AKCCF - Aker ASA Well Positioned For 2023 And Valued Substantially Below The Sum Of Its Parts

Summary

- At the most conservative valuation for Aker ASA, it trades substantially below the sum-of-parts valuation of its public and private holdings as an investment/industrial company.

- Every single one of its affiliated businesses are either backed by infrastructural or at least pseudo-infrastructural economics, favorable S/D dynamics or very strong secular tailwinds.

- While a margin of safety is likely assured even assuming continuation of the current market status quo, it's also a play that's 2023 appropriate with substantial revaluation possibilities in Cognite.

- Leverage is minimal, and there is an ample dividend supported by its strong businesses that pays investors to wait.

- Finally, tax law changes in Norway make it more likely that price discovery will happen, as the majority owner and founder has incentive to offer his shares to the float as a new resident of Switzerland.

Aker ASA ( AKAAF ) is a Norwegian company that trades with millions of dollars in liquidity on the Oslo Stock Exchange and holds an array of investments in both private and also publicly listed companies, mostly trading under some version of the Aker name. Its businesses are either relatively future proof or benefit from infrastructural or pseudo-infrastructural economics with excellent tangible returns and growth opportunities. Otherwise, they own a substantial interest in Aker BP ( DETNF ) which benefits from the current dislocation in the global oil market from the Russia-Ukraine conflict, as well as growing speculation over a China recovery, where China was heavily beaten down by COVID-Zero in 2022. Aker ASA trades well below even the most conservative estimate for its sum-of-the-parts valuation, with substantially more upside if you're bullish on the capital markets and the ability for major assets like Cognite, an AI-powered rig maintenance startup, to get a higher valuation on future rounds of funding than what they got in 2021. Critical for such a thesis, there are also major catalysts for price discovery as changes in Norwegian tax laws sees the founder, Kjell Inge Røkke, leave Norway and move his residence to Switzerland, which has a fraction of the taxes on capital gains - he may contribute many more shares from his controlling interest to the public float and generate institutional interest as a part of his block gets shopped around. As a final level of downside protection, there is an ample dividend yielding above 4%, and more of its companies could approach a dividend paying state over the next couple of years, giving you a clear advantage over owning the Aker holdings independently.

Overall, the company is well defended from secular dangers, and actually sees many if not all of its businesses very well positioned for the current macroeconomic environment. With a discount from NAV already on just the public holdings, some of which will be newly approaching a more mature, dividend paying stage over the next few years, you get access to tangible cash flows cheaper through a safer Aker ownership than you would from the public holdings held in the same proportions but independently.

Public Holdings

Aker's public holdings are each important in their own regard, and most are well positioned in the current environment in terms of valuation and secular growth. Working in Dollars rather than NOK, below is the EV of the company based on current market cap, and the scaled down valuation of Aker's shares in each of their public holdings. Immediately, a discount to the net asset value of public holdings is visible, before even getting to the private assets.

Public Holdings ((VTS))

While taking market values of their holdings is already a pretty conservative way to value a company where markets are at close to 2020 lows, we'll detail each of the holdings and why they are likely at the lower level rather than the higher level of their respective ranges of reasonable valuations.

Aker BP

We have actually covered Aker BP on SA, and most of the ideas still apply since the article was very recent. Firstly, the valuation is low, about 20% lower in EV/EBITDA that other E&P peers. The company pumps oil from major reserves in which they have meaningful stakes. Despite the low valuation, and assets on the Norwegian Continental Shelf which are among the lowest breakeven points in the industry and therefore deserve a premium, Aker BP is ready to quite massively grow production flows as they are about to launch the next phase of production on their most important reserve, Johan Svedrup. Based on the representation of Johan Svedrup in the mix of flows, and the substantial increases in production that will come from Phase 2 which has probably just started (we are now in Q4), production volumes for Aker BP overall should increase 30%. With operating leverage and at current prices (that could be a bottom for oil as China readies its rebound but we won't assume that), that should mean even sharper increases in earnings, easily 50%. That would compress the forward multiple much further and lie substantially below peers whose assets are not as high quality nor fecund for production increases.

