CTRYY - Additional Headwinds Lie Ahead For TimkenSteel

2023-10-17 11:32:37 ET

Summary

- TimkenSteel stock receives a Hold rating due to uncertain short-term outlook for the company and the steel producers in general.

- The company's profitability has underperformed with lower sales and decreased EBITDA margins.

- Adverse macroeconomic and operational factors are expected to push the share price lower in the near future.

This Analysis Assigns a Hold Rating to TimkenSteel Corporation

This analysis confirms a Hold rating for shares of TimkenSteel Corporation ( TMST ) - a Canton, Ohio-based manufacturer, and distributor of alloy steel bars 16 inches or larger in diameter and seamless mechanical tubing and manufactured components in the United States and internationally - as the short-term outlook for this stock and the steel producers, in general, is still seen as quite uncertain.

With the previous "Hold" rating , the analysis assessed the impending downward pressure on the company's shares as profitability was seen to be affected by the following factors: expected lower shipping volumes and reduction in surcharges per ton.

Although the company has tried to support demand for its steel products with its customer backlogs and a gradual return to normality for its Faircrest plant in Ohio after the incident that caused injuries for 3 workers in July 2022, it has not been able to completely avoid the subsequent downtrend in its share price until early June 2023 due to the aforementioned sales shipment and surcharge headwinds to the company's profitability.

Indeed, the company's profitability has underperformed since the previous Hold rating: year-over-year net sales fell 27.5% to $245.4 million in Q4 2022 , fell 8.1% to $323.5 million in Q1 2023 , and fell 14.2% to $356.6 million in Q2 2023 . The lower sales were always due to the lower tons of steel shipped and a reduction in surcharges per ton.

Year over year, adjusted EBITDA fell 80.8% to $11.9 million in Q4-2022, it fell 44.9% to $36 million in Q1-2023, and it fell 40% to $50.5 million in Q2-2023.

Year over year, the EBITDA margin dropped 1,360 basis points (bps) to 4.8% in Q4-2022, it dropped 750 bps to 11.1% in Q1-2023, and the adjusted EBITDA dropped 1,180 bps to 14.2% in Q2-2023.

{kind=link}

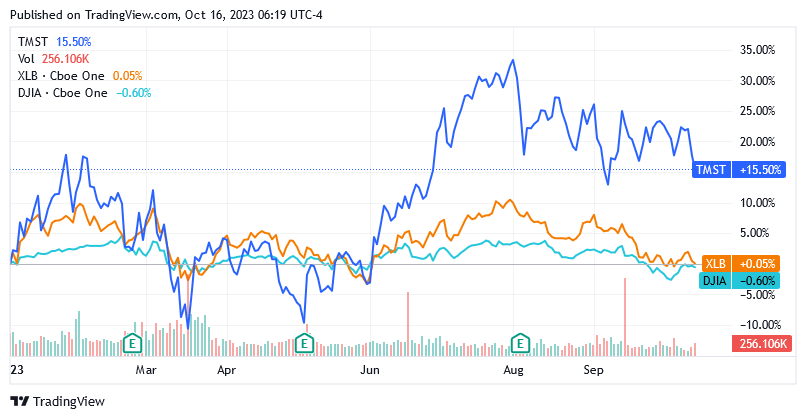

After early June 2023, shares of TimkenSteel Corporation, driven by a rise in the price of steel products benchmarked by the Trading Economics chart, have recovered some of the previous month's losses outperforming the DJI Dow Jones Industrial Average Index ( DJI ) and the Materials Select Sector SPDR ETF (XLB), and are now likely to be in the upper part of the stock price cycle. Shares of TimkenSteel Corporation appear highly responsive to bullish steel prices.

{kind=link}

The share price currently appears to be in the upper part of the cycle but is expected to reach significantly lower price levels due to adverse macroeconomic, geopolitical, and operational factors. Let’s see why.

TimkenSteel Corporation Profitability: What's Next?

As for the immediate future of TimkenSteel Corporation, the company's profitability is still expected to be severely tested by the following headwinds:

- Lower shipment volumes due to deteriorating consumer confidence , combined with weakening consumer demand in some key sectors such as construction, due to a gloomy outlook for refinancing applications and home buyers , and the lack of support for steel consumption from China. The economy of the Asian country and the world's largest steel consumer is paying for the financial problems of some key real estate companies such as China Evergrande Group ( EGRNQ ) and Country Garden Holdings Company Limited ( CTRYF ) ( CTRYY ) because they cannot meet their offshore obligations. The real estate sector is a mainstay of the Chinese economy.

