ACIW - ACI Worldwide: Trading At A Premium Multiple Despite Underperforming Competitors

2023-12-29 12:54:31 ET

Summary

- ACIW specializes in real-time electronic payment processing and has experienced single-digit revenue growth due to the impact of the COVID pandemic on the economy.

- As the pandemic eases, management expects revenue growth to accelerate as demand picks up.

- Strong demand for real-time payment and government initiatives are expected to drive ACIW's long-term growth.

- However, ACIW is underperforming its competitors and is trading at a high P/E ratio. With no upside potential in my target price, I am giving a hold recommendation for now.

Synopsis

ACI Worldwide (ACIW) specializes in developing software for real-time electronic payment processing. Over the last four years, ACIW’s revenue growth has decelerated to a single-digit rate due to the COVID pandemic disrupting the economy. Despite that, its margins were robust, and expenses were well managed. Moving ahead, the strong demand for real-time payment will drive ACIW’s long-term growth outlook. In addition, the government’s initiatives and drive for real-time payment are expected to bolster its adoption, which will provide ACIW with a tailwind for growth.

However, my conservative valuation model revealed that ACIW is underperforming its competitors. Despite that, it is trading above competitors’ median P/E. By applying a more justified P/E, my target price is below its last traded price. Although strong RTP demand and government initiatives will support ACIW’s growth, its current P/E is too high considering its underperformance against competitors. With these things in mind, I am recommending a hold rating for ACIW as of now.

Historical Financial Analysis

Over the last four years , ACIW’s revenue has slowed down drastically. In 2019, it reported revenue growth of ~24.61%. By 2022, it had slowed down to ~3.74%. Since, 2020 onwards, it has been growing, but at single-digit rates. This modest revenue growth was attributed to the impact of the COVID-19 pandemic on the overall economy.

Author's Chart

Despite moderate revenue growth, its margins look robust and are not showing any signs of deterioration. Gross profit margin [GPM] has been robust and stable at ~50% throughout the years. However, operating income margin [OIM] and net income margin [NIM] have been expanding since 2019, and I welcome it as it means generating more returns and value for shareholders. In 2019, OIM was ~9.84%, and it has expanded to ~14.34% in 2022, representing a growth of ~4.5%. For its NIM in 2019, it was ~5.33%, and it has expanded to ~10%, representing a growth of ~4.67%.

Author's Chart

The reason it is able to expand its OIM and NIM is due to its effective expense management. Based on the following chart, shows a clear trend that both SG&A and interest expense as a percentage of total revenue are falling annually. As a result, they allowed its margins to expand.

For R&D, it remained stable throughout the years, and it was not sacrificed in order to expand its margins. I believe R&D is an important expense for software companies as it drives innovation and keeps products and services up-to-date in the fast-evolving tech industry. R&D helps maintain a competitive edge by developing new and improved features. It's crucial for addressing changing customer needs and market trends and ensuring that its offerings remain relevant.

Author's Chart

Moving onto its balance sheet, its debt level is looking healthy as well. In 2020, the debt-to-equity [D/E] ratio decreased from 2019’s 45% to 36%, and it has stayed at that level ever since. With such a healthy debt level, it does not raise any concerns for me regarding insolvency or liquidity issues.

Author's Chart

Analyzing ACIW’s 3Q23 Earnings Results

In my opinion, ACIW reported strong 3Q23 earnings results. Its total revenue grew ~21% year-over-year to ~$363 million, up from 3Q22’s ~$306 million. Strong growth in its license segment is the main factor driving this growth. Its license segment for the quarter grew ~82% year-over-year to ~$79 million, up from 3Q22’s ~$43 million. In addition, its recurring revenue also grew at double-digit rates of ~10%. Overall, its top line is looking extremely strong.

In terms of profitability margins, it is showing an expansion trend. Its 3Q23 GPM expanded ~7% to ~51%, up from 3Q22’s 44%. For its operating income margin, it expanded to ~17% from 3Q22’s 1%. Lastly, for its NIM, it has expanded by ~2% to ~10%, up from 3Q22’s ~8%.