Aker BP is capable of producing growth in volumes, benefits from the China reopening that is heavily being backed by a strategic need by government, and can mitigate volatility or downward pressure on price which would be unexpected but possible in oil markets due to OPEC unpredictability. Its valuation looks low.

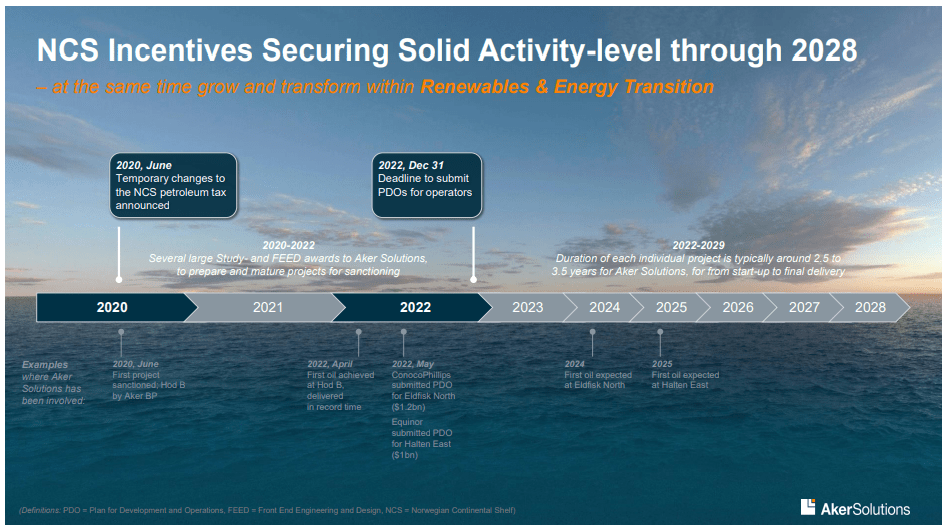

Aker Solutions ( AKRTF )

This is an interesting company. Through a three-way J.V they are solidifying their position in subsea markets, partnering with Schlumberger ( SLB ) and Subsea 7 ( SUBCY ).

During the quarter, we announced that we have agreed to combine the complementary subsea businesses of Aker Solutions and Schlumberger to create a strong and leading subsea company. Subsea 7 will become an owner and a partner in the JV enabling the JV to offer fully integrated subsea projects globally.

Kjetel Digre, CEO Aker Solutions

This subsea venture is about 33% of their business by revenue but 60% by EBITDA and is well positioned with a rapid acceleration in the pace of NCS development to record levels as oil proves critical to Norwegian influence and economic power and is incentivized fiscally by government tax breaks. Their other businesses are mostly very related and benefit as well. Backlog grows sequentially in subsea and stays solid YoY, and order intake was great for gas field works and some carbon capture projects in the Renewables and Field Development segment, so both under and over the sea we see a demand push. Finally, the E&M segment which works on longer-term contracts and is recurring in nature sees sequential backlog improvements with decent economics.

{kind=link}

The low-breakeven points of the NCS below $20 per barrel put them way ahead of most other fields, and the comprehensive exposure to both subsea, consolidated by the SLB and SUBCY cooperation, but also field development and ongoing maintenance and servicing revenues, makes their profile attractive and consistently cash generative.

An essential thing for investors to note is that new projects always start at low profitability and usually become massively higher as low expense work comes towards the end. We still haven't seen the margin lift from the NCS boom. Aker's forward EV/EBITDA is at 6.3x due to a substantial holding in Aker Carbon Capture ( AKCCF ), which puts it in line and their multiple is 30% lower than TechnipFMC ( FTI ) which competes oligopolistically with Aker Solution's new partner, Subsea 7, and does surface technologies as well. There is likely good value here, especially with an advantaged position relative to Norway, but also the Aker conglomerate, because a lot of Aker Solution's business comes from Aker BP.

