.

{kind=link}

Hoya Capital

Apartment : Sticking in the residential sector, a pair of apartment REITs provided operating updates this week. AvalonBay ( AVB ) was among the better-performers this week after it announced that its same-store revenue growth thus far in Q3 is trending 40 basis points above its prior guidance at 5.3% versus the 4.9% expected increase. AVB noted that blended rent growth on new and renewed leases increased by 3.5% year-over-year in July and August, on average, a slight deceleration from the 4.8% increase it posted in Q2. Rent growth in its East Coast markets has been significantly stronger than its West Coast Markets, averaging about 4.3% in Q3 in the East vs. roughly 2.2% out West. Equity Residential ( EQR ) reported that same-store revenue growth "remains on track with the Company’s guidance" and is "finishing a good leasing season with healthy demand and pricing." EQR noted that blended rent growth on new and renewed leases increased 3.5% year-over-year thus far in Q3, a slight deceleration from the 4.3% increase it posted in Q2. Same-store occupancy ticked up to 96.0% in the first two months of Q3 from 95.9% in Q2. Recent Zillow data shows relatively strong rent growth trends in recent months following a sharp cooldown in late 2022 and into early 2023. Month-over-month rent growth exceeded 0.5% for a third-straight month in July, which follows a period of eight-straight months below that level.

