SOJE - ACV: Attractive Discount And Distribution For This Diversified Fund

2023-07-21 16:46:20 ET

Summary

- The Virtus Diversified Income & Convertible Fund has provided attractive returns this year after taking a hit along with the rest of the market last year.

- The fund's discount remains attractive and has widened after starting the year off at a premium.

- ACV's distribution rate is high and definitely tempting; however, the fund will require significant capital gains to fund it unless NII continues to head in the right direction.

Written by Nick Ackerman, co-produced by Stanford Chemist.

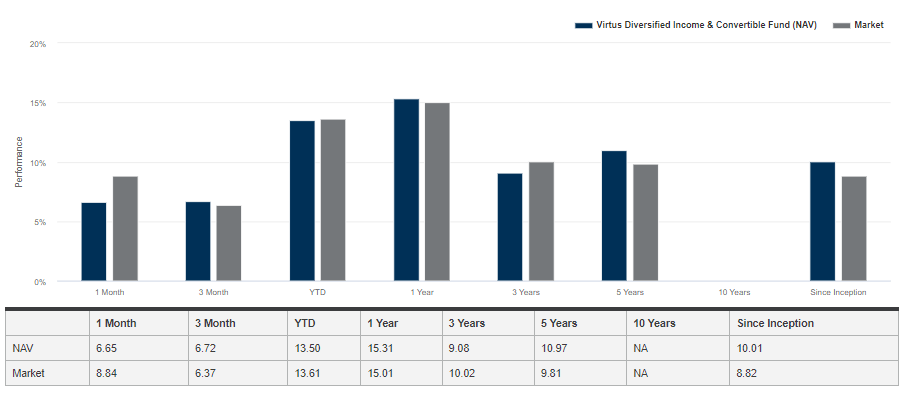

Virtus Diversified Income & Convertible Fund ( ACV ) isn't at the peak levels it was during 2021, but a heavier tech emphasis on this fund has provided some attractive returns this year. Additionally, the fund's discount remains attractive and has actually widened out a bit since our prior update . A widening discount would have limited some of the upside total return results since that update, but the fund has still put up respectable returns during this time.

ACV Performance Since Prior Update (Seeking Alpha)

The fund's monthly distribution also remains quite enticing, though it should be cautioned that the payout will require significant capital gains to fund. Therefore, investing in ACV for the distribution, one would have to believe that the underlying portfolio can deliver appreciation.

The fund is diversified not only with sector exposure but also through asset allocations due to carrying convertibles, equities and high-yield debt exposure. This was one of the funds that benefited heavily from the run-up in equities and convertibles during 2020 and 2021. That euphoria has worn off now, but it only represents a better time to consider this fund for the long term.

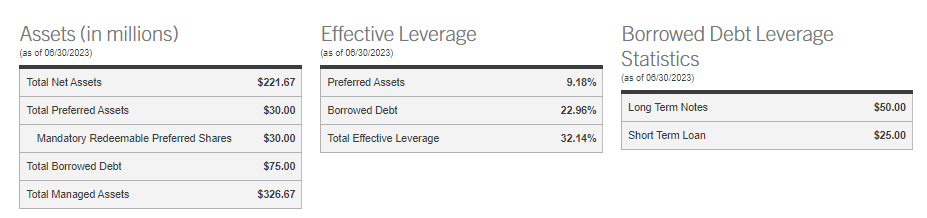

The Basics

- 1-Year Z-score: -0.85.

- Discount: 7.28%.

- Distribution Yield: 10.66%.

- Expense Ratio: 2.17%.

- Leverage: 32.14%.

- Managed Assets: $326.67 million.

- Structure: Term (liquidation expected around May 22nd, 2030).

ACV's investment objective is to "provide total return through a combination of current income and capital appreciation while seeking to provide downside protection against capital loss."

To achieve this objective, they will "strive to dynamically allocate across convertibles, equities, and income-producing securities. The Fund normally invests at least 50% of total managed assets in convertibles and has the latitude to write covered-call options on the stocks held in the equity portion."

With such a flexible strategy, the managers have quite a few levers they can pull in an attempt to generate returns and cover that enticing distribution to investors. The fund being leveraged is one such lever. However, with rising interest rates, the costs of that leverage have increased. The fund's total expense ratio has climbed to 3.49%. That was up from 2.55% in the prior year.

