SOHON - A Softish Landing

Summary

- U.S. equity markets resumed their rebound this past week as investors parsed a busy slate of corporate earnings results and economic data ahead of the Federal Reserve's rate hike decision.

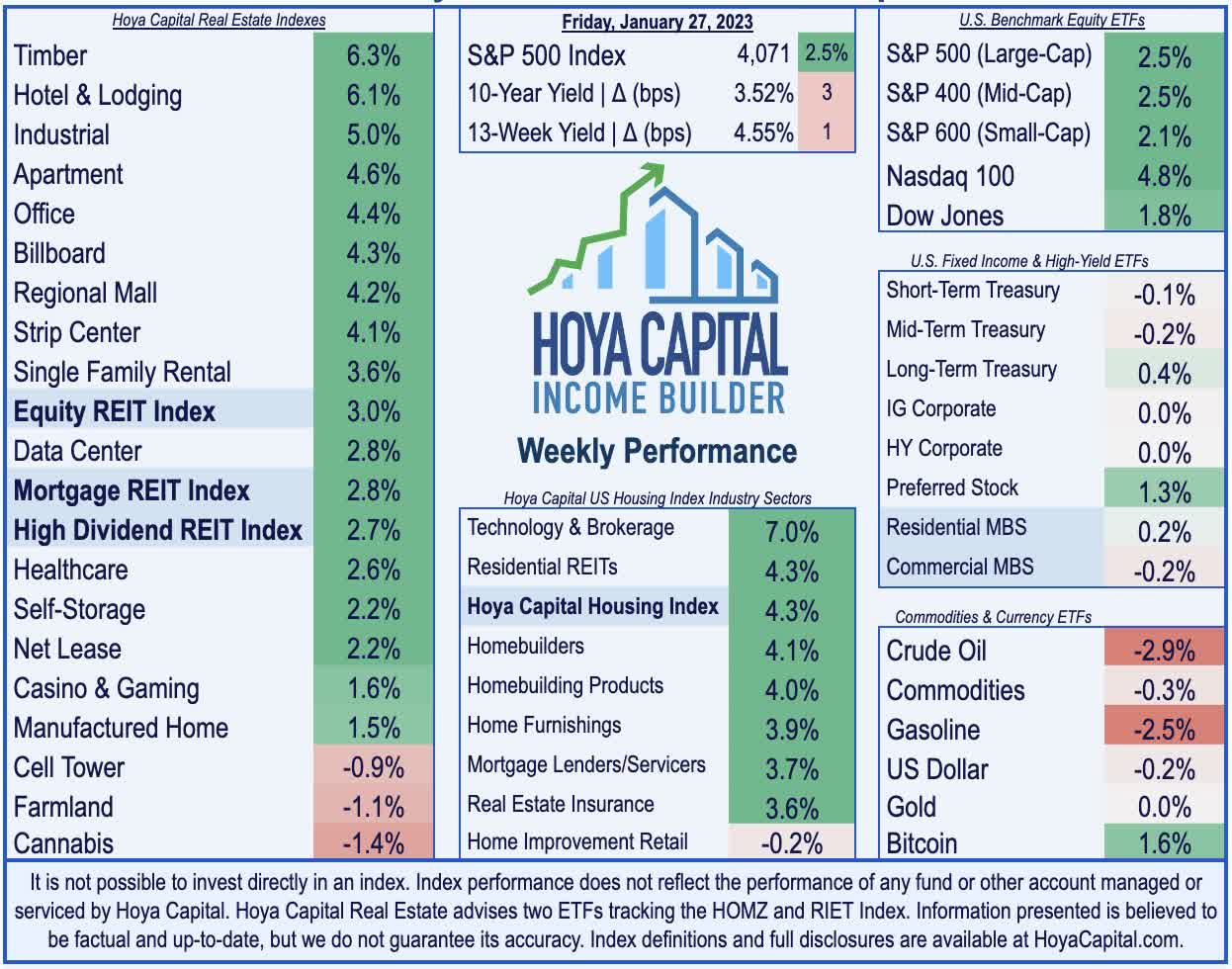

- Gaining for the third week in the past four, the S&P 500 advanced 2.5% on the week while the tech-heavy Nasdaq rallied nearly 5% - its fourth-straight week of gains.