{kind=link}

Hoya Capital

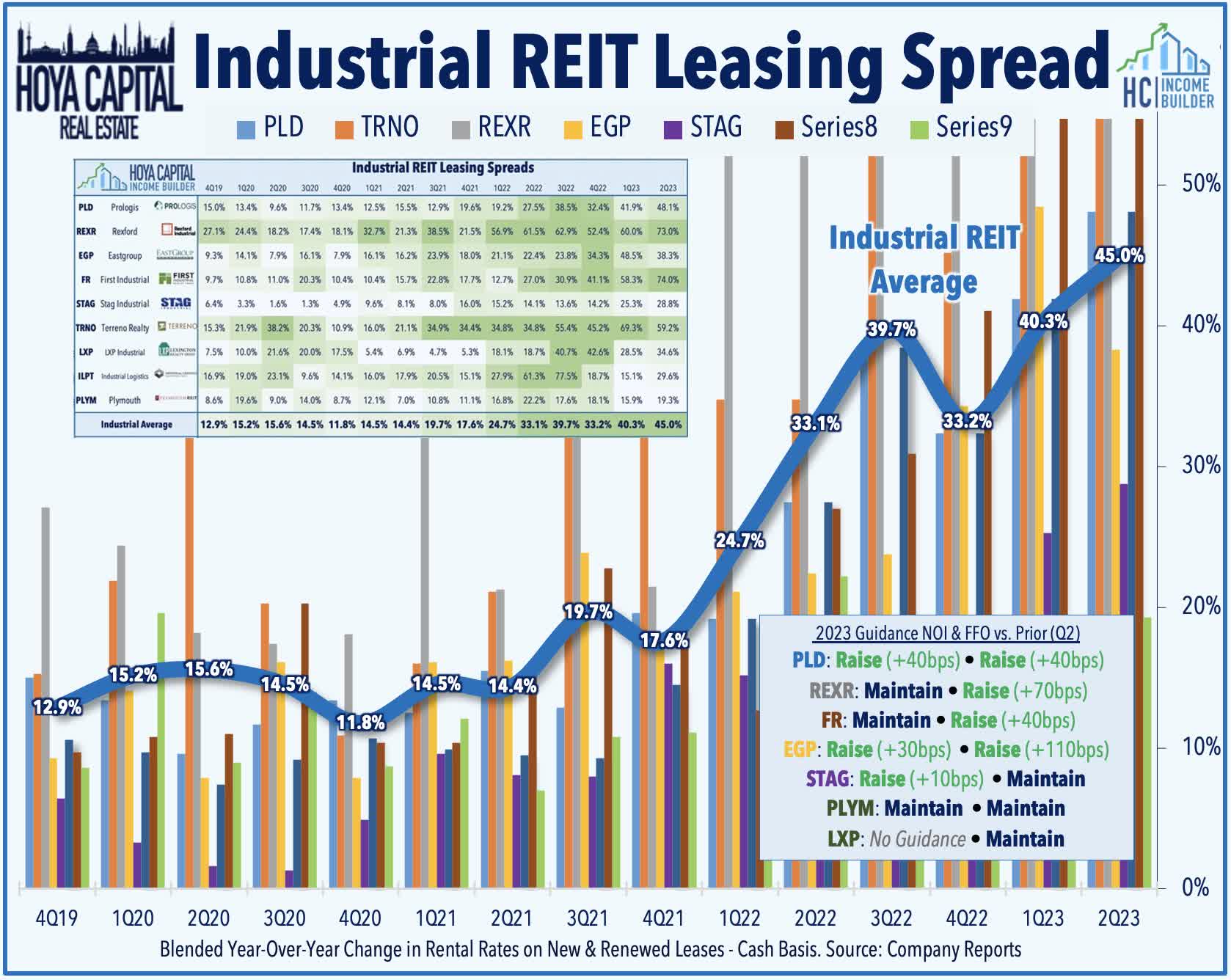

Industrial : A trio of industrial REITs also provided business updates this week. EastGroup ( EGP ) - which we own in the Dividend Growth Portfolio - was among the better-performers this week after it reported that it achieved 56.1% blended rent growth on new and renewed leases (40.1% on a cash basis) in July and August, which represents a slight acceleration from Q2. EGP also noted that it has raised $135M through its at-the-market equity offering program so far in Q3, which it has used to acquire a pair of industrial buildings in Las Vegas for $53M and a parcel of land in East Tampa for $15M, which will accommodate the future development of three buildings containing approximately 500k SF. Elsewhere, Southern California-focused Rexford ( REXR ) announced that it acquired three industrial properties in Long Beach, Gardena, and Orange County for a combined $46M. Terreno ( TRNO ) announced a $15M acquisition of an office building in Santa Ana, California, that will be demolished and repurposed to a 92k SF industrial distribution hub which is already 100% pre-leased. In our Earnings Recap , we noted that industrial REITs reported that rent spreads have actually reaccelerated in early 2023, perhaps credited to a moderation in cost pressures in other areas of the supply chain.