One way to help manage the fund's expenses is through the mandatory redeemable preferred shares ("MRPS"), which is paid a dividend at a fixed rate of 4.34%. That accounts for $30 million in leverage. In addition to the fund's MRPS, they have issued notes that pay a fixed rate at 3.94%. That's another $50 million in leverage.

{kind=link}

That leaves us with the remaining $25 million that the fund has taken out through margin loan financing. At the end of their last annual report , borrowings came to 5.39%. That was up significantly from the average during this period, which was at 3.21%. So while they paid up initially when issuing the notes and the preferred, this has now been to the fund's benefit as interest rates have ramped up.

The fund's notes don't mature until November 22, 2029, six months before the fund itself is anticipated to liquidate. The MRPS has a much sooner maturity with a mandatory redemption date of October 2, 2025. It's unclear what they will attempt to do when that time approaches. Of course, there are still over two years before that becomes a larger question for the fund. In that two years, anything in terms of interest rates could happen, so trying to guess at this point is probably futile.

Performance - Strong Results And Attractive Discount

The fund isn't necessarily the oldest, but it still has some history for a fairly solid track record. The fund was around long enough to see a significant rise after the Covid pandemic due to its convertible and growth-oriented portfolio. Any investor who bought during this period is unlikely to be in a very envious position, as 2022 was a tough year for the fund. That said, the fund has still produced relatively attractive results on most annualized periods when the fund's distributions are factored in.

{kind=link}

Further, the fund's discount remains quite attractive relative to its history. The fund has traded at a premium on several occasions. That includes as recently as the beginning of 2023, despite what would have appeared to be a terrifying downward slope in 2022. The fund's current discount shows it is trading just below its inception average and well below its recent premium levels.

YCharts

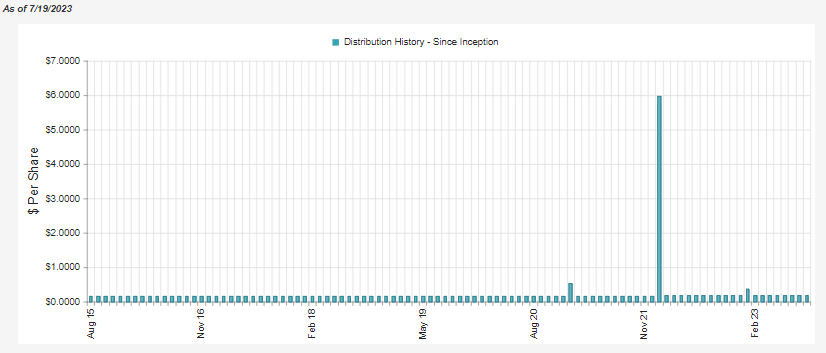

Distribution - Double Digit 10.66% Rate

The fund's distribution is quite attractive, topping out at a double-digit rate, and thanks to the fund's discount, the NAV rate comes in at 9.89%. When things were going well for the fund, investors reaped that reward through a massive year-end special distribution. That alone came at nearly $6 and would have meant a share price and NAV reduction of $6. Even last year, investors saw a special paid out.

{kind=link}

That being said, while the fund's distribution rate is certainly attractive and the discount means the fund has to earn less to cover its payout, at nearly 10%, the NAV rate is quite elevated for this type of fund. This could be considered especially true during what could be a tougher economic period going forward.

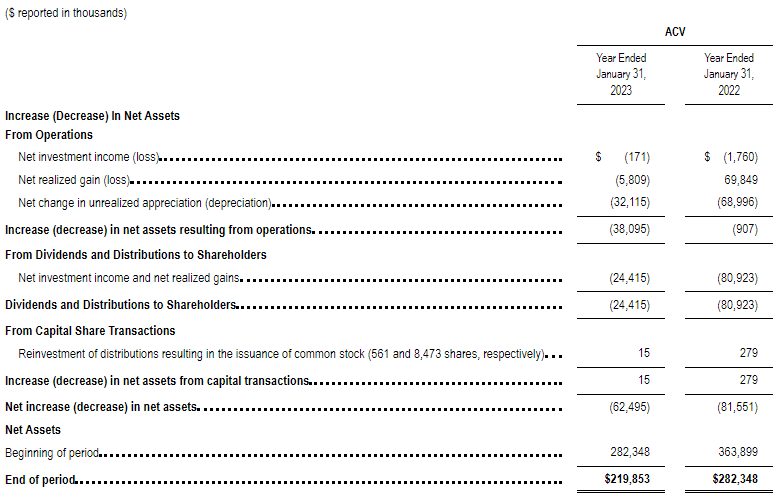

The reason for this is that the fund doesn't actually produce any net investment income. That means that after the fund accounts for all the dividends and interest payments it receives and subtracts the expenses of the fund, there is a negative figure.

