ABB - ABB Is One Of Several Robotic Arm Manufacturers Worth Watching

2023-04-28 04:00:59 ET

Summary

- ABB has healthy financials.

- The entire robotics and automated manufacturing industry is expected to experience sustained tailwinds.

- Its Price/Cash Flow of 32.23 indicates the company is presently overvalued.

- The company projects at least 10% revenue growth for 2023.

- ABB is a Hold.

Thesis

With the cost of labor going up and the cost of industrial robotic arms going down, we are slowly approaching the threshold where companies will be financially incentivised to automate. When this happens, I expect a sudden upward inflection in the demand for robotic arms.

ABB Ltd. (ABB) produces high quality industrial robotic arms. A little over half of its business is involved in automated manufacturing. They have healthy financials and are in an industry that is facing sustained tailwinds. I believe they are presently overvalued. ABB is a Hold.

Company Background

ABB Ltd. is a multinational manufacturer currently headquartered in Zurich, Switzerland. They formed as the result of a 1988 merger between Sweden's Allmänna Svenska Elektriska Aktiebolaget, and Switzerland's Brown, Boveri & Cie, creating ASEA Brown Boveri, which was later simplified to ABB. The company has operations in many countries.

ABB Around The World (Wikimedia Commons - Peeperman)

{kind=link}

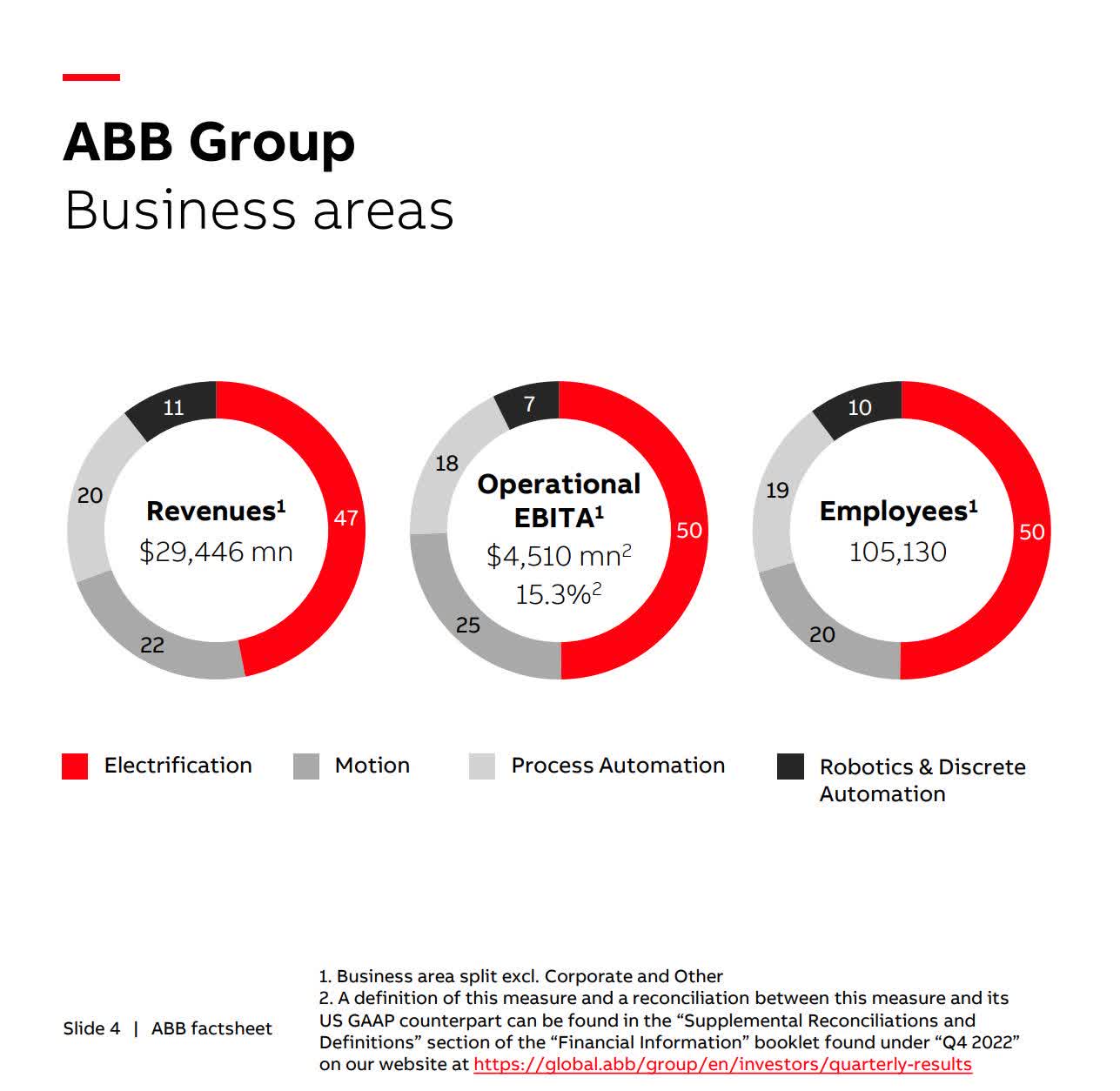

Although I am interested in ABB stock because I am bullish on the long-term prospects of industrial robotics, automation as a whole is only 53% of their business. The Motion and Process Automation portions of their business synergize with their Robotics division. So although only about 11% of their business comes from industrial robotic arms, they also produce other products for automated manufacturing.

ABB Business Areas (ABB Investor And Shareholder Resources - ABB Factsheet)

{kind=link}

Recent forward looking statements made by the company indicate they expect double digit growth for both revenue and operational EBITA in the second quarter of 2023. Their projection for the entire year includes at least 10% revenue growth and improvements to operational EBITA.

Long-Term Trends

The global electrical equipment market size is projected to have a CAGR of 11.1% through 2029. A CAGR of 9.8% through 2029 is projected for industrial automation. The global market for industrial robotic arms is projected to grow at a CAGR of 7.2% until 2030. The global market for collaborative robots is estimated to have a CAGR of 32% through 2030.