{kind=link}

Hoya Capital

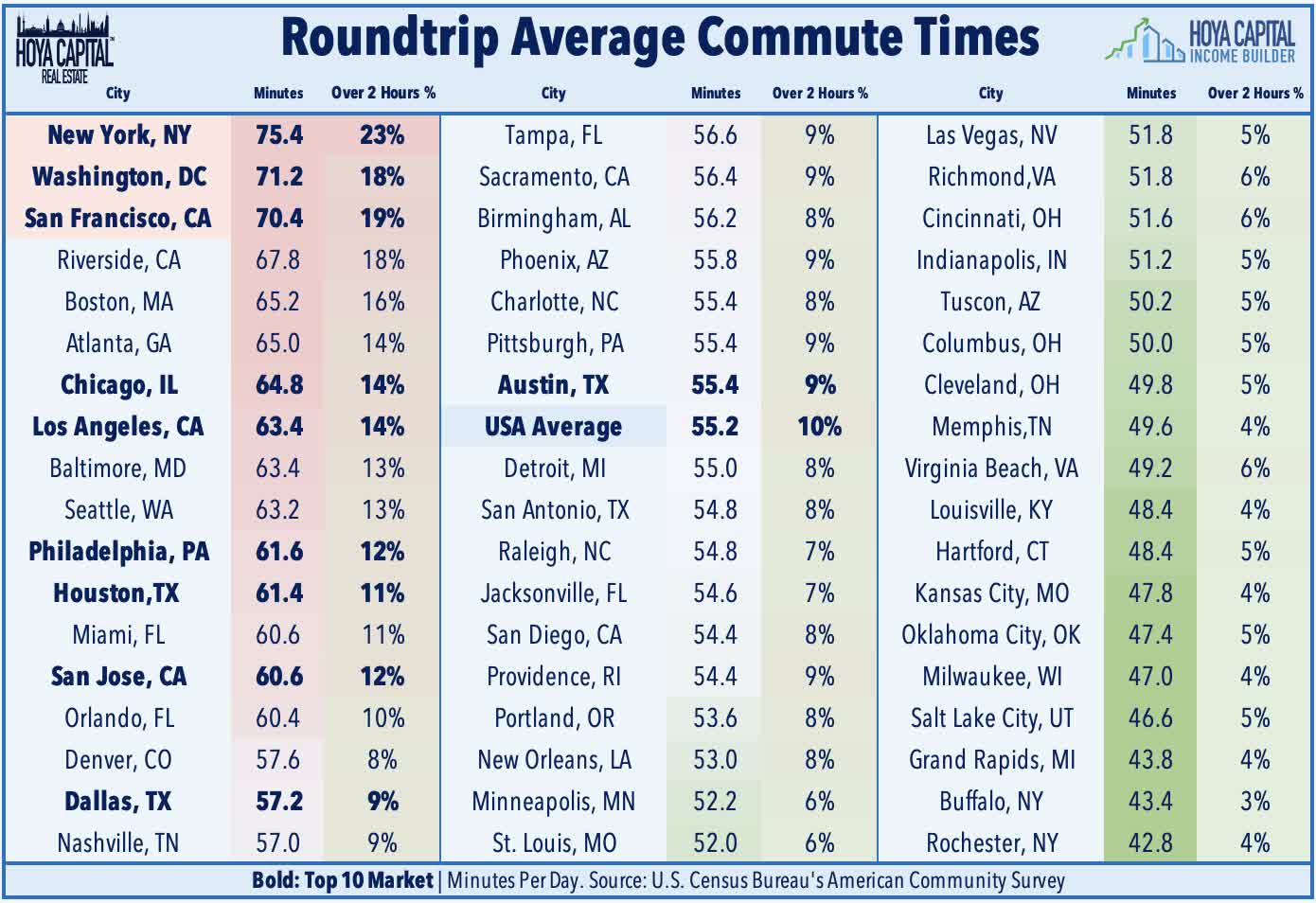

Office : Corporate Office ( OFC ) was little changed this week after it announced that it is changing its name to COPT Defense Properties and changing its ticker symbol to “ CDP ” effective next week. The company noted that the change is intended “to align our name with our investment strategy, and better inform current and future investors of our commitment to our strategy, and the differentiated investment benefits that we believe our strategy has and will continue to deliver to shareholders.” This week, we published Office REITs: It's All About the Commute . Since our last update in late-May when we called a "bottom" for the most battered and unloved property sector, Office REITs have indeed been among the top-performing property sectors with gains of over 20%, lifted by a relatively decent slate of earnings reports and recent indications that "Return to Office" has gathered steam as labor markets weaken, underscored by the ironic "RTO mandate" from Zoom ( ZM ), the "poster child" of Work From Home. We noted that WFH is ultimately an 'economic' decision, and several major markets (SF, NYC, CHI, DC) have an unavoidable structural issue: it takes too long to get to work - largely a byproduct of decades of bad housing policy and urban planning.

