ADPT - Adaptive Biotechnologies: MRD Success In A Challenging Market

2023-12-15 01:19:38 ET

Summary

- Adaptive Biotechnologies' MRD segment, primarily clonoSEQ, shows growth (24% revenue increase) amid sector challenges.

- ADPT faces an overall financial decline (21% revenue drop, larger net loss), reflecting broader biotech industry pressures.

- Short-term financials are adequate with a 25.8-month cash runway, but long-term stability is uncertain.

- Investment Recommendation: Hold. MRD segment shows promise, but caution is advised due to financial and market uncertainties.

At a Glance

Adaptive Biotechnologies ( ADPT ), with its clonoSEQ test in the Minimal Residual Disease [MRD] segment, demonstrates strategic acumen against a backdrop of diminishing COVID-related revenues. The MRD segment's growth, notably a 24% revenue increase, underscores its potential in cancer management. However, the company's overall financial health, marked by a 21% revenue decrease and increased net loss, reflects significant challenges. Adaptive's collaboration with Goldman Sachs for strategic review and its third-quarter earnings paint a complex picture of a company at a critical juncture. Investors should note the robust performance of the MRD segment against a backdrop of broader financial challenges, signaling a nuanced investment consideration. This sets the stage for a cautious yet potentially optimistic outlook, contingent on Adaptive's ongoing strategic responses and market adaptations.

Adaptive's clonoSEQ: Leading the Charge in MRD's Revenue Rally

Adaptive's focus on its MRD segment, particularly through the clonoSEQ test, represents a strategic maneuver in an industry characterized by rapid evolution and stiff competition. This segment's role in Adaptive's portfolio has been increasingly significant, especially when viewed against the backdrop of its third-quarter earnings.

In the third quarter of 2023, the MRD segment demonstrated resilience with a 24% increase in revenue. This performance contrasts with the 52% revenue decrease in the Immune Medicine segment (which features a COVID test product ) during the same period, highlighting the fluctuating dynamics within different segments of the biotech business. This divergence in performance underscores the complexity of operating in such a multifaceted industry.

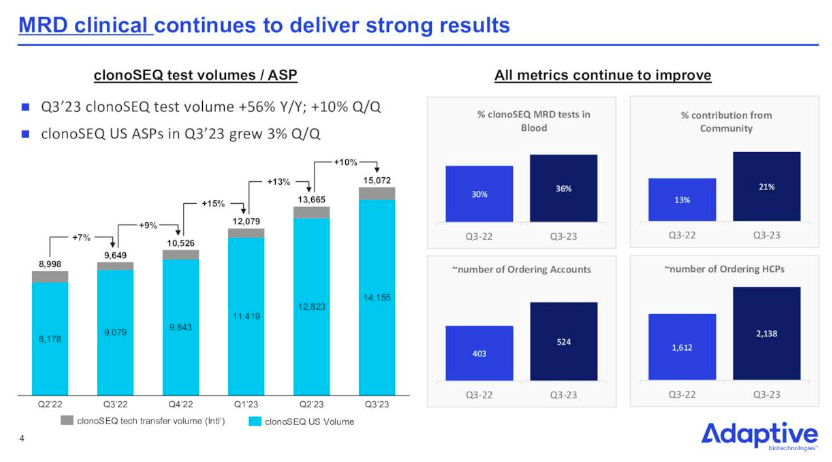

Central to the MRD segment's success is the clonoSEQ test, which has seen increasing clinical adoption. A 56% Y/Y growth in test volume in the third quarter of 2023, totaling 15,072 tests, signifies its emerging importance in cancer management. The clonoSEQ test's clinical utility and accuracy are critical in a field where precise diagnostics can greatly influence treatment decisions.

Adaptive Earnings Presentation

{kind=link}

The strategic direction of the MRD segment is further illustrated by Adaptive's collaboration with Goldman Sachs for a comprehensive strategic review. This initiative aims to maximize the value of both the MRD and Immune Medicine businesses. Such strategic considerations are essential in aligning Adaptive's investment strategies with the rapidly changing biotech market and technological landscape.

Adaptive's Q3 earnings report also revealed a broader picture of its financial health. The company's revenue for this period was $37.9 million, a 21% decrease from the same quarter in the previous year. This decline was driven by a reduction in GNE amortization and a decrease in MRD and Immune Medicine pharma services. Operating expenses were reported at $88.9 million, down from the previous year, but the net loss increased to $50.3 million, compared to $45.3 million in the same period in 2022.

