AGQ - AGQ: Leveraged Exposure To Silver Without The Underlying More Selective Opportunities Elsewhere

2023-11-06 20:00:06 ET

Summary

- Leveraged ETFs provide excellent notional exposure in trending markets.

- In cyclical asset classes, the opportunity is less compelling, especially considering the downside risks.

- AGQ offers investors the kind of exposure and has its limitations with the shift in recent capital flows.

Investment Brief

With the plethora of macroeconomic risks currently plaguing global markets, precious metals, in the eyes of many, offer a potential downside hedge to erosion of capital. Long has the debate raged on precious metals in a diversified investment portfolio. Equally as debated is gold + silver's role as a potential inflation hedge, and 'store of value', as is the saying. It was told to me early in my career that precious metals won't necessarily create wealth, but they can preserve it. Others have dubbed the category akin to owning 'pet rocks'. No matter one's opinion on the matter, the facts pattern is that commodities are potentially within another super-cycle, and there is scope for the sector to catch a bid moving forward.

For investors seeking levered exposure to silver, the ProShares Ultra Silver ETF ( AGQ ) is an instrument worth the analysis. The fund's objective is to capture 2x the daily result of the Bloomberg Silver SubindexSM. It does this by purchasing derivatives contracts that are indexed to this benchmark, but critically, does not own any of the underlying bullion. Being that the fund is directional in nature, there are no dividends to speak of. Instead, investors would buy this searching for capital gains.

The fund's core holdings are comprised of a range of derivatives instruments, ranging from silver futures to a number of swaps on the benchmark index from various institutions. As a result of its 2x leverage, the total weightings amount to 200% of net assets, with 11 holdings at the time of writing. It has $376mm in AUM, and charges a relatively high expense fee of 0.95% on these assets, placing it in the 3rd percentile of the entire ETF universe. Moreover, the tracking error from its benchmark is 52% over the last 3 years, unacceptably high for investors seeking notional exposure in my opinion. There is also the risk of decay in the underlying instruments as they approach expiry, and then will need to be rolled forward onto the new maturities. As a result, this is a speculative play on one's outlook on silver, providing leveraged directional exposure to the underlying, without owning the bullion, as mentioned.

Figure 1. AGQ long-term price evolution, weekly bars.

{kind=link}

Net-net, my judgement on AGQ is mixed at this point in time and with a shifting paradigm on the inflation/rates story and recent macroeconomic data, there are more selective opportunities elsewhere in my opinion. I will run through my reasoning here today. As such, my recommendations across all 3 investment horizons are as follows:

Fundamental:

Neutral across all time horizons, short to long term.

Technical:

Also neutral across all horizons.

In that vein, I rate AGQ a hold.

Talking points

- Mixed outlook for precious metals

My judgement on a levered fund tacking a silver index is mixed at this point in time. Silver spot hasn't shown us much in the back end of '23, nor has it kept up with its counterpart gold's advancements. I don't buy the notion that it is underbought either. For ADQ, this isn't exactly the most compelling viewpoint that screams buy.

It was only a month ago or so when the bullish tone on silver (and gold for that matter) was at its peak. JPMorgan ( JPM ) analysts had predicted record prices for gold, and reporting from CNBC called for silver to outpace the yellow metal's returns. Underneath it all are 3 key macro themes:

(i). The inflation/rates axis

(ii). Geopolitical risks resulting in a flight to quality

(iii). The pace of buying from central banks

All 3 factors are related in one way or another, but there is no denying the sector has seen heightened demand in recent months. Traders lifted the bid on the silver spot from $21/oz to the $23s in mid-October, reversing a sharp selloff that ensued leading into Q3. That rally looks to have run out of steam in the short term, however, as seen in Figure 2. The result was more of a reversion to the mean. As seen in Figure 3, Silver has been trading sideways for the better part of 3 years, after it went vertical at the beginning of the Covid-19 market.

Figure 2.

Source: Kitco

Figure 3.

Source: Kitco

In a note from August, the crowd at UBS was reasonably constructive on Silver. It said there were notable catalysts, such as the ones listed above, that could drive a more compelling investment case for the metal.

"[W] expect silver prices to follow gold. But signs that global industrial production is bottoming out would give silver prices more upside compared to the yellow metal next year," it opined.

