AAVMY - ABN AMRO: Further Upside Amid Dutch Economy Outperformance

Summary

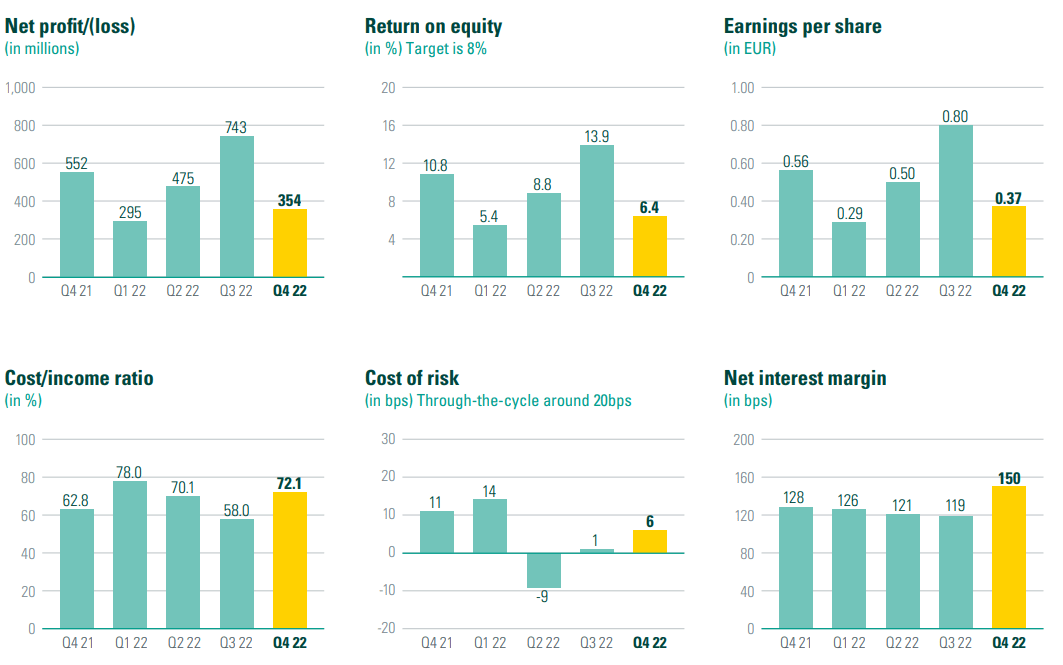

- ABN AMRO Bank N.V. has ROE of 6.4% in Q4, down from 8.7% in 2022. Very low cost of risk at just 3 bps for the full year.

- Q4 strength in Personal & Business Banking and Wealth Management.

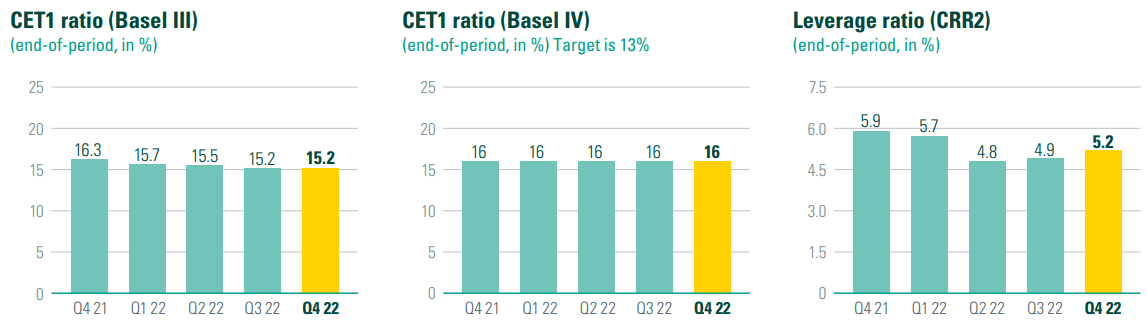

- CET1 of 15.2% some 5.5% above the current 9.7% MDA threshold. Countercyclical buffers to increase MDA requirement by 1.5% into 2024.

- 2023 underlying costs seen at EUR5.3 billion, flat vs 2022. Target of EUR4.7 billion for 2024 harder to achieve.

- Dutch economy should return to growth in H2 2023. Even with a normalizing cost of risk, ROE should be at least 7.5%, absent a larger recession.

Company Overview

ABN AMRO Bank N.V. ( AAVMY ) reports results in four main segments, namely Personal & Business Banking at 50.9% of Q4 2022 operating income ((OI)), Wealth Management at 20.5% of Q4 2022 OI, Corporate Banking at 43.9% of Q4 2022 OI, and Group Functions at negative 15.3% of Q4 2022 OI.

Operational Overview

Personal & Business Banking delivered 34% Y/Y OI growth in Q4, an acceleration to the 12% increase in 2022. Q4 Growth was driven by a 32% Y/Y increase in net interest income ((NII)) which accounted for 80.8% of total Q4 operating income.

Wealth Management saw 15% Y/Y OI growth in Q4, with a 48% rise in NII offsetting a 12% drop in net fee and commission income. Q4 OI growth was in line with 2022 growth of 15%.

Corporate Banking achieved a 7% Y/Y increase in Q4 OI, down from the 20% growth rate for 2022. The deceleration was due to lower other operating income in the quarter (down 30% Y/Y).

Group Functions delivered a EUR285 million loss in the quarter, bringing the 2022 loss to EUR216 million. NII dropped 93% Y/Y in Q4, with mortgage prepayments down significantly.

