AAVMY - ABN AMRO: Plateau In Residential Mortgage Growth Concerning (Rating Downgrade)

2023-10-24 18:13:30 ET

Summary

- ABN AMRO's stock has declined to $13.49 in part due to a plateau in residential mortgage growth.

- Operating income and net interest income have increased, but residential mortgages have declined, leading to a decrease in market share.

- The decline in housing transactions and prices in the Netherlands suggests a weak housing market, impacting ABN AMRO's growth potential.

Investment Thesis: I revise my view on ABN AMRO from buy to hold based on a plateau in residential mortgage growth.

In a previous article back in April, I made the argument that ABN AMRO Bank N.V. ( AAVMY ) could continue to see upside going forward, based on continued growth in net interest income and return on equity.

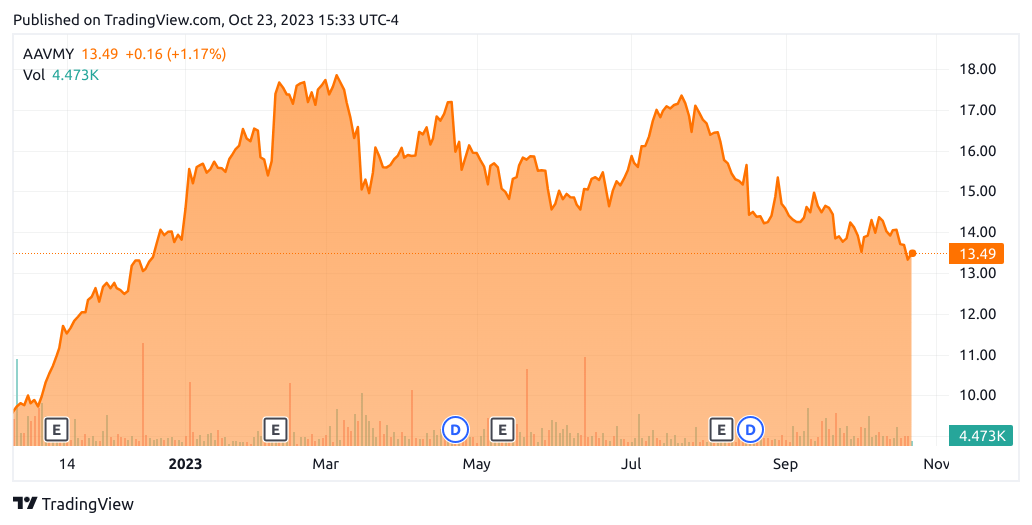

Since then, the stock has descended to a price of $13.49 at the time of writing:

{kind=link}

The purpose of this article is to assess whether ABN AMRO has the ability to see continued growth from here taking recent performance into consideration.

Performance

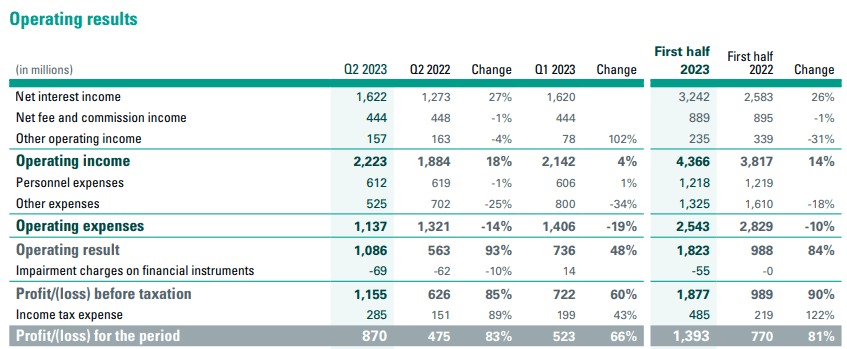

When looking at the most recent Q2 2023 earnings results for ABN AMRO for the period ending 30 June 2023 (and released on 9 August 2023), we can see that operating income is up by 18% YoY while net interest income was up substantially by 27% YoY.

