ATGE - Adtalem: Growth From Medical Training Could Push The Price Up

2023-08-24 18:28:35 ET

Summary

- Adtalem Global Education is focused on capitalizing on the demand for medical training in the US.

- The company's business model includes segments in nursing and health professions, online courses, and medical and veterinary education.

- Adtalem Global Education has a solid balance sheet and potential for future growth, but faces risks from failed acquisitions and lower student attraction.

Adtalem Global Education Inc. ( ATGE ) appears to be making significant efforts to profit from the demand for medical training in the United States. I believe that further sale of assets and acquisition of new graduate and undergraduate courses in the nursing and health professions will continue in the coming years. Also, assuming further integration and creation of online programs will most likely have a beneficial effect on future FCF growth. I do believe that it may face risks from failed M&A, integration of new business models, or lower attraction of students. With that, I think that ATGE does trade quite undervalued.

Business Model

Adtalem is a US-based post-secondary education company focused on developing professionals for the healthcare industry.

Source: Investor Presentation

The operations of this company are divided into three segments: Chamberlain, Walden, and medical and veterinary segments. Chamberlain offers graduate and undergraduate courses in the nursing and health professions within the post-secondary education industry.

In the Walden segment, the activities of most recent acquisitions are integrated. This segment offers more than 100 certified online courses, degrees, and doctorates in a wide variety of areas such as education, labor relations, public administration, and health among others.

The medical and veterinary segment includes the American University of the Caribbean School of Medicine as well as Ross University Medical School, and offers degree courses for professionals in these industries.

In the last 10-k, management reported revenue growth in the three business segments, with increases in operating income in 2022 and 2023. Clearly, the business model appears to be quite successful. In my view, it is worth the attention of investors specialized in the education and healthcare industries, but also those who are not specialized in these industries.

Source: 10-k

In a recent presentation, Adtalem Global Education offered conservative revenue growth targets, including revenue growth close to 4%-6% CAGR as well as Adjusted EBITDA margin expansion for the year 2026.

Source: Investor Presentation

It is also worth noting that Adtalem Global Education reaffirmed its guidance in the last quarter, which includes net sales close to $1.4-$1.45 billion and adjusted EPS of about $4.05-$4.2.

Source: Investor Presentation

Balance Sheet

In 2022 and 2023, Adtalem Global Education sold several ACAMS, Becker Professional Education and OCL, Association of Certified Anti-Money Laundering Specialists, and EduPristine.

On March 10, 2022, we completed the sale of Association of Certified Anti-Money Laundering Specialists, Becker Professional Education and OnCourse Learning for $962.7 million, net of cash of $21.5 million, subject to post-closing adjustments. Source: 10-k

On June 17, 2022, Adtalem completed the sale of EduPristine for de minimis consideration. Source: 10-kOn March 10, 2022, Adtalem completed the sale of ACAMS, Becker, and OCL to Wendel Group and Colibri Group, pursuant to the Equity Purchase Agreement dated January 24, 2022. Pursuant to the terms and subject to the conditions set forth in the Purchase Agreement, Adtalem sold the issued and outstanding shares of ACAMS, Becker, and OCL to the Purchaser for $962.7 million, net of cash of $21.5 million, subject to certain post-closing adjustments. Source: 10-k

The company appears to be reshaping its portfolio to address the rapidly growing and unmet demand for healthcare professionals in the United States.

Source: Investor Presentation

As a result of previous sale of businesses, Adtalem Global reported a decrease in the total amount of assets driven by lower property and equipment as well as lower intangible assets. As of June 30, 2023, the company reported cash and cash equivalents worth $273 million, with accounts receivable of about $102 million, prepaid expenses and other current assets close to $100 million, and total current assets worth $478 million.

Besides, with property and equipment worth $258 million, operating lease assets close to $174 million, and deferred income taxes worth $56 million, intangible assets were equal to $812 million. Finally, with goodwill of about $961 million, total assets stood at $2.810 billion.

Source: 10-k

Adtalem Global Education reported lower net debt, which would most likely offer financial flexibility to acquire more businesses in the healthcare industry.

