AGGH - AGGH: Complexity Is Paying Off For Now

2023-10-27 08:39:41 ET

Summary

- Simplify Aggregate Bond ETF aims to replace traditional core bond ETFs by using tools such as leverage, options, and futures to enhance yield.

- The fund's complex composition of ETFs and derivatives comes with a significant amount of leverage and risk involved.

- AGGH has beaten the index on several important measures, including total return and standard deviation.

Introduction

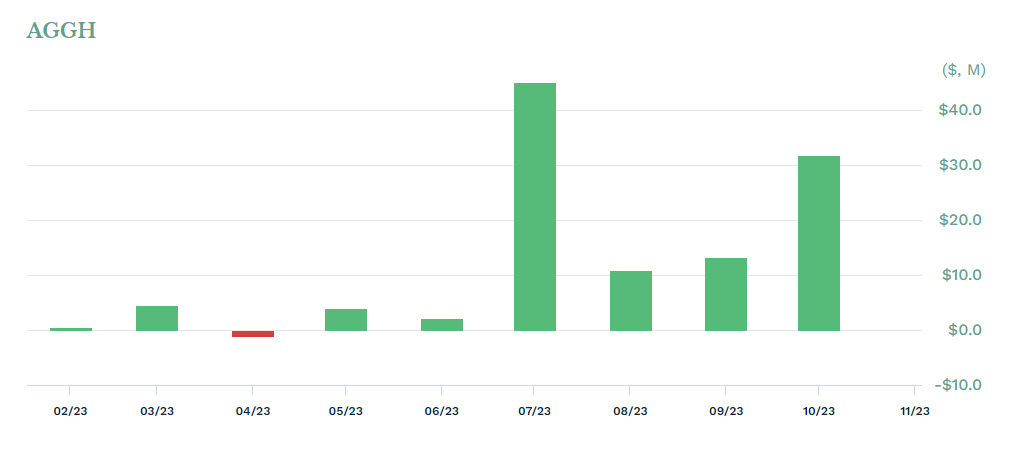

On Valentine's Day, 2022, the Simplify Aggregate Bond ETF (AGGH) launched with little fanfare. It was a desolate turnout, with only $4M added AUM in the first three months.

{kind=link}

AGGH's AUM has grown since then, not only due to bringing in new institutional and retail investors, but also because of Simplify's sister funds buying in. More on that in the risks section.

Simplify claims that AGGH is a new kind of core bond holding. It's here to replace your grandfather's core bond ETF. To make things interesting, as Simplify seems to try to do with all of their funds, Simplify is using several tools to enhance yields and lower overall risk, including using leverage via ETFs, options, and futures; and active management with bond selection.

So far, it's been paying off. Below is the total return of AGGH compared to its best direct passive competitor, the ETF it gets its name from, the iShares Core US Aggregate Bond ETF (AGG).

Brief Overview

At a glance:

- Name : Simplify Aggregate Bond ETF

- Price : $20.98

- Dividend Yield : 5.16%

- Distribution Yield : 11.22%

- Volatility : 9.61

- Beta : 0.013

- Expense Ratio : 0.30%

- AUM : $108,345,048.60

As per Simplify:

The Simplify Aggregate Bond ETF (AGGH) seeks to maximize total return. The fund is actively managed to create a core bond exposure with enhanced yield via structural income opportunities such as more efficient curve positioning and defined-risk option writing. AGGH can be used by investors who not only seek higher yields than investment grade bonds normally provide, but a higher total return as well.