Financials

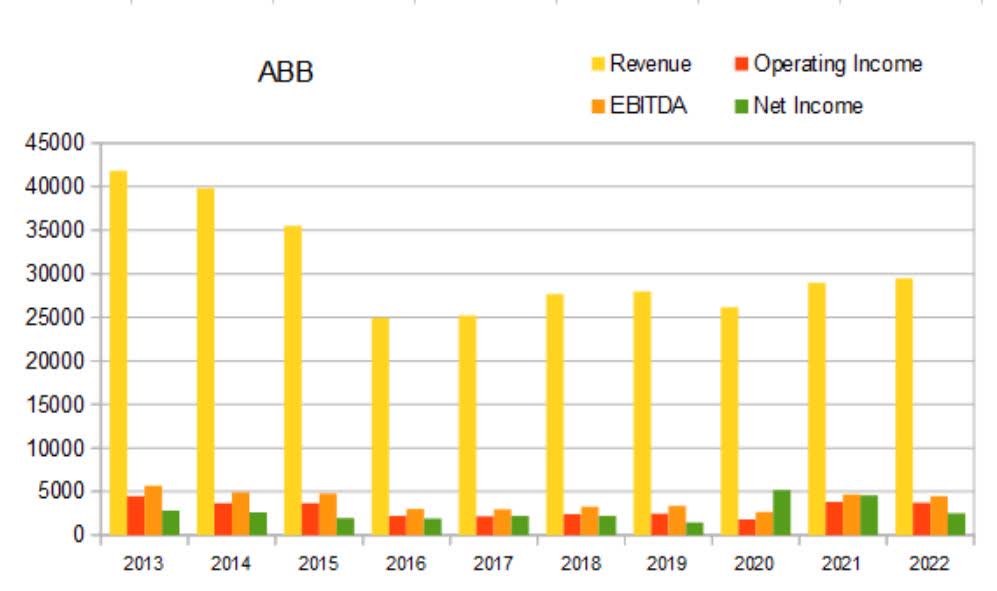

Revenue dropped significantly from 2013 to 2016 but has been slowly increasing since then.

ABB Annual Revenue (By Author)

{kind=link}

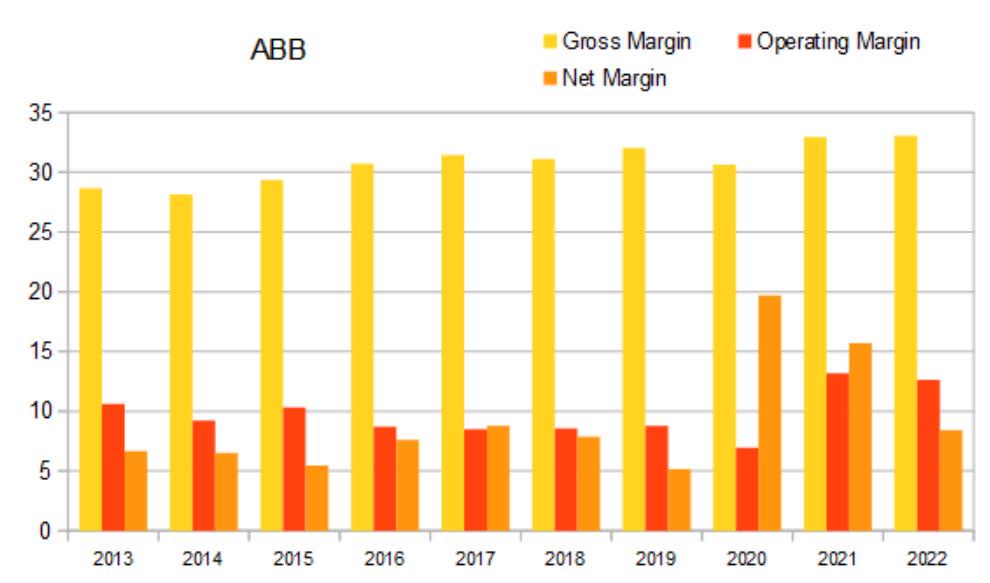

Gross margins have been slowly rising for the last decade. In 2014 it reached a low of 28.15%; in 2022 that had risen to 33.06%. Typically I look for companies that have net margins at or above 10%. Before 2020, ABB consistently had net margins in the 5-10% range.

ABB Annual Margins (By Author)

{kind=link}

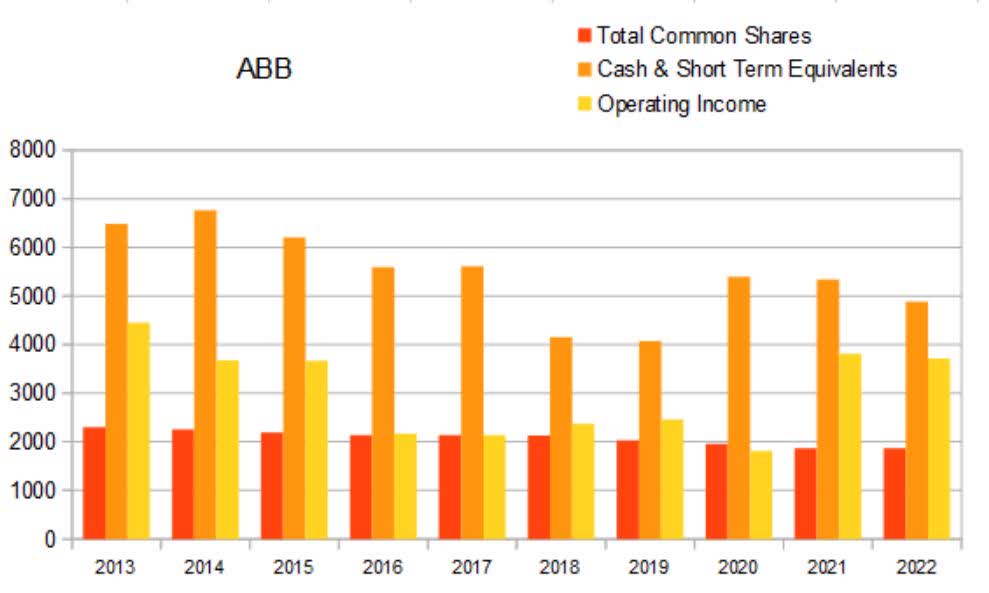

When looking over the relationship between share count, cash, and operating income, it become clear this company has been lowering share count . Total common shares outstanding went from 2.3006B in 2013, to 1.865B in 2022. This represents a 18.93% drop.