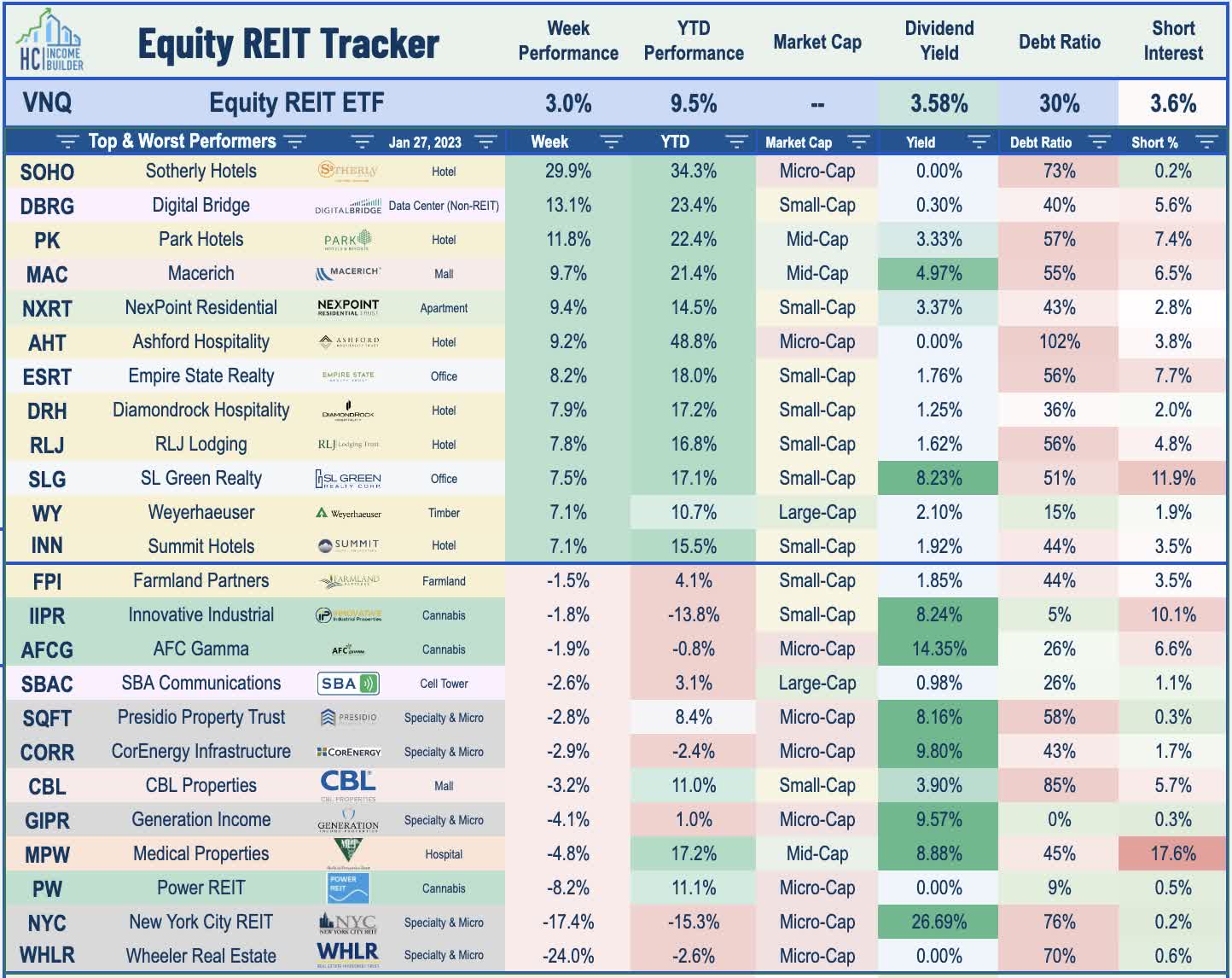

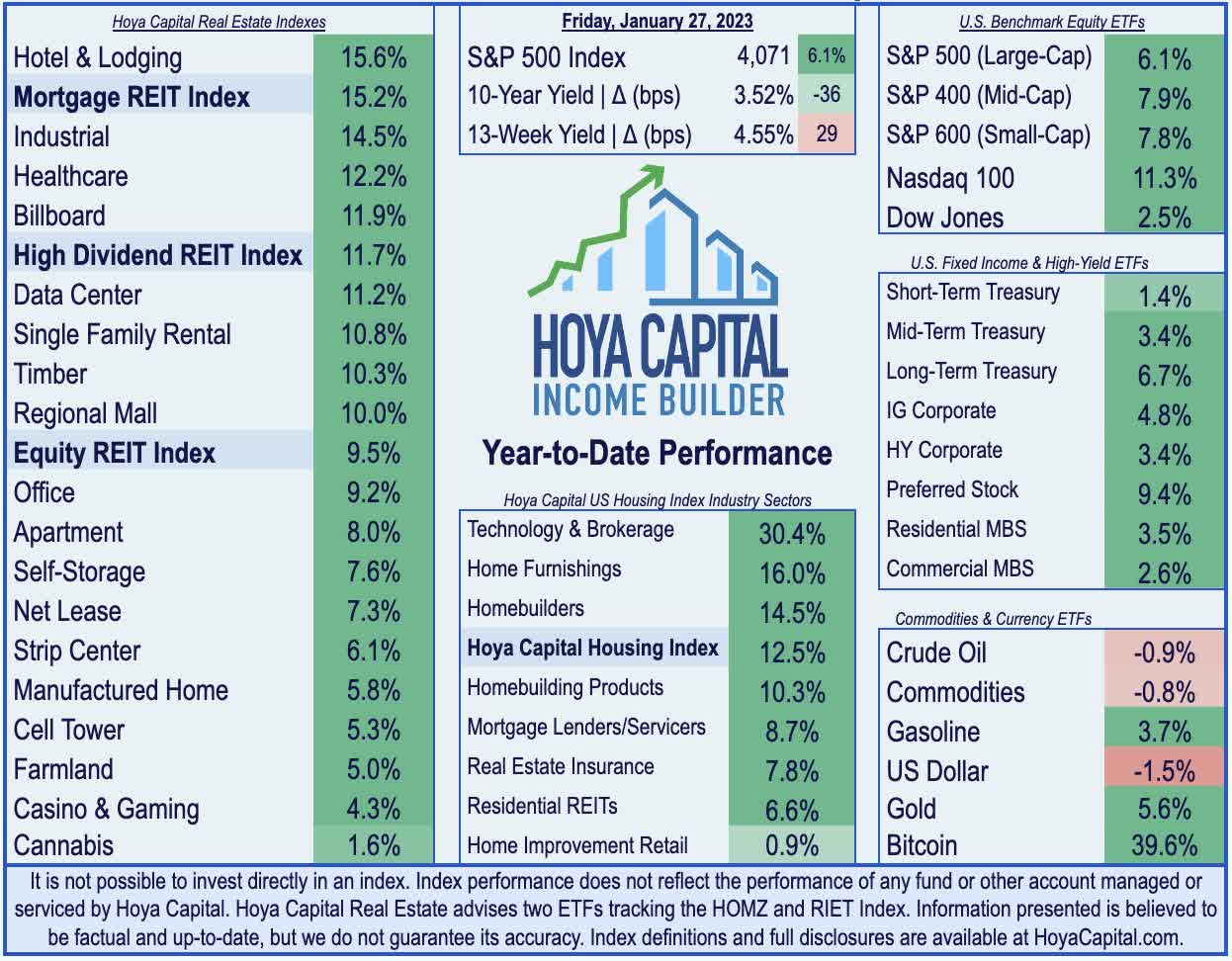

- Real estate equities also continued their hot start to the new year as earnings season kicked into gear. The Equity REIT Index advanced another 3.0% while Mortgage REITs gained 2.5%.

- Timber REIT Weyerhaeuser and office REIT SL Green rallied after reporting earnings results. Sotherly Hotels surged nearly 30% this week after it reinstated its preferred distributions.

- Homebuilders rebounded on signs of thawing in the icy-cold housing market that was left for dead in late 2022 - an industry that must stabilize to keep 'soft landing' hopes alive.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on January 27th.

U.S. equity markets resumed their rebound this past week as investors parsed a busy slate of corporate earnings results and economic data before the Federal Reserve's rate hike decision in the coming week. With a potential "soft landing" still very much hanging in the balance, relatively decent economic data - including a better-than-expected GDP report, cooling PCE inflation, and signs of life in the icy-cold housing sector - were juxtaposed with a cautious corporate earnings outlook defined by a focus on cost-cutting and layoffs.

{kind=link}

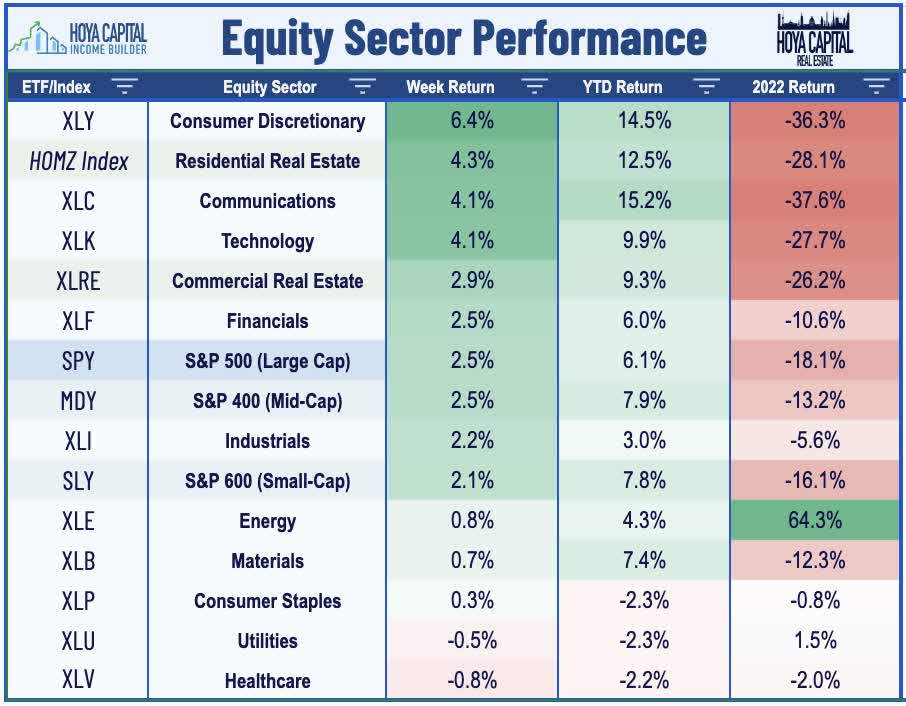

Gaining for the third week in the past four, the S&P 500 advanced 2.5% on the week while the tech-heavy Nasdaq 100 rallied nearly 5% - its fourth-straight week of gains, the longest winning streak since August. Real estate equities also continued their hot start to the new year as earnings season kicked into gear. The Equity REIT Index advanced another 3.0% this week, while the Mortgage REIT Index gained 2.8%. Homebuilders and the broader Hoya Capital Housing Index continued their particularly strong start to the new year with gains of over 4% following another slate of encouraging signs of life for a housing market that was left-for-dead in late 2022.

{kind=link}

Benchmark interest rates ticked slightly higher this week as investors parsed the final slate of economic data before the Federal Reserve's rate hike decision. The 10-Year Treasury Yield rose 3 basis points to 3.52% - up slightly from its four-month lows of 3.37% earlier in the month but substantially below its recent highs last October of 4.29%. Energy prices remained in focus this week given their critical importance for the inflation outlook and, by extension, the monetary policy path. Futures on Natural Gas - the largest source of U.S. electric generation and among the most influential inflation inputs - dipped to 20-month lows amid mild winter weather across North America and Europe, helping to offset potential inflationary pressure from a recent rebound in Crude Oil prices and consumer Gasoline prices, which have each bounced about 15% from their December lows.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

