KWEB - A Goldilocks Economy? I Don't Think So

Summary

- Inflation appears to have peaked for now, and a soft landing is a valid scenario that deserves a small allocation in the portfolio.

- The Federal Reserve will likely cut rates fast, late, and not gradually.

- 2022 was about adjusting the P of P/E. 2023 will be about the E of P/E.

- Future Credit Creation and PMIs still point toward a hard landing.

And suddenly everything is fine

The current Bear-Market-Rally is bound to continue with the release of the CPI data this week (January 12, 2023, at 08:30 EST), contrary to my belief in the last article . The markets are progressively pricing in an increased chance of a soft landing - a term proposed by the Federal Reserve in 2022 in which the economy weakens just the right amount so that inflation is subdued, but the impact on the labor market remains constrained. Still (mostly) wishful thinking, in my opinion.

The labor market remains structurally strong on the supply side, while economic data starts to weaken further. Inflation has peaked for now, and disinflationary/deflationary pressures will reduce the significance of inflation data during 2023. The market is now pricing in a higher probability of a change in the Federal Reserve reaction function.

Meaning, if inflation falls due to weak economic growth, then the Federal Reserve will pivot, and the stock market will rise. Instantly, the market tries to front-run the pivot again and again.

Bad news is still counted as good news, as of now. I believe that's going to change in the course of 2023 as the economic reality sets in and companies record lower-than-expected profits. The Federal Reserve is not hiking rates to 5.0% just to cut them immediately. There's likely going to be a prolonged period of time where the Fed Funds Rate remains elevated and, therefore, consistently restrictive along with Quantitative Tightening, which puts more pressure on the financial markets.

{kind=link}

However, the bullish picture is the following: inflation is going to decrease significantly because of energy price deflation and goods deflation. The core of the economy is weakening, but the reopening of China helps to spur economic growth to neutral (no growth) or mildly positive territory. The labor market remains on the tighter side because of supply constraints. Now, the Federal Reserve and other global Central Banks are able to change their monetary policy stance from restrictive to neutral or even accommodative. After all, inflation is rapidly decreasing. After the recent downturn of 2022, a period of

"Goldilocks economy" reemerges because of mild economic growth and disinflation, which influences monetary policy easing. The results would be similar to the first half of 2019, where the effective Fed Funds were flat and then started to drop roughly one percentage point while the market rallied to new all-time highs.

A valid take, but a few counterpoints

I believe one's portfolio should have some allocation towards this scenario, which is why I hold Chinese tech equities via the KraneShares CSI China Internet ETF ( KWEB ). I regard the equities of the exchange-traded fund ("ETF") as the ones that profit most directly from the Chinese reopening, the accompanied monetary and fiscal easing, and a Chinese economic rebound. Of course, there is political risk associated with that position, which is why I keep it relatively small.

I have a few counterpoints regarding the soft-landing narrative.