ABB Annual Share Count vs Cash vs Operating Income (By Author)

{kind=link}

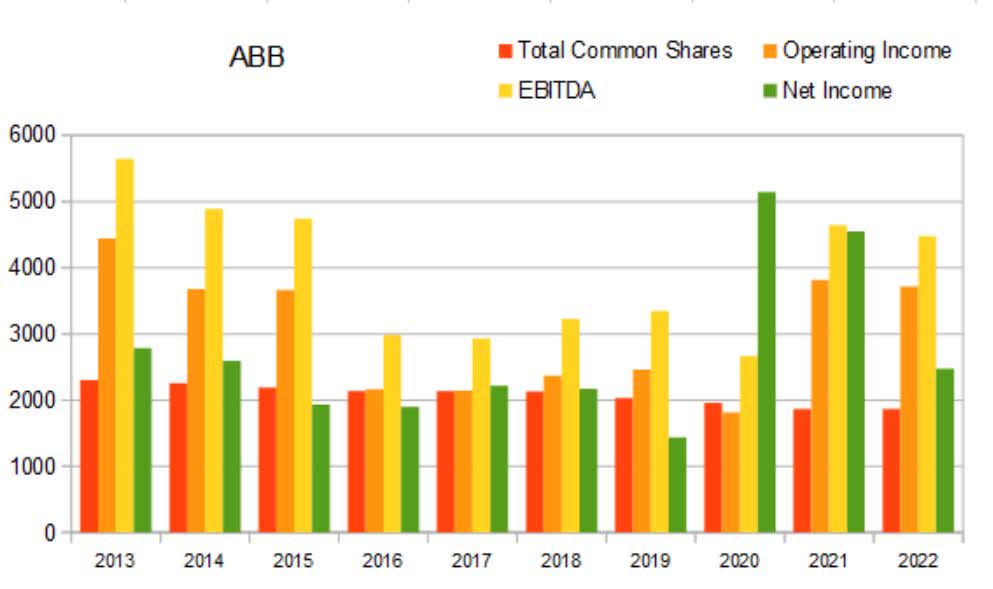

ABB experienced income retractions from 2013 until 2019. The global pandemic and chip shortage seems to have provided a boon in 2020 and 2021. Net income has been declining since 2020.

ABB Annual Share Count vs Incomes (By Author)

{kind=link}

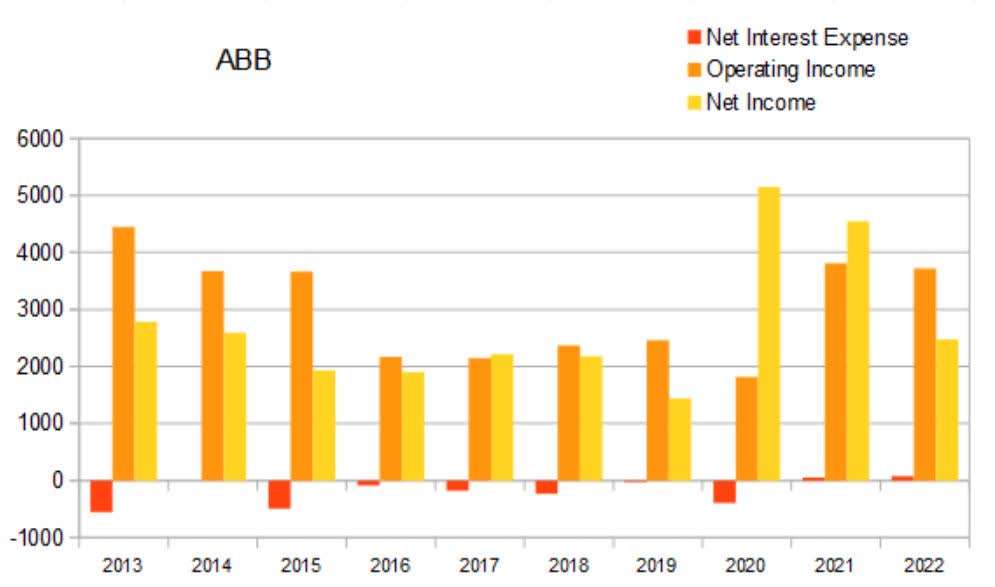

ABB is one of those companies that tries to balance out its short term debt obligations with their income from their own investments. From 2013 through 2020 their interest expenses were significantly larger than their interest incomes. This seems to have shifted, as for both 2021 and 2022 their interest expense is close to zero and they are still collecting roughly the same amount they have historically. Since they are collecting more than they are paying, net interest expenses for both 2021 and 2022 were positive.

