ATEYY - Advantest: The Semiconductor Test Market Seems To Recover In CY2024

2023-11-06 00:24:39 ET

Summary

- Advantest's reported earnings deteriorated for the first two quarters of FY23, with earnings for the first half of the FY down 60%.

- The stock market has not followed the decline in earnings because it looks beyond the currently challenging market environment for the semiconductor test market.

- According to Advantest and its main competitor Teradyne, the semiconductor test market seems to start recovering in CY24.

- While growth drivers are still intact, I will have to reiterate my "hold" rating on Advantest.

Introduction

I wrote my last update on Advantest ( OTCPK:ATEYY ) ( OTCPK:ADTTF ) called " Advantest: The AI Hype Is Here " back on May 30, 2023. After initiating coverage on Advantest in my first article from February 28, 2023, with a "strong buy" rating, I had to downgrade my rating to "hold" because the stock had already appreciated 50+% in a matter of three months due to the AI hype around that time.

For reference, here is my conclusion from my last article in May:

Advantest shares rerated over the past three months, resulting in a 55%+ gain over a very short time period. The initial reaction regarding the Q4 FY2022 earnings report was negative. The stock only started to climb after this initial negative reaction.

The current hype around AI and Nvidia's recent Q1 FY2024 earnings report seem to have sparked some AI hype that also reached Advantest's share price. This can be seen by the reaction of Advantest's share price right after Nvidia's earnings report.

In my opinion, the overall outlook for Advantest and the quality of the business haven't changed that much since my initial article from February 28, 2023. I still think Advantest might be fairly valued in the ¥15,000 ($106.98) per share range (Author's note: These were prices before the 4 for 1 stock split in September) . With the stock currently trading clearly above this number, I have to change my rating from strong buy to hold for now. I think there will be better opportunities to buy Advantest in the future, maybe towards the end of the year when reality sets back in and Advantest reports results as they have guided: declining.

Source: Author's article from May 30, 2023

In this article, I want to update you on what happened since then. Specifically, I will go over the performance since my last article, the results that have been reported since then and some more information I gathered after starting coverage on the company. If you are new to Advantest, I highly suggest reading my initial article, which I linked above, first. I usually cover much ground when I first write about a company so I can refer readers back to my initial coverage to get a good overview of the business and its underlying markets.

Performance since the last article

First of all, I have to say that Advantest did a 4 for 1 stock split in September. So I will just adjust all past numbers to reflect the split. The last time I covered Advantest it traded at ¥4,245 per share ($30.27 per ADR at the then-current exchange rate, ATEYY on the Tokyo Stock Exchange. Advantest currently trades at ¥3,949 per share ($27.47 per ADR), so the stock declined a bit under 10% in the past five months. With the S&P 500 being up around 3% since then, Advantest underperformed the broader market.

With that being said, let's take a look at how the company performed fundamentally since then. Advantest released two earnings reports in the meantime, Q1 23 and Q2 23. Since Advantest's FY ends in March, these two reports are equivalent to Q2 23 and Q3 23 on a calendar year basis. I will just throw both reports together and compare them to the prior six-month period. Here is the result (in ¥ million):

| Results |

| Q2+Q3 22 |

| Q2+Q3 23 |

| YoY |

| Revenue |

| 274,806 |

| 217,511 |

| -20,8% |

| EBIT |

| 87,916 |

| 35,269 |

| -59,9% |

| Net Income |

| 71,161 |

| 25,938 |

| -63,6% |

| Free Cash Flow |

| 36,659 |

| -10,242 |

| n.n. |

While revenue declined by 20%, earnings declined sharply, With EBIT and Net Income declining by around 60% YoY and Free Cash Flow ((FCF)) turning negative.

This also shows in Advantest's guidance. Here is another table showing the company's guidance back in April compared to the guidance that was issued this week (in ¥ million):

| Guidance |

| April |

| October |

| Revenue |

| 480,000 |

| 470,000 |

| EBIT |

| 105,000 |

| 80,000 |

| Net Income |

| 78,000 |

| 60,000 |

While the revision of the revenue guidance is negligible, the effects on the bottom line are massive. According to Advantest's management, the reason for this is a perfect storm of (1) product mix headwinds, (2) declining sales and (3) currency impacts.