Author's Chart

As you can see, both SG&A and R&D decreased in 3Q23. This expense management is what drove its margins to expand for 3Q23. Although I did raise my concerns about software companies cutting R&D, ACIW’s R&D cut is minimal for 3Q23. The main driver of margin expansion is its SG&A expenses, which decreased from 3Q22’s ~21% of total revenue to 3Q23’s ~16%.

Author's Chart

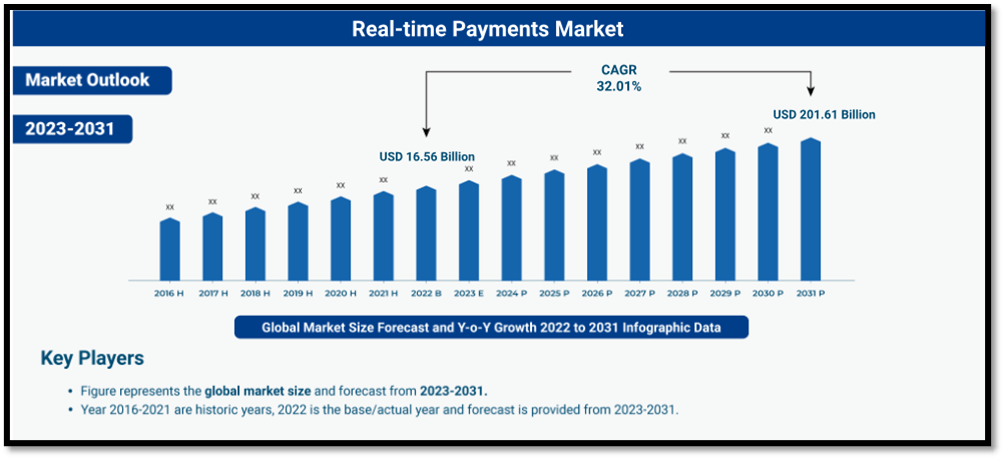

Global Real-Time Payment Demand Is Anticipated to Growth Robustly

In 2022, the global real-time payment [RTP] market size was ~$16.5 billion. It is anticipated to reach a staggering ~$201 billion by 2031. From 2022 to 2031, this represents a CAGR of ~32%. This strong growth is driven by the flexibility and convenience RTP provides to businesses and individuals when it comes to sending or receiving money payments.

Therefore, this strong growth in the global RTP presents significant revenue growth potential for ACIW. With its expertise in payment solutions, it can capitalize on this trend by expanding its customer base and developing innovative RTP services that align with market demands, leading to potential increases in market share and profitability in the long term.

{kind=link}

Government Initiatives Will Drive RTP Adoption

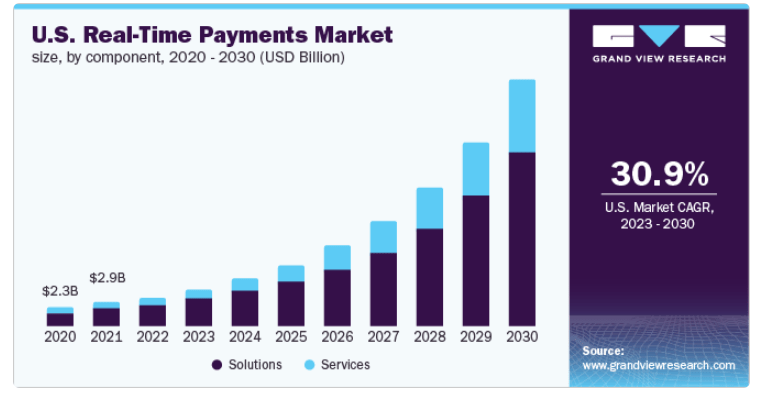

Apart from strong growth in global RTP, the next key driver of RTP adoption is government mandates or government initiatives. In North America, the US Fed has launched its FedNow RTP system. This system could be a major catalyst for RTP adoption in the US due to federal backing, which ensures trust and reliability in the system. It also offers universal access, making RTP services available to banks of all sizes and fostering financial inclusion by enabling immediate fund transfers. This initiative is a significant step in modernizing the U.S. payment system and is expected to drive financial institutions to upgrade their infrastructure.