- The need to keep the surcharge low may still be seen as necessary to support demand for its steel products in a difficult environment and be able to sell its most expensive inventory while steel prices still stay robust, as appeared to be the case recently . Although it does not sufficiently compensate for production costs and therefore affects profitability, the adoption of this strategy could be a signal that the company is not confident in the development of steel demand in the short term, but sees it weakening even further. If this happens, it would reinforce the negative trends of the past three quarters as follows: The company sold 177.5 thousand tons of steel products in the second quarter of 2023, compared to 208.9 thousand tons in the second quarter of 2023. The company sold 172.9 thousand tons in the first quarter of 2023 , compared to 196.4 thousand tons in the first quarter of 2022. The company sold in the fourth Q4 of 2022 128.3k tonnes , compared to 198.3k tonnes in Q4 of 2021.

Surcharges per tonne decreased to $586 in the second quarter of 2023 from $729 in the second quarter of 2022.

Surcharges per tonne decreased to $479 in the first quarter of 2023 from $553 in the first quarter of 2022.

Surcharges per tonne decreased to $425 in the fourth quarter of 2022 from $583 in the fourth quarter of 2021.

Steel sales price remained robust as base sales per ton developed as follows year-over-year: Base sales per ton was $1,423 in Q2 2023 compared to $1,261 in Q2 2022.

Base sales per ton were $1,392 in the first quarter of 2023 compared to $1,239 in the first quarter of 2022.

Base sales per ton were $1,488 in the fourth quarter of 2022 compared to $1,123 in the fourth quarter of 2021.

However, this tailwind from robust steel prices was not enough to prevent the deterioration in profitability illustrated above which resulted in a decline in the share price through early June 2023.

Subsequently, there was a recovery in the stock price due to renewed optimism among investors about an easing of interest rate tightening policy after the US Federal Reserve halted interest rate hikes at its June 14 meeting. But the Fed raised rates in July and said in September that the cost of money will remain high for a long time, which, combined with high inflation, will continue to impact demand prospects. Due to the continued unfavorable demand conditions and the lack of momentum in the recovery of the Chinese economy, an improvement in the profitability of TimkenSteel Corporation is far from expected, which will not have a positive impact on the share price in the coming weeks in my view.

Actually, there is a possibility of a further increase in the cost of money as the federal funds rate is expected to peak at 5.6% by the end of 2023 from the current 5.25% to 5.5% range, creating even more headwinds for the shares of TimkenSteel Corporation.

- In addition, the company's profitability continues to be weighed down by inflationary factors that make the supply of raw materials more expensive, particularly due to the ongoing conflict in Ukraine and the recent Hamas attack on Israel at the center of geopolitical tensions in the Middle East.

Year over year, production costs increased by $43.2 million in the fourth quarter of 2022, by $21.8 million in the first quarter of 2023, and by $15.3 million in the second quarter of 2023.

This increase in production costs is due not only to inflationary factors but also to the temporary inability of the company to absorb all fixed costs as the utilization of the smelters has not yet fully recovered (now it is about 75% against more than 80% before the Ohio incident) and the problem still requires the assumption of additional production recovery costs as well as maintenance and miscellaneous repair costs. Annual maintenance is also expected to weigh more heavily in the second half of 2023, at a fairly significant cost of $12 million.

However, while these higher facility costs should dissipate within one or at most two quarters, costs related to geopolitical or macroeconomic factors, such as renewed inflationary pressures, could continue to weigh on TimkenSteel Corporation's production costs for longer.

A Still Good Financial Condition

For the first six months, the US steelmaker reported a hard decline in free cash flow to $4.4 million in 2023 versus $54 million in 2022, as the aspects highlighted above caused its operations to produce less operating cash flow ($23.1 million in H1 -2023 compared to $64 million in H1-2022), while there was a slight increase in CapEx ($18.7 million in H1-2023 versus $10 million in H1-2022) to finance the integration of additional manufactured components machining lines.

Overall, the financial condition of TimkenSteel Corporation's balance sheet remains strong enough to support the recovery in asset utilization as all demand headwinds fade, China regains strength and even manufacturing costs have time to become significantly less burdensome than they are now.

As of June 30, 2023, total liquidity was $529.9 million, a slight increase from $490.7 million as of December 31, 2022 , enabling, among other things, the repurchase program of 650,300 shares of common stock at $17.53 per share in Q2-2023 and the repurchase of 514,000 shares of common stock at $18.29 per share in Q1 2023. As of June 30, 2023, the company had $52.2 million of its own common stock available for open-market repurchase.

