ADTTF - Advantest: The AI Hype Is Here (Rating Downgrade)

2023-05-30 07:43:06 ET

Summary

- Advantest Corporation's stock price has increased by 56% in the past three months, possibly partly due to the AI hype and Nvidia's recent Q1 FY2024 earnings report.

- The company's Q4 FY2022 earnings report showed revenue growth but declining margins, and FY2023 guidance predicts a decline in revenue and net income.

- I believe Advantest might still be fairly valued at around ¥15,000 ($106.98) per share, but with the current price exceeding this number, I have to change my rating from strong buy to hold.

Introduction

I initiated coverage of Advantest Corporation (ATEYY)(ADTTF) in my article from February 28, 2023, called "Teradyne And Advantest: A Duopoly In The Semiconductor Value Chain". I planned on writing a dedicated article on both companies around year-end when the major effects of the downturn in the semiconductor test market have played out and guidance for 2024 starts. However, market volatility forces me to update my stance regarding Advantest from a strong buy to a hold rating.

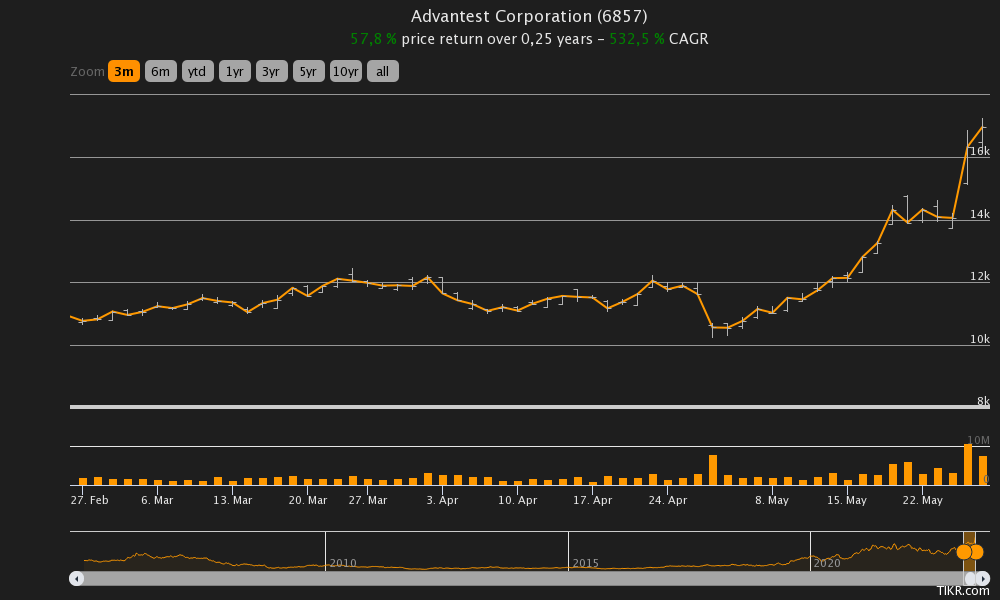

Back then, I started coverage on Advantest with a strong buy rating at the price of ¥10,930 ($77.95) per share. With the stock trading at ¥16,980 ($121.10) right now, it delivered around 56% returns in a matter of just three months, as can be seen in the following snippet from my initial article:

ATEYY Performance since last article (Seeking Alpha)

In this article, I want to go over the recent Q4 FY2022 earnings report and what may have been the catalyst for the major rerating that took place over the past couple of months.

Q4 FY2022 Earnings Report

Advantest reported Q4 FY2022 and FY2022 earnings on April 26, 2023. In my initial article, I stated that earnings are expected to grow in Q4 and guidance for FY2023 is expected to be bad because of the overall downturn in the semiconductor test market.

For Q4, revenue grew from ¥116.8 billion to ¥147.4 billion (+26.2%) while net income grew from ¥26.4 billion to ¥30.6 billion (+15.9%). Meanwhile, margins declined on every level (gross margin, operating margin, net margin).

For the full year 2022, revenue grew from ¥416.9 billion to ¥560.2 billion (+34.4%) while net income grew from ¥87.3 billion to ¥130.4 billion (+49.4%). FY2022 set a new record regarding margins on every level.

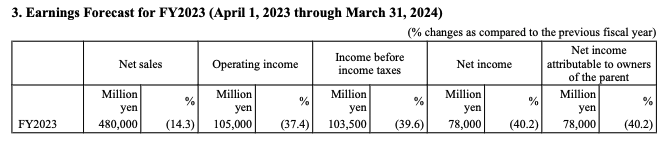

With margins declining in Q4, we can already guess where margins are headed over the near term. Here is the FY2023 guidance that Advantest issued in their latest earnings release:

{kind=link}

Revenue is expected to decline by 14.3% to ¥480 billion while net income is expected to decline by 40.2% to ¥78 billion. Advantest is guiding for a net margin of 16.25% compared to 23.28% in FY2022. We haven't seen this kind of margin level since FY2017. The past five-year average net margin comes in at 21.22%.

I think that the guidance looks far worse than it is. According to the Q4 FY2022 Q&A session :

While we expect the size of the market to be down in 2023, we are hoping that in 2024 it will be equal to or greater than that of 2022.

Source: Advantest Investor Relations - Q&A Summary

While Advantest expects the semiconductor test market to decline for the second year in a row, they also "hope" that the market will recover to FY2022 and above levels by FY2024.