So in conclusion, the current business environment in the semiconductor test equipment market is terrible. However, the stock hasn't nearly declined as much as earnings did. This is because the market is forward-looking. Let's take a look at why the market might behave as it does.

Market Environment and Size

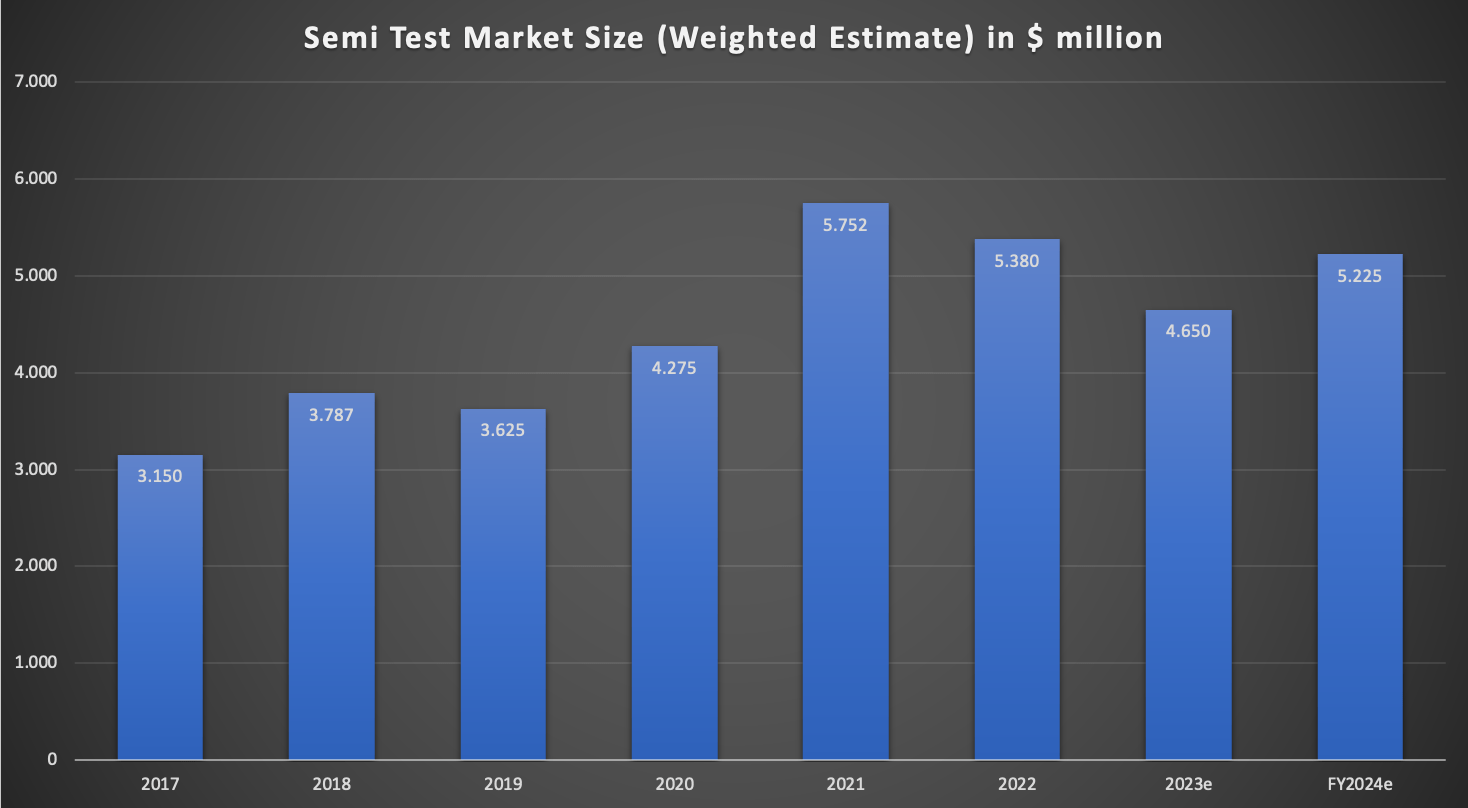

I looked through Advantest's and its main competitor Teradyne's (NASDAQ: TER ) past earnings presentations and earnings calls to see what kind of market size they were estimating for the semiconductor test market. I took the estimates of both companies and divided the sum of them by two to get an adjusted estimate for the total market size. Here is a chart showing the result:

Semiconductor Test Market Size since 2017 (Company reports/earnings calls - Compiled by Author)

{kind=link}

We can see that the test market is growing, albeit with quite some volatility. I need to highlight that both companies have not clearly stated their views on the CY2024 market size at the moment. Teradyne only hinted in the latest Q3 23 earnings call that units will be at or a bit below 2022 levels in 2024 while increasing complexity will drive test capacity requirements. Advantest said in their latest Q2 23 earnings call that FY2023 is the bottom they estimate that FY2024 will be at the level of FY2022 or a bit below. Throwing both statements together, I estimated that the market size might come in at around $5.225 billion, $175 million below the 2022 level.

With my assumption, the growth CAGR from 2017 to 2024 would come in at around 7.5% per year. This is in line with McKinsey & Company's estimate that the overall semiconductor market will grow with a CAGR of 6-8% until 2030. I highlighted this McKinsey report in my initial article where I started coverage on both Advantest and Teradyne. The market is volatile but at the end of the day, it is a market with a clear growth trend.

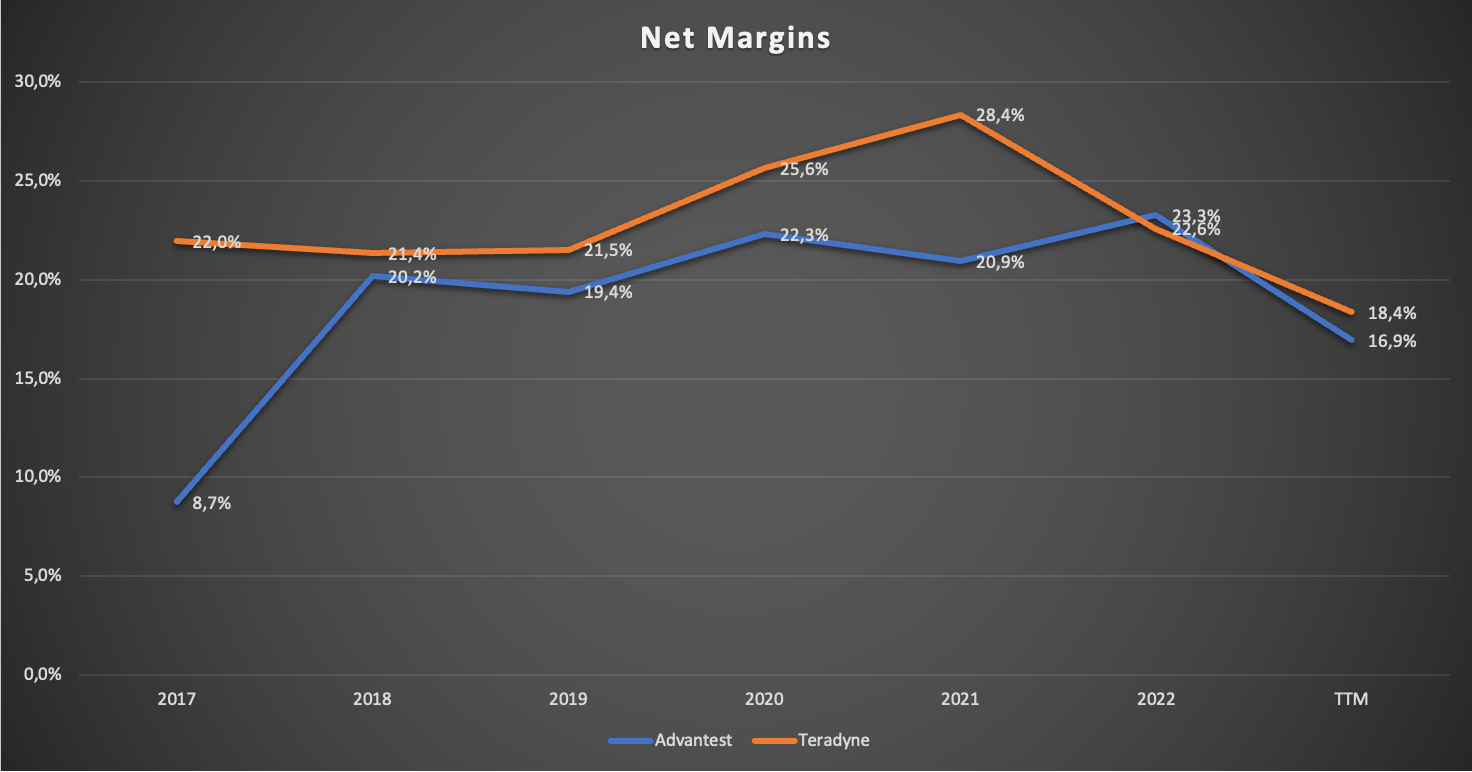

Now why is this so important? The answer is that the margins of both companies are tied to the short-term trends of the overall semiconductor test market. Here is a chart showing the net margins for both companies since FY2017 (note that Advantest's FY ends three months after Teradyne's which distorts this a little bit):

Net Margins since FY2017 (Company reports - compiled by Author)

{kind=link}

We can see the trend of improving margins over time until 2021. In 2019 and 2022/2023, the margins declined with the decline in the overall market size. If the market size recovers in FY2024 (as both companies expect), we should see margins increase sharply over the next years. With Teradyne and Advantest accounting for 95+% of the semiconductor test equipment market, I think that the estimates from both companies are quite trustworthy, especially when they both offer the same outlook.

While we are at it, let me talk a bit about the market share.

