ATGE - Adtalem Global Education: Beat And Raise Initiate At Buy

2023-11-12 06:37:38 ET

Summary

- Adtalem Global Education is a leading provider of post-secondary education in the healthcare segment.

- The company reported strong Q1 earnings, driven by growth in the Chamberlain and Walden segments.

- Despite its strong performance, Adtalem trades at a slight premium to its long-term average and a discount to its peers, suggesting potential for further growth.

Investment Thesis

We ascribe a Buy rating on Adtalem Global Education ( ATGE ) on the back of

1) Stable enrollment trends at Chamberlain demonstrating improving outlook amongst students pursuing healthcare opportunities post the stress since the pandemic lead to several students dropping out

2) Favorable industry tailwinds with a huge shortage amongst the frontline health care workers

3) Margin expansion potential driven by improved utilization and higher enrollment at Walden

4) Comfortable valuation and strong earnings momentum providing favorable risk reward

Company Background

Adtalem Global Education ((ATGE)) is a leading provider of post-secondary education within the healthcare segment. It operates through three segments:

1) Chamberlain: Offering degree and non-degree programs in nursing and post-secondary healthcare through its Chamberlain university in Downers Grove, IL

2) Walden: Offers 100+ online certificates as well as bachelor's, masters and doctoral degrees across a wide range of segments including nursing, business, education, psychology, public administration, social work and public health

3) Medical and Veterinary: Offers degree and non-degree programs within medical and veterinary post-secondary industry through three universities with 2 located in Miramar, Florida and 1 located in Saint Kitts and Nevis

It has about 75k students across ~150 degree programs with more than 80% students focused in healthcare education

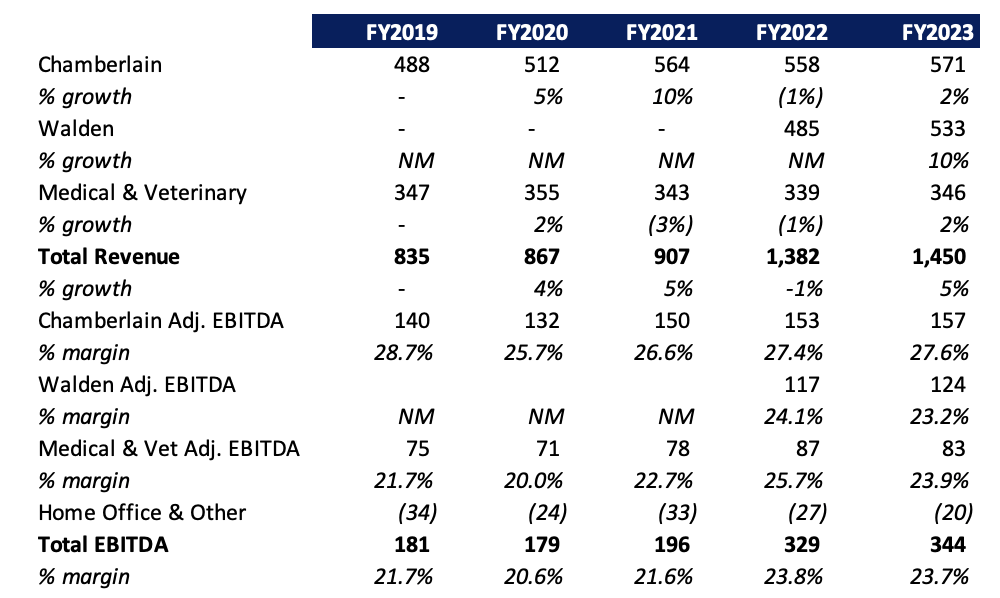

Historical Financials

The company reclassified its segments post the sale of its Financial Services segment comprising ACAMS, Becker, OCL and EduPristine entities for a consideration of $1bn . It also acquired Walden in early 2021 in order to bolster its online offering as well as create adjacencies in its course providing across behavioral health, public administration, psychology and others. ATGE reported a strong growth in FY21 driven by a jump in enrollments in Chamberlain as a result of the significant shortage of frontline healthcare workers in the wake of COVID-19. This was partially offset by a decline in the Medical and Veterinary segment as a result of lower housing and transportation revenue since most of the students started remote learning for the majority of the semester. However, enrollments soon dropped as healthcare workers dropped out post COVID-19 due to the subsequent stress on the healthcare professionals with growth primarily coming from tuition increases. The company embarked on a restructuring beginning 2022 including workforce reductions, cost cutting and real estate consolidation which enabled them to boost EBITDA margins by ~300 bps in Medical and Veterinary segment in FY 2022. However, continued decline in enrollment with higher marketing spends lead to a decline in operating margins for the segment in FY 2023. On a consolidated basis, the company managed to maintain its EBITDA margins as a result of real estate consolidation and lower rent expenses.

