AAVMY - ABN AMRO: Recent Underperformance Enhances The Value Case

2024-01-03 00:53:48 ET

Summary

- ABN AMRO stock has underperformed since my last article in the summer, with the bank disappointing on lower than expected net interest income despite reporting healthy bottom line beats.

- Open questions on expenses and capital returns might not be helping matters either, though more detail should be coming with Q4 results next month.

- These shares have de-rated to just 0.55x tangible book value since prior coverage, putting them at a significant discount to historical levels despite a nice uptick in profitability.

Dutch bank ABN AMRO ( AAVMY )( ABMRF ) has proved a frustrating investment since my last update around six months ago. The ADSs have delivered a roughly flat total return in that time, significantly underperforming larger national peer ING (NYSE: ING ) as well as the broader European financials space, represented here by the iShares MSCI European Financials ETF ( EUFN ):

{kind=link}

Performance is even softer versus U.S. banks, with the latter recovering a heap of lost ground recently on the prospect of Fed rate cuts later this year. Indeed, ABN AMRO's USD-denominated ADSs have underperformed versus the SPDR S&P Bank ETF ( KBE ) by a huge 30ppt in that time. The shares have, however, returned around 30% since I initiated coverage just under two years ago, making for a decent medium-term investment overall.

{kind=link}

Recent underperformance aside, my thesis on the bank hasn't materially changed. The fact remains that ABN AMRO is exceptionally cheap versus historical levels despite currently operating in a more profitable macro environment. While I do think the recent bout of underperformance is somewhat self-inflicted, the value case remains compelling ahead of Q4 results, at which point the bank will provide much welcome clarity on key items like operating expenses and capital returns.

Provision-Fueled Beats Aren't Cutting It

On one level, ABN AMRO's lackluster performance might look a bit odd in light of its financial performance. The bank earned circa €2.40 per share (~$2.63 per 'AAVMY' ADS) in net income over the first nine months of last year, with EPS beating consensus estimates in all three quarters by a heavy margin.