ABB Annual Net Interest Expense (By Author)

{kind=link}

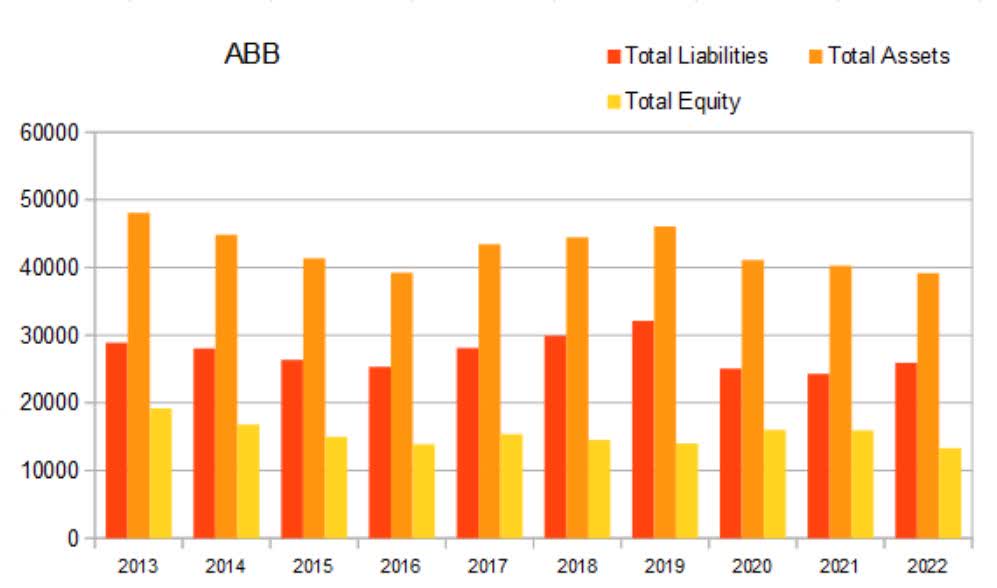

The significant revenue drops that occurred from 2013 through 2016 were also accompanied by drops in total equity. Since 2016, total equity has stayed relatively flat.

ABB Annual Total Equity (By Author)

{kind=link}

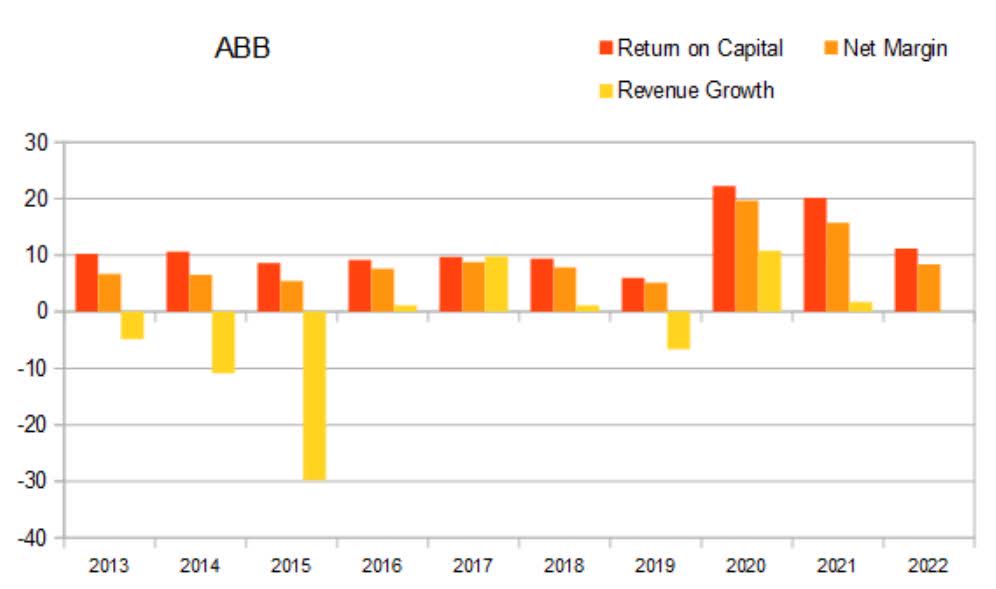

Typically, I want to see already-mature companies keep return on capital at or above 10% a majority of the time. ABB's pre-2020 values were consistently in the 5-10% range. The company experienced a boon from the pandemic and chip shortage, and was able to temporarily experience return on capital values of around 20%.

ABB Annual Return On Capital (By Author)

{kind=link}

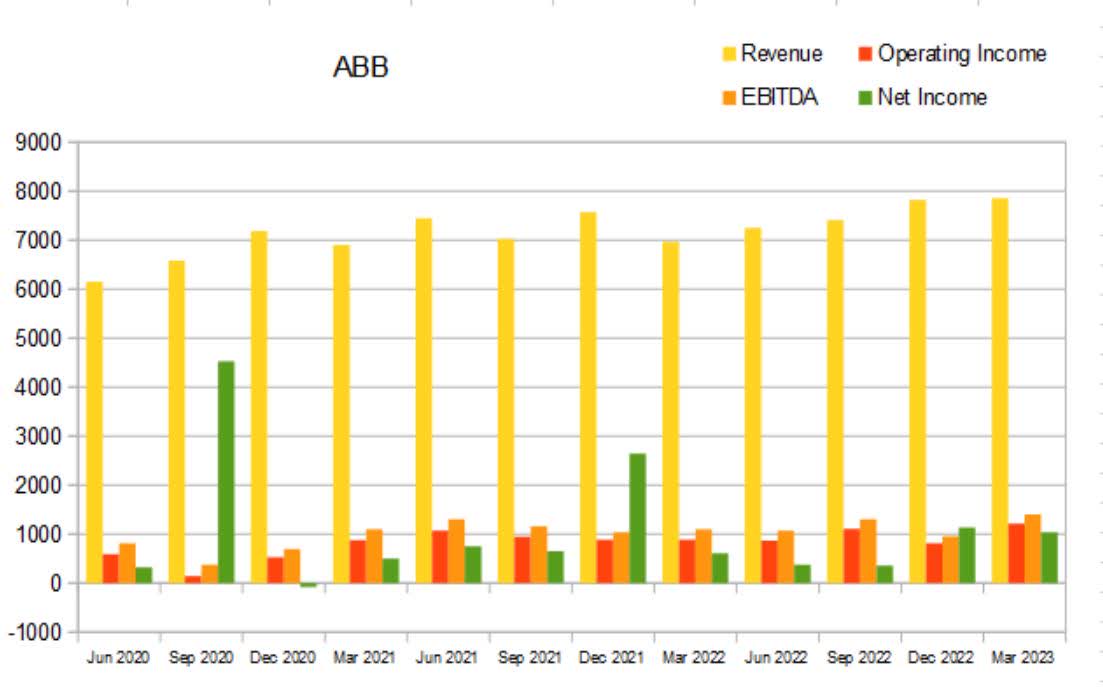

Switching to their quarterly statements now, their revenue has been steadily rising since the low in 2020.