If I interpret Advantest's comments correctly, there should also be some upside to the issued guidance. Here is what Advantest said regarding the sales forecast:

We formulated our sales forecast from the bottom up based on information compiled from our sales team in January and February. We believe that we will be able to maintain market share and do not rule out the possibility of upside, but please take our forecast as our best guess considering that we do not have clear visibility on when the market will bottom out.

Source: Advantest Investor Relations - Q&A Summary

When the forecast is based on information from the middle of a market downturn, shouldn't this be the worst-case scenario? I think there is a good possibility that Advantest will be able to increase guidance throughout the year when visibility starts to improve.

In conclusion, I can only repeat what I stated in the risk section of my initial article. While the overall market (semiconductor market) is expected to grow, it remains a cyclical market. This cyclicality can affect the company to the upside and downside.

Currently, we are right in the middle of a downturn. If we look at the price performance of Micron Technology (NASDAQ: MU ), the textbook example of a cyclical company in the semiconductor space, we can see that MU stock seems to have bottomed out in the high forties (close to book value) and started to rise since then despite reported earnings deteriorating. In the case of Advantest, it seems that the market is already looking beyond FY2023 and expects a major recovery in revenue and margins in FY2024.

The AI Hype

While the conclusion above might explain some of the share price performance over the past three months, it doesn't explain this:

{kind=link}

On April 26, 2023, the stock dropped from ¥11,620 ($82.87) per share to ¥10,550 ($75.24) per share, so the initial reaction to earnings and guidance was negative. Right after that, the price only knew one way: up. I guess that this is due to the current hype around AI. I looked through the latest earnings transcripts of the two major AI behemoths Microsoft (NASDAQ: MSFT ) and Alphabet (NASDAQ: GOOG ) (NASDAQ: GOOGL ). In both Microsoft's and Alphabet's latest earnings calls, the keyword AI was mentioned above 60 times.

On May 24, 2023, Advantest traded at ¥14,060 ($100.27) per share. This was the day Nvidia (NASDAQ: NVDA ) reported Q1 FY2024 earnings . Nvidia jumped over 25% on the earnings release. In the two days following Nvidia's earnings release, Advantest jumped from ¥14,060 to the current ¥16,980 ($121.10) per share.

So what is the narrative here? Big tech behemoths like Microsoft, Alphabet and Amazon want to integrate AI into every aspect of their business. They will need loads of chips/GPUs for their data centers. These will be bought from Nvidia hence Nvidia's incredible revenue guidance. Nvidia's chips will have to be manufactured and tested in the process. These tests will be performed with Advantest's test equipment.

I don't know about you but this doesn't seem like a long-term investment case to me. The semiconductor market is still expected to grow 6-8% annually until 2030 . Nvidia being able to report a couple more billion $ in revenue doesn't mean that semiconductor production capacity will magically increase. Advantest's customers are the likes of Taiwan Semiconductor Manufacturing Company (NYSE: TSM ), Intel (NASDAQ: INTC ), Samsung Electronics ( OTCPK:SSNLF ) and the aforementioned Micron (besides many others). Advantest is an investment into the growing semiconductor market as a whole, not into some kind of AI fantasies.

Valuation

With 184,214,039 shares outstanding and a per-share price of ¥16,980 ($121.10), Advantest is trading at a market cap of ¥3.13 trillion ($22.31 billion). After deducting net cash of ¥34.7 billion ($247 million), the enterprise value amounts to around ¥3.09 trillion ($22.06 billion). With net income for FY2022 coming in at ¥130,400 million, Advantest is trading for around 24 times FY2022 earnings right now.

With companies like Advantest, it is hard to perform a DCF valuation because earnings fluctuate due to the cyclicality of the business. In my last article, I estimated Advantest to be fairly valued at ¥14,783 ($105.43) per share. In my opinion, the overall prospects for the business haven't changed that much since then. The price-to-earnings ratio will be high for FY2023 due to the current downturn in the semiconductor test market but I expect a strong recovery in FY2024 (this would also be in line with what the management of Tokyo Electron ( OTCPK:TOELF ) ( OTCPK:TOELY ), another major semiconductor equipment manufacturer from Japan, said in their Q3 FY2023 Q&A session - see my article from January 27, 2023 ).

Adjusted for the cyclicality of the business, I think Advantest might still be fairly valued at around ¥15,000 ($106.98) per share. With the price currently clearly exceeding this number, I will have to change my stance to hold for now.

Conclusion

Advantest shares rerated over the past three months, resulting in a 55%+ gain over a very short time period. The initial reaction regarding the Q4 FY2022 earnings report was negative. The stock only started to climb after this initial negative reaction.

The current hype around AI and Nvidia's recent Q1 FY2024 earnings report seem to have sparked some AI hype that also reached Advantest's share price. This can be seen by the reaction of Advantest's share price right after Nvidia's earnings report.

In my opinion, the overall outlook for Advantest and the quality of the business haven't changed that much since my initial article from February 28, 2023. I still think Advantest might be fairly valued in the ¥15,000 ($106.98) per share range. With the stock currently trading clearly above this number, I have to change my rating from strong buy to hold for now. I think there will be better opportunities to buy Advantest in the future, maybe towards the end of the year when reality sets back in and Advantest reports results as they have guided: declining.

For further details see:

Advantest: The AI Hype Is Here (Rating Downgrade)