{kind=link}

Hoya Capital

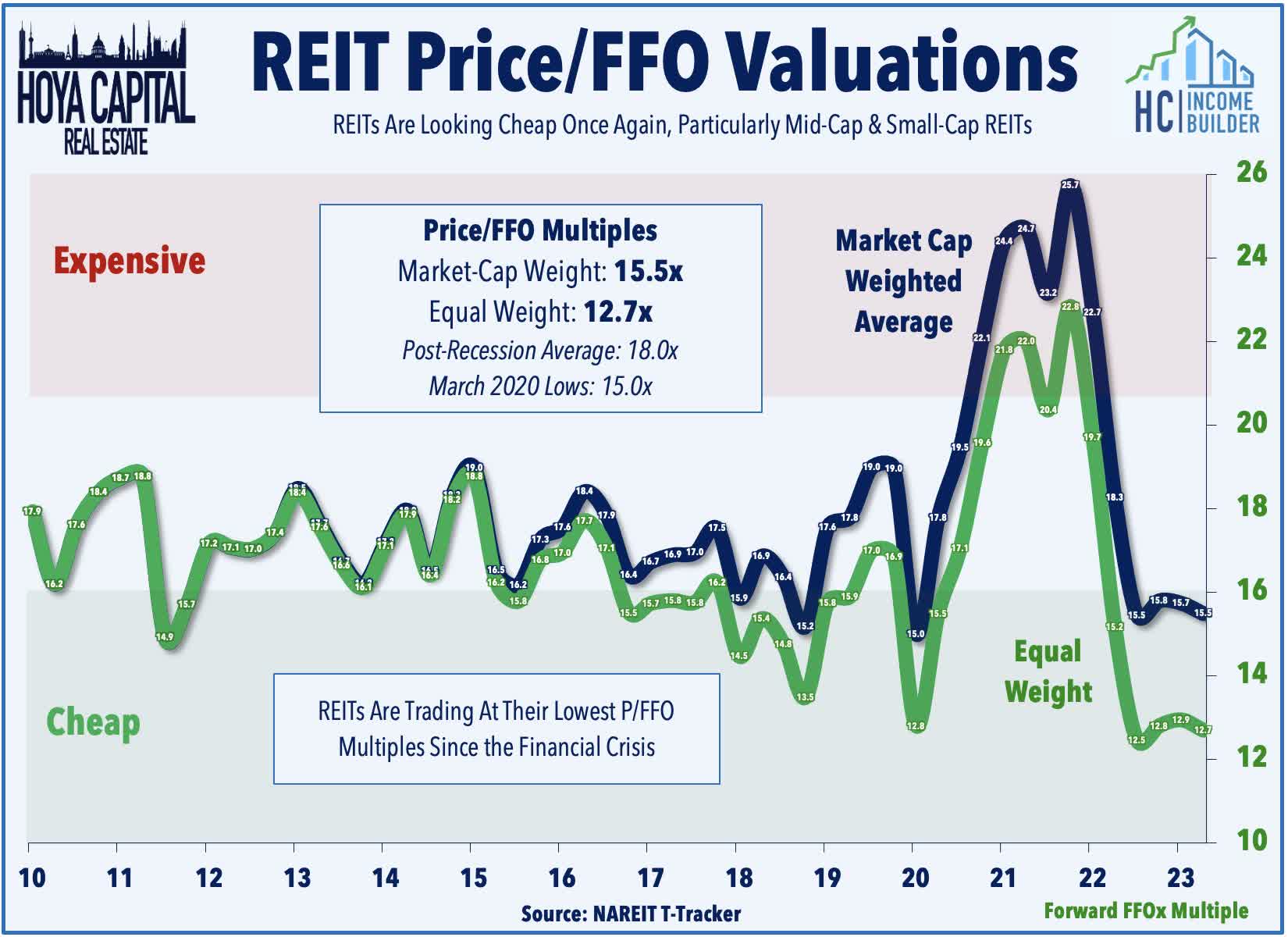

Last week, we published REITs Are Historically Cheap . Commercial and residential real estate markets remain an easy transmission mechanism - or "punching bag" - of the Federal Reserve's historically swift monetary tightening cycle. The business models of many private equity funds and non-traded REITs were simply not designed for a period of sustained 5%+ benchmark rates or double-digit declines in property values. Private market players and non-traded real estate platforms were willing to take on more leverage and finance operations with short-term and variable-rate debt - a strategy that worked well in a near-zero rate environment but quickly crumbles when financing costs double or triple in a matter of months. "Hope" is the only strategy for some highly-levered property owners amid a dearth of buying interest and dwindling refinancing options. Pockets of distress remain almost entirely debt-driven, however, as property-level fundamentals remain solid across nearly every property sector. Public REIT reported that "same-store" property-level income was 10% above pre-pandemic levels in the most recent quarter. Nareit reported earlier this year that nearly 50% of private real estate debt is priced based on variable rates compared to under 10% for public REITs. Bottom line - macroeconomic conditions are aligning in an ideal manner for low-levered entities with access to "nimble" equity capital - conditions that maximize the true competitive advantage of the public REIT model, which these entities have been unable to exploit in the "lower forever" rate environment.