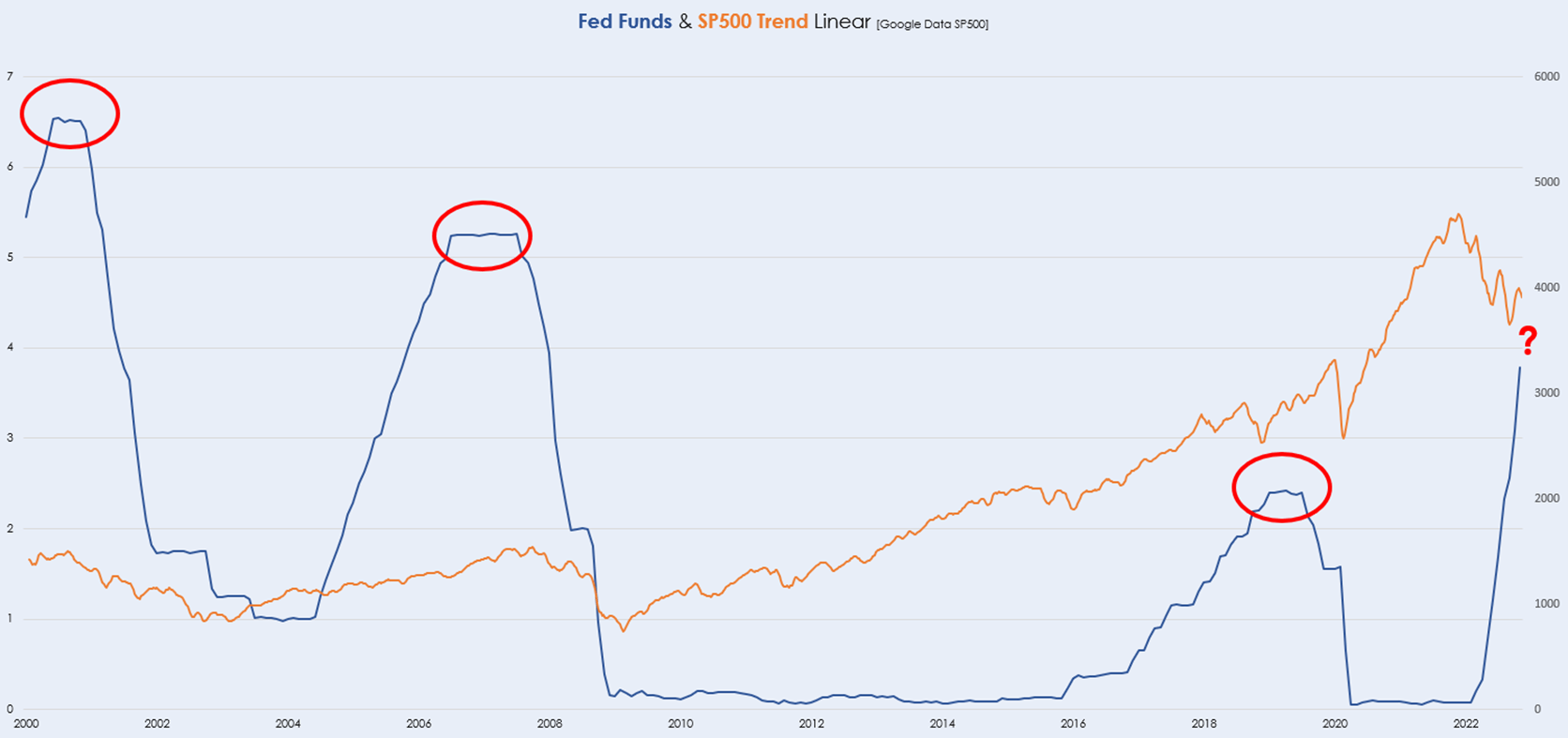

1. The Federal Reserve will likely cut rates fast, late, and not gradually

Historically, rising interest rates have been bullish because the reason for rising interest rates was an overheating economy, meaning earnings expectations usually went up during these times. The last three major rate hikes during the periods from 2018-2019, 2004-2006, and 1999-2000 were all accompanied by a rising U.S. stock market.

However, the rate hikes of 2022 were because of inflation. Real earnings didn't change at all, but the market had to adjust valuations to the downside because the risk-free rates shot up. This doesn't resemble any similarities between prior scenarios during the last 40 years and now.

The Federal Reserve, and therefore all global central banks are on a short leash when it comes to easing monetary policy because the reason for the tightening was primarily inflation. So, the communicated tendency of the Federal Reserve is to keep rates in a restrictive territory rather too long than too short.

{kind=link}

But currently, the Fed Funds futures curve expects the Fed to hike to 5 % in Q2/2023 and then to gradually cut rates in the later stages of 2023. On the contrary, the Federal Reserve expects to keep the Fed Funds above 5% for the whole year of 2023.

I don't believe the FED itself is a good predictor of the Fed Funds rate. Neither is the Fed Funds Futures Curve (i.e., the market). But because I believe it is clear that the inflationary environment of 2021 & 2022 lead to a "tighter for longer" mindset at the Federal Reserve, chances are that the hiking cycle will be prolonged, and therefore the cutting cycle will be rather abrupt and not gradual like during H1/2019.

The Federal Reserve will for sure cut rates in the future. Nobody knows when that's going to happen - even the Federal Reserve doesn't. But I believe that the market has to signal to the Fed that something is breaking/has broken before the actual pivot will be possible. The process of signaling that something is breaking (credit, bonds, or labor market) was never bullish in the past (e.g., 2008-2009 or 2000-2001).

The major lows during these periods were established only after the Fed had already cut rates aggressively. To say it bluntly: When the stuff hits the fan, bad news is bad news.

