FMNY - Active Management Will Drive Muni Returns In 2024

2024-01-18 17:17:00 ET

Summary

- After initial optimism at the start of 2023 spurred strong performance, munis subsequently struggled as the Fed continued its tightening policy, raising fed fund rates to 5.25%-5.50%, before pausing in September.

- The Fed and markets now stand at a crossroads, between the end of a tightening cycle and the beginning of rate cuts, and the timing of this shift is nearly impossible to predict accurately.

- Munis continue to play an important role in any diversified portfolio, and the steady nature of their tax-exempt income and high credit quality remain the cornerstone of the muni market.

By Peter Hayes and Sean Carney

Our 2024 Outlook For Municipal Bonds

BlackRock's municipal (muni) bond experts share their market outlook and the actions you can take to raise your portfolio's potential in 2024.

2023 - One Month Does Not A Year Make

After initial optimism at the start of 2023 spurred strong performance, munis subsequently struggled as the Fed continued its tightening policy, raising fed fund rates to 5.25%?5.50%, before pausing in September. The 10-year U.S. Treasury yield sold off, peaking at 5% in mid-October, and the Bloomberg Muni Bond Index was down by 2.30% on a year-to-date basis by late October.

{kind=link}

However, falling inflation, weakening economic growth, and the prolonged Fed pause led to more dovish expectations for monetary policy - causing a strong interest rate rally into year-end (i.e., rates decline and prices increase). As a result, munis rallied sharply, with the Bloomberg Muni Bond Index posting a total return of 8.67% in November and December, bringing the full-year total return to 6.40%. Favorable technicals, backed by strong fundamentals, were key drivers of muni outperformance and pushed relative valuations to extremely rich levels by year-end.

The Fed And Markets At A Crossroads

U.S. economic data held up very well in 2023, supporting the Fed's decision to raise rates higher. However, the Fed and markets now stand at a crossroads - between the end of a tightening cycle and the beginning of rate cuts - and the timing of this shift is nearly impossible to predict accurately. Looking ahead, we expect assumptions about the economic outlook will strongly dictate muni performance expectations. We believe the peak in rates is behind us, but we also believe the market is currently too aggressive in pricing in rate cuts, both in terms of timing and depth. We expect slowing but positive economic growth throughout 2024, with no deep recession. Around midyear, we believe the Fed is likely to begin a series of smaller, 25 basis point "maintenance" rate cuts. Ultimately, we look for modestly lower rates by year-end, with several periods of volatility as monetary policy evolves, and the election comes into focus. We see limited upside for material price appreciation, given the current rich valuations, and anticipate another year of mid-single digit total returns of 4%?6% for intermediate investment grade munis in 2024. We urge caution and patience to start the year and look for better buying opportunities late in the first quarter or early in the second quarter.