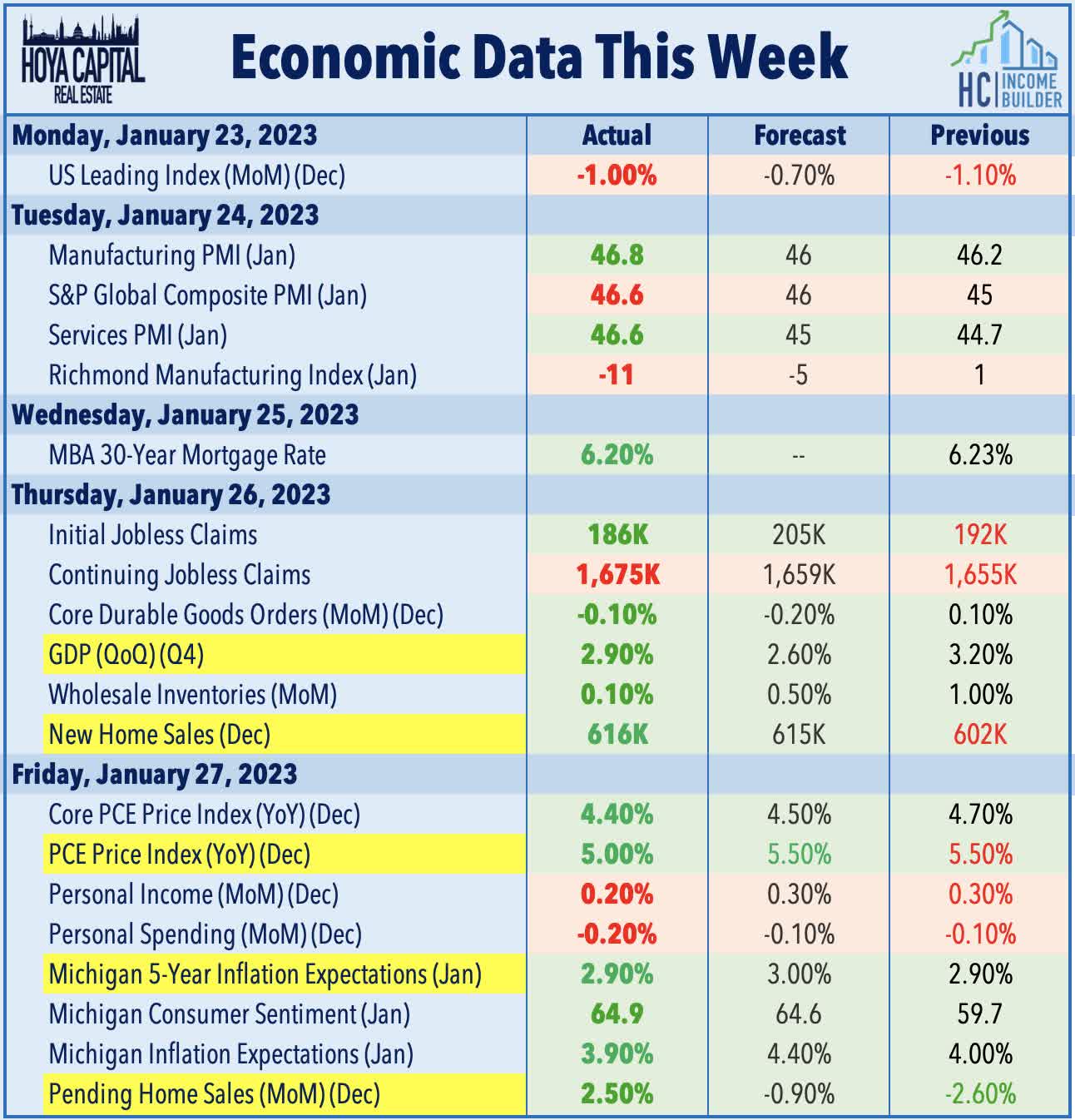

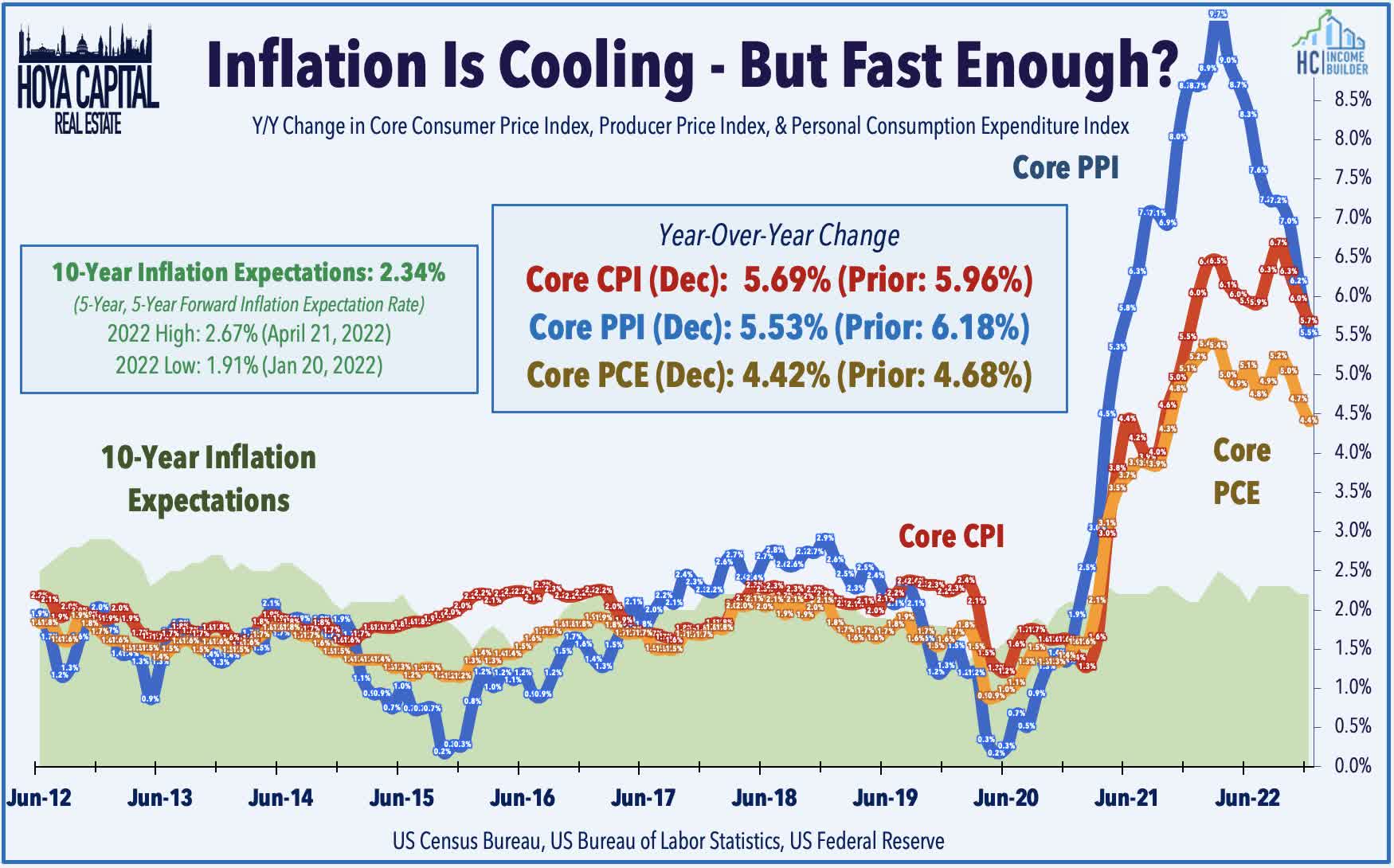

While "peak" inflation now appears firmly in the rear-view as the effects of pandemic-era fiscal expansion fade, there remains an unanswered question about whether "trend inflation" ultimately settles back in the 2-3% pre-pandemic range or at an elevated 3-5% sustained level - the answer to which has significant implications for central bank policy and financial asset values. Personal Consumption Expenditures data this week pointed more to the former with the Core PCE posting a 4.4% increase from a year ago in December - its smallest annual increase since October 2021. The cooler-than-expected PCE print follows data last week showing that the CPI-ex-Shelter Index - the metric that showed the surge in inflation a year before it was reflected in the headline CPI - was negative for the fifth month in the past six, recording one of the most deflationary six-month periods for that particular metric on record.

{kind=link}

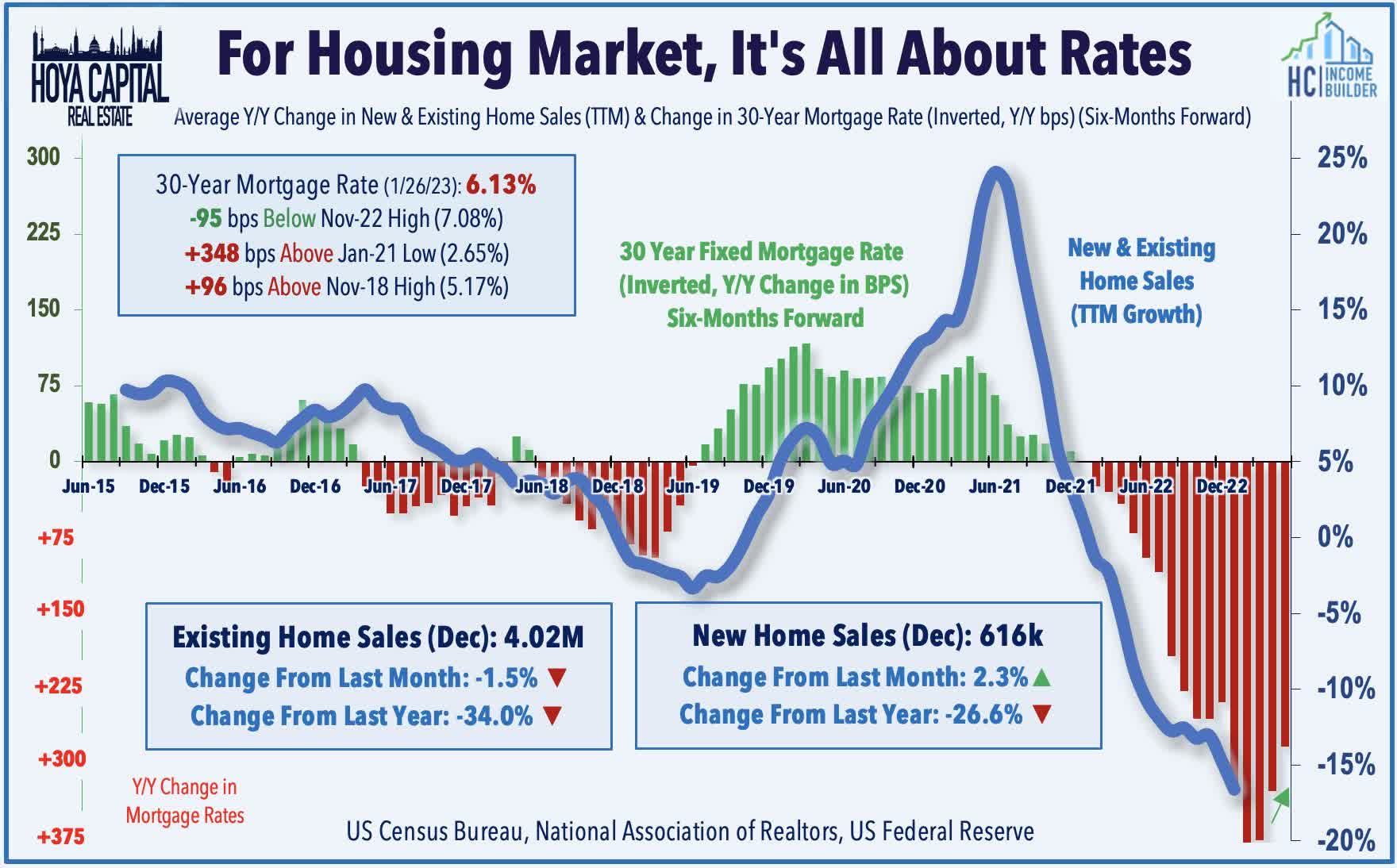

Cooling rate pressures can't come soon enough for the U.S. housing sector, which continues to bear the brunt of the impact of extreme monetary tightening. A busy slate of data this week showed that the icy-cold housing sector has shown early signs of thawing in recent weeks amid a pullback in rates with New Home Sales and Pending Home Sales each advancing in December from the prior month while mortgage market data showed a second-straight week of rebounding purchase demand. D.R. Horton ( DHI ) - the nation's largest homebuilder - reported better-than-expected earnings results highlighted by a decline in its cancellation rate to 27% from 32% in the prior quarter. DHI delivered 17,340 during the quarter - above the upper end of its guidance range of 16,500 - buoyed by incentive offers and reductions in home prices "where necessary to optimize returns."

{kind=link}

Brokerage firm Redfin ( RDFN ) also reported "early indicators of homebuyer demand, including tour requests and mortgage applications, are increasing from their low point." Its Redfin Homebuyer Demand Index—a measure of requests for home tours and other homebuying services—was up 6% from a month earlier during the four weeks ending January 22. The path of the housing industry in 2023 will have major implications on the ability to avoid a recession. Gross Domestic Product data this week showed that Residential Fixed Investment was responsible for a 1.3% drag on fourth-quarter GDP - a slight improvement from the 1.4% drag in the prior quarter which was historically bad, exceeded in magnitude by the 1.54% drag in Q4 2007.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hotels : Sotherly Hotels ( SOHO ) surged nearly 30% this week after it reinstated its preferred distributions on its three preferred issues which had been suspended since early 2020. SOHO noted that it intends to pay the accrued dividends through "periodic announcement of special dividends, as warranted by market conditions and the Company’s profitability.” This week, we published Hotel REITs: Dividends Are Back which discussed the surprising resilience in hotel demand during recent months as several years of pent-up leisure demand helped to offset a sluggish business and group travel recovery. Hotel revenues eclipsed record highs in 2022, but with wide dispersion between markets and segments. We noted that remote work is changing the complexion of business demand - but not necessarily for the worse. The "traveling salesman" visits are being replaced by more frequent group events, which combined with increased work-from-anywhere "bleisure" trips, are skewing demand towards more "destination" segments.