With accounts payable worth $81 million, accrued payroll and benefits close to $52 million, and accrued liabilities of about $105 million, long-term debt stood at $695 million. Besides, with long-term operating lease liabilities worth $163 million, total liabilities were equal to $1.353 billion. The asset/liability ratio stands at more than 2x, so I believe that the balance sheet is quite solid.

Source: 10-k

Cash Flow Model

I believe that further growth of its educational offer, the expansion of its presence at the national level, and the positioning within the offers of digital education and online courses will serve as revenue catalysts. As a result, I believe that we may see further improvement in the FCF growth.

Besides, I am quite optimistic about the growth to capitalize on the healthcare industry in the United States and online platforms. The education industry changed radically after the suspension of face-to-face activities in 2020, which led the company to seek digital alternatives as well as to increase the flow of offers on these platforms.

I am assuming that Adtalem Global Education will be able to acquire new businesses, integrate new teams, and correctly assess the valuation of new targets. In this regard, it is worth noting that Adtalem Global has done meaningful acquisitions in the past, like Walden for $1.488.1 billion.

Adtalem completed the acquisition of 100% of the equity interest of Walden for $1,488.1 million, net of cash and restricted cash of $83.4 million. Source: 10-k

As part of our strategy, we are actively considering acquisition opportunities primarily in the U.S. We have acquired and expect to acquire additional education institutions or education-related businesses that complement our strategic direction. Source: 10-k

Source: 10-k

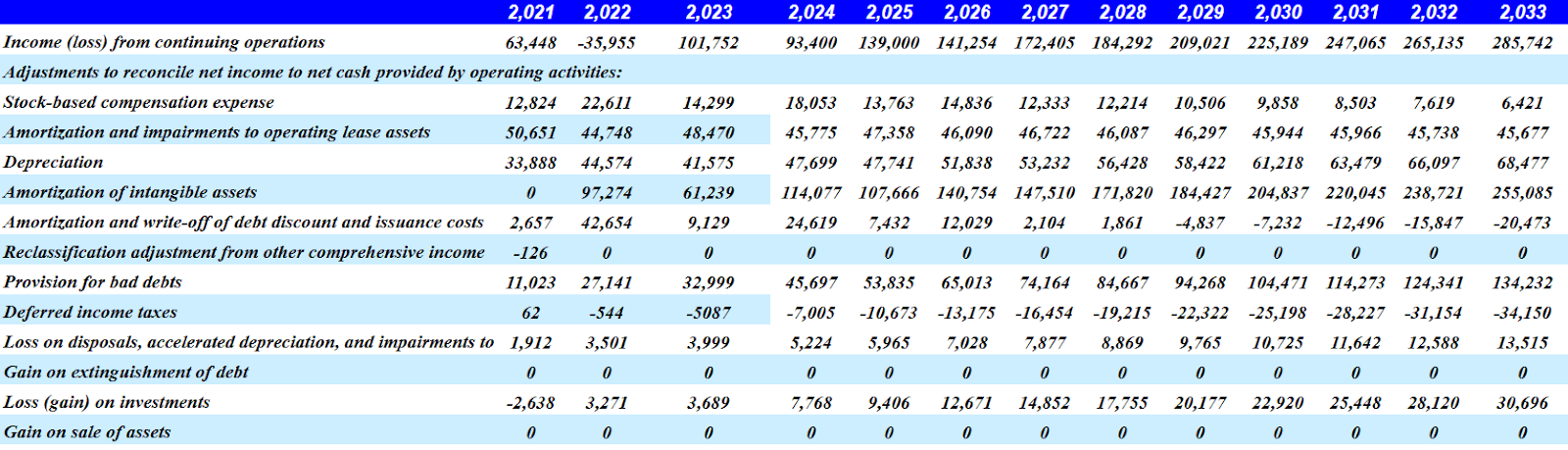

My cash flow statement forecasts included 2033 income from continuing operations close to $285 million, with adjustments to reconcile net income to net cash provided by operating activities including stock-based compensation expense of $6 million, amortization and impairments to operating lease assets worth $45 million, and depreciation of $68 million.

Besides, I also assumed amortization of intangible assets worth $255 million, amortization and write-off of debt discount and issuance costs close to -$21 million, no reclassification adjustment from other comprehensive income, and provision for bad debts worth $134 million.