{kind=link}

Hoya Capital

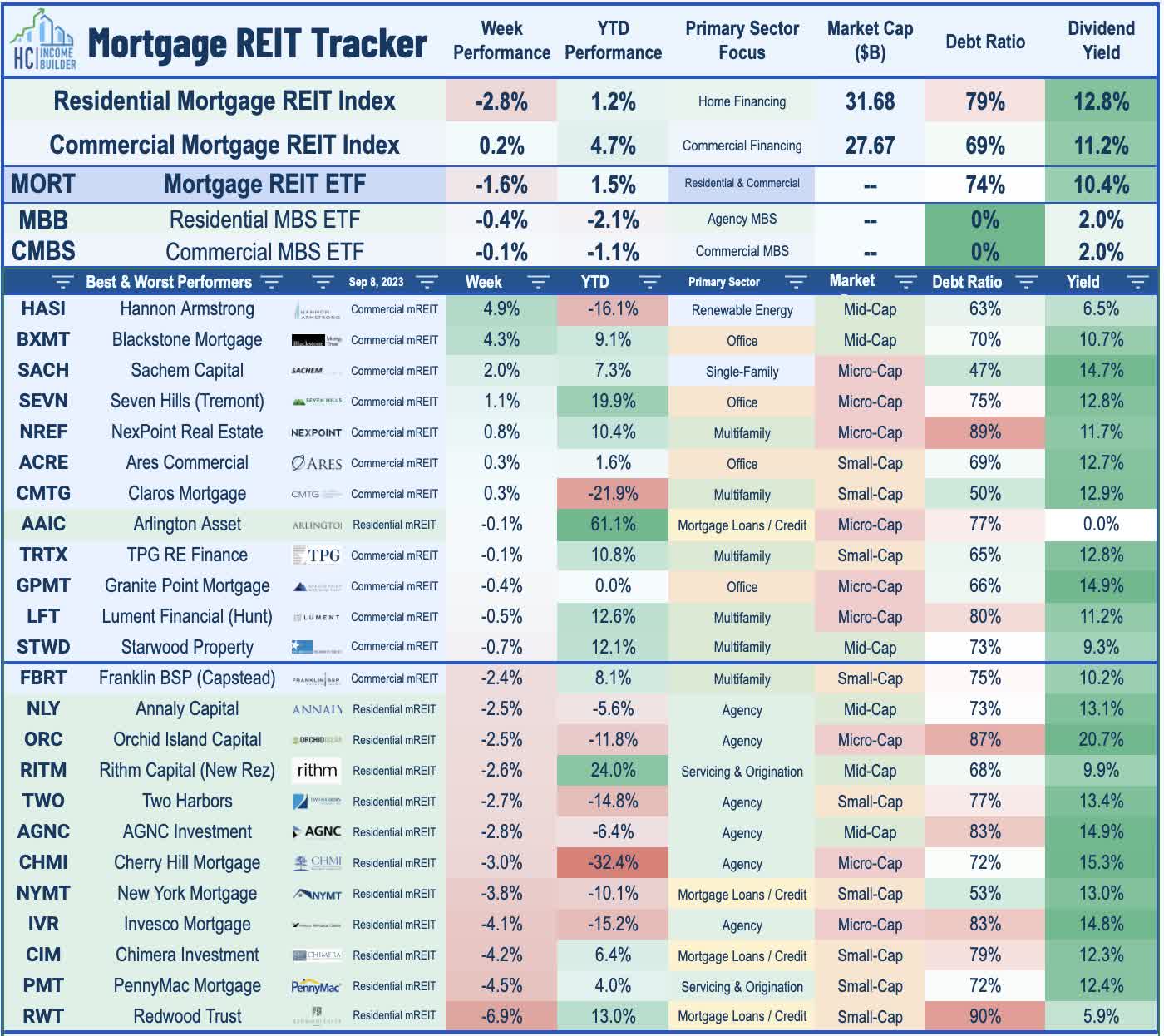

Mortgage REIT Week In Review

Following two weeks of strong gains, Mortgage REITs finished mostly lower on the week, with the iShares Mortgage REIT ETF ( REM ) slipping 1.6% as weakness from residential mREITs offset a relatively strong week for commercial lenders. As noted above, renewable energy-focused lender Hannon Armstrong ( HASI ) rallied 5% after it was added to the S&P Small-Cap 600, becoming one of seven mortgage REITs included in one of the three major S&P benchmarks. Redwood Trust ( RWT ) was the laggard this week after it announced the launch of a home equity investment (“HEI”) origination platform in which RWT will directly originate HEI by "leveraging its network of loan officers, and by establishing direct-to-consumer origination channels." RWT has been among the most active players in the HEI market, purchasing approximately $350M in HEI since 2019 and co-sponsoring the first-ever securitization backed entirely by HEI in 2021.