{kind=link}

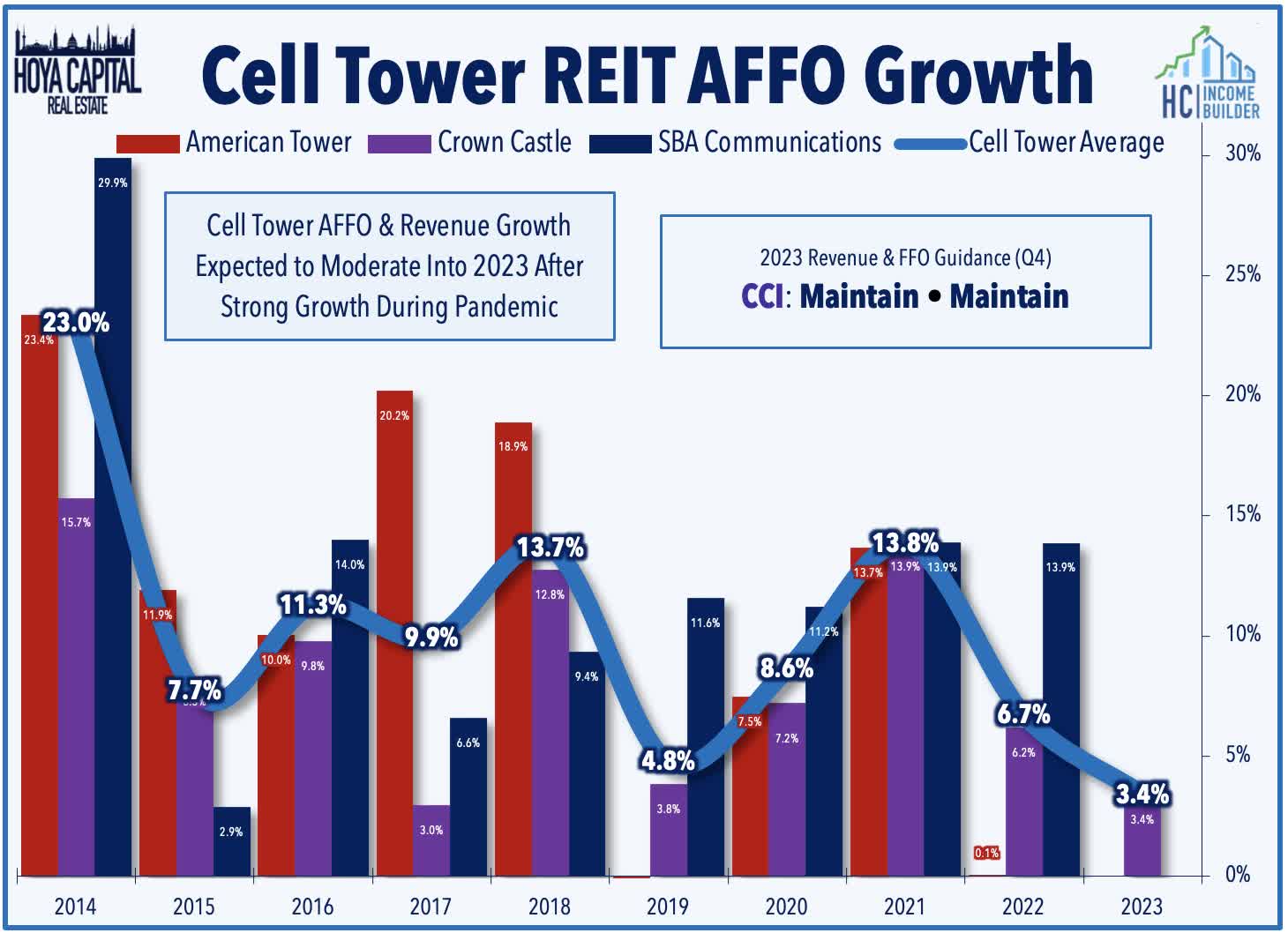

Cell Tower : Crown Castle ( CCI ) - which we own in the REIT Focused Income Portfolio - traded roughly flat on the week after reporting in-line fourth-quarter results, recording full-year revenue growth of 10% and FFO growth of 6.2% - each slightly above the midpoint of its most recent guidance while maintaining its outlook for full-year 2023 which calls for revenue growth of 3.0% and FFO growth of 3.4% as near-term headwinds from higher interest rates and the effects of the Sprint churn offset projected organic revenue growth of 6.8% (4.2% excluding Sprint). CCI noted that this 4.2% organic growth consists of 5% growth in towers, 8% growth in small cells, and flat revenue in fiber solutions. American Tower ( AMT ) was also in focus after reports that it's considering a bid for Cellnex ( OTCPK:CLNXF ) - a Spanish telecom operator which operates roughly 100k communications sites across Europe with a $25B market cap. Analysts expressed doubt over the likelihood of a deal given AMT's recent focus on deleveraging and lack of interest in large-scale M&A.

{kind=link}

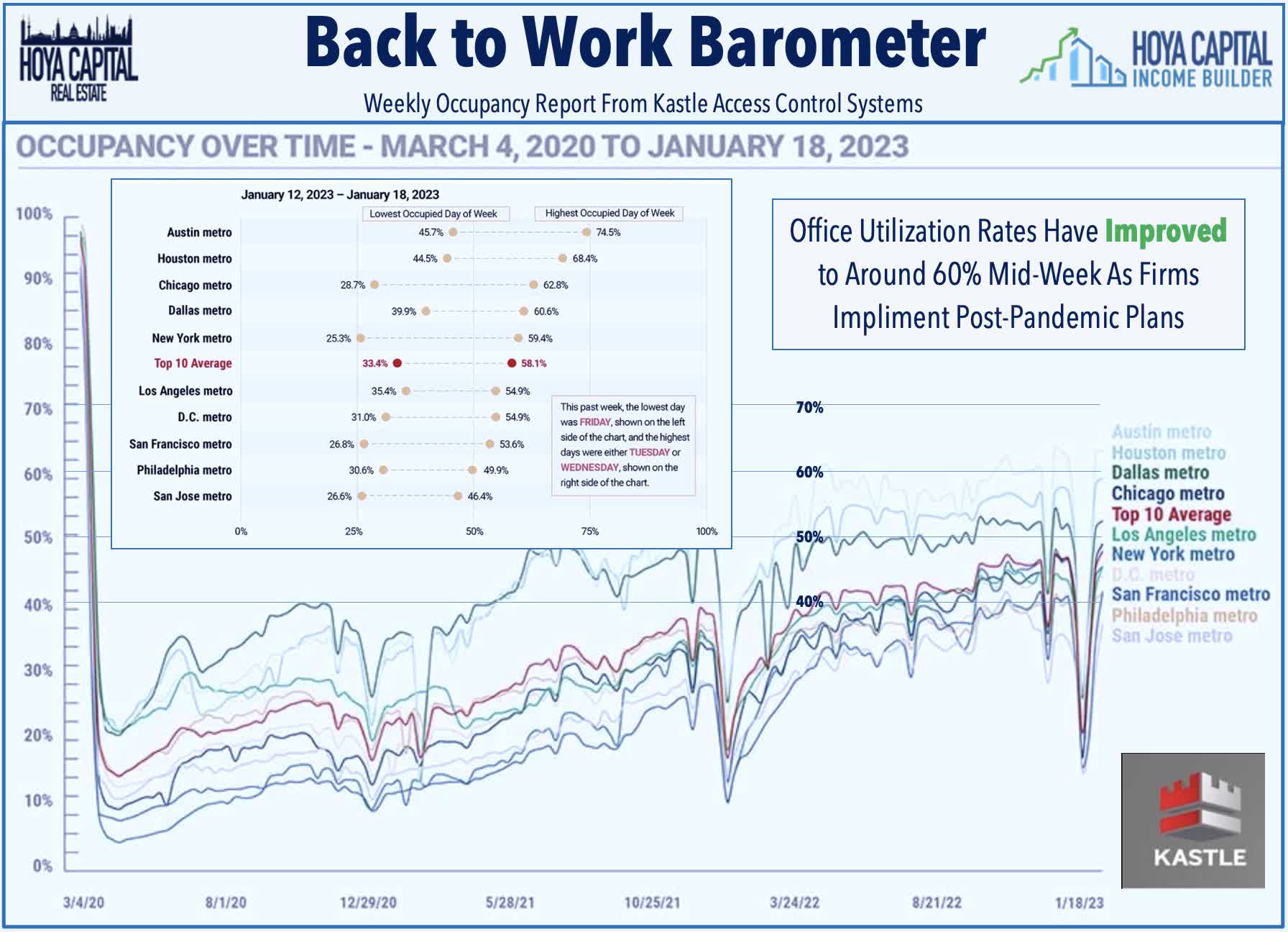

Office : NYC-focused SL Green ( SLG ) rallied more than 7% this week after reporting mixed fourth-quarter results, recording top-line metrics that roughly matched analyst expectations while noting continued downward pressure on rents and occupancy rates. Occupancy in SLG's Manhattan same-store office portfolio dipped to 91.2% - down 90 basis points from Q3 - while it recorded negative leasing spreads on renewed leases of -4.7% for the quarter and -9.2% for full-year 2022. Recent data from Kastle Systems shows that office utilization rates have improved only marginally in most major markets since last April with the national average still sitting below 50%. Consistent with the trends throughout the pandemic, Sunbelt and secondary markets have seen significantly higher utilization rates compared to coastal urban markets. Notably, among the Top 10 markets, Austin and Houston each recorded mid-week utilization rates at over 70% of pre-pandemic levels.

