AEF - AEF: Emerging Market Equity Exposure For Diversification But Caution Warranted

Summary

- AEF focuses specifically on emerging market equity exposure, which could bring significant diversification to an investor's portfolio.

- The fund's history might show inception going back to the early '90s but is a result of a merger in 2018 today.

- The largest exposure is to China, so one would have to have a pretty optimistic outlook there.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on August 19th, 2022.

There are quite a few choices in the closed-end fund space when investing in global securities. However, most of the more flexible global funds carry significant exposure to U.S. investments. In most cases, the exposure is 50% or even greater of the total portfolio being in U.S. investments. That's where the abrdn Emerging Markets Equity Income Fund ( AEF ) can play a unique role in one's portfolio.

I'm generally not one to focus specifically on a certain country exposure, instead choosing those more generic "global" funds to do my international investing for me. That being said, there is still quite a bit of flexibility regarding emerging market exposure through this fund.

There are emerging markets in just about every continent around the globe. Therefore, providing some diversification or the flexibility for such geographic diversification. At the same time, they have no exposure to U.S. markets, meaning one is getting a true global differentiator in this name.

It does come with some downsides. The fund's performance has been quite dismal since it launched and for most periods. That includes its latest transition. This fund really started in 2018. It was the product of a merger of several different funds into what was the Aberdeen Chile Fund ( CH ).

Despite "income" in its name, the payouts were inconsistent and all over the board. There appears to have even been a pause in payouts for a period of time several years ago. However, that was prior to the transition. Additionally, they launched a minimum 6.5% distribution policy in mid-2021. This is based on the previous three months' average daily NAV.

The largest geographic area that appears to have the most promise is Asia; at least, that is where they have positioned the fund most heavily. In particular, China is a significant representation of this portfolio. With the current geopolitical tensions with the U.S. and a slowing economy, China could drag this fund lower. That would make its future performance look much like its past performance, which has mostly been a struggle.

The latest name change in the fund was due to their rebranding. Instead of Aberdeen, they shortened this and dropped the capital letter. Thus, we are left with the abrdn funds .

The Basics

- 1-Year Z-score: -1.33

- Discount: -12.24%

- Distribution Yield: 7.97%

- Expense Ratio: 1.21%

- Leverage: 14.7%

- Managed Assets: $370.5 million

- Structure: Perpetual

The investment objective of AEF is quite simple; they "aim to provide both current income and long-term appreciation." They have five key factors in determining whether companies meet their objective in the emerging market space. Those are "durability of the business model, the attractiveness of the industry, the strength of the financials, the capability of the management and assessment of the company's ESG credentials."

The fund's expense ratio comes to 1.21%. When including leverage expenses, it comes to 1.31%. They are moderately leveraged, but any leverage can add to potential risks. The borrowings are through a credit facility, so higher interest rates often translate into higher interest expenses. Minimal leverage with how volatile the emerging markets can be would seem appropriate.

Performance - Quite Volatile

With emerging markets, they are going to be more sensitive to global economic conditions. I believe that is what we have been seeing in the fund as 2022 proves to be a challenging year. The fund is off much further than its U.S. investment counterparts.

Here's a look at the long-term history of the fund's price action going back to the inception date, when it was focused on Chile.