{kind=link}

Hoya Capital

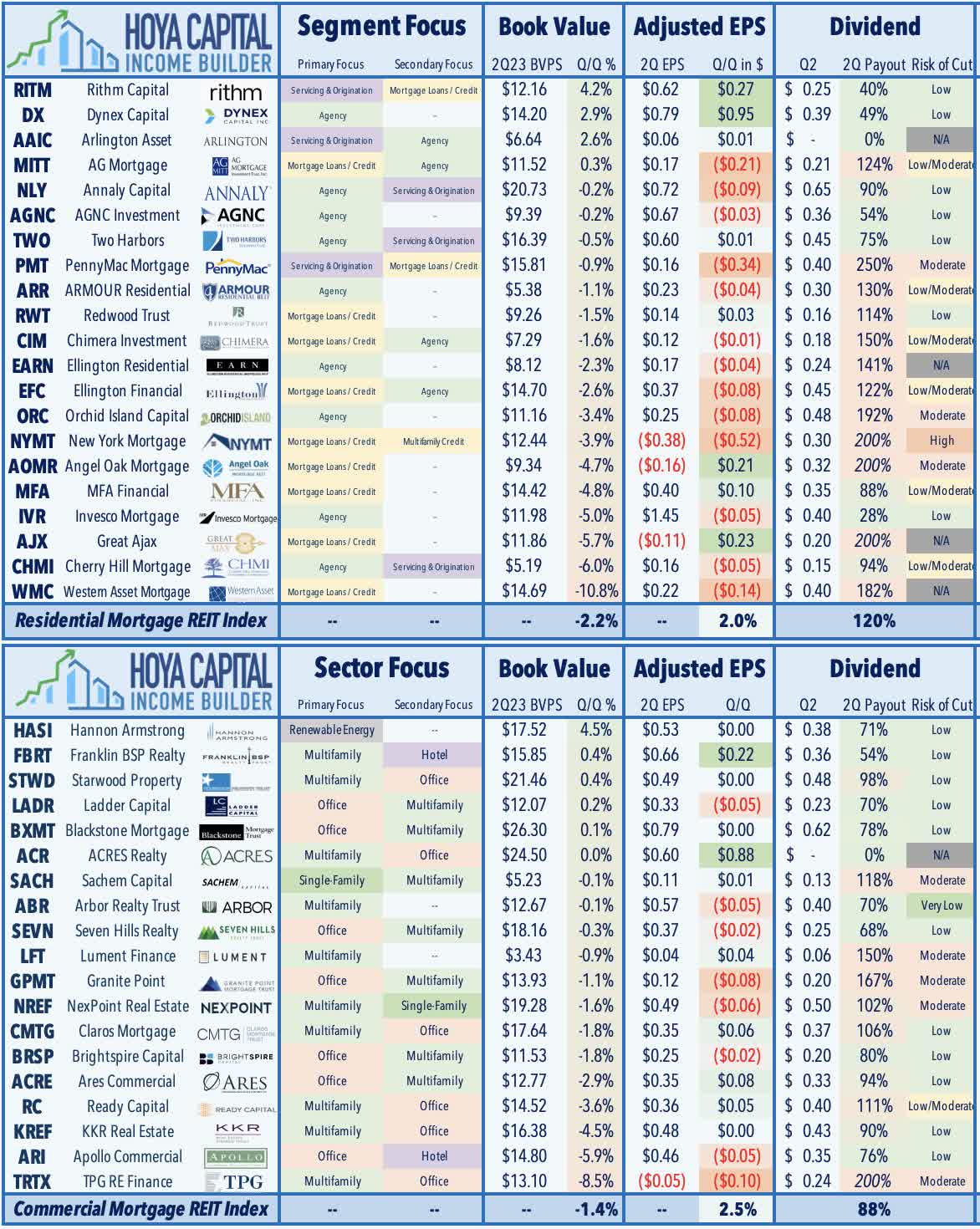

Elsewhere, Rithm Capital ( RITM ) was also among the laggards after its acquisition target - Sculptor Capital ( SCU ) - received another bid from the same hedge fund group whose offer was rejected by SCU's Board last week, citing uncertainty in the group's ability to finance the deal. All three mortgage REITs that declared dividends this week held their payouts steady at current levels: Annaly Capital ( NLY ) held its quarterly dividend at $0.65/share (13.2% dividend yield), Ellington Financial ( EFC ) held its monthly dividend at $0.15/share (13.7% dividend yield), and Ellington Residential ( EARN ) held its monthly dividend steady at $0.08/share (15.4% dividend yield). In our Earnings Recap , we noted that mREITs stand on steadier ground with dividend coverage after a relatively solid slate of earnings results showing a modest increase in earnings per share. On average, the 21 residential mREITs reported a BVPS decline of 2.2% in Q2 but recorded a 2.0% increase in their distributable EPS. The 19 commercial mREITs reported an average BVPS decline of 1.4%, while the average commercial mREIT reported a 2.5% increase in comparable EPS.

{kind=link}

Hoya Capital

2023 Performance Recap & 2022 Review

Through eight months of the year, the Equity REIT Index is lower by 1.1% on a price return basis for the year (+3.9% on a total return basis), while the Mortgage REIT Index is higher by 4.0% (+10.2% on a total return basis). This compares with the 16.5% gain on the S&P 500 and the 6.4% advance for the S&P Mid-Cap 400 . Within the real estate sector, 7-of-18 property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, Industrial, and Timber REITs, while