{kind=link}

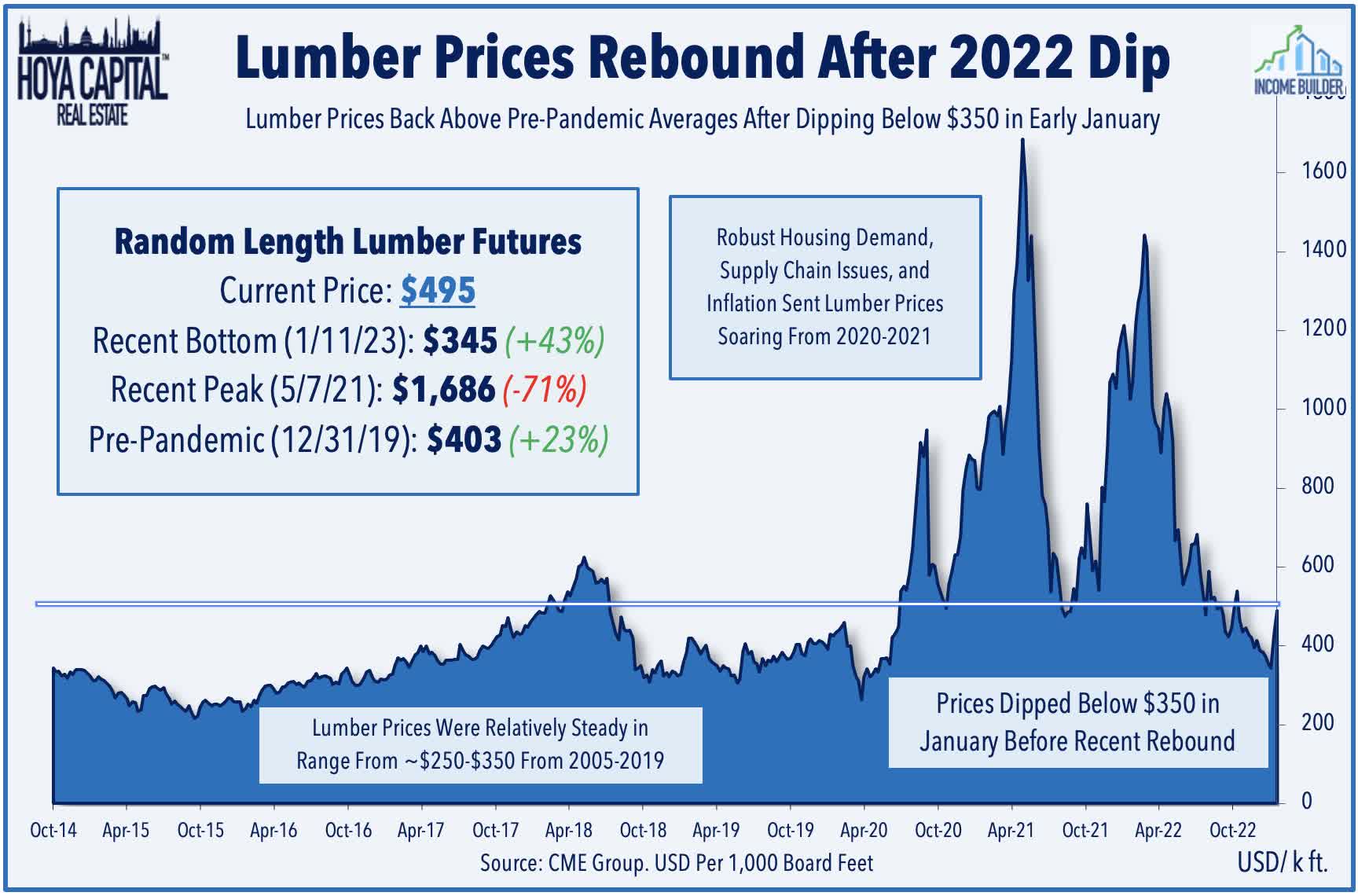

Timber : Weyerhaeuser ( WY ) rallied more than 7% on the week after reporting solid fourth quarter results and declaring a $0.90/share supplemental special dividend - the second year of its "base plus variable" dividend framework which is adjusted based on profitability. WY noted that its seeing "some improvements in certain macroeconomic and housing-related trends" after a period of slow demand in the back-half of 2022. Adjusted EBITDA for full year 2022 was $3.7 billion - down about 10% from the record $4.1 billion in adjusted EBITDA in 2021. Looking ahead, the company expects its three major operating units to post higher adjusted EBITDA in the first quarter. Notably, alongside signs of stabilization in housing demand amid a retreat in mortgage rates, lumber prices have rebounded since bottoming in early January with prices per thousand-board-feet around $500 - down from the incredible surge to nearly $1,700 in 2021, but up from recent lows of $350.

{kind=link}

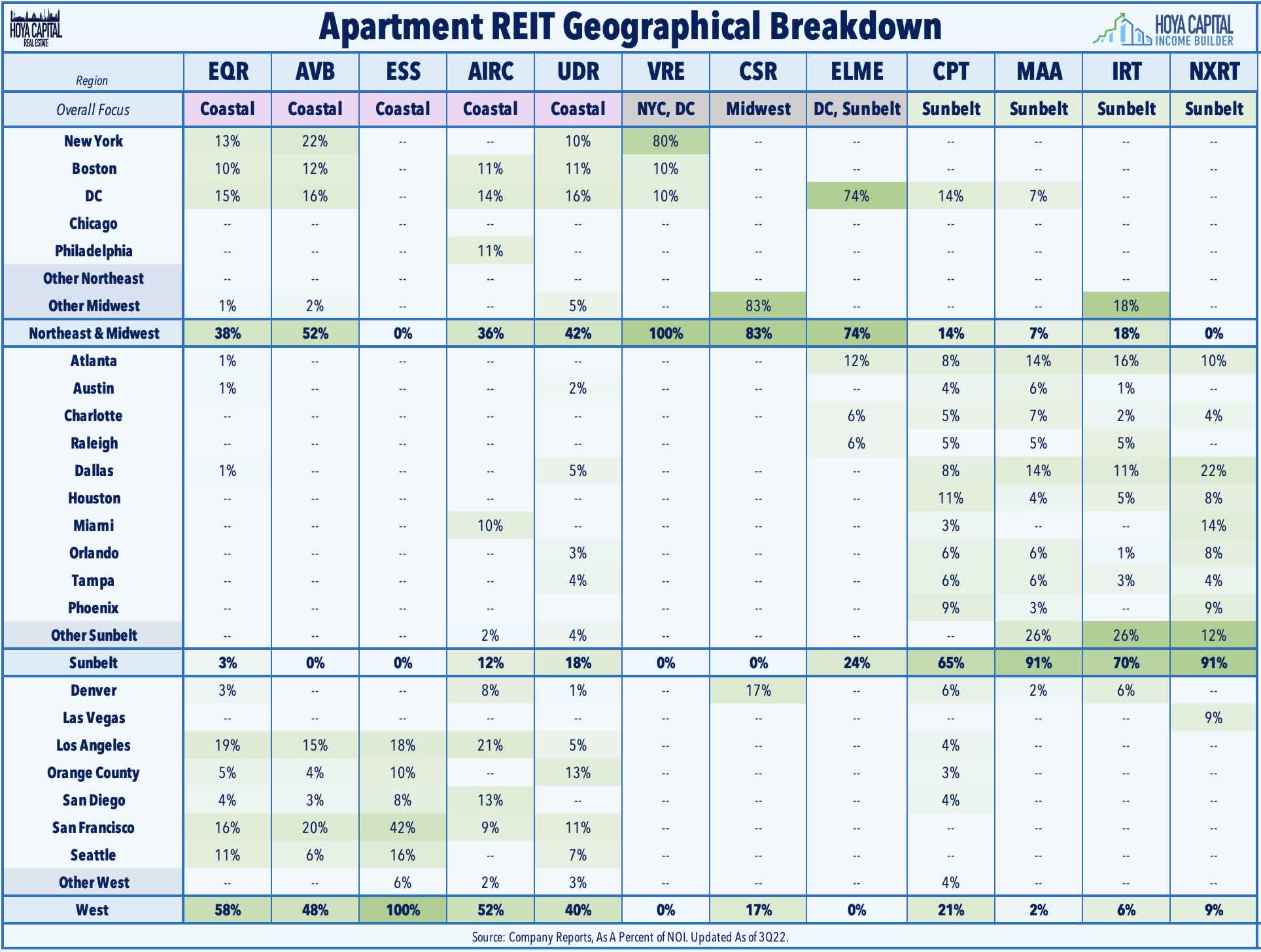

Apartment : NexPoint Residential ( NXRT ) - which we own in the REIT Dividend Growth Portfolio - rallied nearly 10% on the week after announcing that it closed on the $20.6M sale of Hollister Place - a 260-unit apartment property in Houston - at a trailing nominal cap rate of 4.37%. NXRT also announced an agreement to sell Old Farm and Stone Creek at in Houston for roughly $63M - an approximate trailing nominal cap rate of 4.97%. With the completion of these sales the refinancing of a Phoenix property, NXRT expects to pay off the full $73M outstanding balance on its corporate credit facility by the second quarter of 2023. NXRT commented that it "fulfilled our strategic objectives to sell out of our positions in Houston, completing our portfolio refinancing initiatives, and paying off our most expensive debt capital."