Based on the following chart , the US RTP market is also expected to grow at a CAGR of ~30.9% from 2023 to 2030. This, combined with FedNow’s positive influence to spur RTP adoption, will bolster ACIW’s future growth outlook.

{kind=link}

In APAC regions, it is leading in terms of real-time cross-border payment initiatives. Based on an announcement by Singapore’s Monetary Authority of Singapore [ MAS ], it has successfully launched the person-to-person [P2P] cross-border real-time payment system between Singapore and Malaysia. In Malaysia, RTP volume is anticipated to grow at a CAGR of ~19% from 2022 to 2027.

For Indonesia, it’s even more staggering, at a CAGR of ~81.9% from 2022 to 2027. Indonesia’s BI-FAST is one of the fastest-growing RTP systems in the world, and ACIW provides the infrastructure for this RTP system. Overall, the anticipated strong RTP growth globally presents significant opportunities for ACIW, as this trend will drive demand for RTP.

Management Future Guidance Is Positive, Aligning with RTP Growth

As a result of its strong financial performance and the growth catalysts I have discussed in depth above, management’s guidance is also pointing in the same direction. For 2023, total revenue is expected to be in the range of ~$1.436 to ~$1.466 billion, which represents an implied growth rate of ~4% to ~6%. For 2024, revenue growth is anticipated to accelerate to the range of ~7% to ~9%.

When compared to 2022’s growth, which I have discussed under the “Historical Financial Analysis” section, the 2023 and 2024 revenue growth rates are almost double that. This speaks volumes regarding management’s confidence in ACIW’s business model and revenue growth outlook. Overall, management’s guidance seems justified, as the growth catalysts I have discussed above align with it as well.

Comparable Valuation Model

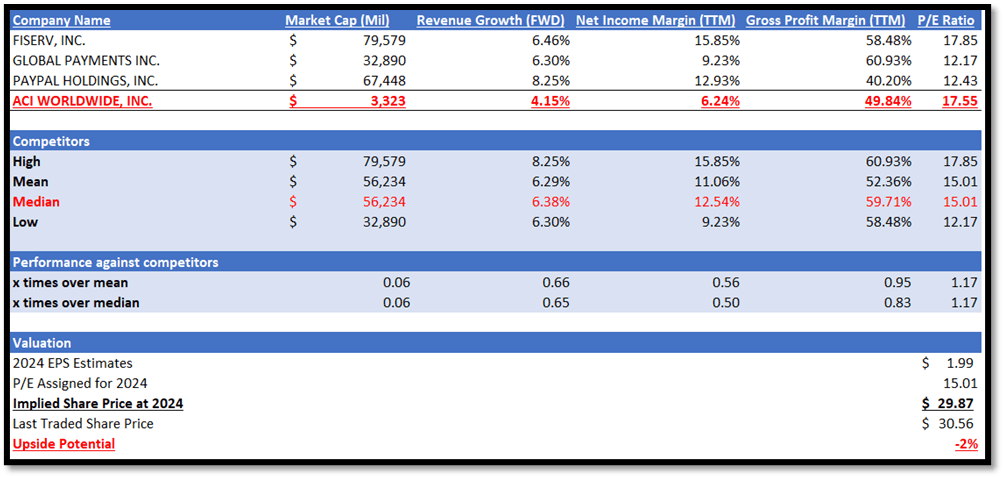

ACIW operates in the application software industry, and it specializes in facilitating digital payments globally. The three competitors I listed in my valuation model also have similar business models.

In terms of market size, ACIW is clearly much smaller than them, as it only has a market capitalization of ~$3.3 billion, while its competitors’ median is ~$56.2 billion. This means that ACIW is only ~6% of their median size.

In terms of forward revenue growth outlook, ACIW also trails behind its competitors. It has a forward revenue growth outlook of ~4.15%, while its competitors’ median is ~6.38%. When compared to competitors’ high range of ~8.25%, it is nearly half of their growth rate.