Cannabis and Cell Tower REITs have lagged on the downside. At 4.26%, the 10-Year Treasury Yield has increased by 38 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but down from its intra-day peak of 4.35% in August. The US bond market has stabilized following its worst year in history as the Bloomberg US Bond Index has produced total returns of 0.6% this year. WTI Crude Oil - perhaps the most important inflation input - is higher by 12% on the year but remains 20% below its 2022 peak.

{kind=link}

Hoya Capital

Economic Calendar In The Week Ahead

Inflation data is in the spotlight in a jam-packed week of economic data in the week ahead. The main event comes on Wednesday with the Consumer Price Index for July, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The Core CPI is expected to moderate to a 4.3% year-over-year rate - down from 4.7% last month - while the headline CPI is expected to rise slightly to 3.6% from 3.3% as some of the "hottest" prints seen in mid-2022 begin to roll off. We've noted in recent reports that "real-time" inflation - as measured by the CPI-ex-Shelter Index - has averaged less than 1% since last July. On Thursday, we'll see the Producer Price Index, which has recently shown an even more significant cooling of price pressures, with the Core PPI expected to cool to 2.2% from 2.4% in the prior month, while the headline PPI is expected to show a 1.3% annual increase - down from the recent peak last March at 11.8%. On Friday, we'll get the first look at Michigan Consumer Sentiment for September - a report which includes the closely-watched inflation expectations survey.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website

For further details see:

A Crude Awakening