2. Holding rates in a restrictive territory is still restrictive

The longer the Federal Reserve keeps rates at or near the current restrictive territory, the more likely a hard landing becomes. Markets price in the future and react instantly to rate of change fluctuations. Therefore, it is reasonable that the market rallies in the short term because of an increase in the probability that the Federal Reserve doesn't actively raise rates anymore but just keeps them at the established levels. But that scenario is more than priced in already.

What's now important is not the actual level of Fed Funds but the duration in which rates stay in a very restrictive area. If the market rallies prematurely, then financial conditions ease, and the Federal Reserve has no reason to ease the monetary policy stance. Additionally, if the labor market remains as tight as it is now, there's a higher chance that the Federal Reserve keeps the rates elevated for longer.

Monetary policy acts with long and variable lags because interest rates have to feed through into the economy. The 2021 stock market craze was mainly the result of the monetary easing and the fiscal spending of 2020. The 2023 stock market will be heavily influenced by the monetary tightening of 2022.

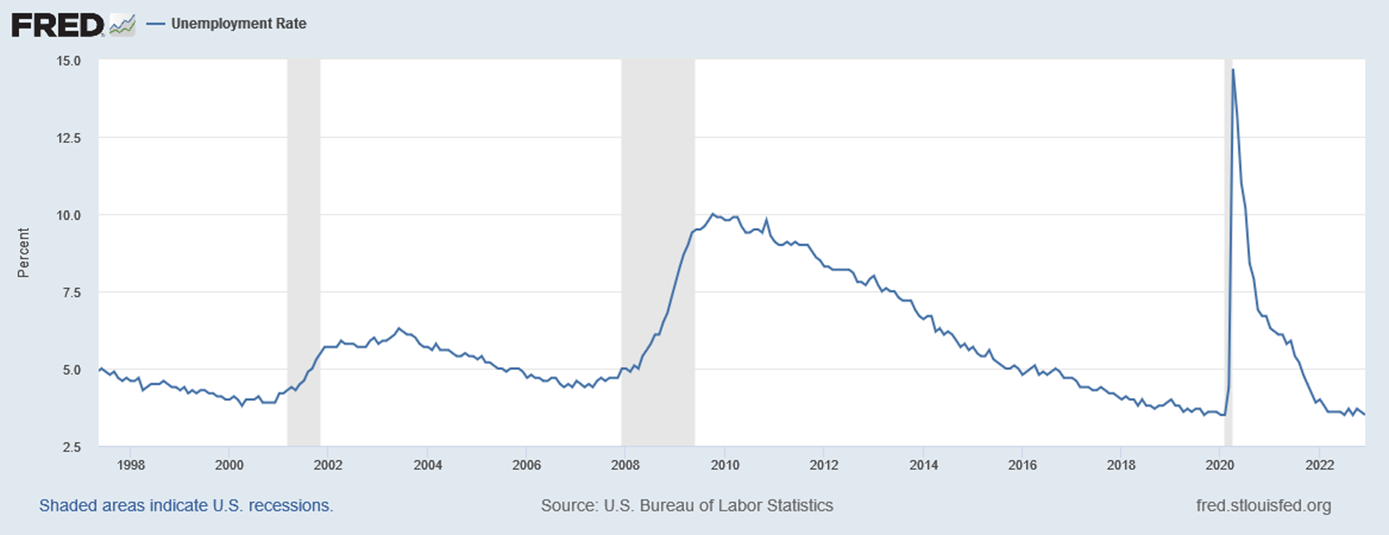

3. The Labor market is a lagging indicator

The labor market is still a lagging indicator. Historically, unemployment only begins to rise during a recession and usually remains elevated even after the recession has officially ended, i.e., economic growth resumes. If unemployment rises significantly, there are good chances that the recession is well underway already.

{kind=link}

If economic growth slows, unemployment rises. Tech firms and banks already disclosed that they would continue significant layoffs in 2023. The leading indicators for economic growth do not show good prospects for unemployment.