{kind=link}

That puts ACV in a position where the entirety of its distribution had required capital gains. Of course, it should also be mentioned that convertibles are experiencing higher yields due to rising interest rates. That is, companies have to actually pay some yields instead of 0% coupons in order to attract investors to their offerings. That said, the fund produced some positive NII in the years 2019 and 2020. 2021 was essentially flat.

For the latest fiscal year-over-year period, loan interest went from $2.241 million in fiscal 2022 to $2.772 million in fiscal year-end January 31st, 2023. The total investment income generated last year was $7.272 million compared to the latest year's $7.719 million. However, one of the largest contributors to the fund's increase in NII besides higher TII was the fact that the fund was much smaller in the latest year. That resulted in the fund's investment advisory fees going from $4.705 million to $3.395 million.

Despite the fund's expenses rising in the prior year, NII moved in a positive direction. Some of that could be due to these higher yields, but of course, portfolio position will also play a significant role too. With most of the fund's leverage based on fixed rates, the next report could even reflect some positive NII should the current trajectory continue.

The fund was also able to generate some options premium in the last fiscal year too. It wasn't significant, but any options premium generated is better than nothing. They write options against individual positions within their portfolio.

ACV Realized/Unrealized Gains/Losses (ACV Annual Report (highlights from author))

{kind=link}

At this point, they appear to be content with continuing to pay out the same $0.18 monthly distribution. If the fund can continue to perform as well as it has been in this rebound, then a cut may be avoided. To help reduce the chances of a cut, seeing higher yields potentially turn into positive NII could also result in a better outlook.

ACV's Portfolio

The fund's turnover rate is rather high for this fund. The last year was the lowest turnover year in the last five, with a 94% turnover rate. That was down from 108% in the prior year, which itself was lower than 128% and 120% in 2021 and 2020, respectively.

That said, the fund's portfolio positioning, in a broader sense, tends to stay rather consistent. The fund's overemphasis on convertible securities at nearly a 60% weighting is rather consistent with the 61.33% reported at the end of 2022. Equities then follow that up with a nearly 25% weight, which is up only from the 22.5% previously. Finally, the high-yield bond allocation came down a touch to 12.61% from 13.84%.

{kind=link}

This sort of weighting comes as little surprise either, as the fund's policy is to generally invest at least 50% of its assets in convertible securities.

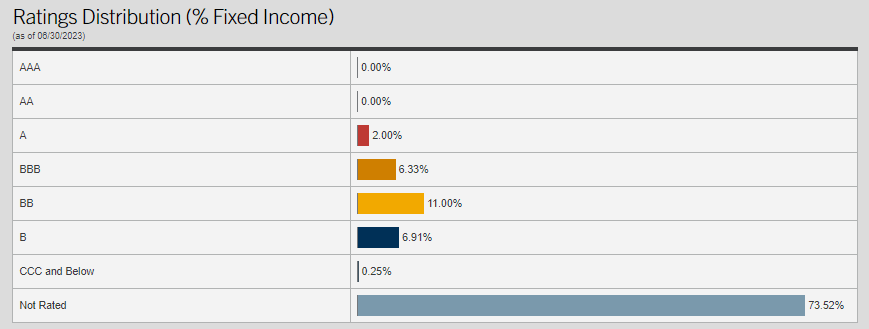

Worth mentioning for a convertible fund is that the largest credit quality allocation is going to be attributed as "Not Rated." This is generally the case as many of the holdings in ACV's portfolio are 144A Securities issued to qualified institutional buyers. These are buyers such as ACV that can then allow access to retail investors through these investment wrappers.