Aker Horizons ( AKHOF )

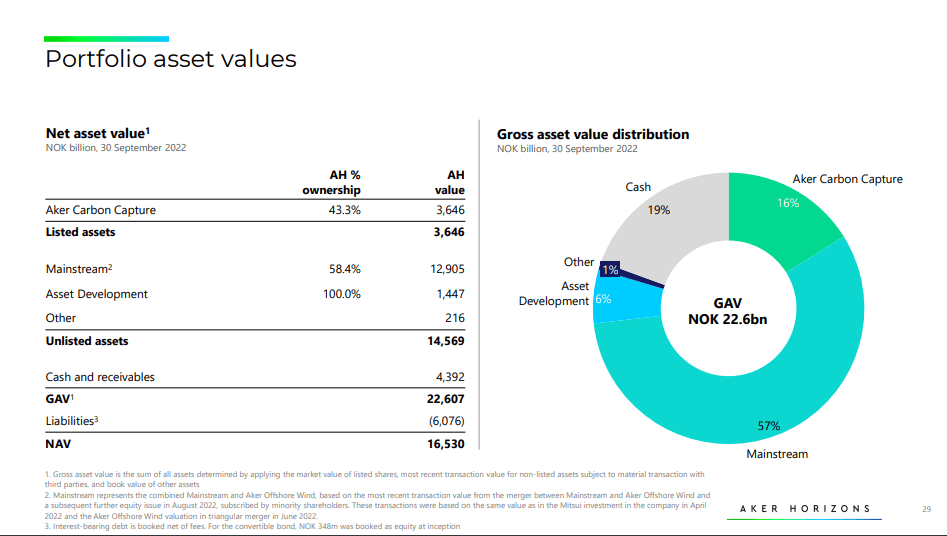

Aker Horizons is a holding company within the Aker ASA holding company structure. Through Aker Horizons, Aker ASA has its ownership of Aker Carbon Capture which will be discussed in the section after this one.

{kind=link}

This is the only avenue through which Aker ASA owns Aker Carbon Capture, so we can't double-count the value of Aker Carbon Capture. Therefore, we subtract the value of Aker Carbon Capture owned by Aker ASA from the value of their holding in Aker Horizons to get the residual value of the non-CCS companies within Aker Horizon's portfolio.

At a NAV of 13 billion NOK which excludes the market cap value of Aker Carbon Capture, the discount is almost 50% from NAV based on the current market cap of Aker Horizons. So the residual ownership in the Mainstream assets are highly undervalued by markets.

Aker's NAV Calculation for Horizons (Q3 2022 Report of Aker ASA)

This cannot be justified. The Mainstream assets were merged with the Aker Offshore Wind holding, which can be seen as separate on previous reports before the merger.

NAV (Annual Report 2021)

These assets, after having been merged, issued equities to minority shareholders in August 2022, after the June downturn at the beginning of the tightening cycle, and the valuation was as given above in the Q3 2022 NAV calculation. This was the same valuation as Mitsui got when it invested in April 2022, and is also the valuation implied by the merger in June. The key thing is the August share issuance, which wasn't subscribed to by Aker ASA which would be a related party, but to minority investors. This valuation in the NAV chart is really what the market value should be, based on recent enough precedents.