{kind=link}

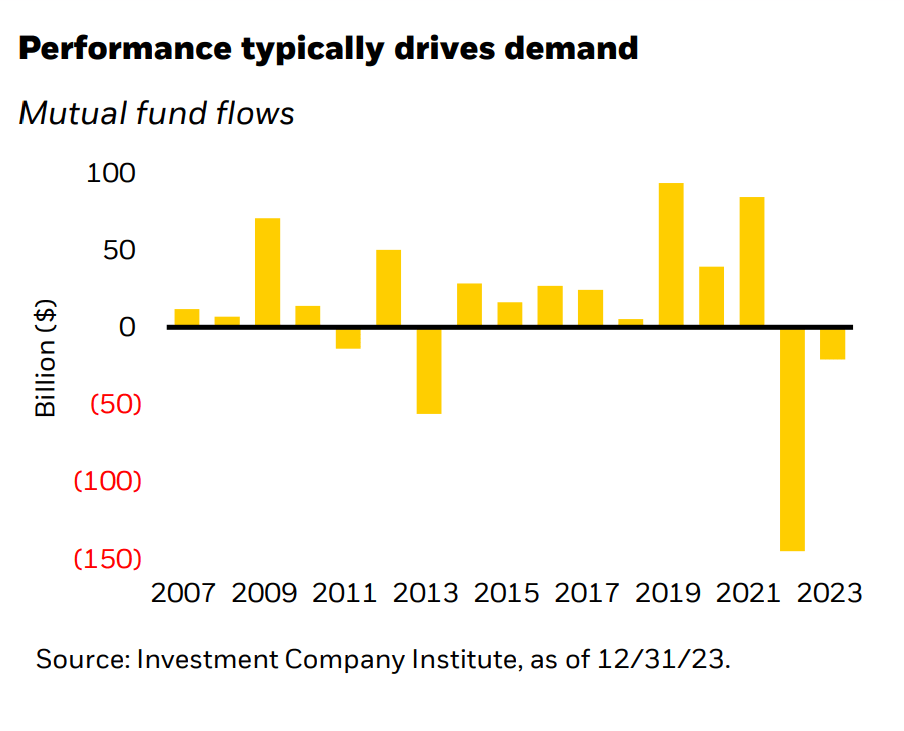

A Demand Shift In Mutual Fund Flows

As rates rose in 2023, mutual fund outflows continued, although the total outflow was much less than in 2022 ($21 billion versus $145 billion), with demand shifting from funds to individual bonds and ETFs. However, given the strong muni performance through year-end 2023 and expectations for a continuing decline in rates this year, we believe some demand could now shift back into funds during 2024. Overall, we foresee flows returning at a slower rate than the recent outflow cycle, with approximately $20?$25 billion flowing back into funds (or about 15% of what was previously lost), creating an opportunity for active management by remaining nimble in evolving markets.

{kind=link}

Issuance in 2023 was just $359 billion, a small 2% increase from 2022, as issuers shied away from rising rates and volatility. Looking ahead, refunding issuance is expected to fall, and new money issuance is expected to rise.

Overall, we are calling for a 15% increase in issuance to $410 billion, as a result of slowing revenue growth, less fiscal stimulus, and pent-up demand. Issuance seasonality should be typical for a presidential election year, with a lighter supply to start 2024, followed by increased supply over the summer, and a significant pull forward from November into October. Net issuance should increase by $39 billion, marking the largest net positive supply environment since 2016 (+$67 billion). We expect taxable munis will account for about 10% of total issuance.

Selection Will Be Key, With An Up-In-Quality Bias

The pull forward of performance experienced in late 2023 warrants patience as we begin 2024. Munis continue to play an important role in any diversified portfolio, and the steady nature of their tax-exempt income and high credit quality remain the cornerstone of the muni market. Given the rise in yields from their lows in 2021, more income can now be generated with less risk. We currently favor a neutral to slightly short duration position, overall, until we see valuations return to more normal levels. We advocate a barbell curve strategy, pairing front-end exposure with an increased allocation to the 15 to 20-year part of the curve, reducing reinvestment risk for when the Fed begins to cut rates. Going out 15 to 20 years allows one to pick up 80%-90% of the curve while assuming just 65%-70% of the duration. We are maintaining an up-in-quality bias with a neutral allocation to high yield, but we think high-yield munis may offer an attractive risk-reward opportunity as 2024 unfolds, given favorable structures and the possibility to generate alpha through careful security selection.

Credit Views For 2024

A Tale Of Two States

With reserves at nearly an all-time high and debt service burden at a 50-year low, states are well-positioned to weather a potential economic slowdown. However, tax receipts are diverging for the states that primarily rely on consumption taxes, compared to their peers that depend on income taxes. State median revenues declined by a slight 1% for the rolling 12 months ending September 2023. States with regimes that favor sales taxes, such as Florida, Nevada, Texas, Tennessee, and Washington, all experienced positive revenue growth, while states that depend on personal income taxes, such as California and New York, experienced much greater declines in receipts, by 23% and 16%, respectively. Particularly in California's case, the rating agencies have been patient, but the risk of downgrades has increased significantly. Meanwhile, spreads remain surprisingly tight, reflecting investor indifference. Personal income tax collections should improve this April, due to a rebound in the financial markets, which should alleviate the strain on New York's budget, but California will need to enact significant corrective action to address its reported $68 billion deficit.

Hard times?

No sector is immune to an economic contraction; however, most municipal issuers are ultra-defensive since they provide essential services and can raise user fees or taxes to cover operations. Across all muni sectors, we anticipate borrowing to increase modestly in 2024 due to various potential factors: revenue shortfalls, aversion to fee increases, reluctance to cut programs, no future federal stimulus, preference to maintain liquidity, and deferral of capital expenditures. Patient investors will have better options in 2024 to buy solid credits in the primary market or discounted names in the secondary market.

Possible Great Expectations

Fundamentals are positive for most high-yield sectors, and issuance remains sporadic. Tax collections in Puerto Rico continue to outperform; enrollment trends remain supportive for charter schools; and strong demand for new housing bodes well for land-secured bonds. Tobacco bonds face some fundamental headwinds with consumption declines exceeding trend and a pending federal ban on menthol. Unlike corporate bonds, municipals are not subject to material refinancing risk. Defaults remain episodic and concentrated in healthcare and industrial development bonds. In 2024, we anticipate a modest uptick in defaults within the high-yield sector concentrated in senior living, project finance, and recent vintage land development deals. Liquidity continues to be a concern for high yield, but technicals remain supportive with low new-issue supply, healthy mutual fund cash balances, and the potential for positive fund flows. Heading into 2024, credit spreads offer fair compensation for risk, and with a significant percentage of the market priced at discounts, high-yield municipal bonds have the potential to outperform the general market.

{kind=link}

This post originally appeared on the iShares Market Insights.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Active Management Will Drive Muni Returns In 2024