Moving onto profitability, it does not look promising either. ACIW’s GPM TTM of ~49.84% also trails behind competitors’ median of ~59.71%. In terms of NIM TTM, ACIW performs poorly compared to its competitors. ACIW’s NIM TTM is ~6.24%, while competitors’ median is ~12.54%, almost doubling ACIW.

Despite ACIW’s underperformance in terms of growth outlook and profitability, its forward P/E ratio is trading higher than competitors’ median. ACIW's forward P/E ratio is 17.55x, while competitors’ median is 15.01x. Even with the growth catalysts I have discussed above, I believe ACIW should not command a higher P/E, and in my opinion, ACIW is overvalued. Therefore, to be conservative in my valuation, I will assign competitors’ median P/E of 15.01x to ACIW.

{kind=link}

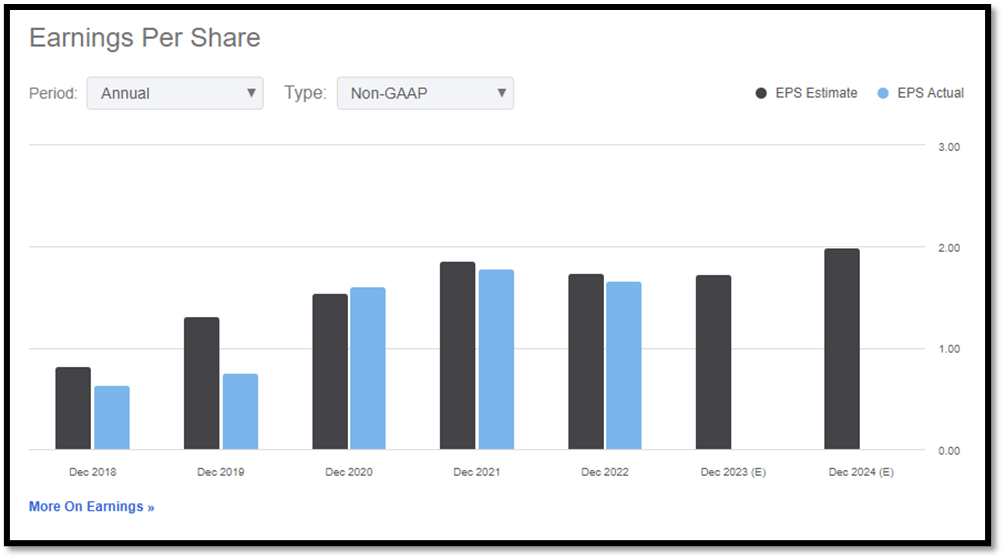

The market revenue estimate for ACIW is expected to reach $1.45 billion in 2023 and $1.55 billion in 2024. The market estimate for ACIW’s 2023 EPS is $1.73, while 2024 is $1.99. The revenue and EPS estimates are reasonable in light of the management's guidance as well as the growth catalysts I have extensively discussed above.