The MRD segment's growth in this context reflects Adaptive's ongoing commitment to innovation, despite the inherent challenges of the biotech sector, such as high research costs and regulatory complexities. The company's focus on continuous advancement is key to keeping pace with scientific developments and maintaining a competitive edge in the market.

Financial Health

Turning to Adaptive's balance sheet , the total for 'cash and cash equivalents', 'short-term marketable securities', and 'investments' is approximately $371.1M, with $88.7M in cash and equivalents and $282.4M in marketable securities. The 'current ratio', calculated as current assets divided by current liabilities, is approximately 4.7, reflecting adequate short-term financial health. When comparing assets to debts, liabilities like accounts payable, accrued liabilities, and various long-term obligations (operating lease liabilities, deferred revenue, revenue interest liability) are significant, totaling around $356M.

Over the last nine months, Adaptive experienced a net cash used in operating activities of $129.4M, averaging about $14.4M per month. The cash runway can be estimated by dividing liquid assets ($371.1M) by the average monthly cash burn ($14.4M), yielding approximately 25.8 months. However, these values and estimates are based on past data and may not be entirely predictive of future performance.

Given the current cash runway and considering the rate of cash consumption, the likelihood of Adaptive requiring additional financing within the next twelve months appears medium.

In summary, Adaptive's short-term financial health can be characterized as adequate, but its long-term financial health seems more fragile, contingent on its ability to manage cash burn and potentially secure additional financing.

Market Sentiment

Adaptive's market capitalization of $718.07 million, combined with declining revenue growth and high debt, signals market doubt despite having a substantial cash reserve. Per Seeking Alpha, analysts project an increase in sales to $224.16M by 2024, indicating potential growth, but recent downward earnings revisions (6 down vs. 1 up) cast a shadow on these prospects. Stock momentum is weak, underperforming SPY significantly in all time frames over the last year, pointing to investor skepticism.

Short interest stands at 10.61%, a moderately high figure, suggesting a significant bearish sentiment. Institutional ownership is notable, with new positions (16 holders, 9,794,897 shares) outnumbering sold out positions (32 holders, 2,127,422 shares), indicating some institutional confidence. Prominent institutions include Viking Global Investors, Vanguard, and BlackRock, each holding substantial shares. Insider trades show a significant positive net activity over 12 months (1,261,755 shares).

Overall, Adaptive's market sentiment can be classified as "Mixed" (neither bullish or bearish) due to apparent differences of opinion between retail and institutional/insider investors.

My Analysis & Recommendation

In conclusion, Adaptive, with its focus on the MRD segment and clonoSEQ test, showcases a strategic pivot post-pandemic, highlighting its adaptability in a competitive and evolving biotech landscape. The MRD segment's robust performance, evident in the latest financial reports, stands as a beacon of potential amidst the company's broader challenges. However, Adaptive's journey is not without hurdles. The financial analysis reveals a delicate balance between current assets and liabilities, with a cash runway that may necessitate additional funding in the medium term. This scenario, coupled with mixed market sentiment and underwhelming stock performance, paints a picture of a company in a critical transformation phase.

Moreover, Adaptive's performance, as indicated by Seeking Alpha's Quant Factor Grades, does not present a compelling investment narrative.

Seeking Alpha

The stock's current valuation appears to have already factored in the decline in total revenues, alongside the growth observed in its MRD segment. A notable concern is the contraction in gross margins (Revenue - Cost of revenue / Revenue), dropping from 68.8% in Q3 2022 to 49% in Q3 2023. This trend underscores increasing cost pressures or inefficiencies in revenue generation. Additionally, the stock's momentum is lackluster, coupled with escalating net losses, further diminishing its attractiveness from an investment standpoint.

In light of the company's robust MRD segment and sound short-term financials, a "Hold" recommendation seems judicious for investors. However, caution is advisable due to potential concerns over long-term financial stability and lukewarm market reactions.

Investors looking to mitigate risks while holding Adaptive shares should consider a diversified biotech portfolio, spreading investments across companies with varying focuses and stages of growth. This strategy can help buffer against sector-specific volatilities. Furthermore, staying abreast of industry trends, regulatory changes, and Adaptive's performance metrics will be crucial in reassessing the investment as new data emerges. Lastly, setting strict stop-loss orders could help limit potential losses if the stock's performance deteriorates unexpectedly.

In essence, while Adaptive presents a compelling narrative through its MRD segment, investors should approach with caution, balancing optimism with a keen eye on the evolving biotech sector dynamics. This is one to watch moving forward contingent on the company turning a quick corner.

For further details see:

Adaptive Biotechnologies: MRD Success In A Challenging Market