ABB Quarterly Revenue (By Author)

{kind=link}

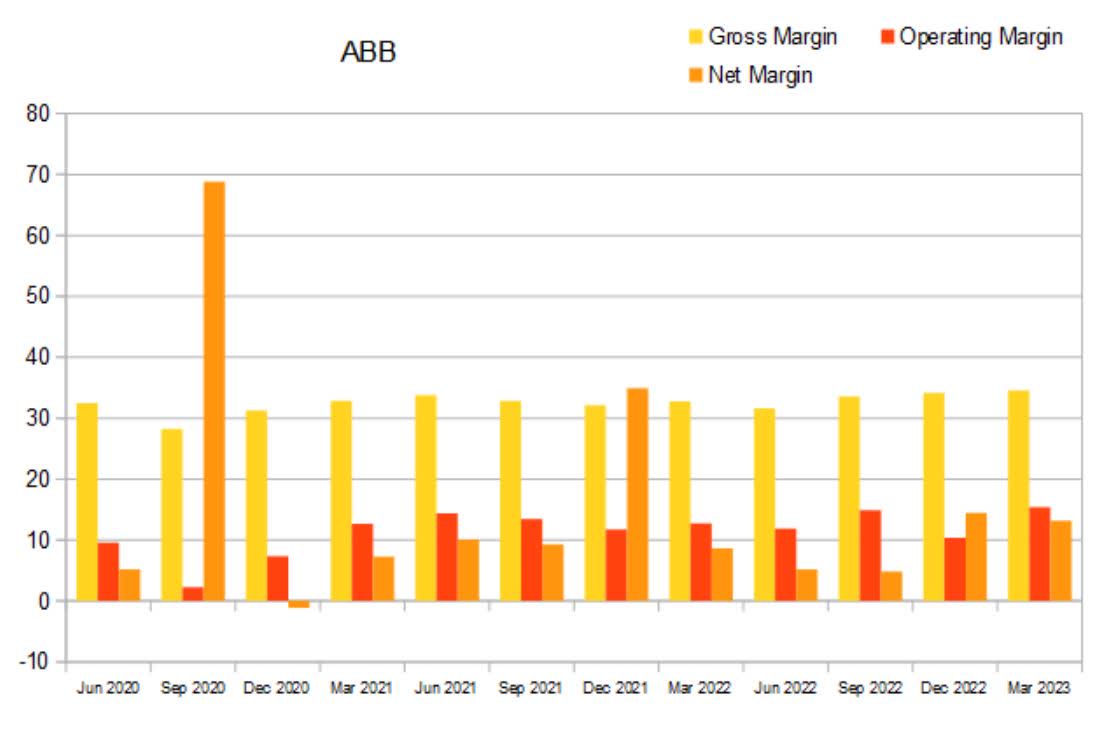

Gross margins are fairly consistently in the low 30s. The company clearly experienced a disruption to its regular activities in 2020 and this shows up as a temporary margin contraction. Operating and net margins both came out very strong on the other side. Net margins experienced another contraction in mid-2022.

ABB Quarterly Margins (By Author)

{kind=link}

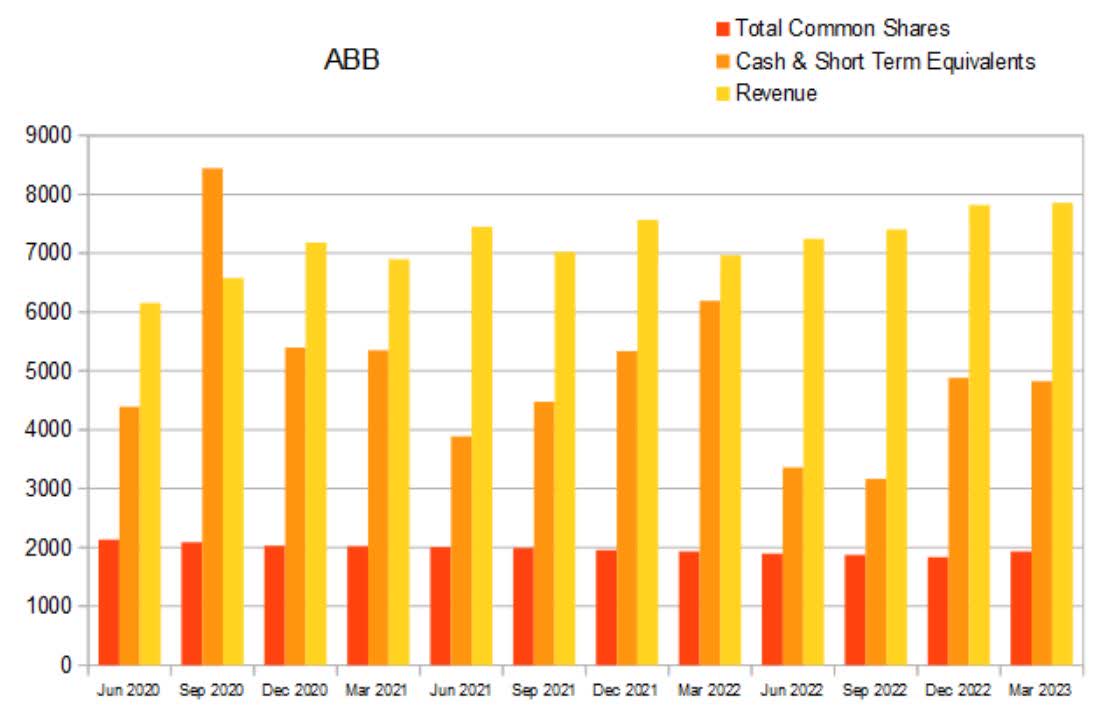

Here we can again see share count falling most quarters while revenue rises. The most recent quarter witnessed a 3.43% rise in total common shares. When a company is able to grow revenue while buying back shares, it's an indication of financial health. This behavior looks attractive to investors.