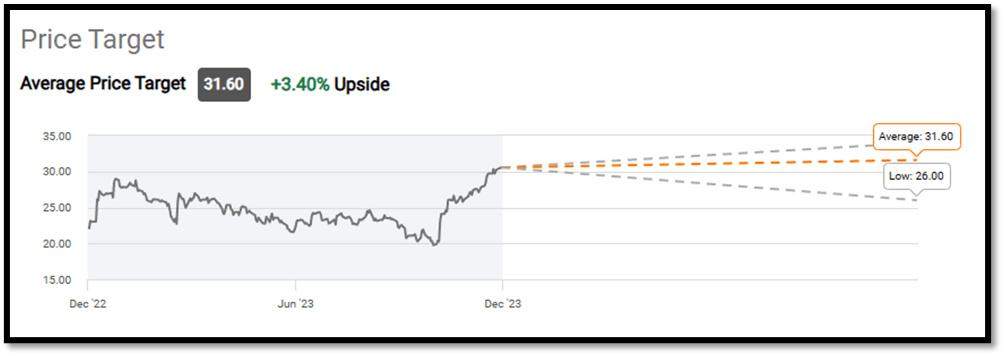

By applying its competitors’ median P/E to ACIW's 2024 EPS estimates, my 2024 price target is $29.87, and this represents a downside of negative 2%. In addition, Wall Street’s average target price of $31.60, which also implies modest gains of only 3.40%, is in line with my target price. Therefore, it suggests that my valuation model is not only logical and realistic but also aligns well with broader market expectations. This correlation serves as a check and balance, reinforcing the credibility and justification of my target price. With these factors in mind, I am recommending a hold rating for ACIW.

{kind=link}

{kind=link}

{kind=link}

Upside Risk to My Hold Recommendation

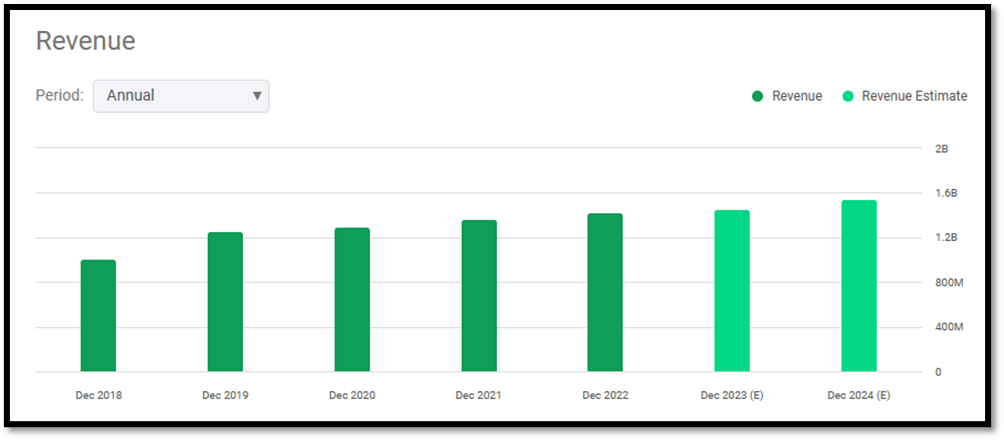

The main upside risk to my hold recommendation is regarding ACIW’s NIM. Based on the following chart, it is clear that SG&A forms the bulk of its expenses. With inflation cooling, it might potentially drive SG&A down even more, and this will boost its NIM.

Under my valuation section, ACIW is outperforming its competitors in terms of forward revenue growth outlook but trails in terms of NIM. If it is able to expand its NIM and move closer to competitors’ median, the general market might give credit to that, and its share price might see positive movement.

Author's Chart

Conclusion

Even since 2020, ACIW’s revenue growth has decelerated drastically when compared to 2019’s double-digit growth rate. Management attributed this to the COVID pandemic disrupting the economy, which ultimately affected their business as consumers cut down on spending. Despite the slowdown in revenue, its margins remained robust, and this was achieved through effective expense management.

In terms of long-term growth, the strong and growing demand for RTP globally is expected to bolster ACIW’s growth outlook. In addition, management’s revenue guidance for the next two years also shows that growth will accelerate, which is in line with the RTP demand trend. In addition, governments around the world are also starting to adopt the use of RTP. These initiatives are expected to boost the adoption of RTP, thereby providing tailwinds for ACIW’s revenue growth.

However, when I compared ACIW with its competitors, it clearly showed underperformance in terms of revenue growth outlook and NIM. Despite these factors, ACIW is trading at a high P/E ratio compared to its competitors’ median, and I do not believe this is justified. After adjusting for ACIW’s P/E, my target price is 2% below its last traded price. In addition, my target price is also in line with Wall Street’s estimates, and this serves as a form of check and balance.

Although I agree that the growing global demand for RTP will boost its revenue growth, its current P/E is too high considering its underperformance against competitors. With this in mind, I am recommending a hold rating for ACIW as of now.

For further details see:

ACI Worldwide: Trading At A Premium Multiple Despite Underperforming Competitors