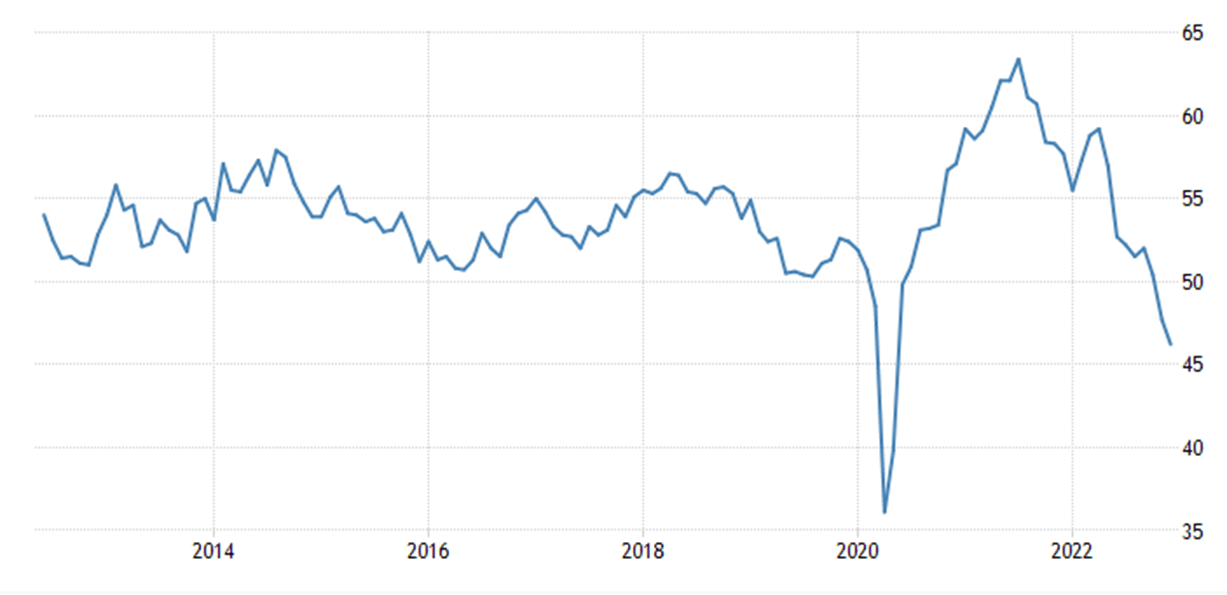

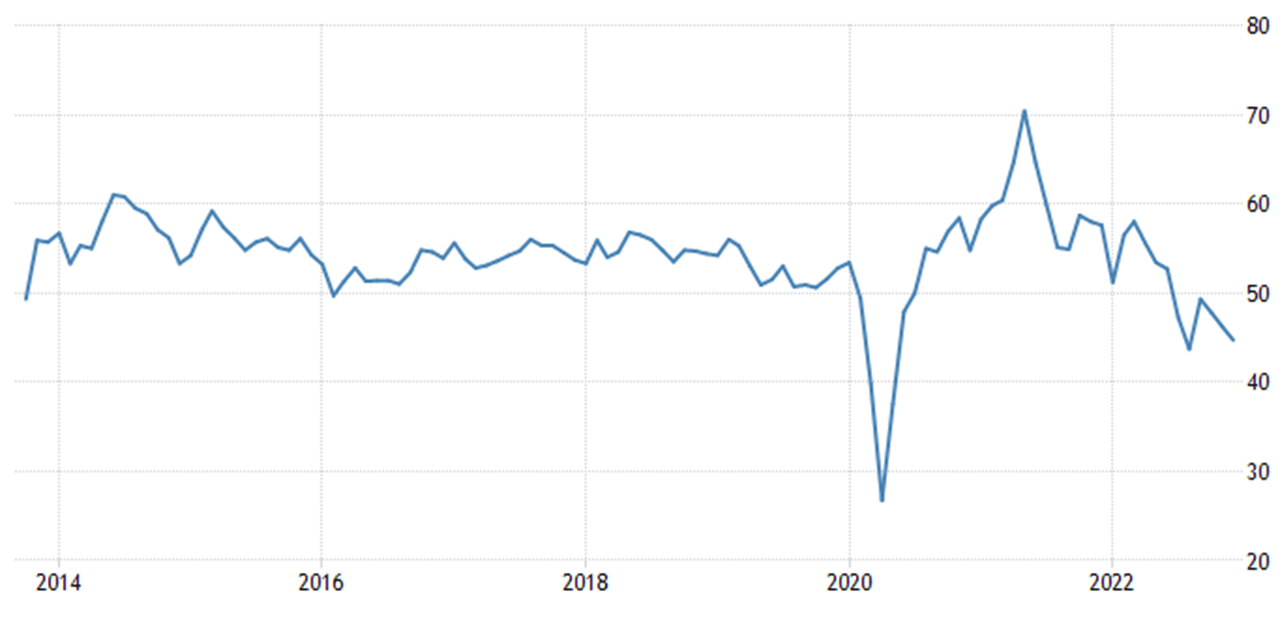

4. Credit Signals & PMIs signal a hard landing

The Manufacturing PMI for December 2022 is already in a recessionary territory at 46.2 as of December 2022 because of significantly weakening demand.