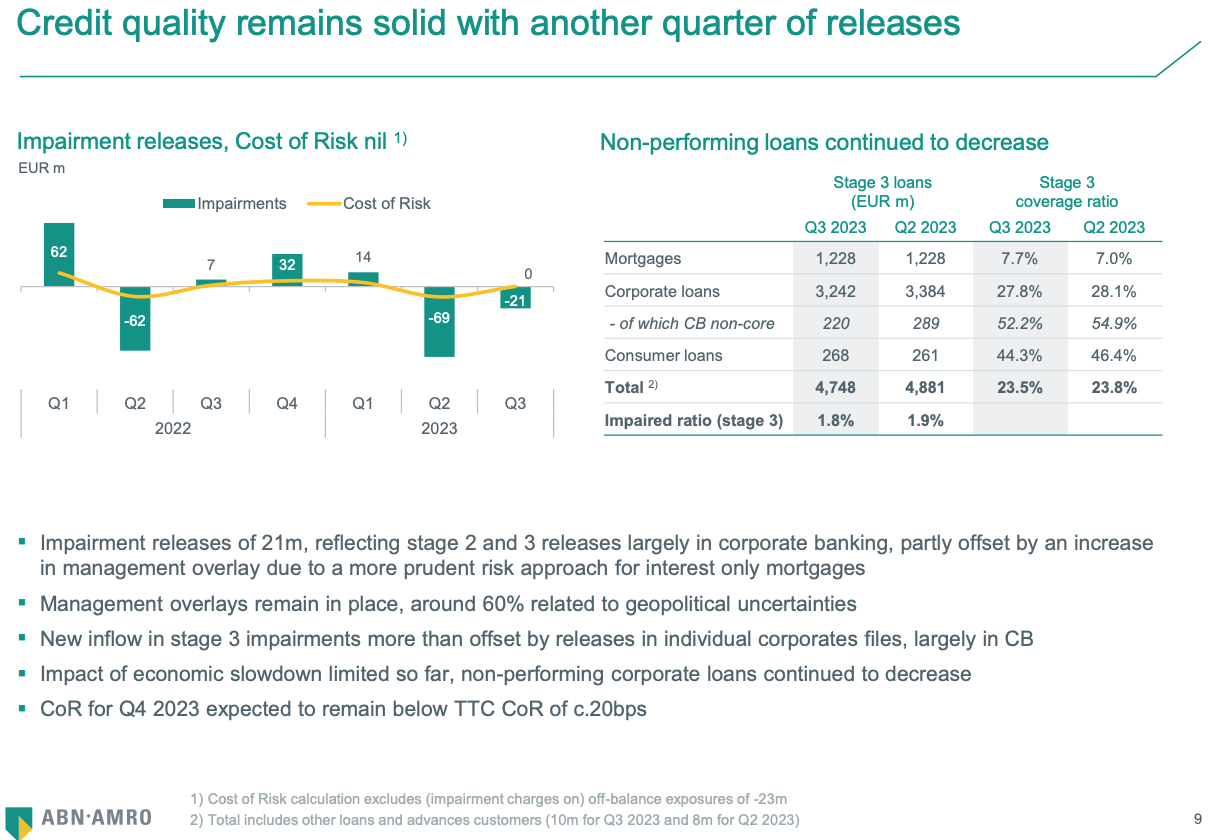

The reality, though, is that earnings beats are not all equal, with the market clearly in little mood to credit those fueled by lower bad debt expenses, as is the case here. Credit quality remains one of the standout features of ABN AMRO's recent results, with the bank reporting a cost of risk ("COR") of essentially 0bps in Q3 on the back of modest releases from reserves. Stage 3 loans were also down 10bps sequentially as a proportion of total loans (to 1.8%), with the Stage 2 ratio also down 40bps sequentially to 9.1%.