That said, investor interest in the metal has yet to turn the corner as well. We have no doubts that this will be the case once elevated risk-free opportunity costs moderate, renewed USD weakness emerges, and investors look for real assets, such as precious metals. In terms of the short-term price trajectory, pullbacks into the USD 20-22/ oz range are likely as the Fed could raise rates further. But once that round of expectations has worked its way into the market, we expect the metal price to stabilize."

The UBS team wasn't far off in fact. As mentioned already, silver reverted back to its long-term mean and has congested sideways since.

- Capital flows potentially weighted to equities

The outlook for precious metals including silver is currently mixed in my view and less compelling than it was around 3-6 months ago. The Fed's decision to pause the tightening cycle has been a bullish factor for equities, and institutional interests have piled into stocks in the last week or so. A note from Goldman Sachs ( GS ) on Monday noted that hedge funds were aggressive buyers of U.S. equities last week after the FOMC meeting. This, along with the initiating buying from the likely event (where price moves ahead of value) has resulted in the largest 5-day allocation to equity longs since the December '21 rally. Part of the sharp reversal was no doubt a burst of short covering for those short of stock, in my opinion.

The two identifiable risks to silver venturing higher, in my opinion, are (i) a continued levelling off or pullback in Treasury yields, and (ii) continued strength in the USD. The former would result in a sharp inflow to equities in my view, as we've seen in the last week or so (especially on the speculative side). The latter knocks silver's potential within the flight to quality, because it's arguable investors would rather own USDs than precious metals. Net-net, the path for silver moving forward is mixed, and less compelling than it was around 3-6 months ago. For AGQ, this is particularly concerning on the long side, given its 2x leverage on national assets. Whilst it may prove to be a potential on the short account, I do not hold this directional view on the fund. This supports a neutral view.

Collectively, without the 1) underlying market fundamentals, 2) capital flows, 3) flight to quality extending, my judgement is that investors will have a difficult time lifting the bid on sliver, and therefore, a 2x leveraged fund tracking the same as in AGQ. This supports a neutral outlook in an environment where short rates are still above a 4 handle, and equities are ripe for a fresh influx of money flows.