Ycharts

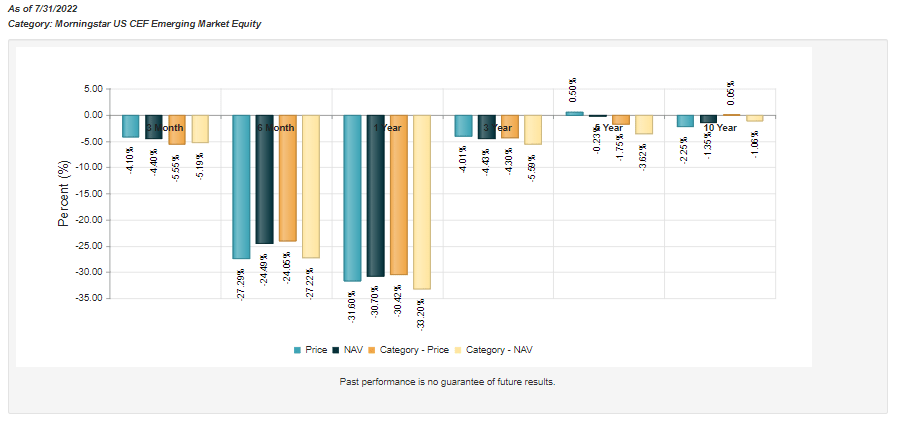

Every standard annualized performance period, which includes the distributions paid out, shows a negative number on a total NAV return basis. The one period that shows a positive is the total share price return over the last five years; though, that's only slightly positive. This includes the last three years where the fund had completed its transition.

{kind=link}

AEF Annualized Performance (CEFConnect)

I don't believe the challenges for this fund will change going forward. At the beginning of the year, Russia was 5.5% of the fund's exposure. In March , they updated that the overall exposure was slashed to 1.17% after Russia's invasion. That just highlights the significant risks of geopolitics at this time.

The next drastic change could come from China. China's exposure was 35.6% at that same time. At the end of May, exposure to China has fallen to around 28.6%. Still, that sizeable allocation leaves the fund vulnerable to continued geopolitical tension and a slowing Chinese economy . The constant lockdowns due to their COVID policy appear to continue hurting their economy drastically.

A CEF's performance can be impacted significantly by a good discount. For this fund, the discount is larger than average if we look at the last ten years. However, that's largely being impacted by a significant premium at the beginning of this period. There must have been quite the enthusiasm for Chile's investments at that time.

Ycharts

Since this fund really had its transformation in 2018, going back roughly four years shows us that the latest discount is right near the average of this period. I think that given the significant risks at this time, it would appear a wider discount could be appropriate.

Ycharts

Distribution - Trying To Add Predictability

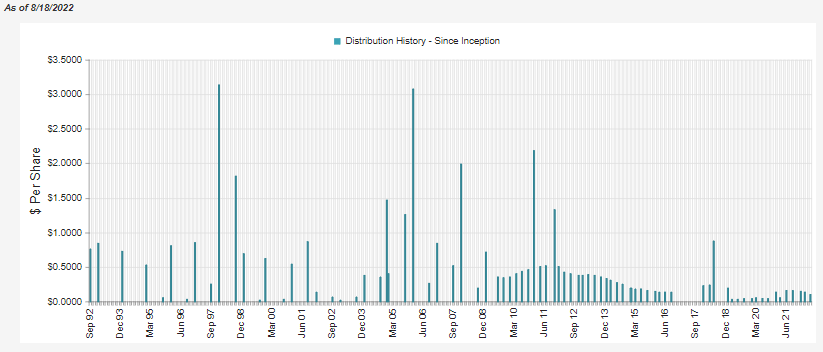

With the overall emerging market space being quite volatile, it's not really a surprise to see a volatile distribution history. The income of this fund has been significantly volatile too. However, they implemented a 6.5% distribution minimum policy in mid-2021. This seems to be in an effort to smooth out the payouts to investors.

On April 20, 2021, the Fund announced it will pay quarterly distributions at an annual rate, that is a percentage of the average daily NAV for the previous three months as of the month-end prior to declaration. The Board determined that the initial annualized rate beginning with the June 2021 distribution is 6.5%. This policy is subject to regular review by the Board.

The policy is expected to provide a steady and sustainable quarterly cash distribution to Fund shareholders that may help reduce any discount to NAV at which the Fund’s shares trade. There is no assurance that the Fund will achieve these results.

{kind=link}

AEF Distribution History (CEFConnect)

Again, just a reminder that prior to 2018, the fund was focused entirely on one country. Chile is an emerging market, but a smaller one. I believe the distribution history of an emerging market fund could look quite similar even if it was more broad-based.

In this distribution policy, as long as the NAV is going lower, the payout will continue to go lower and vice versa. At least with a managed distribution policy, this can now provide some predictability in what these quarterly payouts will be even if the underlying assets are incredibly volatile.