Portfolio Composition

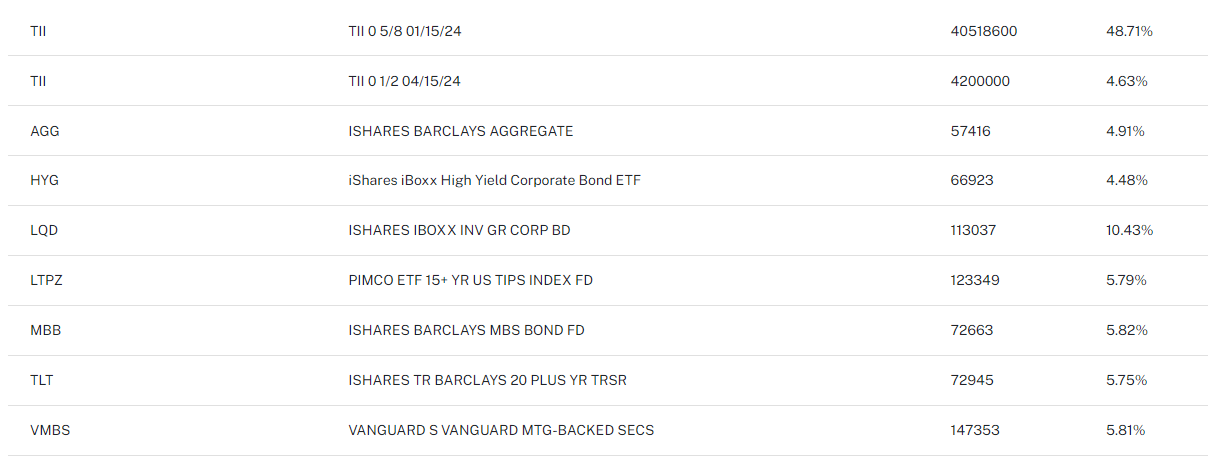

The fund runs multiple strategies in its portfolio. First, it primarily holds other bond ETFs. These account for 98.62% of the fund's weight, as shown below in Figure 3 (not included in Figure 3 is a 2.29% weight in T Bills).

{kind=link}

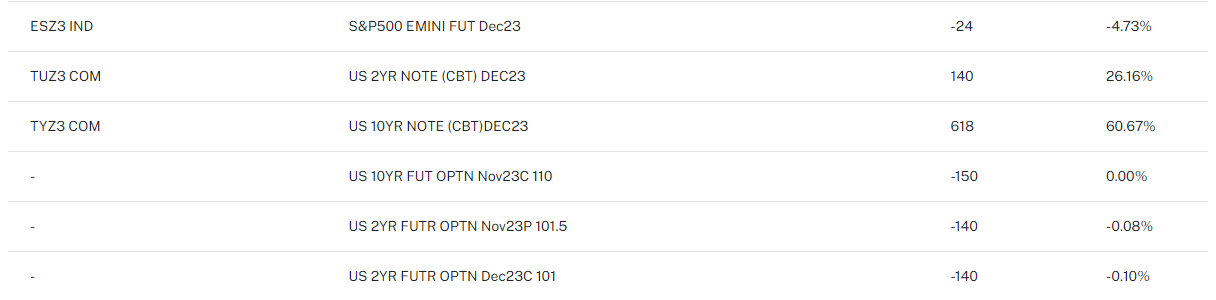

This on its own would be a fascinating position to analyze, but we see the addition of even more complexity. The portfolio managers sold S&P 500 futures and deployed cash into treasury futures and treasury futures options.

{kind=link}

Notice the massive weight that the 2YR and 10YR futures have on the portfolio due to their leverage. While we have almost 100% exposure to bonds from ETF holdings, the managers added another 86.83% exposure to these futures. This is a massive bet, and one investors should be wary of when adding AGGH to their portfolio. This is a large amount of leverage, and a risk investors should be wary of.