ABN AMRO Q3 2023 Results Release

{kind=link}

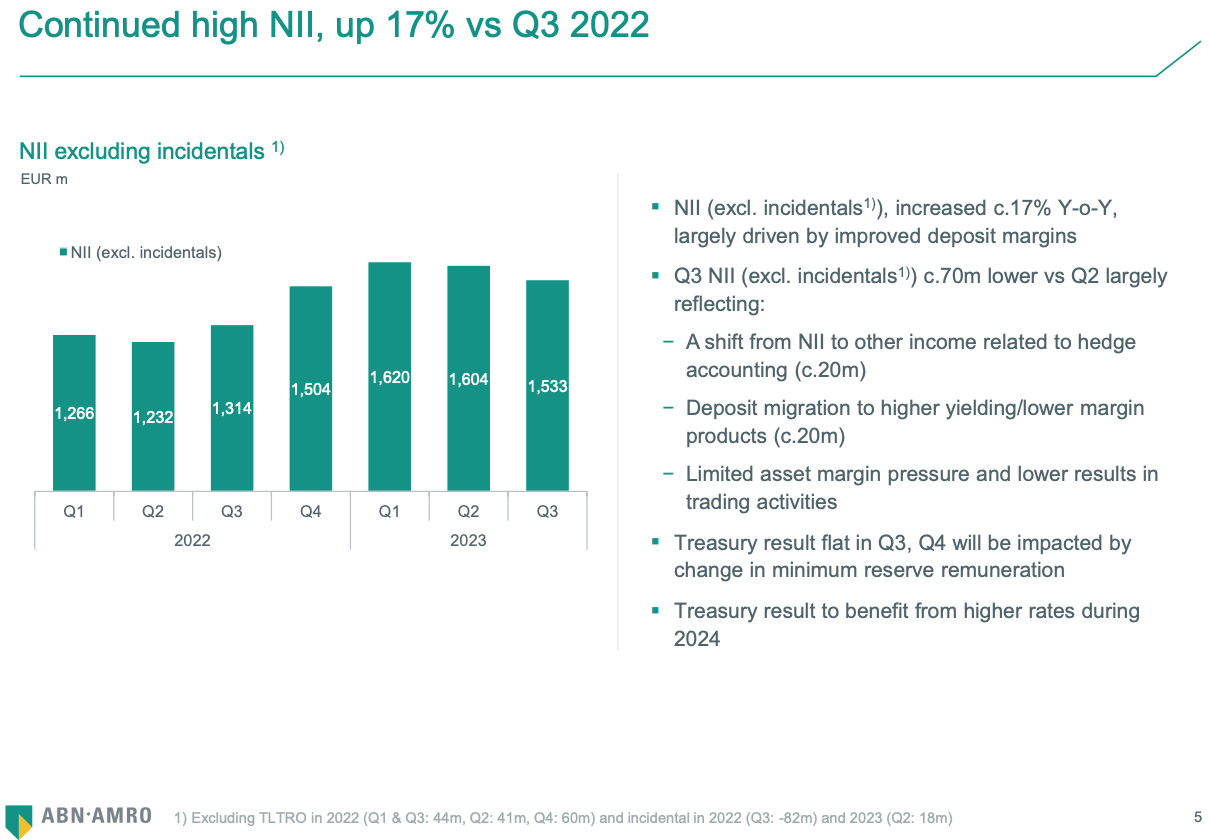

On the flip side, pre-provision income drivers like net interest income ("NII") have largely disappointed. Indeed, Q3 NII of €1.533 billion landed a little over 6% below the consensus estimate of €1.633 billion. Like many banks, ABN AMRO has seen upward pressure on deposit costs on a combination of interest rate hikes and mix effects. Current account balances had fallen by around €24 billion, or circa 20%, over the first nine months of 2023, with more expensive Time deposits up around €17 billion, or 100%, over the same period.

The bank is also experiencing ongoing margin pressure from the fiercely competitive Dutch mortgage market, with residential mortgages making up around 63% of its €240 billion loan book. As higher margin loans mature from the back book, they are replaced with lower margin mortgages on the front book, putting downward pressure on lending margins. At the same time, loan growth remains anaemic, with total client loans up just €340 million, or 0.1%, through Q3.

Source: ABN AMRO Q3 Results Presentation

{kind=link}

More positively, management expects deposit migration to slow next year, while the €170 billion replicating portfolio should provide support to NII. In simple terms, the replicating portfolio can basically be thought of as acting like a portfolio of fixed-income securities. With rates now higher in the Eurozone after years of being at zero/negative levels, the spread the bank can earn on its sticky deposit base has become much more valuable:

Now looking ahead to next year, I expect the Treasury result to increase during 2024. Our replicating portfolio continues to benefit NII, given current market rates, and we expect the current pace of deposit migration to come down during next year, as we expect most of the migration to occur this year.

Although we cannot predict how our margins will develop, our current view is that NII may recover a good part of this quarter’s decline during 2024.

Robert Swaak, CEO ABN AMRO, Q3 Earnings Call

Some Self-Inflicted Hits Not Helping

I did mention that self-inflicted hits have likely not helped matters here. One of those is arguably regarding expenses. Last time out, when the most up to date numbers covered Q1 2023, management was guiding for €5.3 billion in FY2023 operating expenses, with its longer-term cost reduction target of €4.7 billion by FY2024 still in place. The former has since been lowered by €100-200 million due to delayed investments. As for FY2024, I remarked on how aggressive the implied level of cost cutting looked last time given the inflationary backdrop, and unsurprisingly management dropped its target in the following quarter (i.e. Q2). At this point I think a good result for the bank would be roughly flat OpEx in FY2024, so around €5.1 billion in cash terms. Management will provide a firmer target alongside Q4 results in mid-February.

Analysts have also been pressing for some more clarity regarding capital returns plans. The bank's CET1 of 16% based on Basel IV is higher than its threshold for triggering stock buybacks, with analysts unsure what constraints are stopping management from distributing excess capital already. Management again pledged to provide more detail alongside Q4 results next month.