On a group level , despite a slight deceleration into Q4, 2022 was a great year for ABN AMRO:

{kind=link}

ROE was 6.4% in Q4, down from 8.7% in 2022. The cost/income ratio of 72.1% also deteriorated versus the full year at 69.2%. Cost of risk increased only marginally in Q4, at just 6 bps, versus 3 bps for the full year. Tangible book value per share rose by 0.09 EUR/share Q/Q to about 23.07 EUR/share in Q4. The dividend for 2022 is up 62% Y/Y to 0.99 EUR/share (0.67 EUR/share final payment) and a new EUR500 million buyback program replaces the old EUR250 million authorization. The buyback will run until June 2023.

Capital Position

The bank remains very well capitalized, with a CET1 ratio of 15.2%, some 5.5% above the 9.7% maximum distributable amount ((MDA)) requirement:

{kind=link}

The 15.2% CET1 already incorporates a provision for the upcoming buyback. The bank estimates the CET1 ratio will improve to 16% with the 2025 introduction of Basel IV.

As disclosed in the Q4 report, the MDA should rise to about 11.2% in 2024:

The Dutch central bank ((DNB)) will increase the Countercyclical Capital Buffer (CCyB) for Dutch exposures to 1% by 25 May 2023. Full implementation of the 2% CCyB rate is expected by Q2 2024. This will cause the MDA trigger level to increase by around 1.5%. This is already reflected in our 13% CET1 target under Basel IV.

Outlook 2023

Full-year underlying costs are expected around EUR5.3 billion, same as 2022, as inflation and higher investments delay the impact of savings programs. 2024 target at EUR4.7 billion, although the abovementioned challenges remain, as discussed on the conference call :

So then turning to our 2024 cost target. As we stated before, a significant proportion of cost reductions are back-ended loaded, for example, the reduction in regulatory levies of around €200 million. We have some plan to bring our investment spend down by €100 million in 2024. We're working hard to reduce costs further. However, given the cost drivers I mentioned for '23, achieving our '24 target will be challenging.

Cost of risk target remains at about 20 bps through the cycle.

Fee income should see growth of 5-7% compounded going into 2024.

Net interest income should further improve, although no precise guidance was announced.

CFO Lars Kramer is leaving the bank on April 30th.

Long-term Capital Return Potential

ABN AMRO currently sits on EUR19.5 billion of CET1 capital. Roughly speaking, each 1% of CET1 capital represents EUR1.28 billion. The buffer relative to the bank's 13% CET1 target is 2-3%, with Basel III buffer of 2.2% and Basel IV buffer of around 3%.

While exact developments will largely depend on operating performance and economic indicators, it can be argued that the bank can "create" some EUR1.2 billion of value via buybacks based on its Basel III capital buffer, or EUR1.55 billion based on its Basel IV buffer. The calculations are based on the current tangible book discount of around 29%.

As things stand, the threshold for buybacks remains 15% CET1 (based on Basel IV as discussed on the conference call) and the bank has some leeway to deploy additional capital.

Conclusion

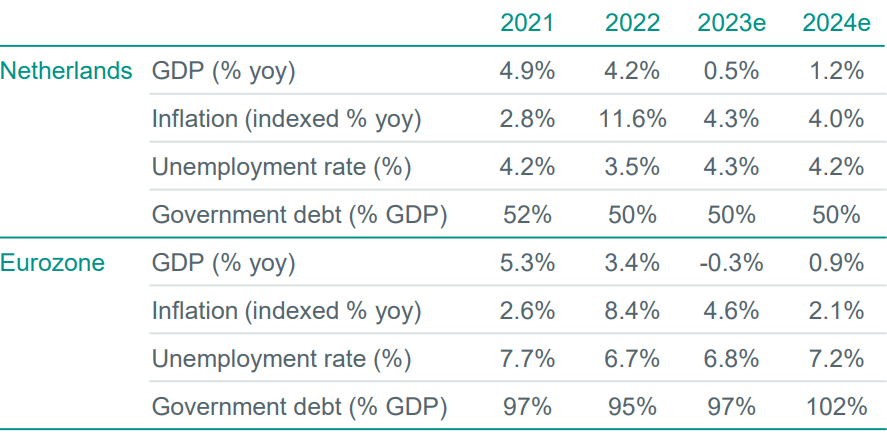

The Dutch economy is expected to outperform the Eurozone average in 2023, with a shallow H1 contraction followed by growth in H2:

{kind=link}

If events play out as expected, ABN AMRO should be able to deliver an ROE of at least 7.5% in 2023 (based on a normalizing cost of risk), with room for further improvement in 2024 to its 10% target. This should allow the bank to deploy some excess capital in H2 and further bridge the valuation gap with ING Groep N.V. ( ING ).

Despite strong year-to-date performance and appealing valuations of banks with a weaker capital position, I think ABN AMRO shares should see further upside. As always, caution is advised as the economy will likely deteriorate before it gets better. Furthermore, a domestic-focused bank such as ABN AMRO will get little valuation reprieve from a ceasefire in Ukraine, which will hopefully materialize later this year. On the flip side, the shares should not suffer as much in case of escalation.

ABN AMRO Bank N.V. remains a self-help story, and the tangible book discount is sufficient to make the buybacks accretive. Hence, I think sticking with ABN AMRO Bank N.V. stock is worthwhile.

Thank you for reading.

For further details see:

ABN AMRO: Further Upside Amid Dutch Economy Outperformance