ADSK - A Hidden German Champion: Mensch und Maschine

2023-10-16 10:00:00 ET

Summary

- Mensch und Maschine Software SE is a hidden German champion in the construction software industry.

- MuM develops and distributes various software solutions, predominantly in Europe.

- The company benefits from secular tailwinds in the construction industry and has a growing dividend.

- At its current valuation, shares look cheap.

Mensch und Maschine Software SE ( OTC:MSHHF ) has been a hidden German Champion for a while but hasn't found much appreciation in the global investor community. This could be due to its German name and small cap under a billion Euros market cap. The name Mensch und Maschine translates to man and machine and the founder still holds 45.7% of shares outstanding, with an additional 6.1% of shares in the hands of the management team. Over the last decade, MuM (I'll use this abbreviation from now on) vastly outperformed the S&P 500 with share price appreciation and a fast-growing dividend.

{kind=link}

Construction software business model

The company develops and distributes its Computer-Aided Design ((CAD)), Manufacturing ((CAM)) and Engineering ((CAE)) software, as well as Product Data Management ((PDM)) and Building Information Management ((BIM)) software. The majority of sales, however, come from the VAR business, which develops customer-specific digitalization solutions, predominantly with standard software from competing companies like Autodesk ( ADSK ). It is basically a consulting business. Germany also has another hidden Champion in this niche, which I owned and covered earlier this year: Nemetschek ( OTC:NEMTF ); you can read my article here . The largest difference between the two is that Nemetschek is a software pure play, while the picture below shows the diversified nature of MuM. Around 65% of the business is VAR, with lower margins. 35% of software sales contribute 65% of the company's EBIT.

Business Mix (MuM Investor Presentation)

