LBRDB - ACV: Hybrid Closed-End Fund Worth Watching

2023-11-09 18:00:19 ET

Summary

- Virtus Diversified Income & Convertible Fund is a hybrid fund that invests across asset classes, though it tilts towards convertibles with a tech-tilt.

- The fund's leverage and being a closed-end fund can often make this fund quite volatile, which can lead to opportunities that can show up quickly but can disappear as quickly.

- The fund's distribution rate is quite tempting, but I would still remain cautious given that it is elevated while capital gains are needed to fund it.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Since our last coverage on Virtus Diversified Income & Convertible Fund ( ACV ) earlier this year, shares have been in for a wild ride. Most recently, the fund had dropped significantly as the S&P 500 and Nasdaq slid into correction territory before sharply reversing those losses.

ACV went from an attractive discount back to a narrow discount just as fast, which highlights how quickly opportunities can come and go. The fund has a hybrid approach, and, as its name would suggest, it is fairly diversified. Given the leverage of the fund, that can make it even more volatile.

ACV Performance Since Prior Update (Virtus)

I would switch to a 'Hold' rating at this time, looking for a wider discount of 5%+ before considering the fund to be more attractively priced. Investors who were quick could have just recently had such an opportunity to buy it at those levels. In addition, it was combined with the fact that the overall market had slumped meaningfully.

The Basics

- 1-Year Z-score: 0.69

- Discount: -1.40%

- Distribution Yield: 11.33%

- Expense Ratio: 2.27%

- Leverage: 35.38%

- Managed Assets: $305.4 million

- Structure: Term (liquidation expected around May 22nd, 2030)

ACV's investment objective is to "provide total return through a combination of current income and capital appreciation while seeking to provide downside protection against capital loss."

To achieve this objective, they will "strive to dynamically allocate across convertibles, equities, and income-producing securities. The Fund normally invests at least 50% of total managed assets in convertibles and has the latitude to write covered-call options on the stocks held in the equity portion."

While there is an appeal to ACV currently, the expense ratio isn't one of its flattering points. This is high, and it only gets higher when including the leverage expenses. The total expense ratio for the last six-month report came in at 4.06%. That's up from the 3.49% in the prior fiscal year-end and up from the 2.55% from the fiscal year-end 2022.

{kind=link}

ACV Leverage Stats (Virtus)

Some of this leverage is at fixed rates, and we've still seen the costs rise substantially. The fund has three different forms of leverage: a mandatory redeemable preferred share series A that pays a fixed 4.34%. This matures toward the end of 2025, and that is $30 million of the leverage. They also have secured notes that pay a fixed 3.94%; this matures at the end of 2029 and is the largest amount at $50 million.

Finally, it is the margin loan that had $25 million in play and saw an average interest rate of 5.94%. This is based on a spread above OBFR. At the end of their last fiscal year, the average interest rate for that was 3.21%. So we can see that there was a significant jump, as expected. That's been the driving factor in seeing the expenses rise for the fund.

Performance - Attractive Discount Comes And Goes

When looking for CEFs to buy, we get the chance to exploit discounts/premiums as they often trade wildly different from their NAV per share. One of those opportunities just came and went quite quickly as the broader market entered correction territory before bouncing sharply higher. During this time, ACV went to an attractive discount and then narrowed sharply. With the fund trading above its longer-term average, it doesn't present an appealing time to consider adding to the fund. On the other hand, it also isn't grossly overvalued either.

The primary caution, besides being a leveraged fund that will exaggerate both upside and downside moves, would be that the fund's distribution is running a bit hot here. We've already seen several closed-end funds cut their distributions over the last year as the markets remain pressured by rising risk-free rates. If ACV cuts, we'd likely see a sizeable drop as the fund goes to an even deeper discount.

One recent example of a fund that was already at a discount but cut and went even deeper into the discount territory was Virtus Total Return Fund ( ZTR ). A completely different fund with a completely different investment policy and approach; however, distribution cuts are almost always met with the same reaction no matter what CEF you look at. So, being at a discount certainly keeps the carnage more limited, but it doesn't take away the downside move.

The fund has had a decent run when considering the asset allocation they have generally been positioned with. That is primarily convertible bonds, most recently around 60%, then equity exposure at around 25% and then around 12.5% in high-yield bonds. Overall, the fund has performed more similarly to its convertible ETF counterpart, iShares Convertible Bond ETF ( ICVT ). The fund participated in the big boom of 2020/2021 when convertibles were really popular but then subsequently lost a sizeable amount of those gains through 2022, along with most convertible securities.