ABB Quarterly Share Count vs Cash vs Revenue (By Author)

{kind=link}

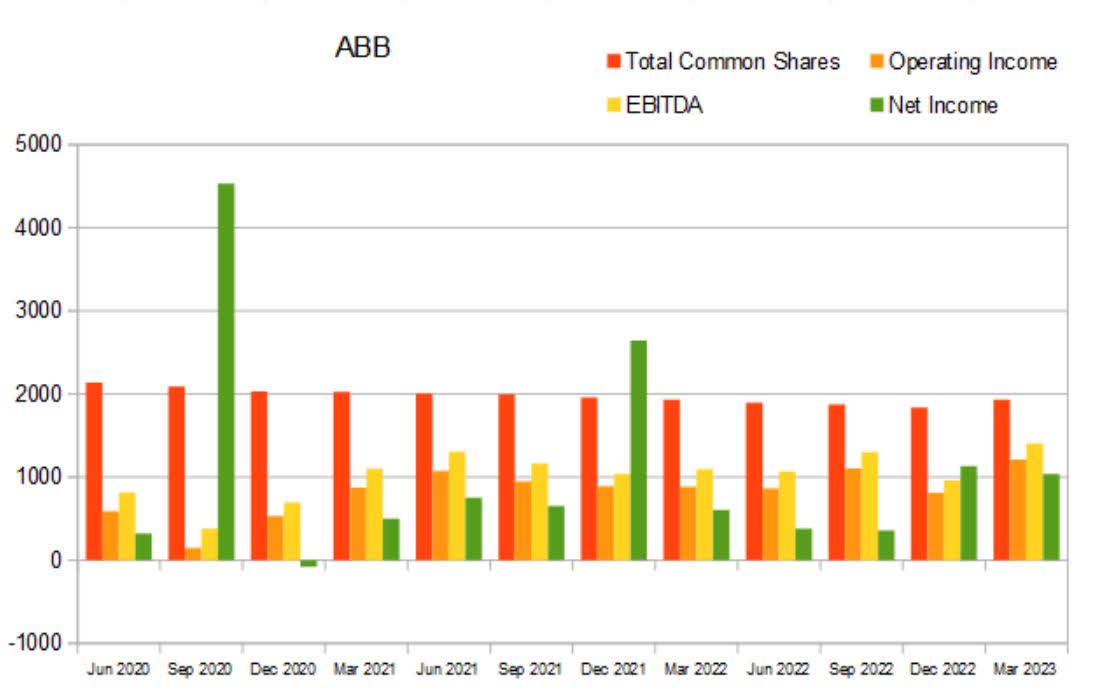

Here we can see that same drop in share count compared to operating income, EBITDA, and net income. I would like to be seeing their cash flow increase because of the revenue rises, but that does not appear to be happening.

ABB Quarterly Share Count vs Incomes (By Author)

{kind=link}

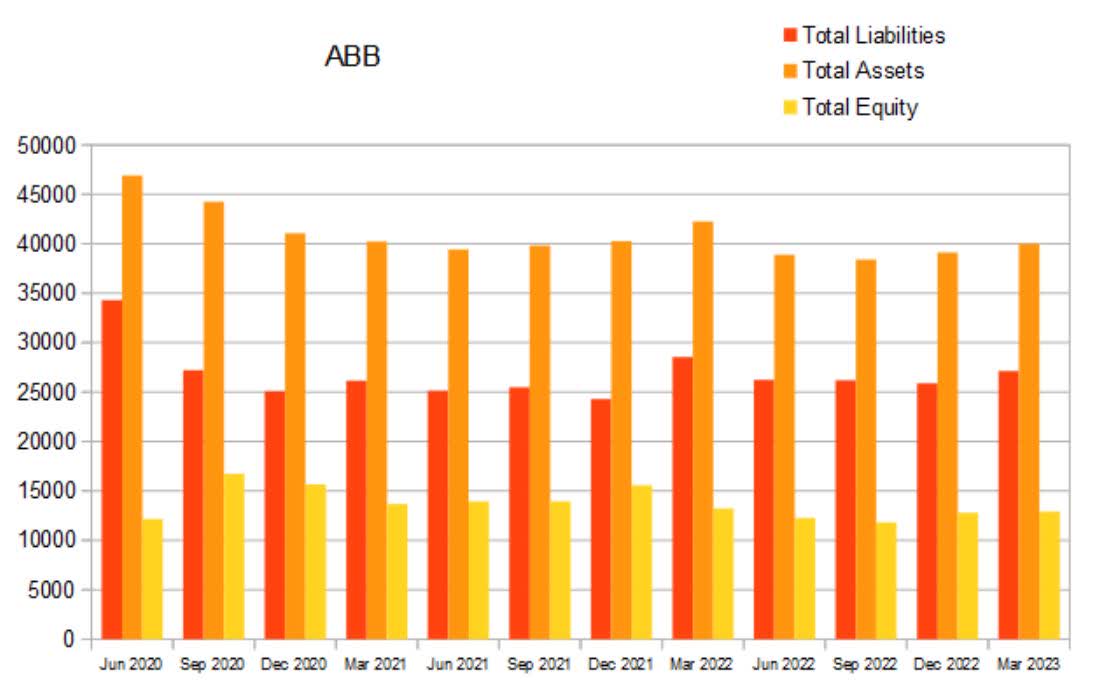

Their equity curve is far from appealing. Temporary pullbacks are fine, but I want to see total equity rising.