Additionally, I took into account deferred income taxes worth -$35 million and accelerated depreciation and impairments to property and equipment close to $13 million, but no gain on extinguishment of debt and no gain on sale of assets.

{kind=link}

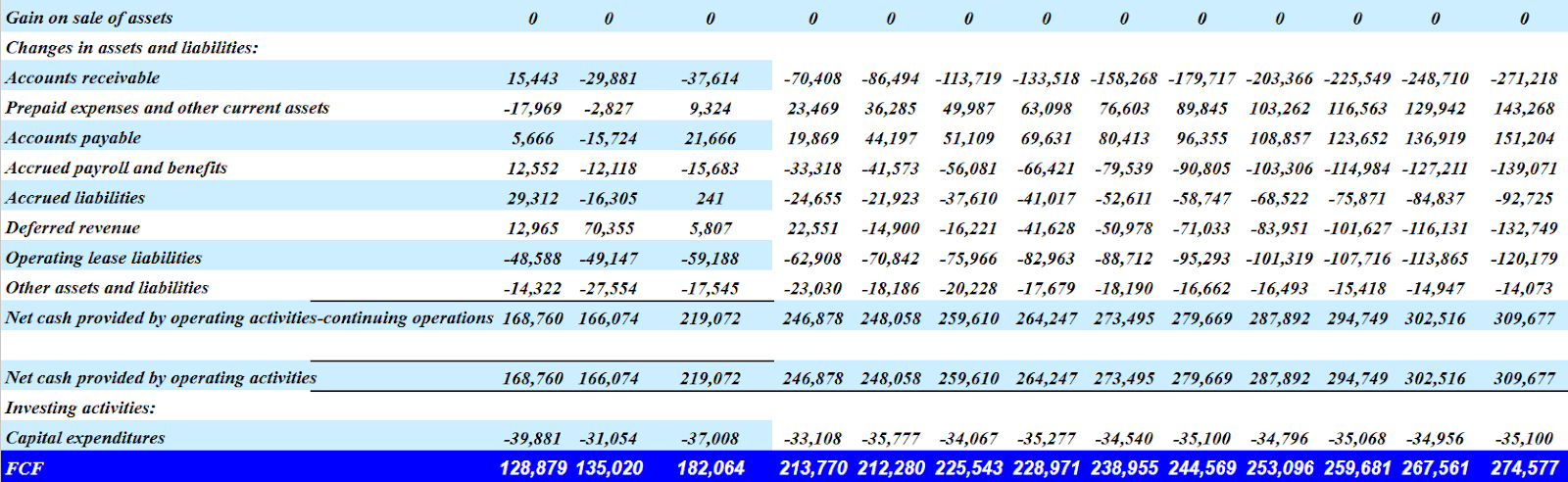

Additionally, changes in assets and liabilities included changes in accounts receivable of -$272 million, prepaid expenses and other current assets worth $143 million, changes in accounts payable of about $151 million, and changes in accrued payroll and benefits of about -$140 million.

Finally, with changes in accrued liabilities worth -$93 million, changes in deferred revenue of -$133 million, and changes in operating lease liabilities of about -$121 million, net cash provided by operating activities would be about $309 million. If we also assume 2033 capital expenditures of close to -$36 million, 2033 FCF would be $274 million.