YCharts

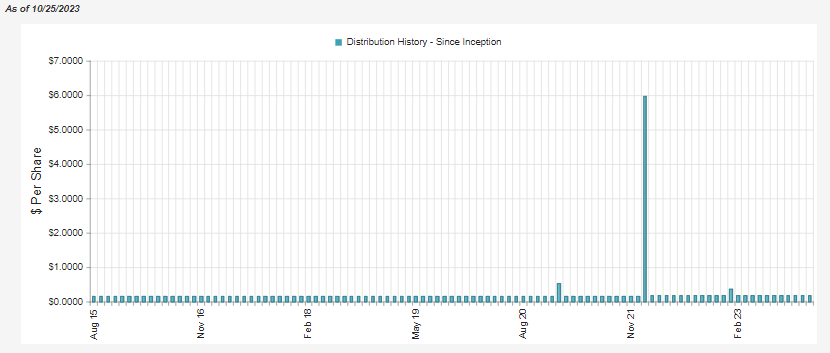

Distribution - Looking Tempting, But Caution Remains

ACV has only ever increased their distribution and even paid a few specials in the last several years. However, that's been primarily a function of a strong operating environment for convertible and equity funds.

{kind=link}

ACV Distribution History (CEFConnect)

Given that equities have been mostly moving sideways outside of the mega-cap tech names, ACV's distribution could be hard to maintain. At a distribution yield of 11.33%, it certainly is attractive, but the fund's underlying NAV still has to earn a rate of 11.17% to cover it. Like many equity funds with a heavy emphasis on tech, it started to look promising earlier this year.

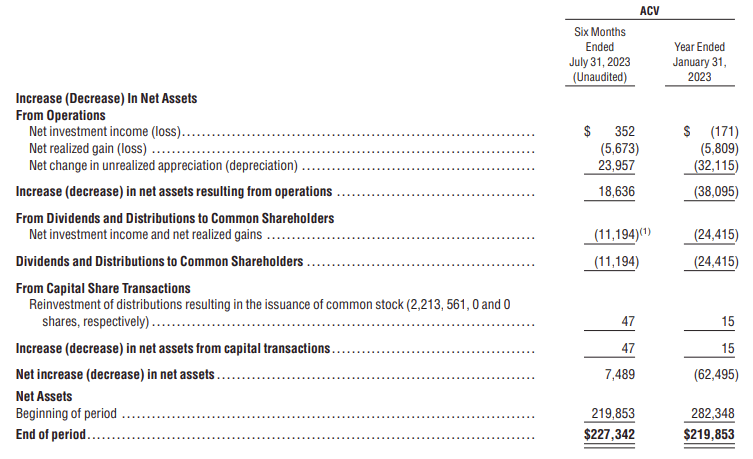

We can see that while the fund realized losses, the unrealized gain pool grew in the first half of its fiscal year to support the payout. Since this report, however, the NAV has slid lower, and that would mean the fund has experienced losses since this report.

{kind=link}

ACV Semi-Annual Report (Virtus)

On the other hand, a benefit of rising rates has been that yields have come up now, and that appears to have helped ACV move to a level where they can actually have positive net investment income. This reflects that it has even been enough to counteract the growing interest expense of the fund. Still, coverage from NII remains only a fraction of what is ultimately required.

In terms of tax classifications for the distribution, we covered that earlier this year for the breakdown. Official characterizations aren't known until year-end, meaning we won't see a new tax breakdown until earlier next year. Here is a recap:

For tax purposes, the last two years show that the majority of the distributions were either ordinary income or long-term capital gains. However, as we touched on above, capital gains can become harder to come by if there isn't some rebounding in the broader convertible and equity market. At some point, destructive return of capital could be utilized to maintain the same distribution.

ACV Distribution Tax Classification (Virtus)

{kind=link}

ACV's Portfolio

ACV is a fairly active fund when it comes to buying and selling; the last six-month report shows turnover came to 59%. Over the last five years, the turnover rate has averaged 111%.

Despite that, the fund's overall positioning has remained fairly similar to our last update. Consistent with the fund's strategy of at least 50% being allocated to convertible securities, we see that as the largest weighting of the fund. Nearly identical to the 59.46% weighting we saw at the end of June 2023.

{kind=link}

ACV Asset Allocation (Virtus)

In terms of the fund's credit quality of its fixed-income sleeve, the majority is going to be mostly unrated or not rated. This is because the fund invests in convertibles that often don't get rated and are sold to qualified institutional buyers such as this fund. What is rated is primarily below investment grade, though, which is what we would expect.