{kind=link}

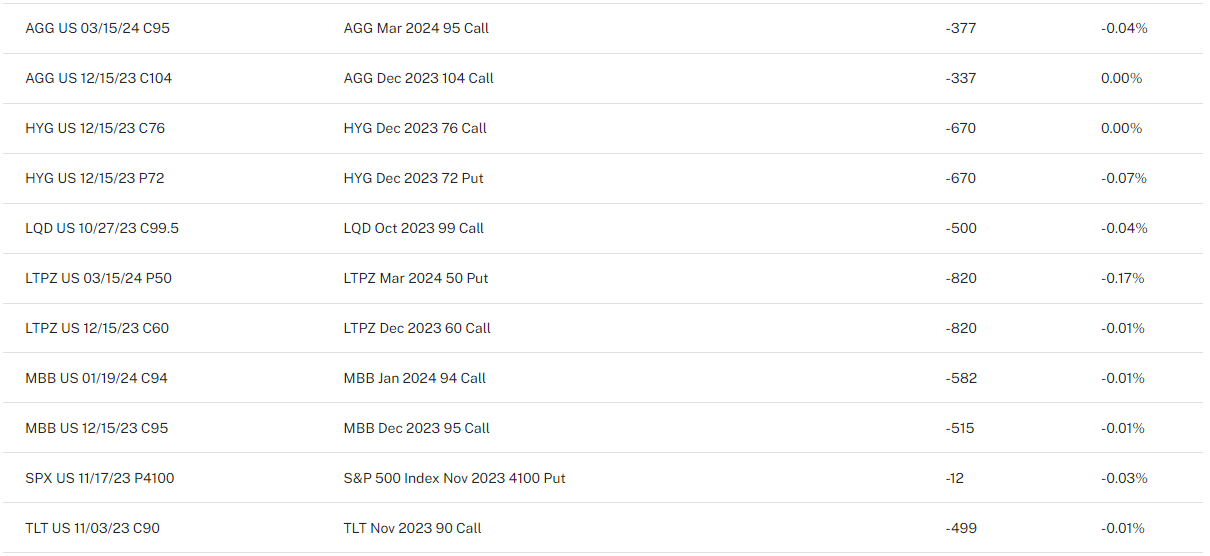

Here's where we get weird. Simplify has a very interesting take on options in a bond fund, as they are not running the usual gambit of passively selling calls against their holdings, such as the strategy TLTW uses; see my analysis here . Some of their holdings, such as LQD and TLT have covered calls deployed on them, they also stagger their strikes and expirations on several of their trades.

Notably among the fund's covered calls are the staggered calls on the mortgage-backed securities (MBB) position. They only sell calls against 15% of their shares, but for those, the payoff looks like this:

{kind=link}

These strategies are core to AGGH's goal: maximum income. In order to sustain the staggering 11% distribution yield, the managers needed to add extra income on top of the bond ETFs.

Through synthetic or direct exposure, the fund carries a total of 184% exposure to bonds. This may be less in reality, once options premiums are factored in, but without the data showing each trade made in the fund, it's impossible for me to tell what that real percentage is. Based on how much of the fund is exposed via these options, I would say that total exposure is likely in the 150 - 170% range.

Volatility & Risk

The first question we should ask is whether this complexity had added excess risk. Compared to AGG, we can see in Figure 8 that AGGH, during its short tenure so far, did exhibit lower overall volatility for most of this year, a year where bonds were hammered. There has been a reversal in the last few weeks, though I believe this is temporary. I suspect this increased volatility is from the large holding in 10YR UST futures that AGGH holds as well as the smaller 20+ year bond ( TLT ) position.

Beyond this, there are several risks to be aware of with AGGH. First, it's a new fund, and that means that there is uncertainty ahead in its future. While I can't recall any funds Simplify has closed, there is definitely a possibility of issuer risk that could cause investors to be forced to liquidate and take on tax burdens otherwise unnecessary. If that were to happen, the burden could eliminate excess gains made from the active management of the fund.

I promised we would talk about this, so here we are. Figure 9 above shows us the AUM of the fund over time, similar to Figure 1 in the introduction. The very large jump in July was not sudden retail or outside institutional interest in the fund. Simplify's other ETFs began to buy AGGH as core holdings. Most notably, the Simplify Volatility Premium ETF ( SVOL ), which holds 17.7% of its AUM in AGGH. The Simplify Macro Strategy ETF ( FIG ) also holds AGGH, totaling 6.4% of its AUM.

The SVOL holdings are a significant portion of AGGH's AUM, with a total of $83.17M in AGGH shares held by SVOL. In total, an absolutely staggering 78% of AGGH's AUM is held by Simplify's other ETFs . This could pose incredible risk to investors if SVOL's or FIG's managers decide to off-load shares of AGGH for their own strategy. That scenario could happen even if AGGH performs well, since the other funds have very different strategies that may or may not involve AGGH in the future.

Conclusion

AGGH has outperformed its passive counterpart, AGG, since inception, but not without risk. This added risk has paid off since it has not been shown in the fund's standard deviation, which has historically been lower than the index.

Looking under the hood, we can see that the fund is using unusual tools to increase distribution rates, such as holding futures for leverage, selling options against holdings, and changing the weightings of holdings away from their natural market weights in an aggregate index.

By almost all measures, aside the risks mentioned above, AGGH has done its job well enough to be considered for a core bond holding. Because of those risks, especially the risk of co-mingling 78% of assets within other Simplify ETFs, I cannot give AGGH a buy rating. For now, it is a hold.

If AGGH can grow AUM so that it can no longer be adversely affected by Simplify's other funds selling it off, I would be happy to change my rating to a buy.

For further details see:

AGGH: Complexity Is Paying Off For Now