{kind=link}

Services remained somewhat resilient during 2022, but the new orders component of the Services PMI now shows significant weakness in services demand too.

Services PMI came in at 44.7 in December 2022 again because of significant demand destruction.

{kind=link}

Notably, the new orders subcomponent of the Services PMI dropped to 45.2 in December. In the months before, new orders were firmly above 50, signaling resiliency in the Services sector.

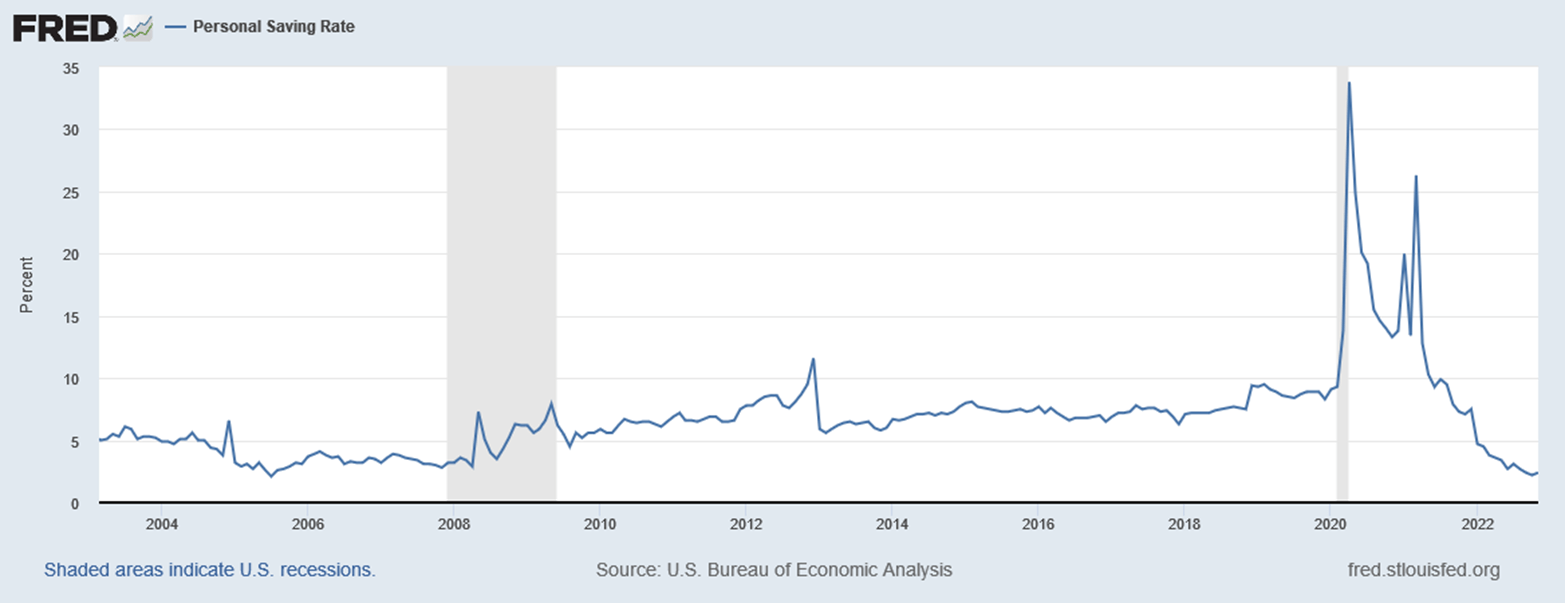

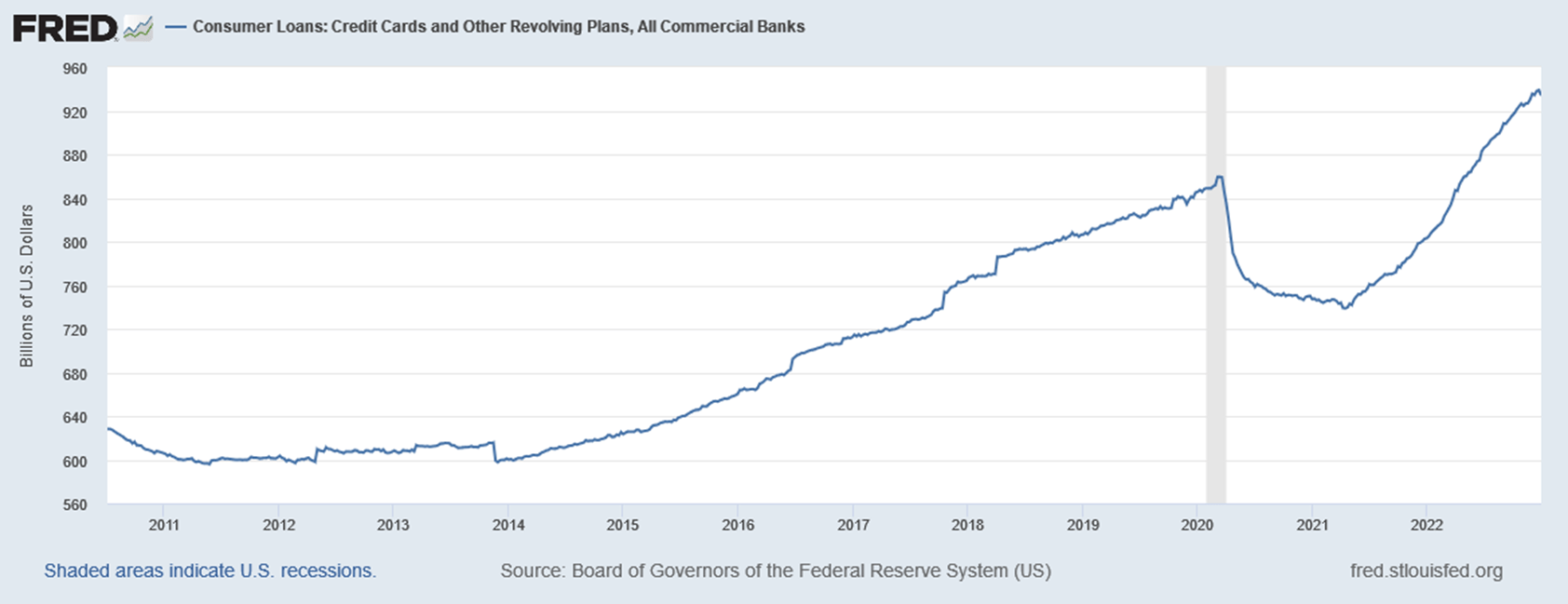

The signs of receding consumer resiliency are now clearly shown in the data. That's no surprise since the recent spending was because of a drawdown in the personal savings rate and an increase in credit card debt, with elevated lending costs.