{kind=link}

ACV Credit Quality Rating (Virtus)

For the sector weighting of the fund, the fund remains over a quarter invested in the information technology sector. Following that, we have the consumer discretionary sector present. That's primarily consistent with what we saw previously.

However, instead of healthcare coming in at a nearly 16% allocation that rivaled a close weighting to consumer discretionary, we now see a shift toward industrial. Industrials saw their weighting increase from ~9.6%, while healthcare saw its allocation drop to around 9% now.

{kind=link}

ACV Sector Allocation (Virtus)

That's not an immaterial change, but with the fund still being dominated by tech and discretionary, that will still play a bigger role in the fund's performance. On the other hand, we still see the fund carries diversified exposure with at least some allocation to each broader sector. With around 285 holdings, that isn't too surprising.

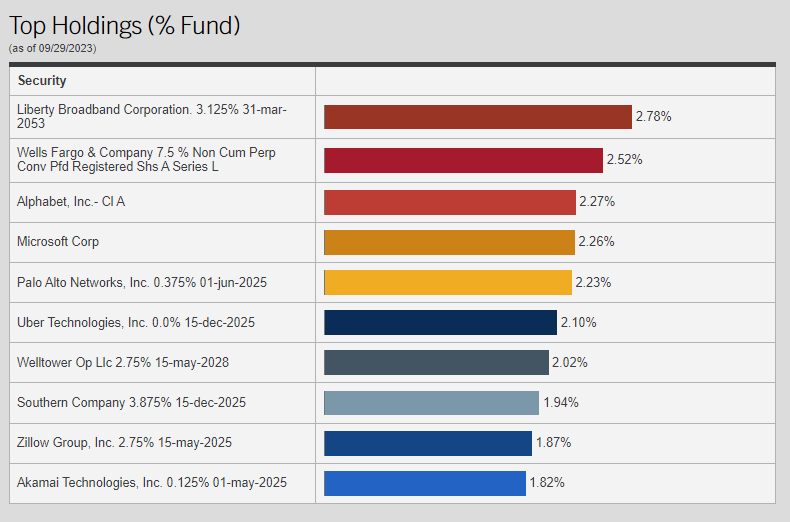

For the fund's largest holdings, we see a few names on the list shuffled around. With allocations that are fairly evenly split without significant weight to any specific holdings, natural gyrations of the market can cause some changes on their own. Given the highly active nature of ACV's management, that can also contribute to more consistent changes.

{kind=link}

ACV Top Ten Holdings (Virtus)

Liberty Broadband Corporation's ( LBRDA ) 3.125% convertible position has made a move from the tenth largest holding to now holding the highest weighting of the fund. That saw the weighting go from 1.74% to the 2.78% we see today. This is an example of a 144A security, which gets sold to QIBs.

Microsoft ( MSFT ) and Alphabet ( GOOG ) were also previous positions in the fund's top ten. Although, a notable removal from the top ten list was Apple ( AAPL ). They held an equity position in that name as well, which came to around a 1.96% weight. This position sunk to a 1.12% weighting when looking at the full holdings list , which dropped it to the 13th largest position of the fund.

Conclusion

As we recently saw, ACV reacted in quite a volatile manner with what ended up being an incredibly short correction we recently experienced for equities. The fund's discount rose sharply to a fairly attractive level before snapping back.

The fund has primarily fixed-rate financing in terms of its borrowings, but the portion that is floating on the margin loan has seen its costs rise fairly significantly. enough of a rise that we've seen the total expense ratio climb meaningfully.

That said, the underlying portfolio has started to yield some NII for the fund. We saw that reflected in the fund producing positive NII in the first half of the year, while last fiscal year, it was negative. It's almost negligible at this point as it was $0.03 per share, and if that continued through the second half of the year, it would be $0.06. That's not even enough to cover half of one monthly distribution. Still, if yields stay elevated, this should continue to head upward.

Outside of leverage, my main concern would be the fund's higher distribution yield. While that could easily be considered its strongest selling point, it's at a level that seems unsustainable. That opinion would change if the fund's NAV rate drifted below the double-digit level if this recovery continues.

When distributions are cut, there is often a harsh negative reaction, and being in an unfavorable environment with CEFs trading at near historically deep discounts, investors seem to be ready for any reason to sell.

Overall, ACV continues to be a name worth sitting on an investor's watchlist.

For further details see:

ACV: Hybrid Closed-End Fund Worth Watching