Market share

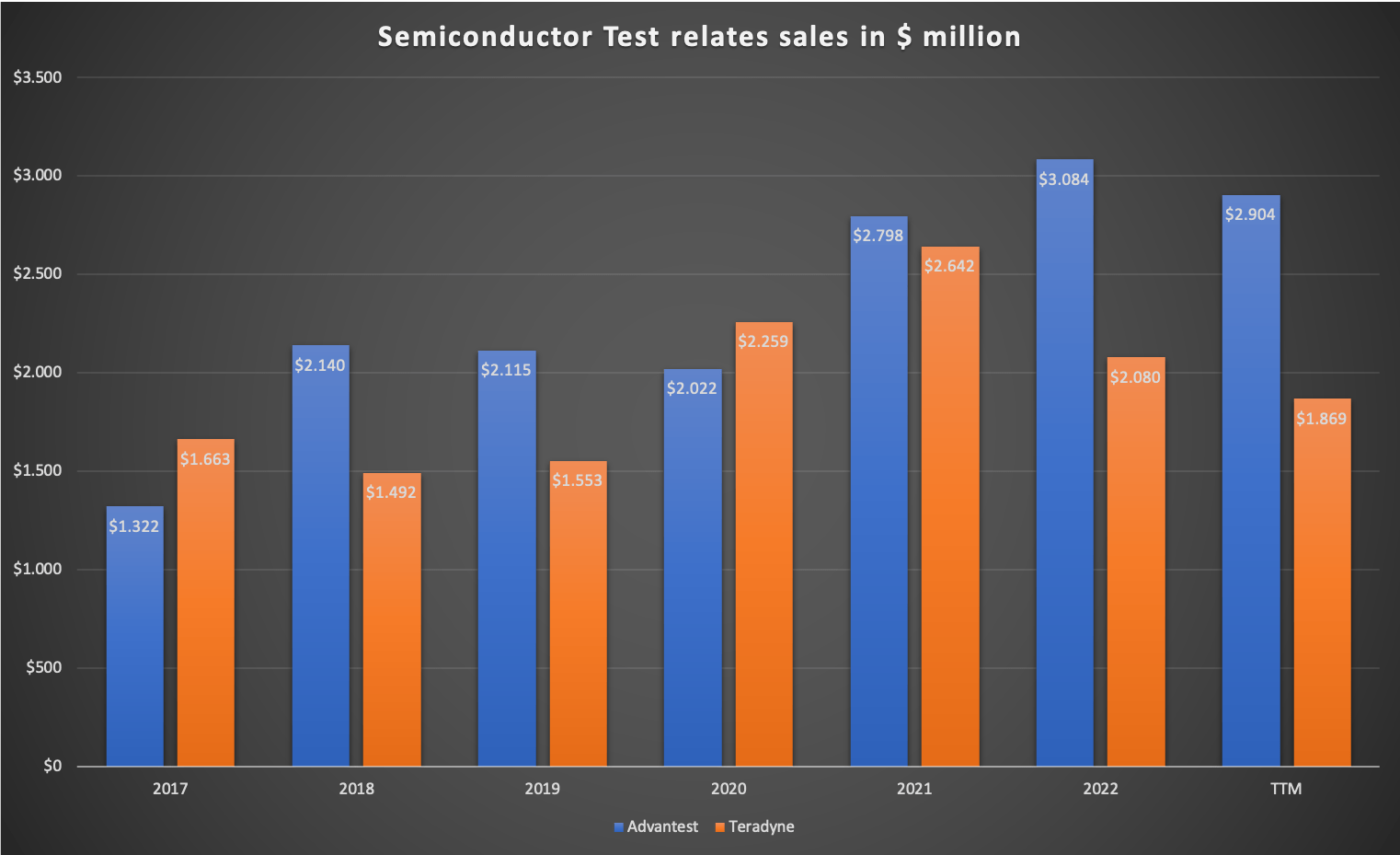

Advantest and Teradyne account for 95+% of the semiconductor test equipment market. I dug through past earnings releases and presentations to gather data regarding both companies' semiconductor test-related sales. Here is a chart showing the result:

Semiconductor Test related sales since 2017 (Company reports - compiled by Author)

{kind=link}

Overall, Advantest had slightly more sales than Teradyne over the whole timeframe since 2017. Teradyne's test-related sales only surpassed Advantest in 2017, 2020 and 2021. Meanwhile, Advantest's revenues have seen much more resiliency over the recent past.