{kind=link}

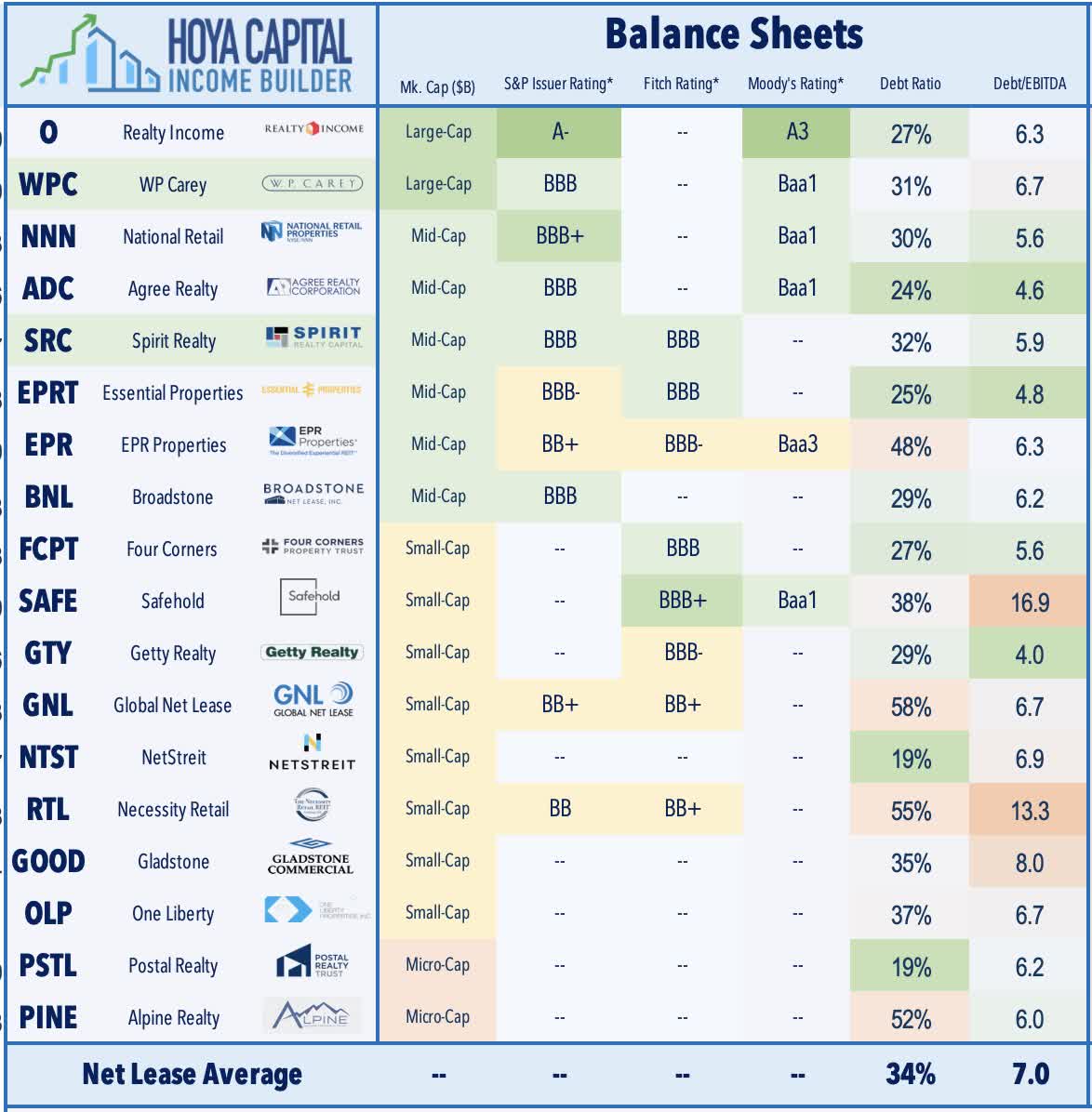

Net Lease : W.P. Carey ( WPC ) - which we own in the REIT Focused Income Portfolio - advanced 2% on the week after it received a credit rating upgrade from S&P Global, which boosted its rating to BBB+ from BBB on expectations that its contractual rent increases and acquisitions will support further operating outperformance over the next two years despite recession risks. As analyzed in Net Lease REITs: Calling The Fed's Bluff , WPC is poised to deliver outsized FFO growth over the coming year due to its inflation-linked rent escalators across over 50% of its portfolio. S&P Global noted that it expects demand to "remain healthy over the next several years," reflecting solid net lease industry fundamentals. Spirit Realty ( SRC ) - which we own in the REIT Focused Income Portfolio - rallied nearly 4% on the week after Fitch Ratings affirmed its credit ratings at “BBB” with a stable outlook.

{kind=link}

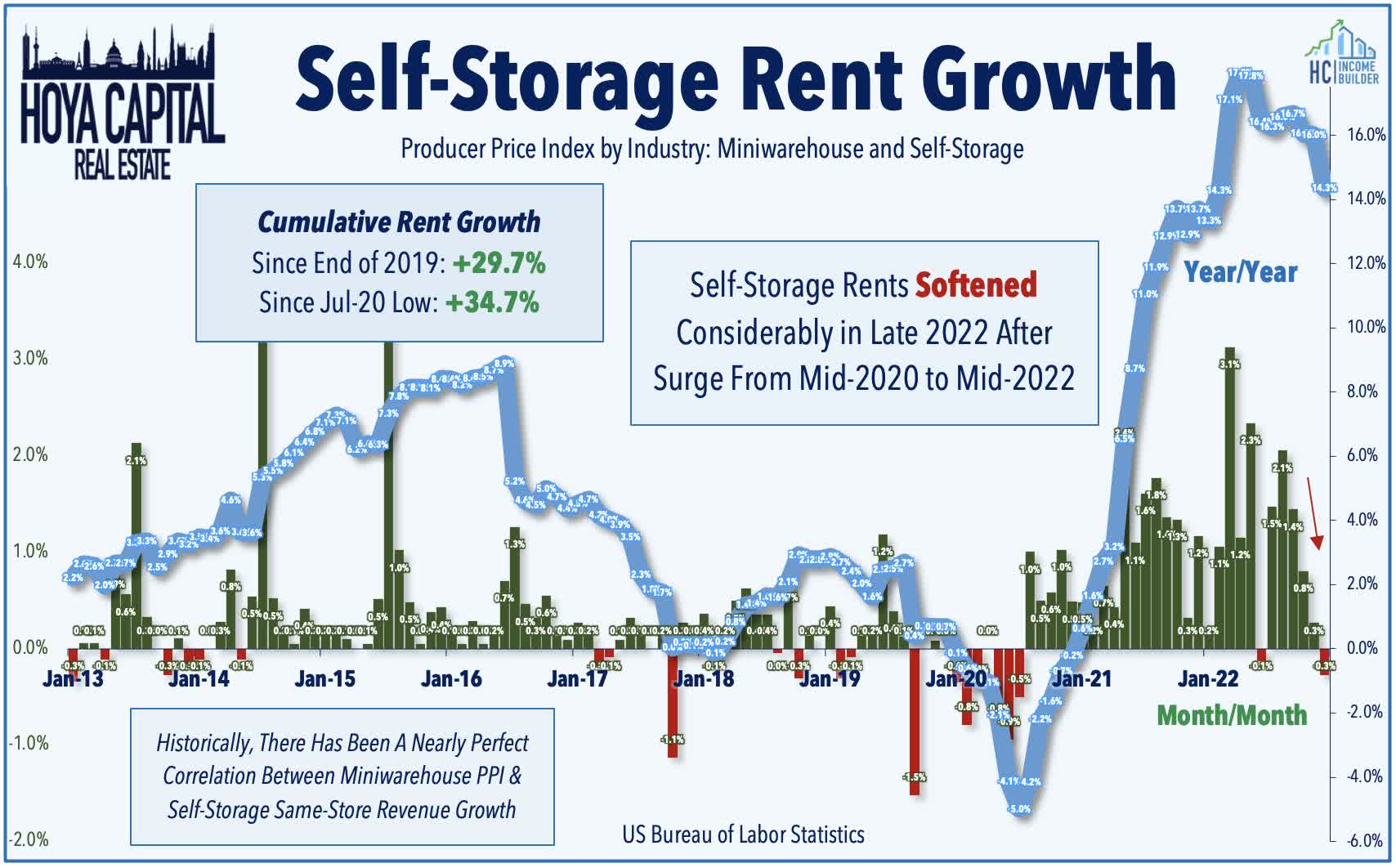

Storage : This week we published Self-Storage REITs: Downsized Demand which analyzed why storage REITs have lagged over the past quarter despite delivering the strongest earnings growth of any property sector since the start of the pandemic. Storage demand is driven largely by housing activity - specifically home sales and rental market turnover - and while we've seen some encouraging hints at a housing demand recovery in recent weeks, we don't think that the soft patch for storage REITs is fully discounted, potentially providing better buying opportunities later this year. Patience will be required over the next several quarters as expectations adjust to the post-pandemic normalization, but we continue to like the longer-term prospects for the storage sector given the 'stickiness' of demand, strong balance sheets, low cap-ex needs, and impressive operational track record.

{kind=link}

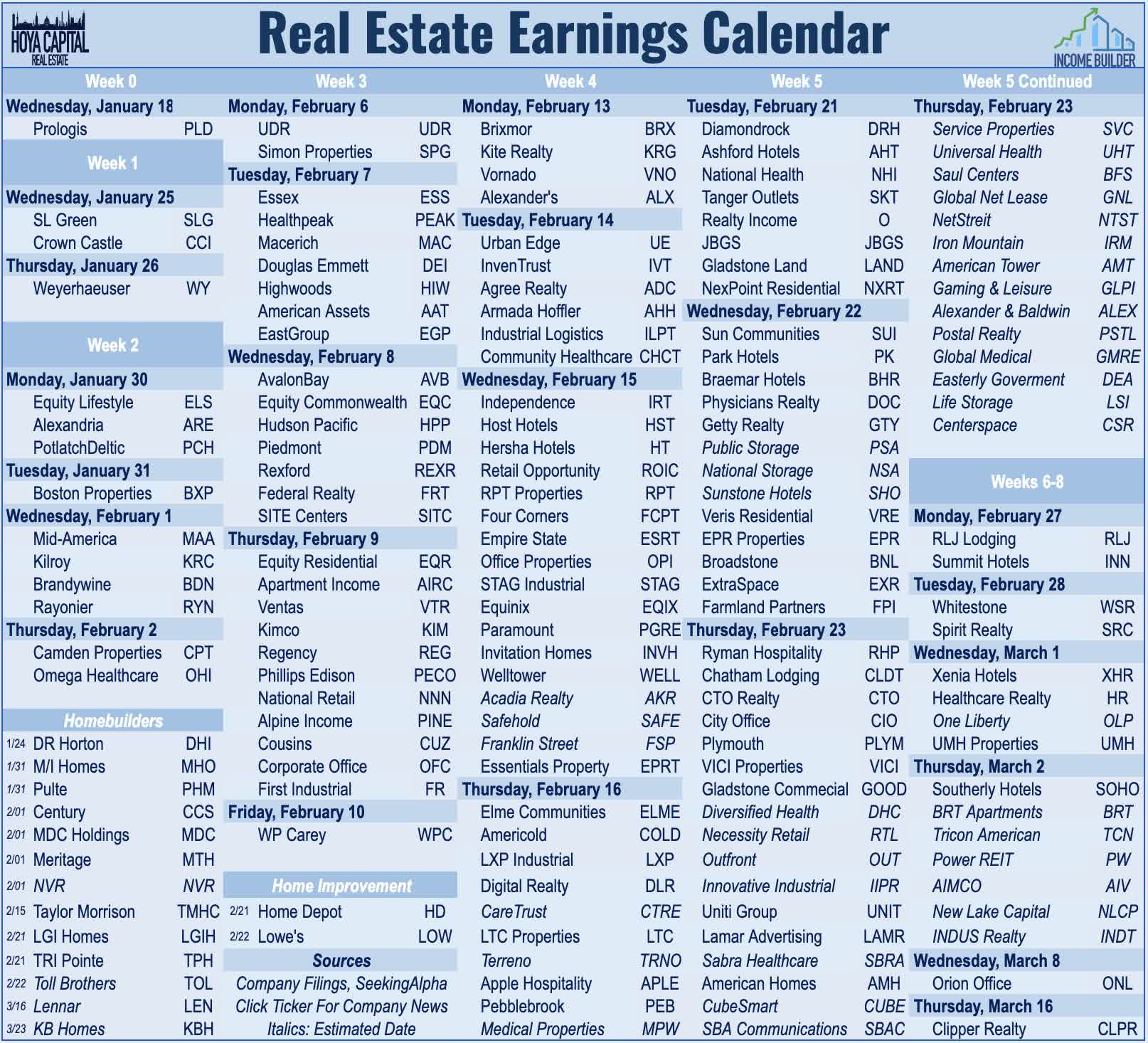

The real estate earnings calendar heats-up next week with results from a dozen REITs alongside a half-dozen homebuilders. On Monday, we'll see results from Equity LifeStyle ( ELS ), Alexandria ( ARE ), and PotlatchDeltic ( PCH ). On Tuesday, Boston Properties ( BXP ) reports results followed by reports on Wednesday from Mid-America ( MAA ), Kilroy ( KRC ), Brandywine ( BDN ), and Rayonier ( RYN ). On Thursday, Camden Properties ( CPT ) and Omega Healthcare ( OHI ) round out the week. We'll publish our Earnings Preview report this weekend which will discuss the major themes we're watching over the next six weeks of REIT earnings reports.