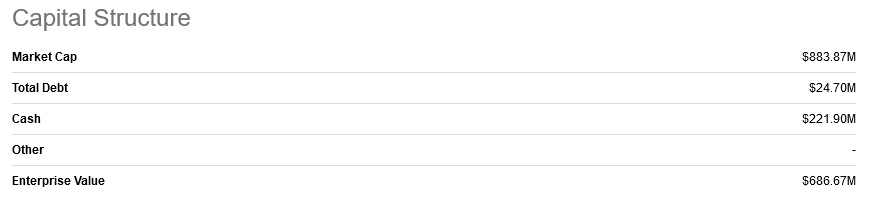

Total debt was only $24.7 million versus cash and equivalents and total short-term securities of $222 million, and the Altman Z-Score of 2.51 (scroll down this Seeking Alpha page to the "Risk" section) indicates a low risk of bankruptcy for the next few years.

The Stock Valuation

In light of the above and given that the stock price does not currently appear to be in the lower part of the cycle, this analysis suggests that investors should hold off on purchasing TimkenSteel Corporation shares for the time being.

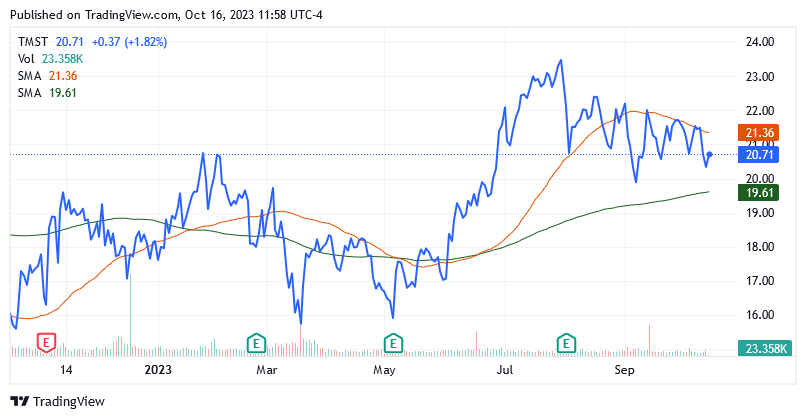

Instead, I assign a Hold rating as current unfavorable macroeconomic and operational factors are likely to push the share price in the lower part let’s say below the longer trend of the 200-day simple moving average line of $19.61. Currently, shares are well above that, but below the $21.36 value that sits instead on the 50-day simple moving average.

Shares were trading at $20.71 per unit giving it a market cap of $883.87 million as of this writing.

{kind=link}

Shares are also slightly above the middle point of $19.395 in the 52-week range of $15.30 to $23.49.

After the stock price reaches a level more in line with the company's profitability, it may also be worth adding to the stock in anticipation of the next upward steel price cycle, but for now, the Hold rating is the most suitable stance for this stock.

Now, shares have a 14-day relative strength indicator of 44.32x, which indicates they are neither oversold nor overbought, but there is plenty of room for shares to move lower and be more fairly priced than they are currently.

{kind=link}

Let's say a stock price of around $15.65 has a 14-day RSI of 30. This is the price I target to buy shares of TimkenSteel Corporation.

This price target also represents a correction from the price the company paid to redeem its own common stock in the first half of 2023, when the stock price formed its lower part of the cycle.

TimkenSteel Corporation has the following Enterprise Value (EV) equation: The EV of $686.67 million is equal to the market cap of $883.87 million plus total debt of $24.70 million minus cash of $221.90 million.

TimkenSteel Corporation has a 12-month adjusted EBITDA of $109.2 million. Thus, the EV/12-month adjusted EBITDA ratio is currently 6.29x.

{kind=link}

A 10% decline in the stock price to the target price of $15.65 implies an EV of approximately $476.22 million, as the market cap would be $673.42 million with approximately 43.03 million shares outstanding.

Then the EV/12-month adjusted EBITDA ratio would be 4.36x, which is almost in line with the annual estimate of 4.24x for 2023 by Aswath Damodaran, professor of corporate finance and equity valuation at New York University's Stern School of Business.

Holding shares in TimkenSteel Corporation until adjusted EBITDA reaches the desired multiple means a low risk that shares won't get cheaper than current levels, as a "higher for longer" hawkish stance on rates by the Fed really creates a depressive environment for the shares.

Conclusion

TimkenSteel Corporation's profitability continues to be threatened by various adverse factors, both macroeconomic factors that will impact demand for steel products and geopolitical factors that will impact production costs.

Moreover, operational activities are not yet up to standard after the incident in Ohio more than a year ago.

Currently, the shares have a valuation that does not appear to be particularly exploitable compared to the company's profitability, which is weakening under the weight of the factors highlighted, while the current share price is still in the upper part of the price cycle.

The conditions are in place for the market to form a more reasonable share price for this stock, and this analysis suggests not purchasing shares until current prices experience a contraction.

For further details see:

Additional Headwinds Lie Ahead For TimkenSteel