Technical factors for consideration - price structure, market character

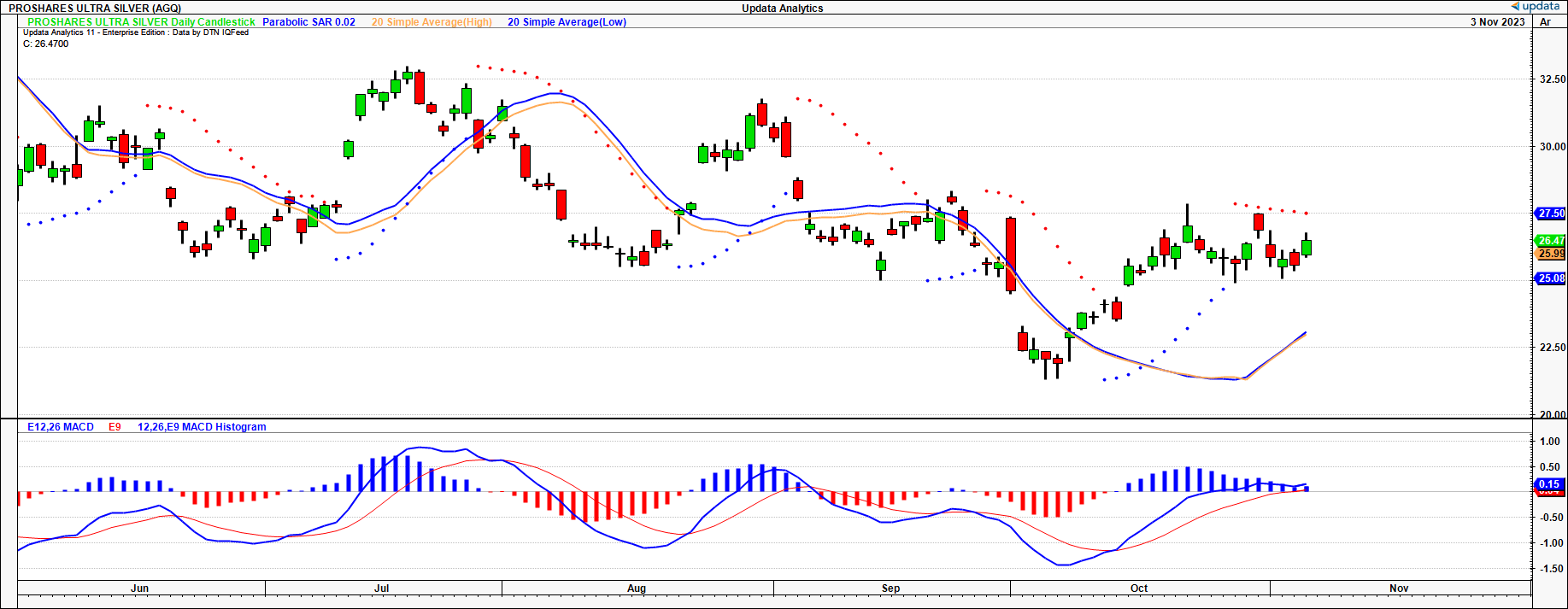

1. Regarding momentum

There are several notable features from the various momentum studies presented in the figure below. Critically, the fund has just completed a 3 waves down move and retaken the gap down from September. As to the rate of price change/momentum:

- We saw a bullish cross of the MACD in mid October and this has held trend into November. It is also curling up off 6-week lows, a sign of the positive momentum.

- The price line has crossed the 20DMA high and lows at the same time and this suggests a period of higher highs and higher lows rolling into November, corroborated by the hammer candle beginning of last month.

- The Parabolic SAR also showed a turning point with the price reversal off September lows.

- More recently, however, the trend has shown signs of exhaustion in the short term. This is seen via (i) the shooting star candle midway through October, a sharp turning point, and (ii) the double top leading into the new month. A break above the $27s is therefore critical for bulls to regain control. In the meantime, price has congested sideways.

Figure 4.

