AFRAF - Air France-KLM: Valuation Attractive (Rating Upgrade)

2023-06-21 10:41:18 ET

Summary

- The company's net debt was further reduced by €1 billion.

- Air France-KLM is focusing on improving its balance sheet, which is a positive catalyst to address investor concerns.

- The company is taking steps to achieve the medium-term core operating margin. Therefore, the company is now a buy on our list.

Today, we (once again) comment on Air France-KLM's ( AFRAF ; AFLYY ) latest development. Last year, it was an excellent call to remain cautious and provide a publication called a no-go opportunity . However, even if " We Still Prefer Low-Cost Operators ," we believe it is time to increase our rating on the French flight player. Indeed, air traffic is growing and getting closer to pre-COVID-19 levels. Flight operators are returning to profitability even though the airlines are still heavily in debt. One of the winners is Ryanair , which emerged from the crisis with a larger European market share (we also cover easyJet with a buy rating target ). Among the national legacy carriers, excluding Turkish Airlines , we see negative signs in EU market share development for Lufthansa (from 10% to 9%), IAG (from 7% to 5%), and Air France-KLM (from 6% to 5%). To sum up, at the aggregate level in the EU area, low-cost airline operators increased their market share penetration to 54% from 48% (from the pre-COVID-19 level in 2019). Despite that, the airline sector is back to profit for the first time since the crisis, and it is expected to close the current year with net profits estimated at $9.8 billion , a sign of recovery compared to the $3.6 billion loss achieved in 2022. If the sector starts on a rapid recovery path, the uncertainties associated with the global economic slowdown and inflation could reduce household disposable income and travel demand.

Despite that, before analyzing the latest Air France-KLM financial figures, it is essential to report the news from the Paris Air Show , which is currently underway (from 19 to 25 June 2023). The event is dominated by the return of travel demand for tourist and business passengers, and airlines are gearing up. However, during an interview, the CEO of Qatar Airways confirmed that the aviation sector supply chain has not yet recovered from the pandemic shock. Increased production rates and supply chain delivery difficulties continue to worry aircraft manufacturers and, therefore, travel operators. This might provide a two/three years delay in deliveries. Even if it is a problem, here at the Lab, we see a compelling opportunity, so the commercial aircraft sector will likely experience a strong price momentum. In addition, many planes are grounded due to problems with engines, avionics, or other broken systems. Repairs are not happening at the expected pace, limiting the sector's capacity. COVID-19-induced divestment and the 2023 solid demand created the perfect conditions for high prices over a long period.

Changes in our estimates

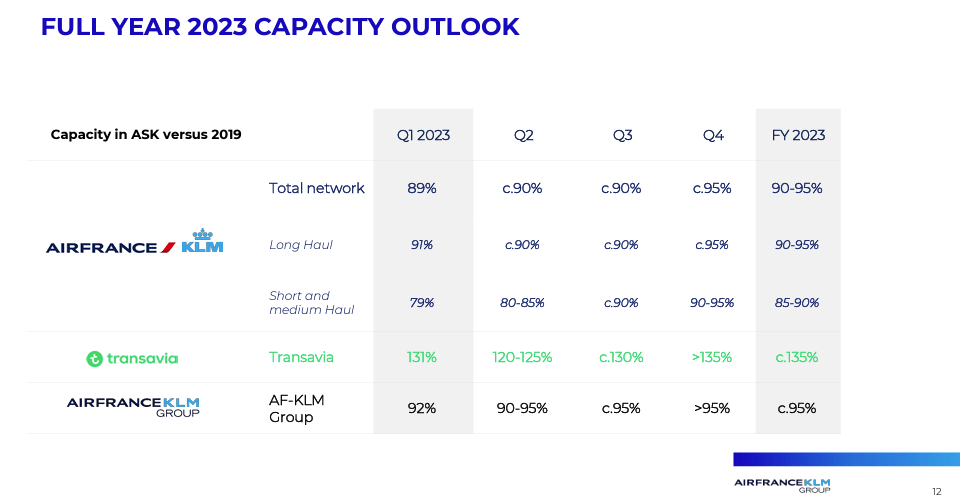

Very briefly, Air France-KLM delivered an operating loss of €306 million compared to a consensus forecast set at €282 million loss. Despite that, the company operated with a capacity at 92% of the pre-COVID-19 level, with a yield up 18% on a yearly basis and almost 20% higher versus Q1 2019. There is no sign of weaknesses, and the company decided to prioritize profits over load factors. Since demand is high and is already helped by capacity constraints, we are forecasting €29.6 billion in top-line sales for 2023. In addition, this summer season will be the first without any restrictions. On the other hand, we are forecasting lower capacities for Japan and China for this year. We adjusted our forecasts at the Lab to reflect the Q1 figures. Therefore, we increased our yield projections to capture a solid trading outlook.