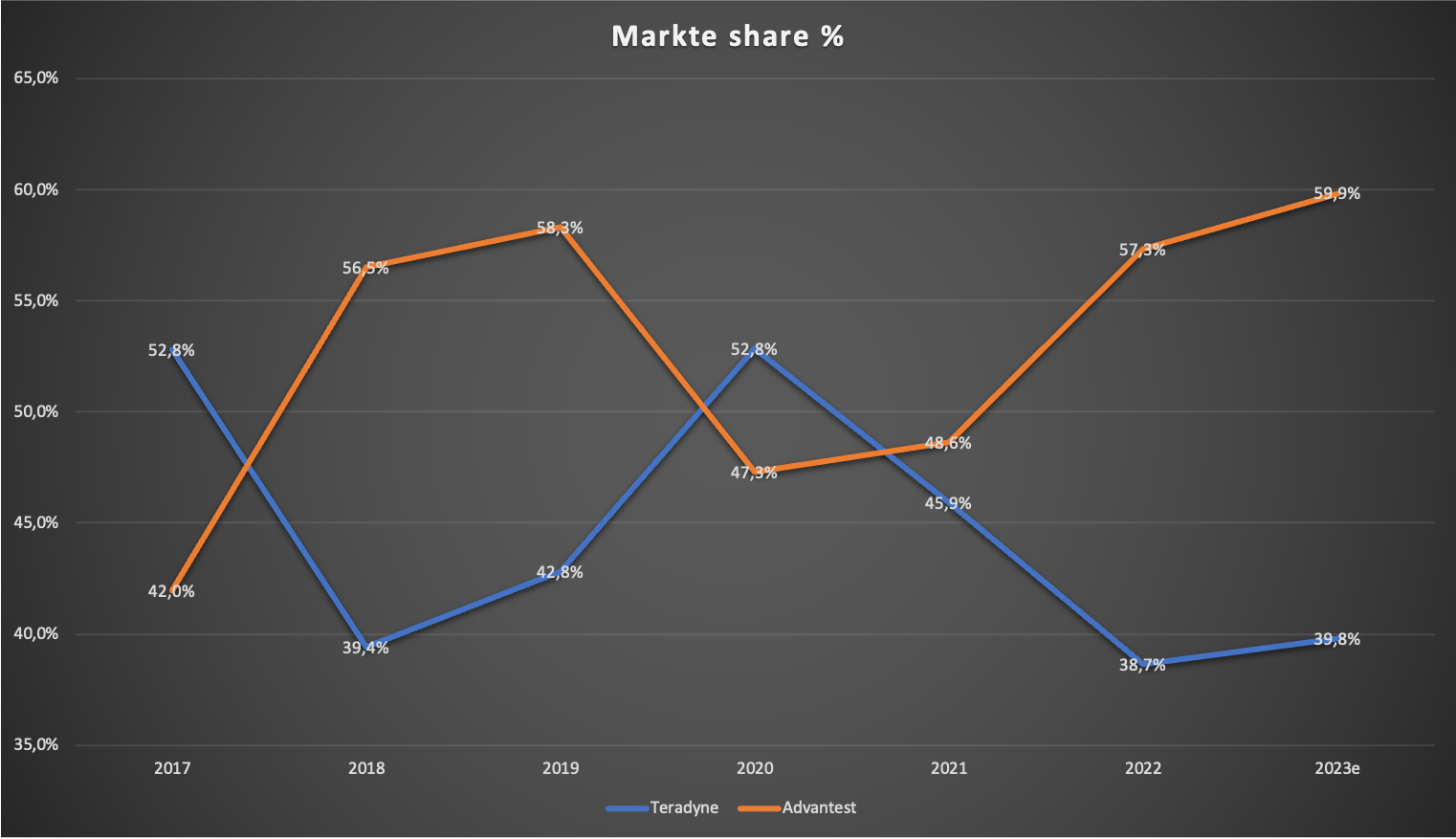

Next, I set these sales in relation to the aforementioned overall market size estimates, resulting in market shares. Here is the result (note that due to inaccuracies, some years don't add up to exactly 100%):

Semiconductor Test market share (Company reports - Compiled by Author)

{kind=link}

Here we can see that excluding the boom years 2020 and 2021, Advantest's market share has been pretty stable at a bit below 60% in the past few years. Teradyne's market share hovered around 40%, again excluding 2020 and 2021. In the Q3 23 earnings call, Teradyne said it expects that its overall market share will be flat to slightly up next year. So it seems that this 60/40 market share distribution will remain unchanged in 2024.

Long-term Outlook

Regarding the long-term outlook, I can only repeat what I said earlier. I think that the semiconductor test market will grow in line with the overall semiconductor market. As I mentioned earlier, McKinsey estimates the semiconductor market to grow with a CAGR of 6-8% into a $1 trillion industry. More semiconductors need more testing. The increase in complexity with the transition to smaller nodes might be an additional tailwind. Advantest seems to use the same assumptions, as can be seen on the last slide of the IR Technical Briefing presentation from December 7, 2022. Teradyne on the other hand reiterated its stance on the long-term outlook for the test business in the most recent Q3 23 earnings presentation (slide 14). Teradyne expects the growth to continue on the 9% trendline from 2016, or 7-11% off of the 20/21 average, a bit higher than my assumptions. Maybe Teradyne includes some market share gains in their assumptions.