ABB Quarterly Total Equity (By Author)

{kind=link}

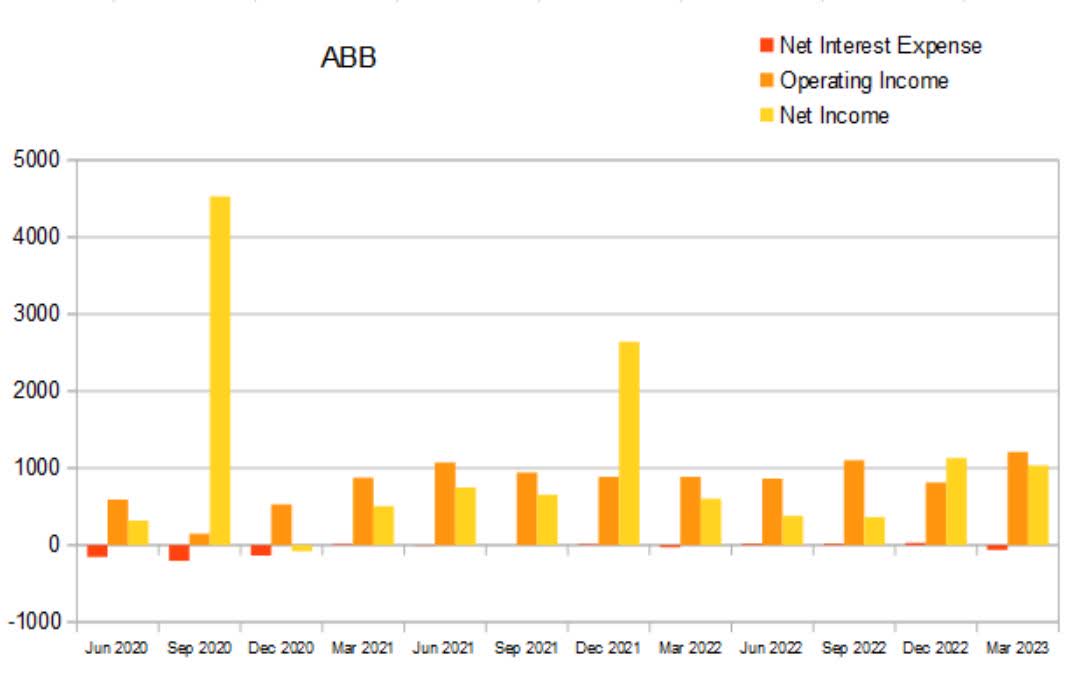

The shift in debt that occurred in 2020 also shows up well in the quarterly interest expenses. Without going back and reading the old 10-Ks and earnings call transcripts, I can only assume they decided to shed their debt when faced with the extreme uncertainty the pandemic brought. It was a wise move and should help the company thrive going forward.

ABB Quarterly Net Interest Expense (By Author)

{kind=link}

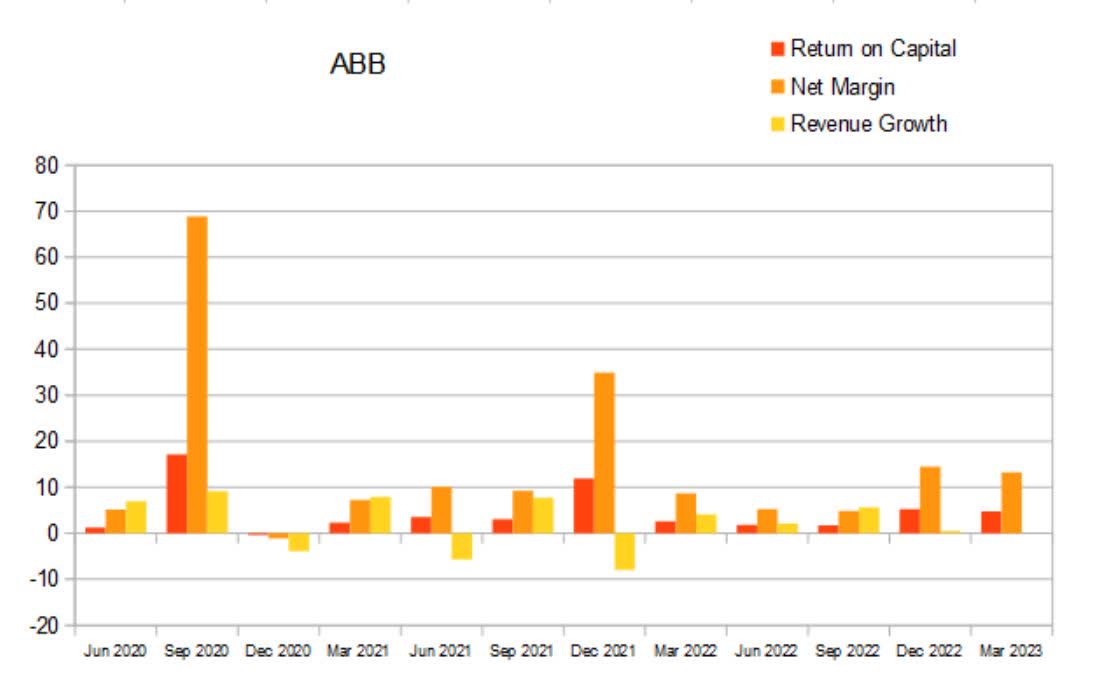

Looking at their return on capital over a quarterly basis makes clear that ABB is subject to swings in efficiency. These are likely the result of changes in demand and other factors not within the control of the company.

ABB Quarterly Return On Capital (By Author)

{kind=link}

Valuation

As of April 27th, 2023, ABB had a market capitalization of 69.04B and traded for $36.44 per share. The company has a forward P/E of 21.80, a trailing Price/Cash Flow of 32.23, and a forward EV/EBITDA of 14.89. Although a P/E of 15 is considered average for a mature company, this company is in an industry that is expected to witness sustained tailwinds. This means a P/E of 21.8 might be fair value. However, from a cash flow perspective they appear to be significantly overvalued.