{kind=link}

{kind=link}

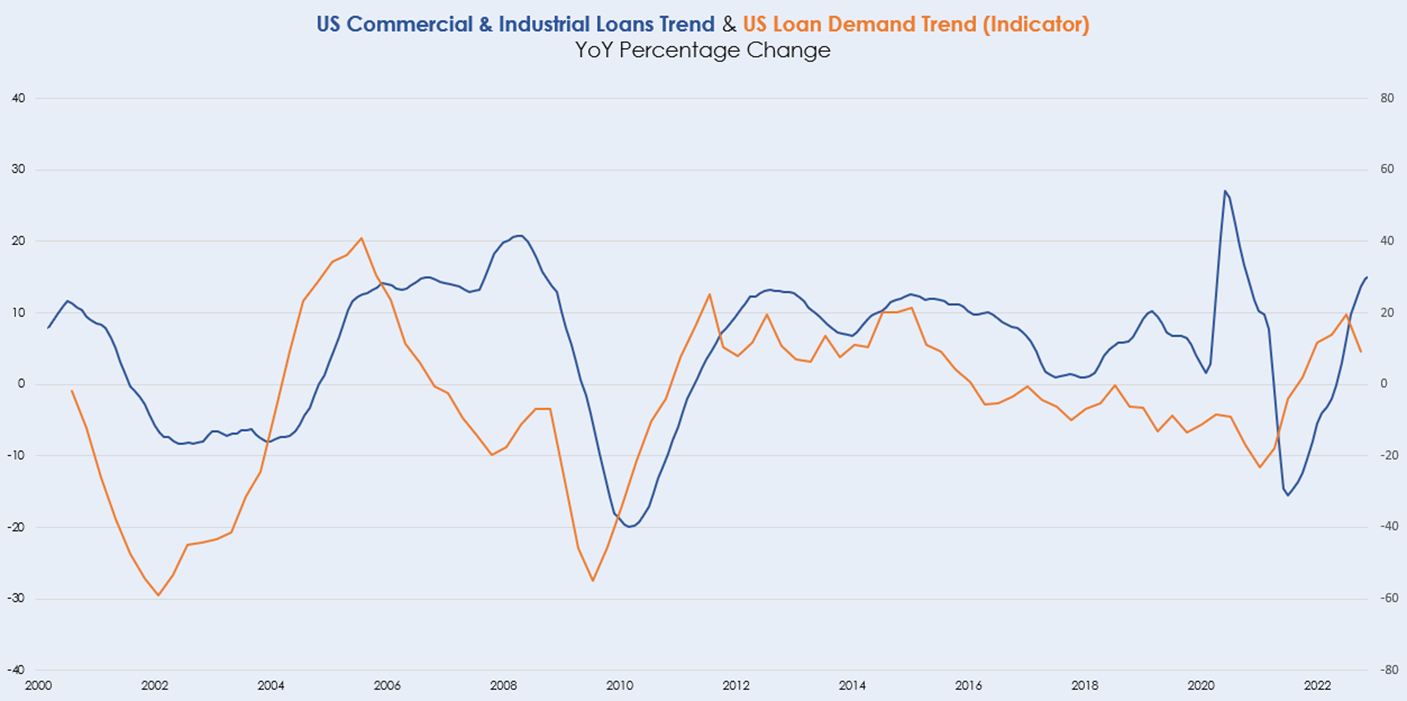

While consumers are likely going to cut spending in 2023 because of a worsening balance sheet, banks are starting to report decreased demand for commercial and industrial loans. The data isn't as clear because it's only reported quarterly. However, the reports from the banks roughly reflect loan demand and tend to lead actual commercial and industrial loans by 2-3 quarters.

US Commercial & Industrial Loans Trend & US Loan Demand Trend (Author, using Excel)

{kind=link}

Key takeaways

Inflation has peaked for now, and a soft landing is a valid scenario that deserves a small allocation in one's portfolio. I don't regard it as a base case, though. The Federal Reserve will likely cut rates fast, late, and not gradually. The prerequisite for cutting rates that fast is something breaking. I believe that the breaking part won't be bullish for equities.

2022 was a story of adjusting valuations to the risen risk-free rate (P of the P/E). If the Fed funds rate doesn't change during 2023, and the corporate profits turn out to be lower than expected, then the market has to adjust the E of the P/E. Valuations and Earnings Expectations are usually not bottoming at the same time.

The labor market is a lagging indicator and will likely rise only if the U.S. is in the midst of a recession already. Credit provision and PMIs are better indicators of corporate profits. Almost every data point is pointing toward a rather hard landing, which increases with every day the Federal Reserve keeps the monetary policy at a deeply restrictive level.