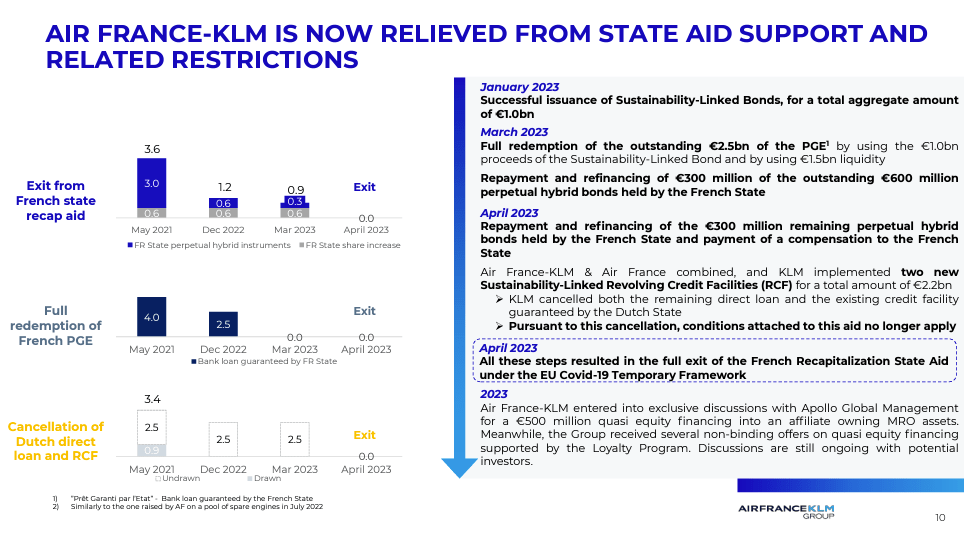

In Q1, Air France-KLM reduced its financial debt by almost €1 billion to €5.5 billion, with net debt/EBITDA improvement from 1.8x to 1.5x. The company also repaid €2.5 billion of state financial aid, removing all the restrictions attached to the Government support. The company is now focused on balance sheet improvement to cover positive cash flow into equity. This will support investors' concerns in our view. For this, the CEO confirmed discussions with Apollo Global Management for a €500 million equity financing support for an affiliate with spare engine assets. Air France-KLM is also considering equity financing thanks to its Flying Blue loyalty program. Here at the Lab, we believe these are reasonable steps to support the company's equity to open a path for dividend payments. Our estimates confirm a CAPEX of €3 billion for 2023.

On the 2024-2026 targets, a 7/8% core operating profit is achievable. However, we should remember that exceptional items at the FCF level may still impact the company. These are mainly related to tax and social charges and also cargo claims. Consensus Fiscal Year 2023 operating profit has grown to €1.9 billion from €1.5 billion, identical to the 2019 profit peak in 2017 when the company reported €1.9 billion. The issue with the current negative equity (-€2.9 billion) may be solved thanks to the new Apollo deal, the loyalty program, and the improved net income generation.

Air France-KLM relieved from state aid support (Source: Air France-KLM Q1 results presentation)

{kind=link}

Conclusion and valuation

We believe that Air France-KLM offers an attractive valuation. Therefore, we are moving our rating from neutral to buy. We are also confident that the company is taking the necessary steps to improve investors' sentiment. The company is currently trading at a 2023 EV/EBITDA multiple of 3.1x, approximately 40% lower than its competitors. To support our rating upgrade, Air France-KLM is currently trading on an EV/EBITDA of circa 2.9x for the Fiscal Year 2024 estimates; however, the 5-year pre-COVID median was 3.9x. We decided to base our price target on an EV/EBITDA of 3.9x (in-line with the company's historical average), and we derived a target price of €2.3 per share ($2.5 in ADR). On the downside risk, we should report that the company left unchanged its cost guidance for the current year. This is mainly due to wage inflation. Additional hazards include FX evolution, lower travel demand, jet fuel cost evolution, and higher competition from low-cost operators.

{kind=link}

Air France-KLM guidance

For further details see:

Air France-KLM: Valuation Attractive (Rating Upgrade)