{kind=link}

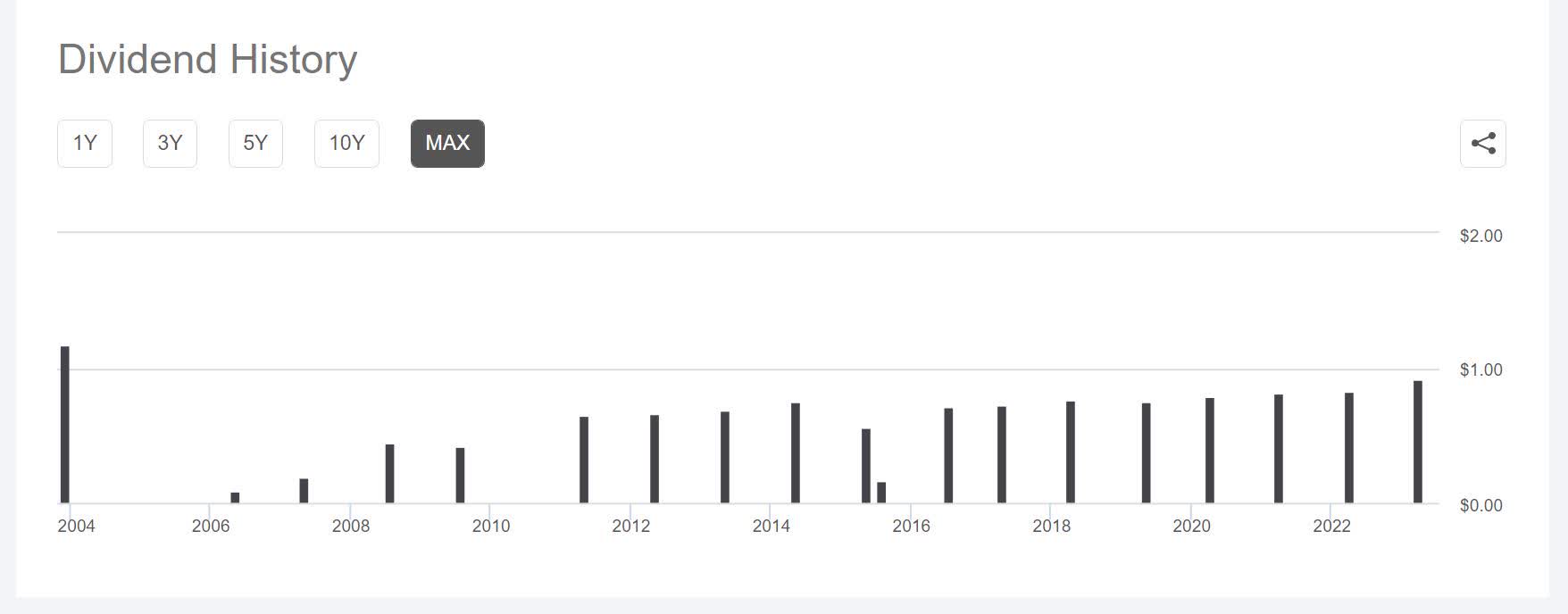

ABB currently offers a 2.58% variable dividend. Their dividend policy prioritizes the long term health of the company over paying a fixed dividend. Assuming no dividend growth and using a discount rate of 9%, a company would have to offer an average annual dividend of $3.19 for 20 years for me to want to pay $35.42 per share. If we instead assume dividend growth is maintained at 5% for the entire 20 years, their present day annual dividend would have to be at or above $1.86 for me to want to buy it for its dividend value alone. With the most recent annual dividend at only $0.92, the company would have to have to shift to a policy of 10.65% annual dividend growth and be able to maintain that pace for 20 years for me to be willing to buy it for today's dividend.

ABB Dividend History (Seeking Alpha)

{kind=link}

Overall, ABB stock appears to be overvalued. They have healthy financials and are expected to experience sustained tailwinds, so this is to be expected.

Risks

Although producing semiconductors is only a small part of their business, the global chip shortage has incentivized most of the worlds chip manufacturers to expand their operations. ABB faces additional competition from Taiwan Semiconductor Mfg. Co. Ltd. ( TSM ), AMD ( AMD ), Intel ( INTC ), Alphabet ( GOOG ) ( GOOGL ), Micron Technology, Inc. ( MU ), Nvidia ( NVDA ) and others.

Catalysts

Eventually, the cost of labor will rise above the cost of automating and manufacturers across the globe will transition. Each industry is presented with their own challenges, so I expect adoption will happen in waves. We have already been experiencing this shift toward automated manufacturing from companies like Whirlpool ( WHR ) and Tesla ( TSLA ); other companies will join them.

Telling workers to learn to code isn't a viable long term solution either as most of the world's programmers are already facing increasing competition. Right now, the buzz is about how everyone from digital artists and voice actors, to mid-level bureaucratic paper pushers are about to be driven out of work by A.I., but this is just the start. Retraining workers into integrators will only delay the inevitable as the eventual marriage of industrial robotics and A.I. will produce A.I. integrators that significantly faster at programming other robots than you or I could ever be.

Conclusions

This is a large mature company and robotics is only a part of their overall business. Although far from a pure play, this diversity means the company will have additional cash flow to draw on if increases in demand incentivize them to scale up their industrial arm production. Although we are likely years away from the inflection point, eventually a wave of demand will hit industrial robotic arm producers as manufacturers adopt automation. ABB is very likely going to be one of the long-term winners in the industry but I doubt it will be the only one.

ABB is only one of several robotic arm manufacturers I am looking at. I have also recently written articles on FANUC ( FANUY ) and Teradyne ( TER ), and am planning on also taking a look at KUKA ( KUKAF ), Yaskawa ( YASKY ), and Kawasaki ( KWHIY ). Because all these separate producers are competing for the same customers, my goal is to identify the most competitive players well ahead of the inflection point.

For further details see:

ABB Is One Of Several Robotic Arm Manufacturers Worth Watching