{kind=link}

Earnings Beat and Raise

ATGE reported a strong Q1 with revenues increasing 4% YoY to $369 mn, slightly ahead of the consensus estimates. The strong growth was driven by a 5.3% growth in revenues for Chamberlain segment along with a 8.2% growth in Walden partially offset by 3.8% decline in Medical and Veterinary segment. The growth in Chamberlain segment was driven by a strong 5.2% YoY growth in enrollment along with marginal benefit from tuition increases, marking the fifth straight quarter of enrollment growth evidencing stability in the enrollment trends.

{kind=link}

The robust growth in Walden segment remained the highlight for the quarter driven by a positive enrollment growth and higher utilization reaping the benefits off the marketing campaigns and management focus to differentiate the brand after years of decline. Tuition prices increased by ~6% YoY across the modules and courses which along with positive enrollment growth helped the company to deliver robust results marking the beginning of its turnaround.

{kind=link}

Medical and Veterinary enrollment trends continue to be volatile marking second straight quarter of decline facing tougher comparables with enrollment down 7.5% YoY, however, an increase in average tuition fees by ~3.5-4.0% aided the top line partly. The decline is lead principally by weakness in medical school which we believe will improve but likely pressured, while Veterinary school continues to be robust and operate at full capacity. Management expects to remediate the enrollment in medical schools through a capstone project to improved preparedness for USMLE exam, however, we believe while the step is in the right direction, it may not be able to stem the decline by a meaningful measure.

{kind=link}

Adj. EBITDA margins declined by 180 bps YoY to 21.8% primarily driven by decline in margins within Chamberlain and Medical & Veterinary segment partially offset by margin expansion in Walden. Chamberlain margins declined by 280 bps YoY while Medical and Veterinary margins declined by 210 bps YoY as a result of a jump in labor costs and higher retention expenses. EBITDA margins at Walden expanded by 260 bps YoY primarily on the back of higher utilization and pricing actions. In all, the company reported a non-GAAP EPS of $0.93, significantly ahead of the consensus estimated pegged at $0.81.

Balance sheet position remained strong with the company ending with a cash balance of over $260 mn and total debt outstanding of about $708 mn rendering a net leverage ratio of 1.3x. This provides further flexibility for the company to invest in growth areas and pursue opportunistic M&A activities.

ATGE raised its guidance for the year driven by strong quarter and continued earnings momentum with the company now anticipating revenues of $1.47 - $1.53 bn (vs $1.46 - $1.52 bn previously) and Adj. EPS of $4.25 - $4.45 (vs $4.20 - $4.40 previously) implying a conservative approach. We believe the company is likely to face tougher comps in Chamberlain going forward (Sep'22 enrollment growth was down 4%) and expect enrollment growth to retreat back to its 2% range. We believe Walden turnaround could be a bigger play which has been gradually improving and remain positively skewed on the segment driven by online capabilities which can drive higher utilization and margin expansion going forward. Medical schools remains the weakest link which has been declining since several quarters and we believe the enrollment trends will likely be pressured, however, certain tuition increases as evidenced historically can help them arrest top line decline.

Valuation

Despite the continued earnings momentum as well as 10%+ jump in stock price on the print, the company trades at just 12.8x at a slight premium to its long-term average of ~11.8x however, at a discount to its peer average of 17.3x.

We believe given the strong outperformance and improving visibility on the enrollment trends which could further drive earnings growth after several quarters of muted enrollments warrant a premium. We ascribe a 30% premium to its long term average and ascribe a target PE multiple of ~15.3x Fwd P/E (which is broadly in line with peer average excluding Strategic Education due to its higher growth premium) and Initiate with a Buy rating with a target price of $67.

Risks to Rating

Risks to rating include

1) ATGE generates about 72% of its revenues from Title IV programs and any reduction in government funding or its inability to be eligible for the programs due to change in regulations could adversely impact its operations

2) It operates in a highly regulated sector and its inability to maintain adequate standards and comply with regulations can significantly impact its business

3) ATGE operates in a highly competitive sector with 700 institutions offering RN to BSN programs (directly competing with Chamberlain), 300 schools in the US and Caribbean offering veterinary and osteopathic medicine courses (directly competing with its Medical and Veterinary segment) and Walden competing with a wide range of edtech players as well as other schools, universities and institutions

Conclusion

ATGE had been facing a temporary headwind as a result of higher number of frontline health workers dropping out due to the stress since the pandemic. According to a Mckinsey Survey , over 30% of registered nurses intended to leave their current direct patient care, up from 22% in Feb 2021. In addition, increasing number of retirements would lead to an ensuing shortage within the sector with about 1.2 mn gap currently. We believe the stable enrollment trends, growth within its online Walden segment on the back of improving utilization and strong industry tailwinds would continue to drive long term value creation.

{kind=link}

For further details see:

Adtalem Global Education: Beat And Raise, Initiate At Buy