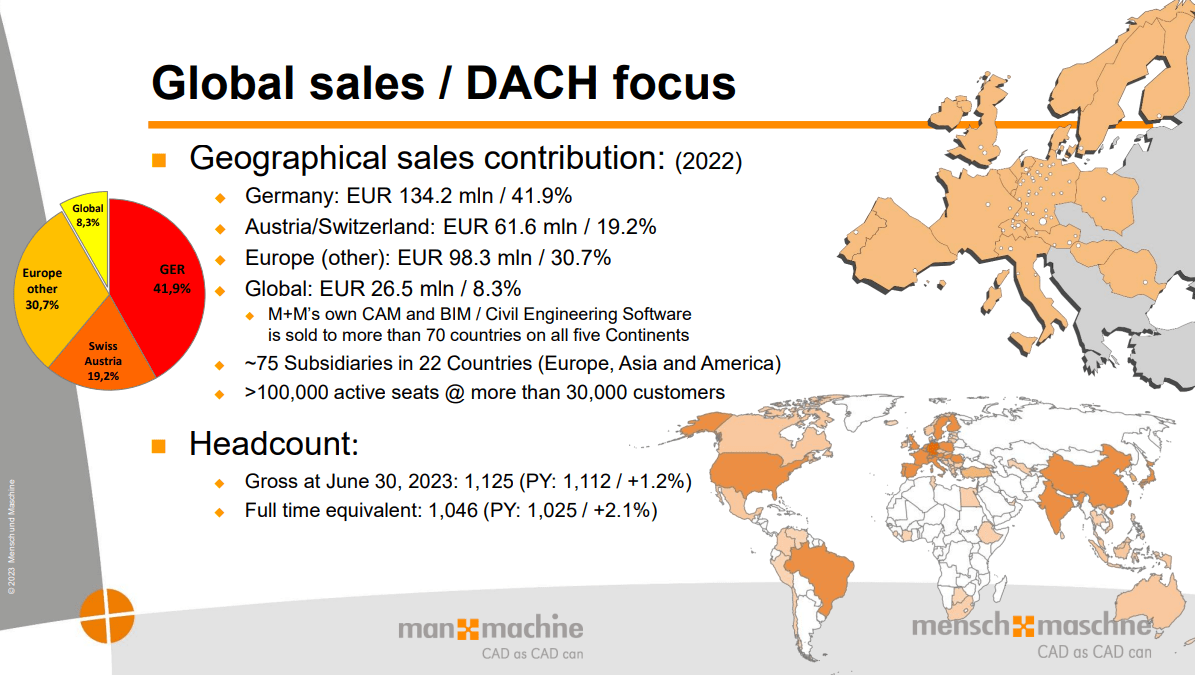

While the company is global, it focuses on Europe (30.7% of sales) and especially DACH (Germany, Austria and Switzerland; 61.1% of sales). Global customers represent just 8.3% of sales and a big opportunity for further expansion.

{kind=link}

MuM benefits from similar secular tailwinds as Nemetschek. Construction is a vast market at over $12 trillion globally, contributing around 40% of global CO2 emissions, with millions of small players and the majority lagging on digitalization. Proper planning software can reduce costs, reduce waste and improve the utilization of tools and employees. This is especially crucial as there is a lack of workforce in the industry. These tailwinds should help both companies realize good organic revenue growth for many years.