ABN AMRO: Interim Report & Quarterly Report - Second quarter 2023

{kind=link}

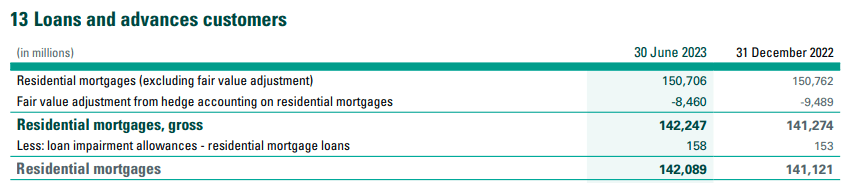

When looking at residential mortgages (excluding the fair value adjustment), we can see a slight decline for the month ended June 2023 as compared to the month ended June 2022:

ABN AMRO: Interim Report & Quarterly Report - Second quarter 2023

{kind=link}

Moreover, margin pressure saw net interest income on residential mortgages decline, in spite of growth in average volumes.

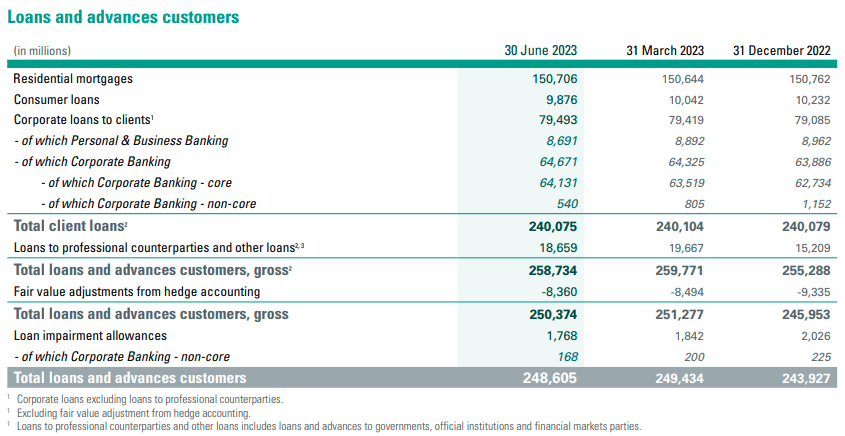

Market share of residential mortgages had also declined to 14% in Q2 2023 as compared to 17% in Q2 2022, as a result of increased competition. The reason I make particular reference to residential mortgages is that this segment accounts for the majority of total loans and advances for ABN AMRO in terms of gross carrying amount - over 60% of the total as of 30 June 2023:

ABN AMRO: Interim Report & Quarterly Report - Second quarter 2023

{kind=link}

When looking at residential mortgages by quarter - we have seen that the first two quarters of 2023 have shown significant growth on that of the previous year.

Figures sourced from ABN AMRO historical quarterly reports (Q1 2020 to Q2 2023). Plot generated by author using Python's seaborn visualisation library.

With that being said, we have also seen growth plateau since that of the last quarter of 2022.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, a plateau in growth across residential mortgages seems to be a significant contributing factor to the decline in stock price that we have been seeing lately.

Investors appear to be growing apprehensive that a slowdown in residential mortgage growth has the capacity to lead to a slowdown in overall loan growth.

When looking at the housing situation in the Netherlands more generally, housing transactions for the month of September came in at 16,089 - which was 8.7% lower than that for the same month in the previous year.

{kind=link}

Moreover, house prices were also 3.5% lower in September than that of September 2022. Given that housing transactions have been falling in tandem with price - this reflects a degree of weakness across the Dutch housing market. As a result, the plateau that we are seeing in residential mortgages growth for ABN AMRO is not particularly surprising - and I take the view that the stock may continue to see downward pressure until such time that we see a significant recovery in housing demand across the Netherlands.

I had previously stated that I took a bullish view on ABN AMRO in spite of a high price to book ratio - as net interest income had continued to rise and we also saw an impressive return on equity growth.

We have seen the price to book ratio come down from levels seen near the beginning of the year, and return on equity continues to reach new 5-year highs.

Price to Book

YCharts.com

Return on Equity

YCharts.com

In this regard, I take the view that ABN AMRO could potentially have the capacity to see a rebound in upside to prior levels of $16-18. However, I take the view that ABN AMRO would need to demonstrate significant growth in residential mortgages over the next couple of quarters if this is to be the case.

Conclusion

To conclude, ABN AMRO has seen a plateau in residential mortgage growth over the last two quarters - which has been influenced by weakness in the Dutch housing market. I take the view that until we see a recovery in residential mortgage demand - growth for the stock more generally could remain weak. As a result, I revise my view on ABN AMRO from buy to hold.

For further details see:

ABN AMRO: Plateau In Residential Mortgage Growth Concerning (Rating Downgrade)