{kind=link}

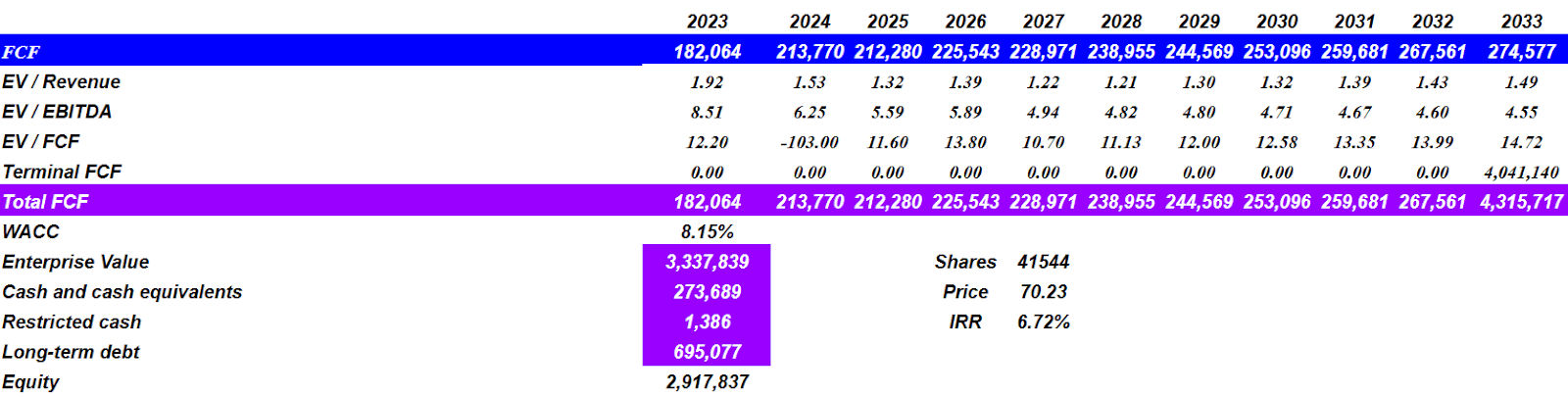

For the valuation model, I included EV/FCF of 14.7x with total FCF of about $4.315 billion and a WACC of 8.15%, which implied an enterprise value of about $3.337 billion.

Also, adding cash and cash equivalents worth $273 million, restricted cash of $1 million, and long-term debt close to $695 million, the implied price would be $70.23 per share, and we would be talking about an internal rate of return of 6.72%.

{kind=link}

Considering the implied fair price that I obtained, I understood a bit more the aggressive share repurchases that the company undertook in 2023. I believe that further acquisition of shares would most likely have a positive effect on the stock price.

As of June 30, 2023, $172.7 million of authorized share repurchases were remaining under this share repurchase program. The manner, timing and amount of any share repurchases may fluctuate and will be determined by us based on a variety of factors, including the market price of our common stock, our priorities for the use of cash to support our business operations and plans, general business and market conditions, tax laws, and alternative investment opportunities. Source: 10-k

Competitors

Each of the segments varies in its competence due to the type of professional training it offers. In the field of nursing, there are currently more than 2,000 educational centers in the United States that offer certified degrees as well as other 700 educational centers that offer graduate degrees in nursing. Chamberlain competes in this segment, and according to AACN statistics, it was the institution with the most enrollments in US-based programs for some of the educational categories.

The stiffest competition exists for Walden, which competes with a wide variety of local education offerings and globally through digital platforms. This segment grew particularly when the educational offer for professionals under 25 years of age was underdeveloped, and the company was able to position its courses as value contributions in that market. Currently, competition has grown, and entry conditions are lower than before, therefore as we have seen, student enrollment in this segment is lower year after year.

Lastly, the Medicine and Veterinary segment exists in an environment of around 150 medical schools nationwide, 48 schools of osteopathy, and 40 schools in the Caribbean. It is the industry that has experienced the most expansion in recent years.

Risks

There are a series of risks associated with the legal conditions to practice within the educational industry in the United States and the validation of degrees offered that affect the company, specifically in the legal disputes that are currently underway, the resolution of which could affect the company recognition. In addition, it could affect the relationship of the company's institutions with the economic provisions provided by public institutions.

On the other hand, the ability that the company has to attract new clients, the future of the students trained by its institutions, and the place that professionals can occupy in the industry are key factors in the continuity of the business and the attraction of students. Of course, this factor is also subject to global economic conditions and the segment of the population that can access paid education for their professional training.

Finally, we can add that the integration and selection of future acquisitions as well as the risks arising from expansion into new international markets.

Conclusion

Adtalem Global Education recently made an impressive sale of assets to profit from the growing and unmet demand for healthcare professionals in the United States. With a solid balance sheet and a recent decrease in the net leverage ratio, I believe that we can expect new inorganic growth acceleration in the coming years. Besides, if the company successfully invests more money in online platforms, we may also see further improvements in the FCF margin growth. I did identify risks from failed acquisition, integration of new teams, failed attraction of online and offline students, or lower revenue than expected. With that, I think that Adtalem Global Education appears undervalued.

For further details see:

Adtalem: Growth From Medical Training Could Push The Price Up