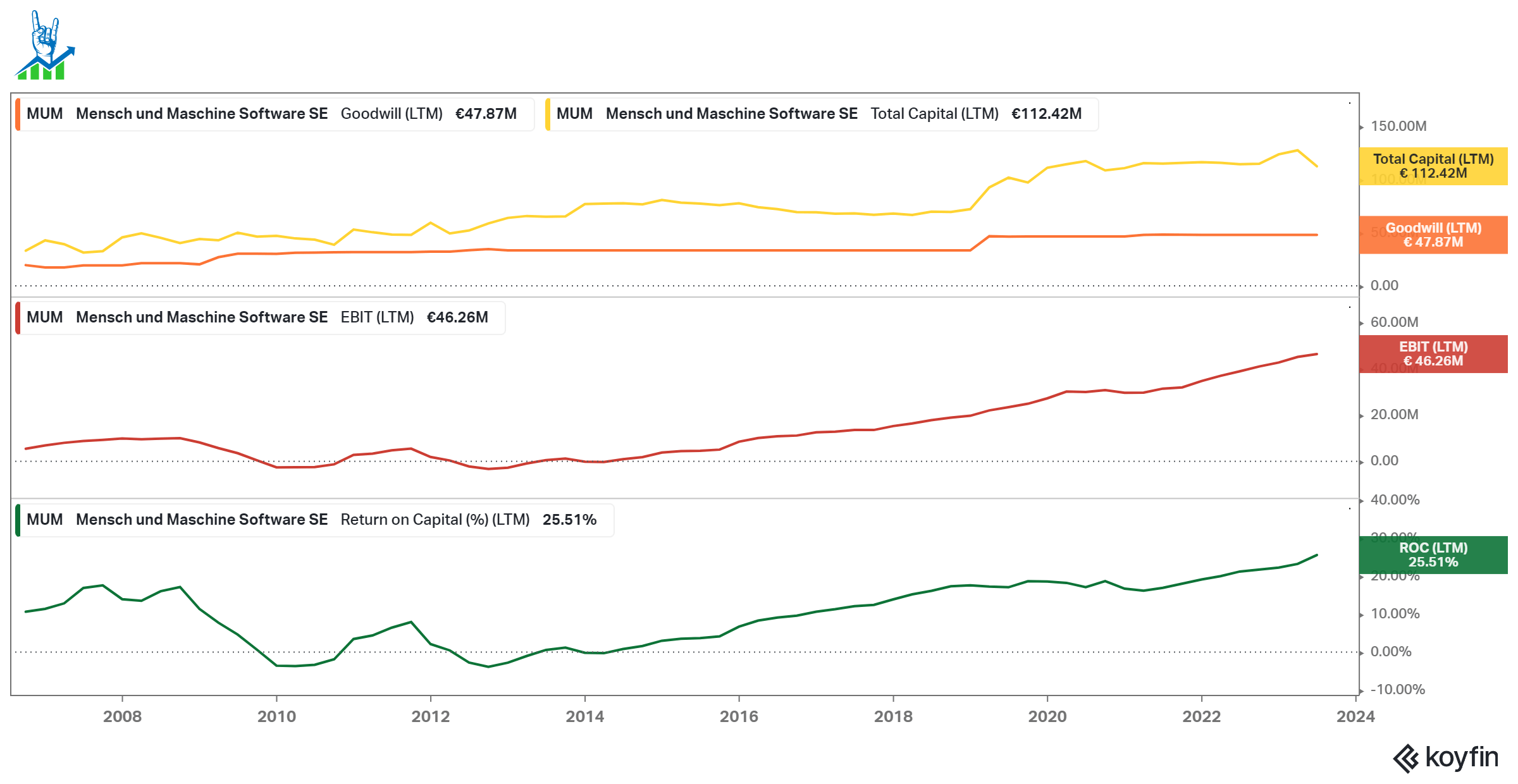

MuM generated good returns on invested capital with 25% in the last twelve months. The company has a lot of goodwill on its balance sheet, much like Nemetschek, but growing EBIT with a steady capital base has increased ROIC over recent years.

{kind=link}

A growing, well covered Dividend

MuM is a committed dividend payer with a long history of consistent raises. Over the last three years, the dividend grew 18% each year, with the rolling three-year CAGR median at 26% over the past decade. The rapidly growing dividend accounts for 83% of net income but just over 50% of Free Cash Flow, so there is enough room for further increases from this current 3% yield. MuM has continuously improved its net working capital and thus achieves much higher cash flows than earnings. Buybacks are not a large part of the shareholder return for MuM, but they do buy back occasionally, they do however dilute shareholders as well.

{kind=link}

MuM Dividend history (Koyfin)

MuM is cheap

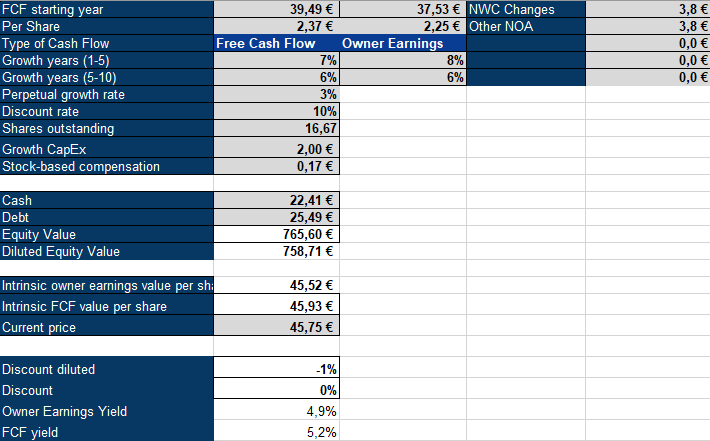

To value MuM, I'll use an inverse DCF model. As a software company, they do not require a lot of capital expenditures, with just $6.6 million of annual capex. Stock-based compensation expenses are also low. Sadly, we do not get a good split between Net Working Capital changes and only get the result. Using these adjustments, we arrive at 37.5 million Euro in Owner Earnings. This implies 8% growth for the next five years and 6% for the following five.

{kind=link}

MuM guided for 26% EBIT growth this year and expects its profits to double in 4-5 years, implying a mid-term guidance of 14-18% growth. This seems realistic, given their industry's structural tailwinds and the underpenetrated markets they can tackle. 14-18% is significantly above the 8% required by the model, so I'll put a buy rating on MuM. While Nemetschek is more expensive, I still prefer and own the company instead of MuM because I like the software pure-play aspect more than the consulting business in MuM. I believe both companies have a bright future and investors should take a second look at both.

For further details see:

A Hidden German Champion: Mensch und Maschine