{kind=link}

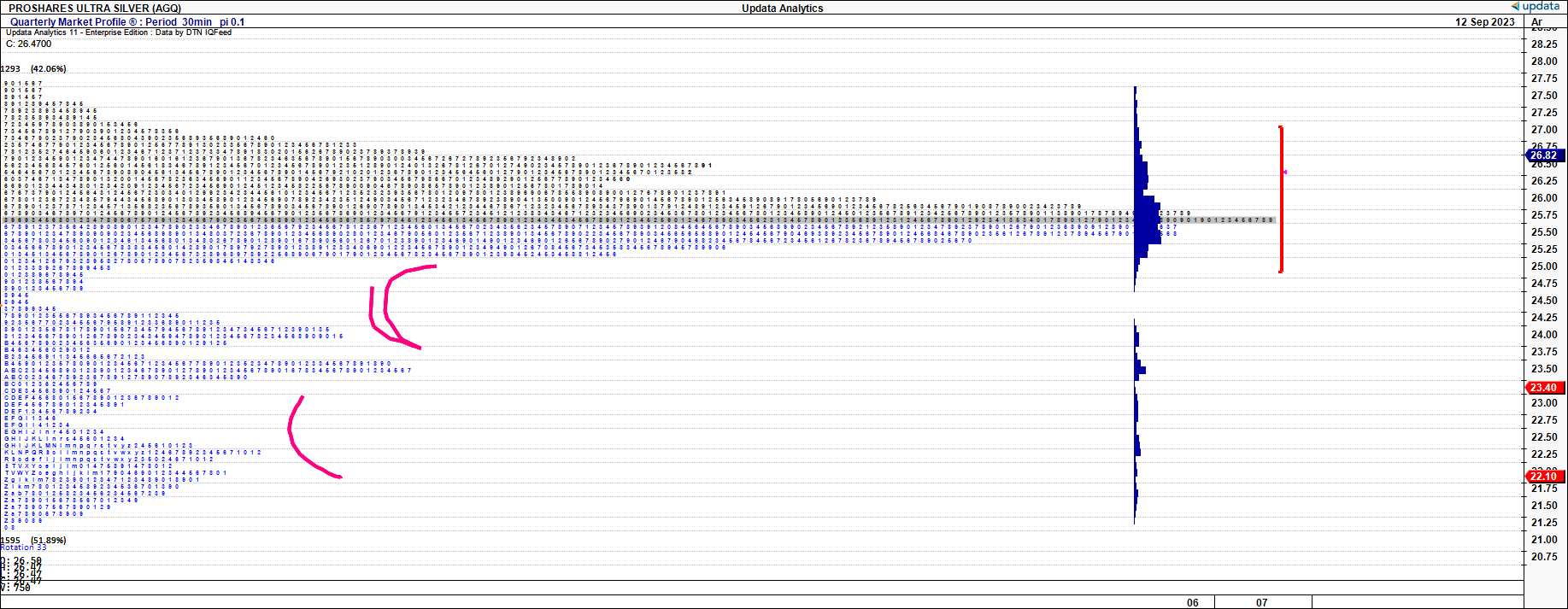

2. Skew, price distribution

Observations: The bulk of price usage from Q1-Q3 has centered around the peak of $25-$26.00, as seen below. This is observed at the point of control ("POC") and the volume point of control ("VPOC") in that region, which also captures the 'value area', i.e., around 70% of the distribution of the POC. This is a high-volume node that may be a magnet for price in further sideways trade, so watch out for this. We also have 2x pockets of low usage below the POC, in the $23-$24s, and the $21-$22s. It is not unreasonable to foresee these pockets getting filled on a bearish reversal from current value. Investors are already building the ledge in the $23s, and in my opinion, there is scope for this range to be filled to match the higher ledge/distribution. Keep in mind, that markets tend to rotate from pockets of high usage to low usage. We would also look for a matching ledge of the POC/value area to suggest the low-pocket area would have been filled, in order to complete the distribution. The distribution is also positively skewed, supporting the notion of further incremental losses, and snapback rallies as responsive buying.

Key levels: It would be advisable to closely watch the current value area in the $25-$27s, as this could be a magnet for the price to return on a snapback. I would also advocate watching the $22-$23 zone if the market were to fill this low usage pocket.

Actionable strategy: Given the distribution from Q1-Q3 is not yet completed, directional trade is not yet supported. Range trade is, however. There is scope to buy the bottom of value and sell the top of value if the fund continues backing and filling sideways.

Figure 5.

{kind=link}

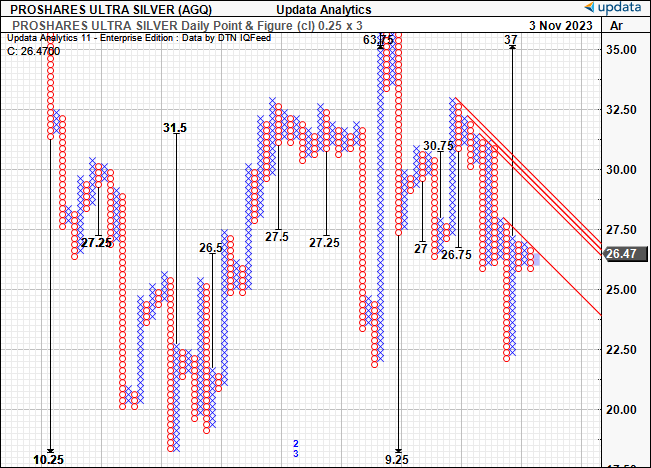

On the flip side, we have upsides to the $37 region that cannot be ignored. You'll also note the cluster of price targets in the $26-$30 region, aligning with the value area described in the market profile. The $37 upside target cannot be ignored as mentioned and would be activated with a catalyst relating to spot silver. I am watching this mark very closely moving forward.

Figure 6.

{kind=link}

3. Directional bias of trend

Based on the data, there is not yet support for a directional breakout as mentioned. As to the trend, note the following:

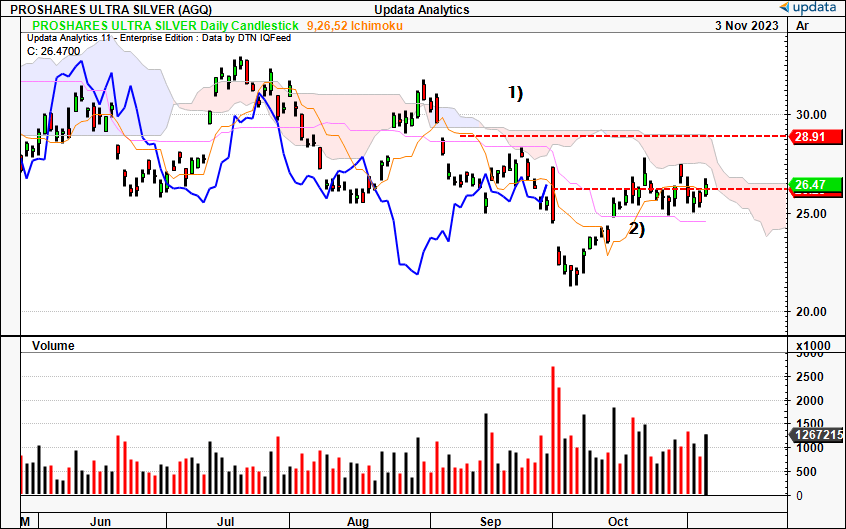

Figure 7. Medium term (Daily chart, looking to the coming weeks)

(1). We are neutral beneath the cloud, with both price and lagging lines under the cloud base. Critically, the double top outlined earlier tested and rejected the cloud.