{kind=link}

Mortgage REIT Week In Review

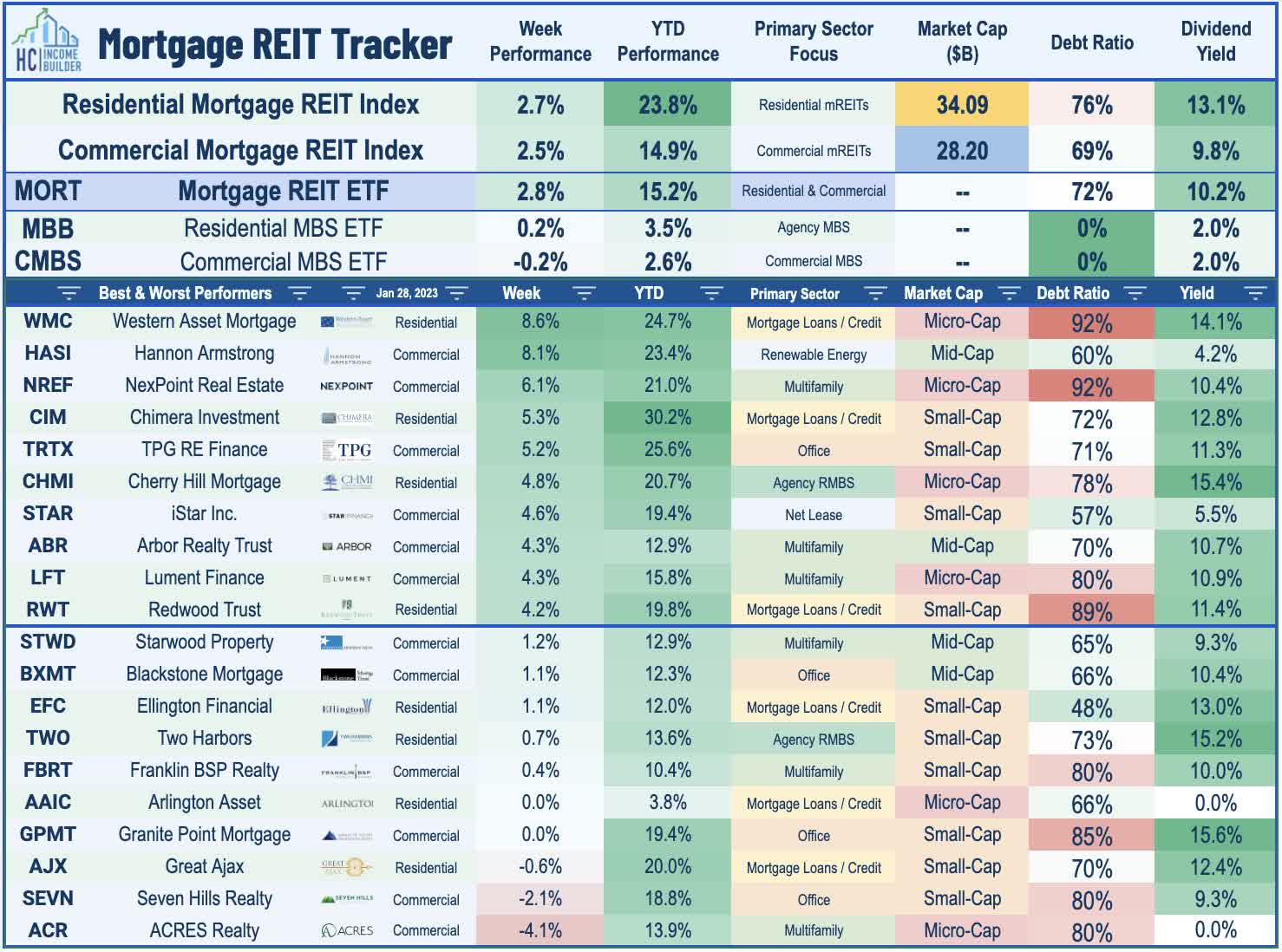

Mortgage REITs continued their stellar start to the year with the iShares Mortgage REIT ETF ( REM ) advancing another 2.8% on the week, pushing its year-to-date gains to over 15%. Residential mREITs have led the rebound this year with average gains of nearly 25%, buoyed by a revived bid for residential mortgage-backed bonds as the iShares MBS ETF ( MBB ) - an unlevered index of residential mortgage-backed bonds - has gained over 6% since the start of October. Ellington Financial ( EFC ) was among the laggards this week, however, after it reported that its Book Value Per Share ("BVPS") was estimated to be $15.05 at the end of December - up about 1% during the month, but down about 1% from the end of Q3. We'll hear results from three mREITs next week: AGNC Investment ( AGNC ) and Dynex Capital ( DX ) on Monday, and on Tuesday, we'll see results from PennyMac ( PMT ).

{kind=link}

REIT Capital Raising & REIT Preferreds

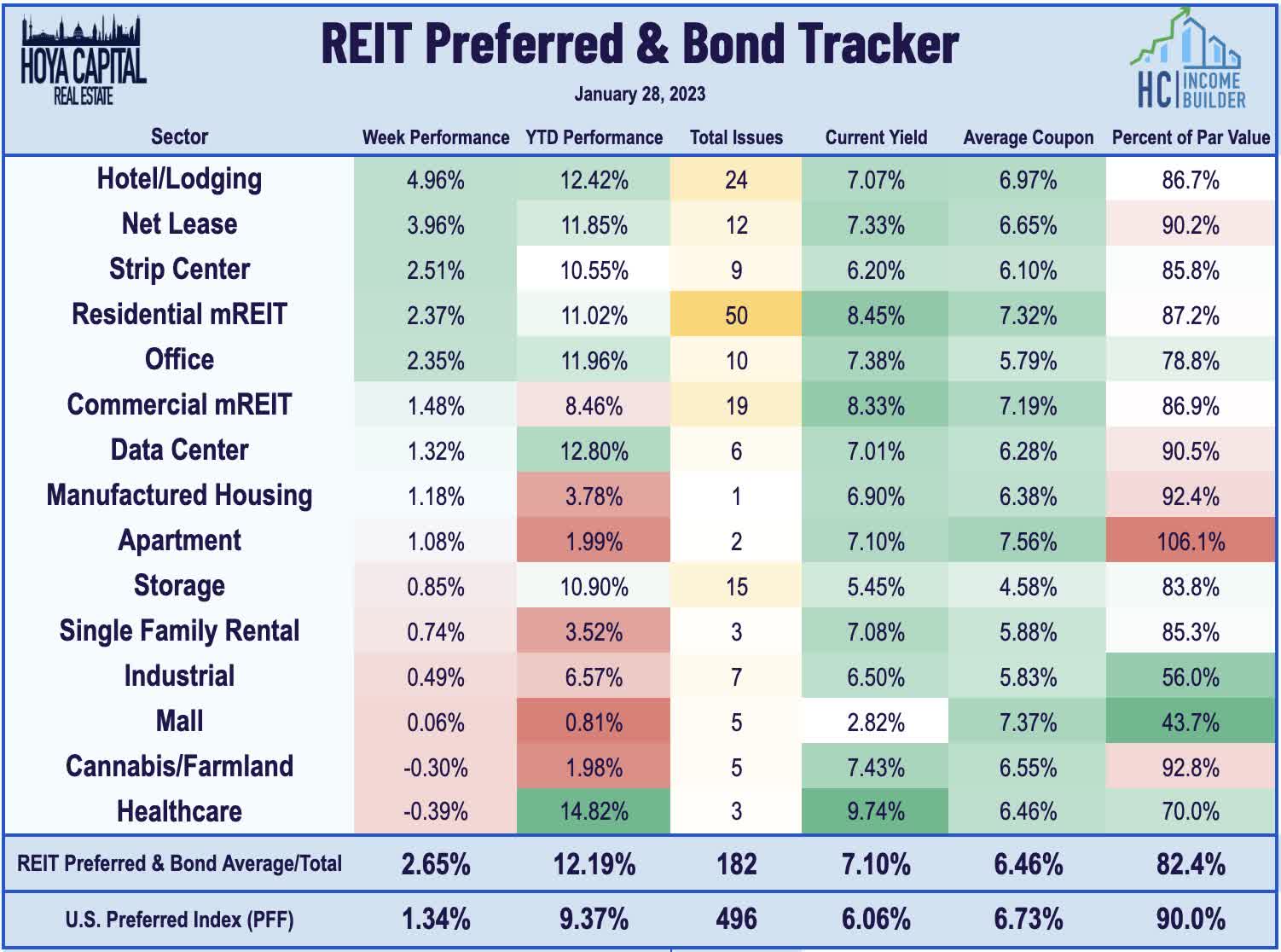

The strong start to the year continued for preferred securities as well with the REIT Preferred Index ( PFFR ) gaining another 2.6% - pushing its four-week gains to over 12% - while the broader iShares Preferred and Income Securities ETF ( PFF ) advanced 1.3% on the week. The trio of preferred issues from Sotherly Hotels ( SOHOO , SOHOB , SOHON ) soared more than 15% on the week after SOHO announced the resumption of its preferred dividends. Apart from micro-cap Wheeler Real Estate ( WHLR ), SOHO was the only REIT with suspended dividends. A handful of REITs have seen their suite of preferred stocks rally more than 15% this year including two of our three 'Best Preferred Picks' - Arbor Realty ( ABR ) and Summit Hotels ( INN ) - along with Rithm Capital ( RITM ), Pebblebrook ( PEB ), and New York Mortgage ( NYMT ).