Valuation

In my last update, I wasn't confident enough to perform any kind of DCF calculation because the visibility regarding earnings was very limited. With the new comments from both companies' management regarding test market size for FY2023 and FY2024e, I think we can try to do some calculations now.

Advantest currently has 738,128,556 shares outstanding at the current price of ¥3,949 per share ($27.47 per ADR), so the current market capitalization amounts to ¥2.915 trillion ($19.5 billion). The net cash position stands at ¥5.75 billion ($38.5 million) so the Enterprise Value (EV) comes in at ¥2.909 trillion ($19.1 billion).

Now we need to make some assumptions for the future. Let's assume that revenue and margins are 100% tied to the test market size. I outlined earlier that I estimate the CY2024 market size to come in at around $5.225 billion compared to $5.38 billion in CY2022. This would be 97% of the CY2022 market size. If we tie revenue to market size, FY2024 revenue should come in at around ¥543 billion (97% x ¥560 billion, FY2022 revenue). Since the first quarter of CY25 counts toward Advantest's FY24, the actual number should be slightly higher. This is nearly in line with the Analyst estimates for FY24 which project revenue of ¥555 billion (Source: Tikr/S&P Capital IQ). As I highlighted earlier, margins are tied to market size and revenue. FY22 net margin came in at 23.28% (off of ¥560 billion revenue) so I think a 23% net margin for FY24 is optimistic but not impossible. In this scenario, FY24 net income would come in at around ¥127.6 billion. So Advantest would be trading at 22.8 times FY24 earnings right now which is neither cheap nor expensive in my opinion.