(2). However, we are about to push into the cloud and a break above $27 by end of November could be positive for AGQ's price structure.

(3). The lagging line needs a break above $28 to illicit the signal.

Key levels:

- The marabuzo line from September was retaken last month however we didn't really break higher from here. So $27 remains the next point of resistance to break.

- If that occurs, we are looking at $29 as the next upside event, corresponding to the gap down from August.

- On the downside, a break below $25 would be significant, and that would have me looking at $21 from there.

{kind=link}

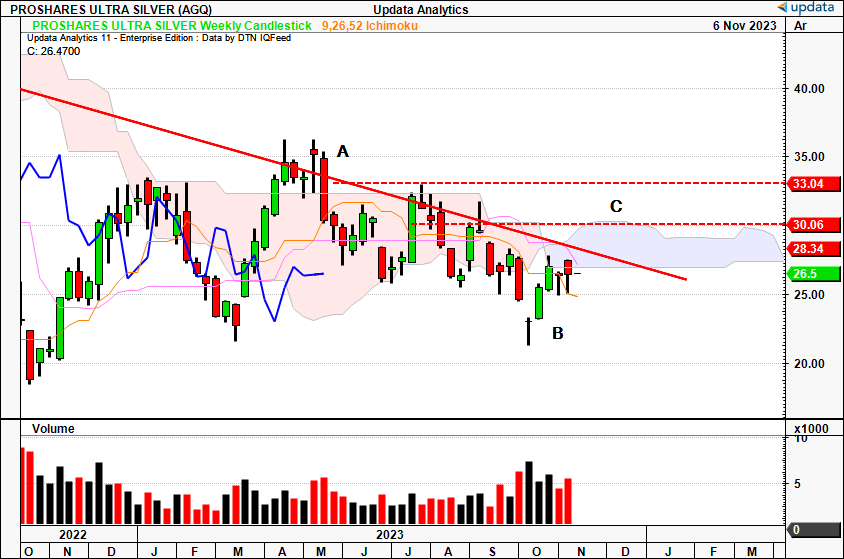

Figure 8. Long-term ( Weekly chart, looking to the coming months)

(1). We remain within a longer-term downtrend that's been in situ since March. At A, we topped with a reverse hammer and large marabuzo candle that was the cloud top until September. This is now a key upside level at $33.

(2). We reversed off the year's lows last month with morning star formation after the Doji candle at B. The following weeks were a period of high-volume buying, and this is critical as volume often precedes price.

(3). We've not had 3 weeks of tight closes and were unable to break into the cloud on the price. The lagging line is pushing sideways into the cloud.

(4). There is no directional bias on this trend just yet. We need to recapture the marabuzo line at C ($30s) and if done by December this would bring us into a bullish zone. The cloud pinch last month may facilitate this, but both i line and conversion line are still tending lower, offsetting this notion.

Key levels: The key levels to eye are the marabuzo lines at C then A. This corresponds with the cloud top on the upside. Again $25 is the support level on the downside, so if we break there, it would be remarkable.

{kind=link}

Discussion Summary

In short, playing leveraged funds can be an opportunistic investment in rallying markets. With commodity-based funds, that are cyclical and sensitive to exogenous factors, this can be equally as profitable in the right setting. My judgement is that it is not currently the right setting for AGQ at this time. With risk assets now catching a bid again, the scope for a flight to quality beyond what's been seen to date is now less compelling. There is a chance this thesis is wrong. But the main thing is, there are equally as defensive assets to protect capital and/or speculate on secular markets than AGQ in my view. Technicals are also unsupportive, which corroborates the neutral view. Net-net, rate hold.

For further details see:

AGQ: Leveraged Exposure To Silver Without The Underlying, More Selective Opportunities Elsewhere