{kind=link}

2022 Performance Recap & 2023 Check-Up

Through the first four weeks of 2023, the Equity REIT Index is higher by 9.5% on a price return basis for the year while the Mortgage REIT Index is higher by 15.2%. This compares with the 6.1% gain on the S&P 500 and the 7.9% advance on the S&P Mid-Cap 400 . Within the real estate sector, all 18 property sectors are in positive territory on the year led by Hotel, Industrial, and Healthcare REITs. At 3.52%, the 10-Year Treasury Yield has dipped 36 basis points since the start of the year - well below its 2022 highs of 4.30%. The US bond market has rebounded following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 3.0% this year.

{kind=link}

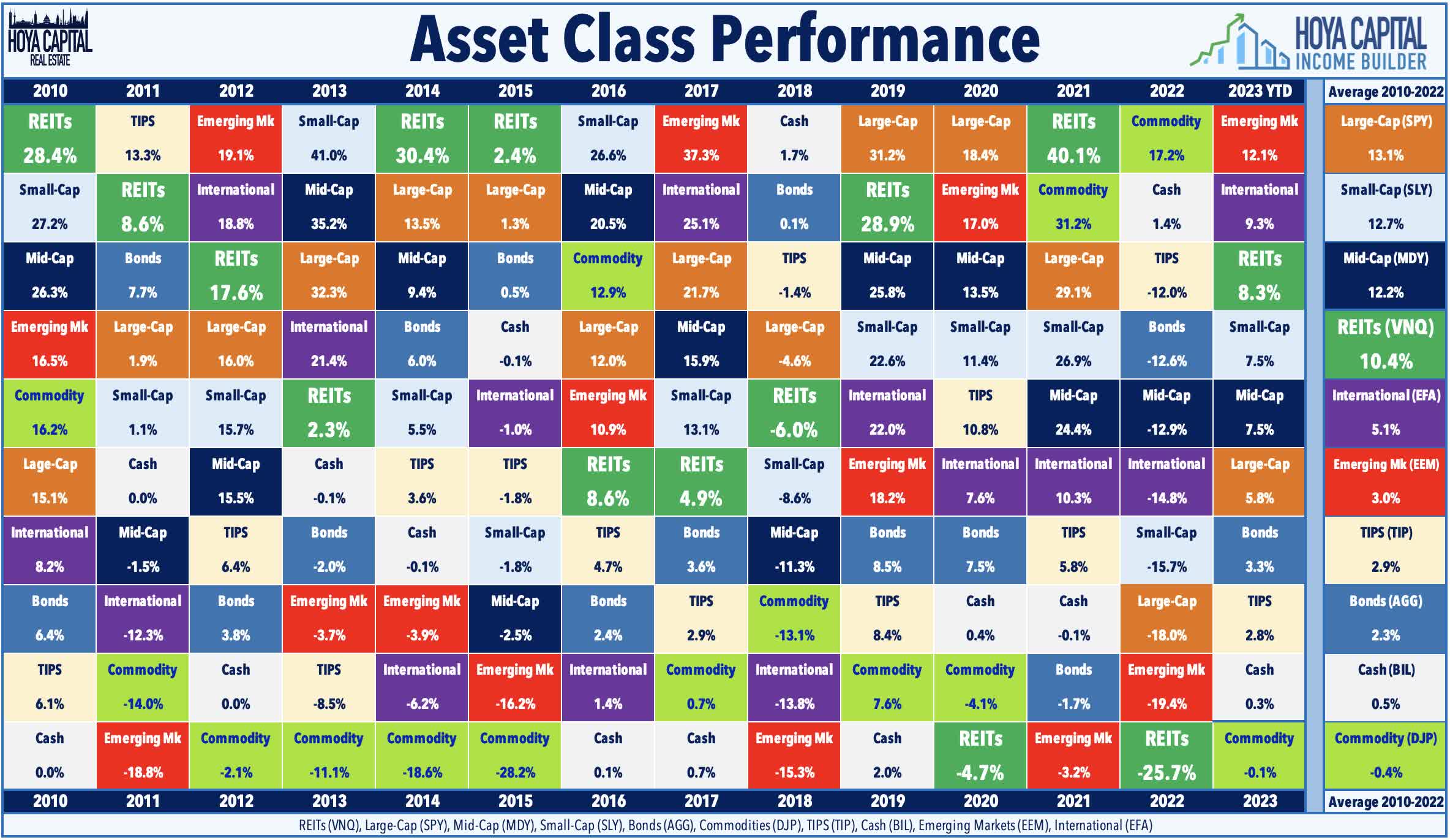

Good riddance, 2022. There were few places to hide across financial markets in a historically brutal year for investors that wiped out nearly a fifth of global financial wealth. The typically-steady US bond market delivered its worst year in history in 2022 with a loss of 13.01% on the Bloomberg US Aggregate Bond Index , which is over 4x larger than the previous worst year back in 1994 (-2.9%). Closing at 3.88%, the 10-Year Treasury Yield surged 237 basis points from the start of the year. Among the ten major asset classes, Commodities ( DJP ) were the only segment to see positive inflation-adjusted returns for the year. After leading the charge in the prior year, REITs finished in the basement of the performance tables among the ten major asset classes on a total return basis with declines of roughly 25%. Performance patterns have flipped this year with Emerging Markets ( EEM ), International ( EFA ) and Real Estate (VNQ) topping the leaderboards thus far in 2023.

{kind=link}

Economic Calendar In The Week Ahead

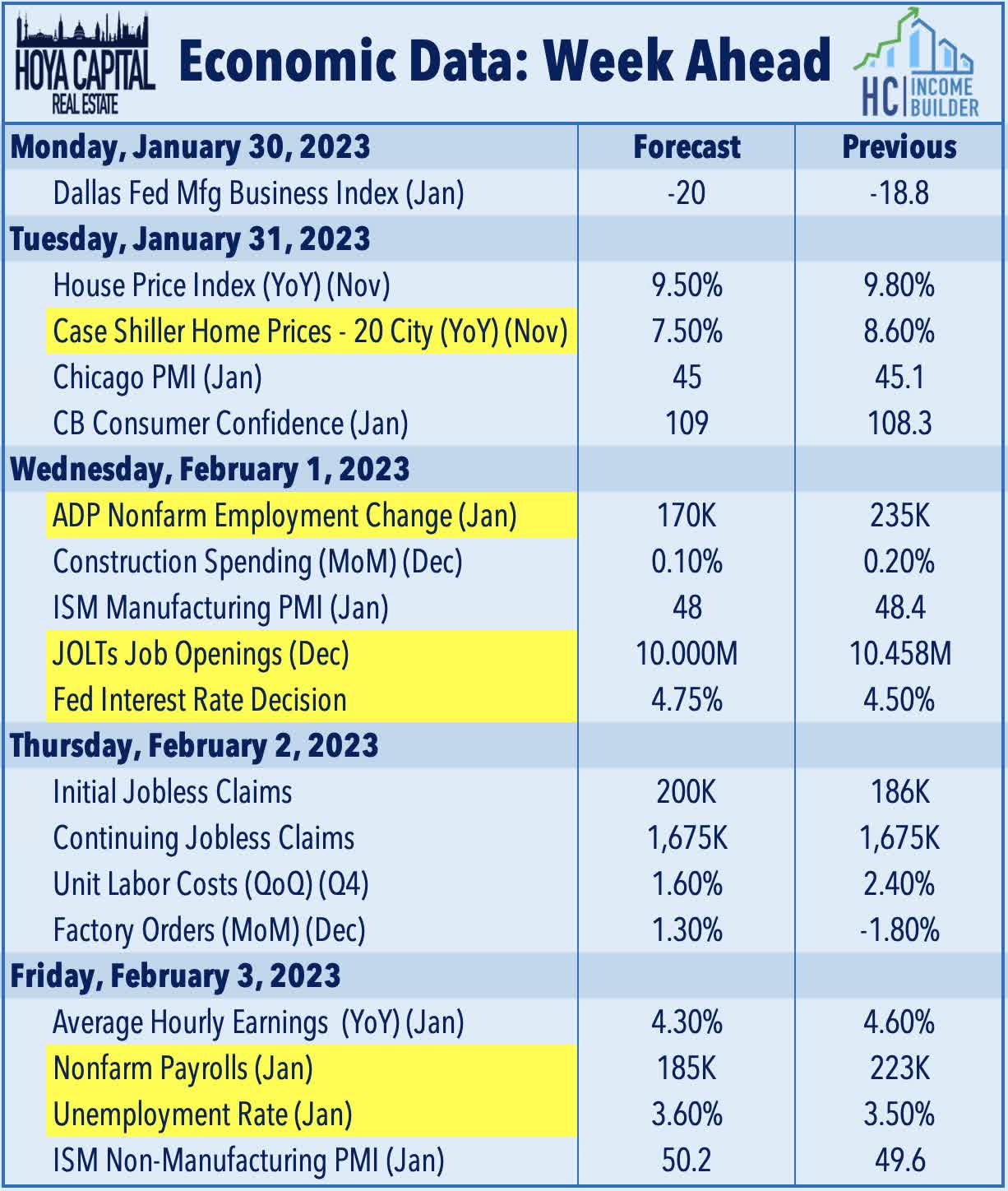

It'll be another jam-packed week of economic data with the main event coming on Wednesday with the FOMC Interest Rate Decision in which the Fed is widely expected to raise rates by 25 basis points to bring the Fed Funds rate to a 4.75% upper-bound. Notably, market pricing indicates expectations of just one additional 25 basis point hike in March - peaking at a 5.0% rate - with rate cuts beginning by the end of this year. Sandwiched around the Fed's decision is a critical slate of employment data headlined by JOLTS data on Wednesday, ADP Payrolls and Jobless Claims data on Thursday and the BLS Nonfarm Payrolls report on Friday. Economists expect job growth of roughly 185k in January and for the unemployment rate to tick higher to 3.6%. Average hourly earnings - a closely-watched metric in recent months - is expected to slow to a 4.3% year-over-year rate from 4.6%. We'll also be watching home price data earlier in the week via the Case Shiller Home Price Index for November which has declined in four-straight months.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

A Softish Landing