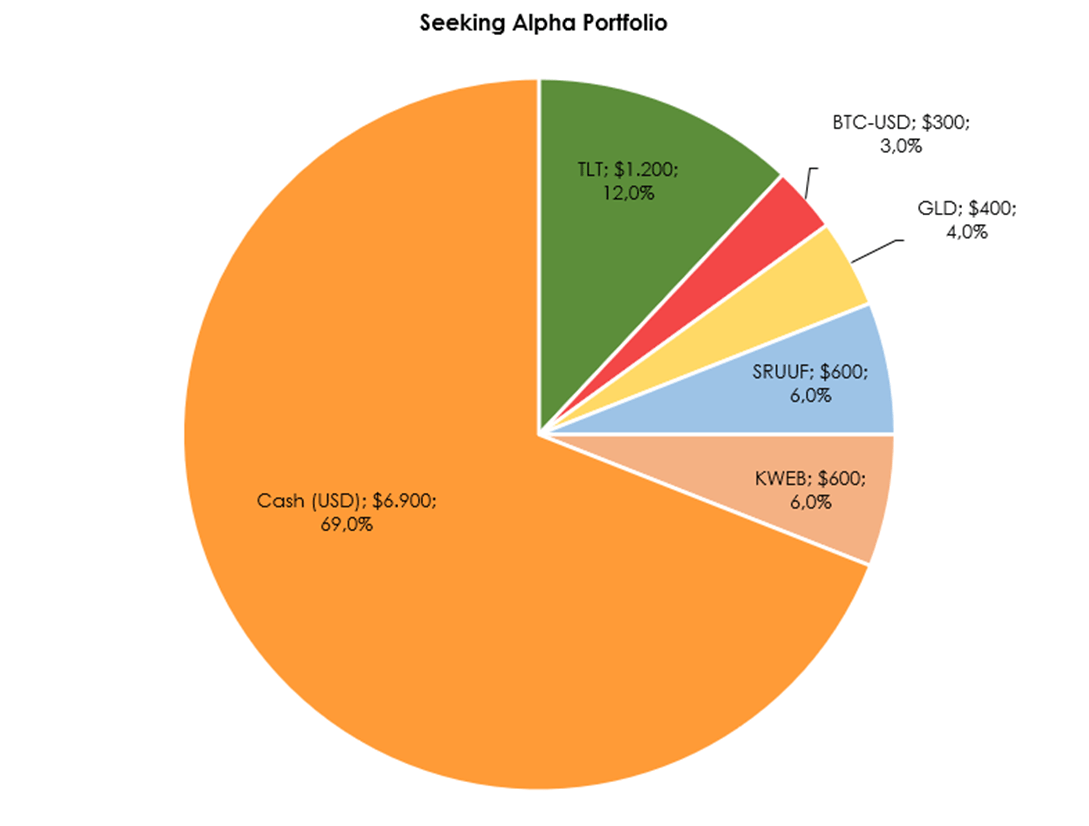

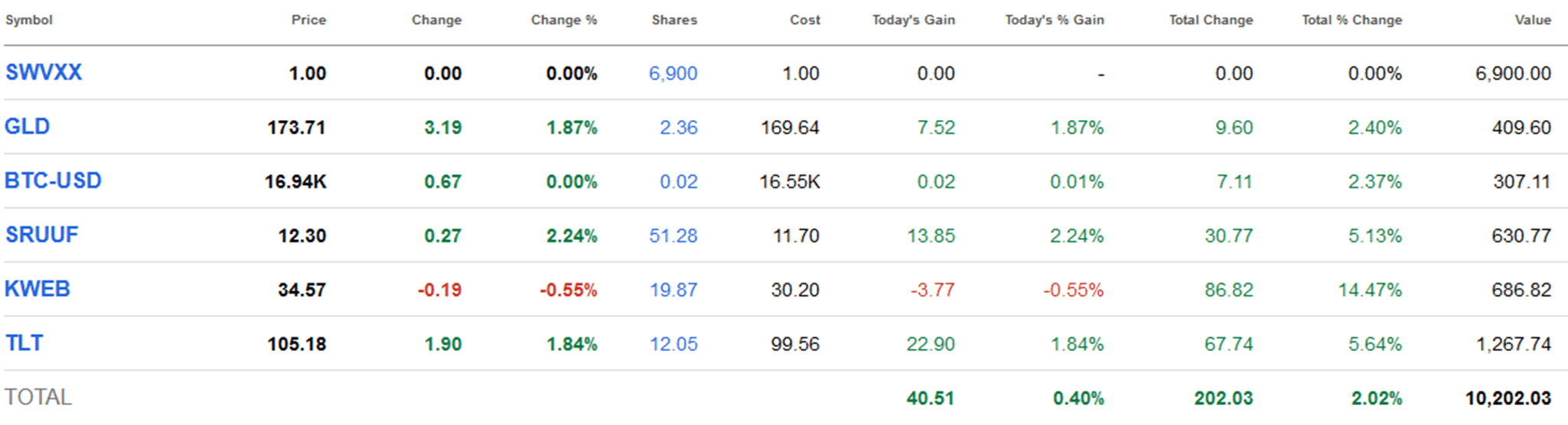

A model portfolio for Seeking Alpha

At the start of 2023, I built a small model portfolio using the tools of Seeking Alpha. It resembles a simplified version of my own portfolio. The starting capital is $10,000. I plan to illustrate my asset allocation with this tool from now on. I refer to my previous article for the reasoning of the positions: ( TLT ), ( BTC-USD ), ( GLD ), ( SRUUF ), ( KWEB ), ( SWVXX ).

{kind=link}

{kind=link}

For further details see:

A Goldilocks Economy? I Don't Think So