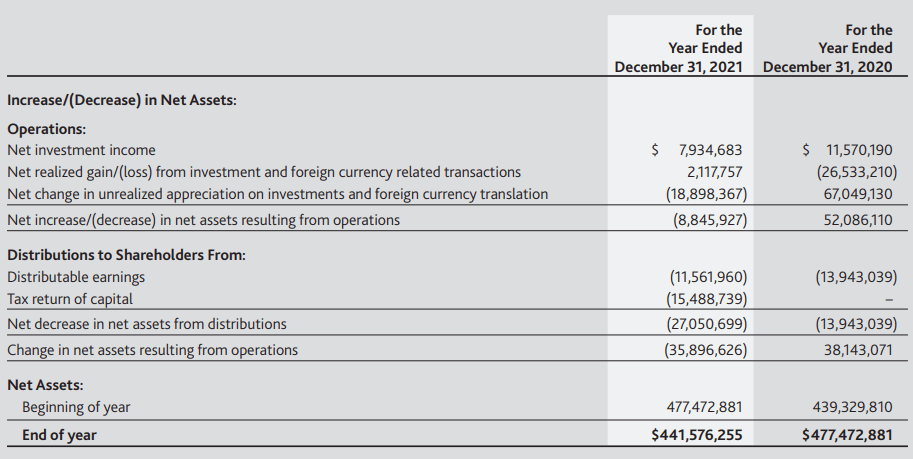

To cover the fund's distribution, it will rely heavily on capital gains. That is quite common with all equity funds. In each of the last two years, the distribution wasn't covered. NII had declined year-over-year as well.

{kind=link}

AEF Annual Report (abrdn)

With the lack of coverage, we should expect some of the distribution to be classified as return of capital. In this case, it would appear to be destructive return of capital for the last year.

{kind=link}

AEF Annual Report (abrdn)

AEF's Portfolio

AEF's turnover rate can change quite drastically. Last year they reported around a 50% turnover rate. In the year prior, it was only 21% and even more shallow in 2019 at just over 13%. Then in 2018, it was 145%, but this was due to the transition the fund had made in that year.

The fund's largest sector exposure is dedicated to tech. Following that, the fund is tilted towards financials with meaningful exposure to consumer discretionary, materials and industrials.

AEF Sector Exposure (abrdn)

The largest geographic exposure is concentrated in Asia at this time. However, the Americas are also represented, as well as some small exposure to Africa through South Africa.

AEF Country Exposure (abrdn)

A significant weighting in Asia and specifically China will determine the result of this fund. This is a significant risk due to the details mentioned above, but we are also now seeing Chinese companies delist off the NYSE . This is marking yet another escalation in tensions that we've been seeing between the world's largest economies. There are risks of further delistings , such as Alibaba Group Holding ( BABA ), which was the fourth largest exposure in AEF.

However, there have been some optimistic news on that front. An agreement between U.S. regulators and China has been announced. It doesn't take the risk of delisting to zero, though.

An additional consideration is that the top holdings represent a fairly large slice of the investment pie for this fund. The three largest holdings represent 21.2% of the fund's holdings. The top ten make up 37.4% of the fund. In total, CEFConnect puts the total number of positions at 81.

AEF Top Holdings (abrdn)

Conclusion

The history of AEF has certainly been a rough one. However, noting that the latest fund really only goes back to 2018 and not the 1991 inception date that they provide. This was because they made a big transition and name change to consolidate several funds into this more broad-based emerging market fund. COVID rocked the fund during this time, so the short results thus far don't look promising either. Going forward, one would have to have a high conviction in China to see a positive outcome in this fund. This is because China represents a fairly large impact in terms of direct exposure. Not only that but also indirectly to the geographic region in which most of this fund is invested.

At this time, I wouldn't invest in this fund unless there was a larger discount. That being said, at a smaller allocation, it could still provide an appropriate global tilt for diversification purposes for some investors.

For further details see:

AEF: Emerging Market Equity Exposure For Diversification, But Caution Warranted