{kind=link}

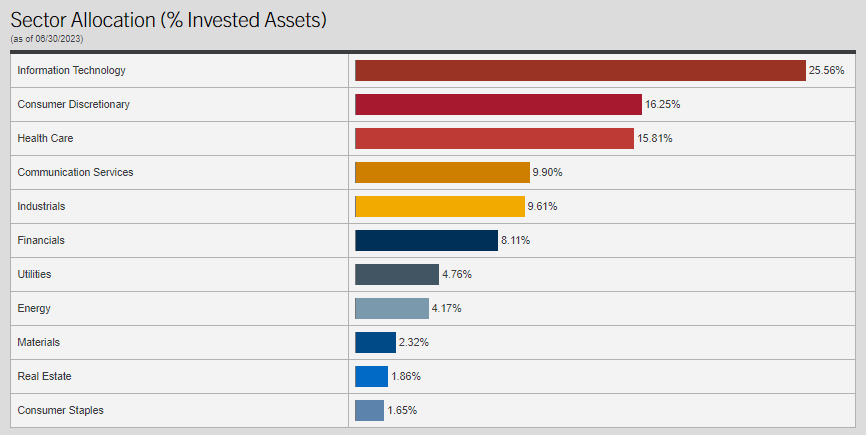

The sector weighting of the fund is where we've seen some shifting in terms of the allocation. Tech still represents the largest allocation by a significant amount relative to the next largest sector allocations of consumer discretionary and healthcare. However, this is down from the 27.36% listed in information technology previously.

{kind=link}

Going back even further, we'd see that the sector allocation to tech was even larger in the same period reported a year ago. At that time, the sector came in at a weight of nearly 33%. That makes the fund still growth-oriented in its approach, as it naturally would be with convertible securities. Still, the tech sector allocation has come down quite materially from where it was. That could put the fund in a better position to actually offer a more diversified approach.

This also coincides closely with the subadvisor change . This had previously been an AllianzGI fund, but they were barred from operating in the U.S. due to fraud in an unrelated fund. This is how it became a Voya-managed fund. That said, two of the same managers transitioned with the fund from AllianzGI to Voya, which had been managing it since its inception in 2015. So this could have been just a natural shift in the portfolio manager's decision.

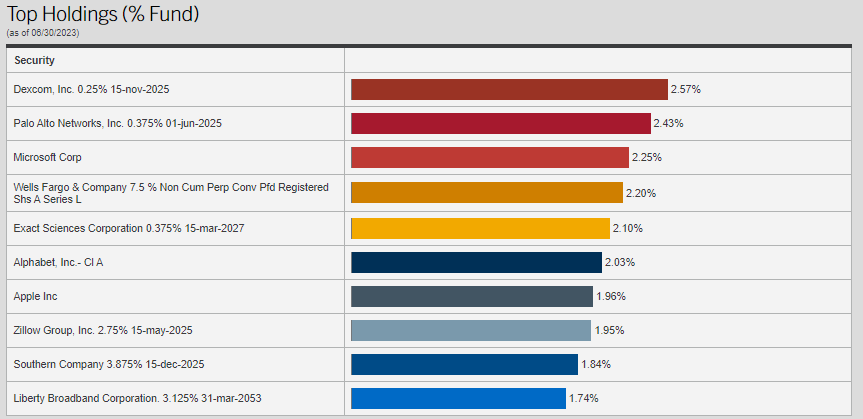

The fund's top holdings give us a good mixture of equity and convertible positions. The convertibles are representative of the lower-yielding types that were issued when interest rates were much lower. At the same time, we are starting to see some higher yields show up, too.

{kind=link}

For example, the highest convertible yield in the portfolio previously was GS Finance Corp at 0.5%. We now have Zillow Group's 2.75% ( Z )( ZG ), Southern Company's ( SO ) 3.875% and Liberty Broadband Corporation ( LBRDA ) with a 3.125% convertible position. The Liberty Broadband positions that the fund carried previously were lower-yielding instruments, with this latest one issued to repurchase the previous debentures. A good example of having to issue a higher coupon with newer debt obligations being issued into 2023.

ACV Snapshot of Holdings (ACV Annual Report (highlights from author))

The Zillow 2.75% was a previous position, and the 3.875% from SO is also a newer position to show in the fund since its last annual report. SO issued this earlier in 2023 . That's another good example of convertibles being issued with higher yields, but also the fact higher quality companies are issuing convertibles to keep their debt costs more reasonable. That was another topic discussed in the fairly recent Calamos article discussing the opportunities in convertible bonds.

Conclusion

ACV remains an attractively valued fund at a discount; the fund's distribution rate is certainly tempting. With some better yields in the market, convertibles are starting to pay something these days that could help provide coverage for the payout. Should the market continue to cooperate and the underlying positions recover further to provide an appreciation for the fund, then that would put ACV in an even better position to cover its payout. Thanks to mostly fixed rate costs for their leverage, they aren't facing the same pressures that some other CEFs face through rapidly rising borrowing costs.

For further details see:

ACV: Attractive Discount And Distribution For This Diversified Fund