Valuation Remains Puzzlingly Cheap

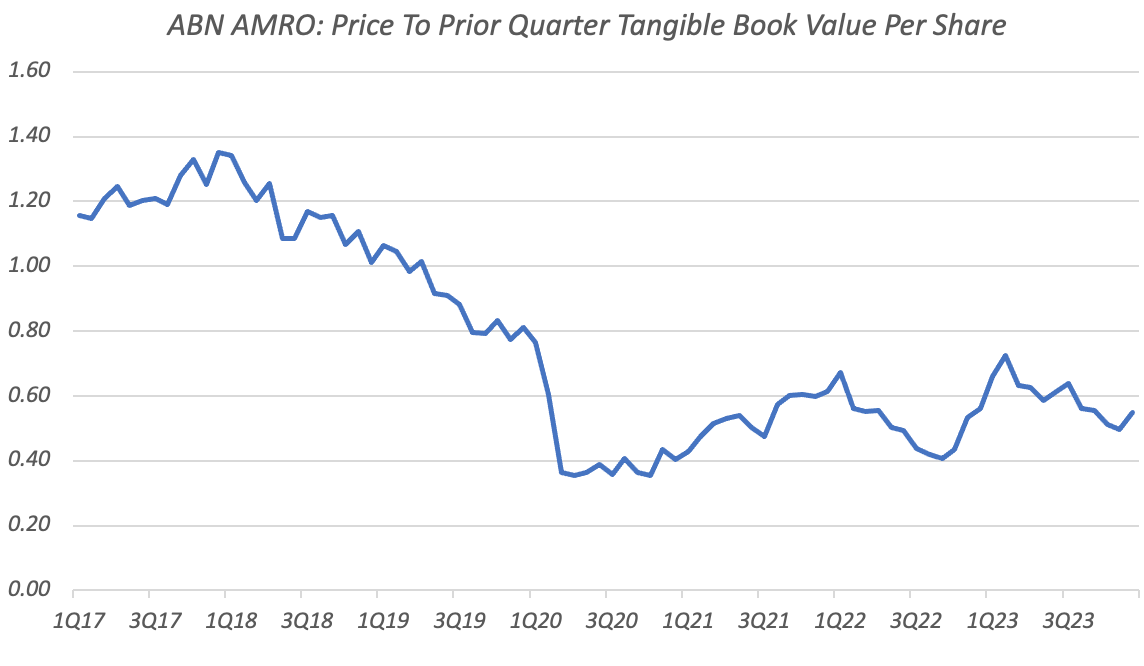

The above notwithstanding, ABN AMRO stock remains puzzlingly cheap. The shares trade for €13.85 in Amsterdam trading as I type ($15.07 per ADS), putting them at just 0.55x tangible shareholders' equity per share. That is even cheaper than the ~0.65x multiple it was on last time, and further represents a significant 50% discount to its average in the three years before COVID, when the bank frequently traded at a premium to tangible book value and was earning a circa 10% return on tangible equity ("ROTE"). For reference, 9M'23 EPS of €2.40 per share maps to a ROTE in the 13-14% region, further highlighting just how wide the valuation disconnect appears to be right now.

Data Source: Yahoo Finance, ABN AMRO Quarterly Results Releases, Author Calculation

{kind=link}

Now, it's only right that we should make some deductions to account for the current favorable macro environment. Although it has been a bright spot for much longer than anticipated, credit quality is going to normalize at some point in the near future. With NII also topping out, we have likely hit peak earnings both here and indeed across the wider European bank space.

Even so, bumping up COR to 20bps in order to better reflect mid-cycle conditions still allows the bank to make a decent return. Baking in a modest decline in NII, plus flattish fee income and OpEx, should still allow the bank to earn circa €2 billion in net income, or around €2.35 per share (~$2.60 per ADS). That would map to a circa 10% return on tangible equity as things stand.

Given that, I don't see any reason to downgrade my prior 0.8x-0.9x fair value multiple, implying a fair value of ~€21 per share (~$21.90 per ADS) at the mid-point. With the bank paying out 50% of net income by way of dividends, shareholders are likely in line for a bumper payout in respect of FY2023. However, even applying more normalized levels of earnings power still results in substantial high single-digit dividend yield potential, rewarding investors while they wait for the valuation gap to narrow.

Risks

In terms of risks to the thesis, there are always plenty to consider with any bank. Through-the-cycle credit quality guidance could prove overly optimistic, while the bank might struggle to keep a lid on operating expenses. One key point to chew on with ABN AMRO in particular is that NII accounts for a disproportionately large of its revenue (70% in 9M'23) compared to peers. Should interest rates in the Eurozone fall back to the zero/negative levels they were pre-2022, this will have a material impact on the bank's profitability over time, with it less able to lean on fee income sources compared to other European banks, though as implied earlier the replicating portfolio will shield it to some extent over the medium term.

Still, with the bank trading at such a large discount to tangible book value, I would argue the market is already baking this in, and as a result I am happy to keep my Strong Buy rating on the stock.

For further details see:

ABN AMRO: Recent Underperformance Enhances The Value Case