Now we need to gauge a sustainable rate of cash conversion (FCF as a percentage of revenue) so we can calculate a normalized FCF yield. This is not so easy in this case because the FCF is pretty volatile. Cash conversion is expected to exceed 100% (according to Analyst estimates) in FY24 and FY25. This seems to make sense since cash-conversion was pretty low in FY22 and FY23 because Advantest couldn't sell their inventories, as we can see in the following chart:

{kind=link}

Inventories skyrocketed in FY22 and currently stand at ¥198 billion, so we can conclude that the cash conversion numbers of these two fiscal years are outliers and have to be excluded if we want to calculate "normal" cash conversion numbers. Excluding these two fiscal years, cash conversion came in at 82% for FY16-FY21.

Now we can put it all together. I assume an FY24 net income of ¥127.6 billion. With an average cash conversion of 82%, FY24 FCF would be around ¥105 billion. So Advantest is trading at a normalized 3.6% FCF yield on FY24 numbers right now, a rather high multiple for a business that is "only" growing at around 6-8%.

If we combine the FCF yield of 3.6% (what the company can pay out to us) and the mid-point of my assumed growth rate of 6-8% (so 7%), Advantest seems to be set up for around 10.6% long-term return potential at the current price. This is pretty good but there are better options in the current market.

Let's do a simple DCF calculation to see if we have any valuation upside here. Assuming FCF per share of ¥142 (3.6% FCF yield x ¥3,949 share price), a 7% growth rate until 2030, 6% growth into perpetuity (due to the wide moat that stems from the duopoly with Teradyne) and a 10% discount rate, one share should be worth around ¥3,962 ($26.27 per ADR), as can be seen in the following screenshot from a simple DCF calculator:

DCF calculation (moneychimp.com)

I have to note that the ¥3,949 price doesn't include the Friday 3, 2023 trading day (where the ADR increased 3%) because the Tokyo Stock Exchange was closed. So in conclusion, Advantest seems to be a bit overvalued right now. Keep in mind that this assumes FY24 numbers.

Risks

The main risks are (1) the cyclical nature of the semiconductor equipment market and (2) market share losses.

(1): While I think that Advantest's underlying market will grow in line with the overall semiconductor industry, there might be times when the market is declining or stagnant for several quarters or even years (just like we are seeing right now). This market volatility will find its way into Advantest's earnings. Investors need to be willing to stomach such volatility. If you think you are not ready to hold this stock even through declines in the range of 30-50%, you should consider investing somewhere else where there is less volatility involved.

(2): To be honest, I am not an expert regarding semiconductor equipment or design. This is why I limit my investable universe in this space to companies with very high market shares like Advantest and Teradyne. I think that the semiconductor test market is not big enough and too complex to attract serious competitors. To compete with Advantest and Teradyne, you would need to make big upfront investments without even knowing if these may pay off. However, existing semiconductor equipment manufacturers like KLA Corp. (NASDAQ: KLAC ), Applied Materials (NASDAQ: AMAT ) or Lam Research (NASDAQ: LRCX ) may decide to invest and offer products in the testing space in the future. Reasons for this might be that they want to offer a broad suite of products to their customers or that they just want to discover new growth opportunities. There is also the risk that Advantest loses significant market share to Teradyne, its only real competitor at the moment.

Conclusion and what to look out for

Advantest traded down since my last update in May 2023 which wasn't unexpected due to the huge run-up at the time of the AI hype. The market outlook in the semiconductor test market seems to brighten up with Advantest and Teradyne assuming that the market will get close to CY22 levels in CY24. Excluding temporary market size volatility, the semiconductor test equipment market is expected to grow between 6-8%, in line with the overall semiconductor market, until 2030.

Investors should look out for any comments regarding the FY24 and beyond market size development from both companies' management teams.

Since Advantest is a volatile stock, I think there will be better prices to buy. With total long-term return potential sitting at around 10.6% right now and my DCF calculation showing that Advantest might be fairly valued (on FY24 earnings) at best, I will have to reiterate my "hold" rating. I might change my stance to a "buy" rating closer to ¥3,500 per share.

I will keep covering the company and write another update sometime next year when FY24 guidance starts.

For further details see:

Advantest: The Semiconductor Test Market Seems To Recover In CY2024