AEG - Aegon: Merger Of Dutch Business Unlocks Significant Value

Summary

- Aegon and ASR Nederland have recently announced an agreement to merge their Dutch businesses.

- Aegon will receive close to €5 billion, through cash and a 29.99% stake in ASR.

- This deal improves Aegon’s financial profile and increases its long-term dividend sustainability.

Aegon ( AEG ) has recently announced a deal to combine its Dutch operations with a close competitor, receiving some €5 billion in cash and shares. This represents some 50% of its current market value and seems to be a great deal to unlock value.

As I've analyzed in previous articles , Aegon has been in restructuring mode for some years, which was leading to an improved operational and financial profile. Despite that, its valuation was still quite low and had good prospects of delivering a growing dividend, something that was delivered in recent months.

More recently, the company announced the combination of its Dutch operations with its domestic competitor ASR Nederland ( OTC:ASRRF ), a move that it expects to create significant synergies and unlock value for shareholders over the long term.

Background

Aegon is a life insurance company based in the Netherlands, which has operations across several geographies. Its current market value is about $9.8 billion, and its shares are traded on the New York Stock Exchange.

Aegon has good business diversification, offering a full range of life insurance and other financial services to its customers. Its two largest markets are the Americas (the U.S. plus Brazil) and Netherlands, which together represent some 73% of its operating results in 2021, while other markets such as Spain, Portugal or China are reported as International.

Operating result (Aegon)

Over the past few years, Aegon has made a significant restructuring of its business profile, with the goal of having a stronger balance sheet and a more recurring financial profile. This was pushed by the low interest rate environment that lasted many years, both in the U.S. and Europe, which forced insurance companies to adapt their business model to this reality.

To mitigate the impact of low interest rates in the company's life business, Aegon pushed for fee-based products instead of traditional insurance products with guaranteed rates, leading to a less-capital intensive business than it had some years ago.

Additionally, the company made several disposals and focused its operations in a smaller number of countries, where it had better profitability levels. While this strategy was largely completed, Aegon has recently announced a merger of its Dutch business with its competitor ASR, creating a leading company in the Dutch insurance market.

Dutch Business

Aegon's operations in the Netherlands are diversified across several segments, even though life insurance is the largest one measured by operating income, as shown in the next graph. Nevertheless, Aegon also offers mortgages, banking services, annuities, and retirement solutions to some 2.7 million customers.

Dutch operating result (Aegon)

About a week ago, Aegon announced that it reached an agreement with ASR to combine its operations in its domestic market, receiving €2.5 billion in cash and a 29.99% strategic stake in ASR, valued at €2.4 billion when the deal was announced. This deal is expected to close during the second half of 2023, following shareholder, regulatory, and antitrust approvals.

This move is justified by Aegon's desire to release capital from mature markets and to allocate its resources in markets where it has better growth prospects over the long term.

From an operating perspective, this deal seems to make sense given that it will increase both company's position in several segments of the insurance and banking markets, namely in disability insurance, P&C insurance, and mortgage origination, leading to significant revenue and cost synergies.

Aegon's strategy is to use cash proceeds to reduce debt and return capital to shareholders, which will lead to strong dividend growth next year. Indeed, Aegon's annual dividend in 2022 was €0.20 per share, while Aegon's guidance is to have a DPS target of €0.30 in 2023. This represents annual dividend growth of 50% and is above what the market was expecting before the merger announcement. Note that the current consensus only expects €0.277 per share in 2023, as some analysts have not yet updated their estimates following Aegon's revised guidance.

Dividend (2023) (Bloomberg)

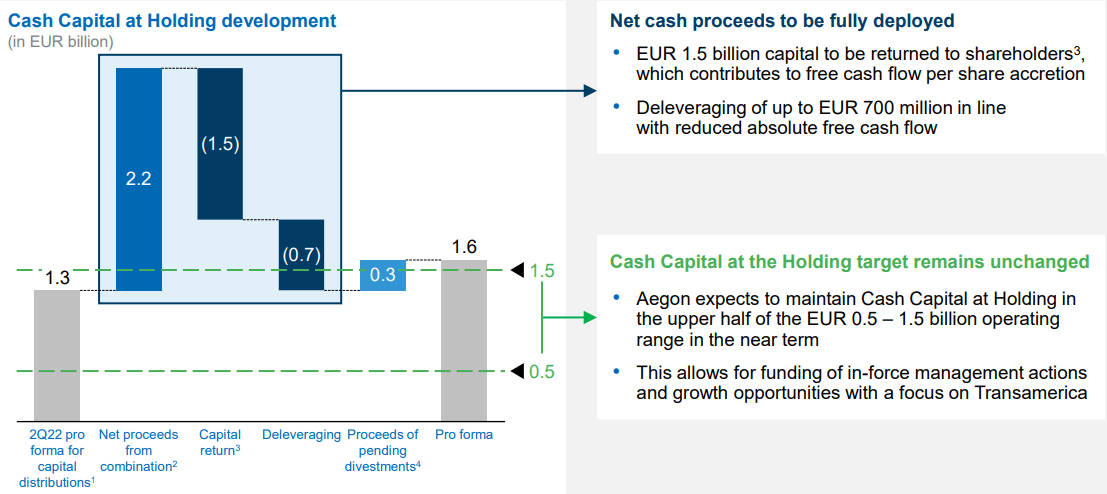

Aegon had about €1.3 billion in cash at the holding level available for cash distributions before this deal and expects to return some €1.5 billion to shareholders following the disposal of its Dutch operations. Considering that it will use €700 million to reduce debt and still has some €300 million to receive from pending disposals (Romania and Poland), Aegon will have some €1.6 billion pro forma available at the holding level, which is above its own target of being between €0.5-1.15 billion. This means that Aegon has plenty of room to increase its dividend (which will lead to a cash outflow of about €600 million), potentially perform a share buyback of about €900 million (9% of its current market value), and invest for growth in its Transamerica unit.

{kind=link}

This deal is also expected to be free cash flow accretive to the holding level, as the loss of cash remittances from Aegon Netherlands will be offset from ASR's future dividends, lower interest expense, and synergies to be extracted from the business combination. Aegon expects its dividend to be well covered by free cash flow in the next few years, which means that Aegon's dividend sustainability increases with this deal as cash at the holding level is expected to increase and will have less need to retain cash following its balance sheet deleveraging measures.

Aegon is expected to update its financial targets and growth opportunities during 2023 in a capital markets day, as the company's operating profile will be much more biased to the U.S. market and is likely to use some of the proceeds to perform some bolt-on acquisition in this market.

Regarding its dividend, as the company is now committed to distribute at least €0.30 per share in 2023, while previously its guidance was for €0.25 per share, this means that Aegon is currently trading at a forward dividend yield of about 6.4%.

This is a very attractive dividend yield and has good dividend growth prospects, as the company's financial position will be stronger following the merger of its Dutch business, allowing it to deliver a growing and sustainable dividend for its shareholders over the medium to long term.

Conclusion

Aegon's investment case was highly geared to its dividend, given that it is not a growth company, justifying its cheap valuation. Its recent deal to merge the Dutch business with ASR Nederland is a great step to unlock value, as gross proceeds amount to close to 50% of its market value, while this operation had a smaller weight on its operating income.

Its financial profile will improve following this deal, which should lead to extraordinary capital returns and a more sustainable dividend over the long term. Its dividend yield is expected to be above 6% over the next twelve months, which is very attractive for income investors.

For further details see:

Aegon: Merger Of Dutch Business Unlocks Significant Value