Aker Carbon Capture

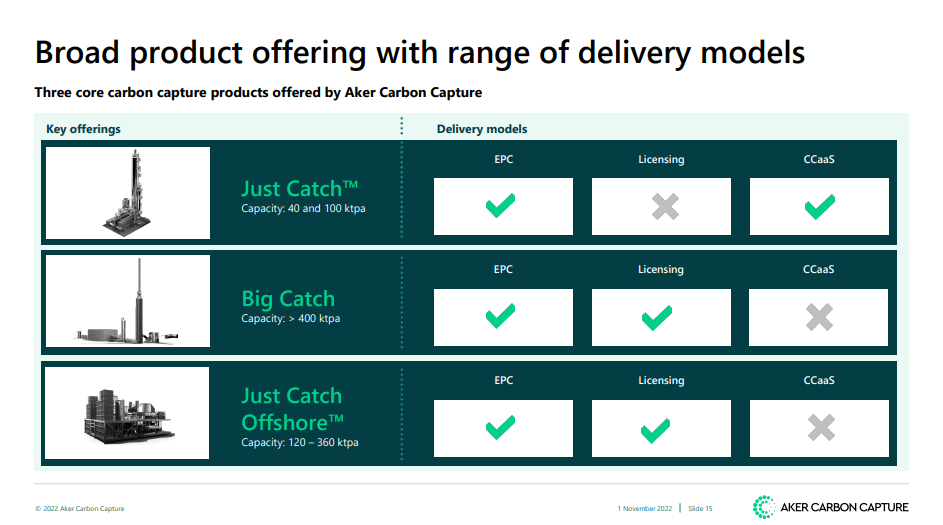

The Brevik project is the only currently in-progress project, but they are already partnering with major companies and emitters like Babcock ( OTCPK:BCKIF ) in the UK, Siemens ( OTCPK:SMAWF ) and BP ( BP ). The business model is that they can build CCS facilities for clients at the site of their works (depending on their carbon emission needs) and then maintain and service the facilities thereafter.

{kind=link}

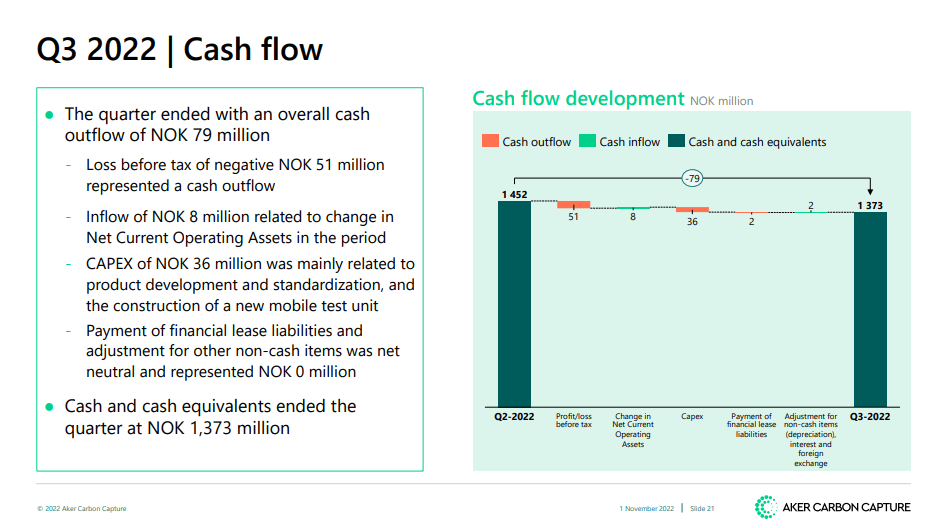

Much like subsea companies we expect favorable mix and scale effects as projects go into their later stages, in particular when they become maintenance cash cows, and we notice already shrinking EBITDA loss margins as Brevik progresses. Cash burn is also very limited and the company is well capitalized. They have not issued shares since last year and will not likely have to issue shares going forward. With the price discounted, this mitigates reflexivity effects. They also have no executive compensation plans that pay in shares and would further dilute shareholders. That is very rare for a company that is in a relatively fashionable industry.

Cash Flow Profile (Q3 2022 Pres)

{kind=link}

The Chief Executive Officer determines the remuneration payable to key executives in accordance with board guidelines. Aker Carbon Capture has no stock option programs. The remuneration for executive management includes a fixed annual salary, standard employee pension and insurance schemes and a variable pay element.

Finally, in terms of valuation, Aker Carbon Capture is not at stratospheric levels. Current EV/Revenue is 8.75x. With only one project in action, and two more in very early stages, a tripling in revenue appears feasible. There are also other contracts that have been definitively signed. As the projects there launch, we should see more than a 5x in revenue over the next 2-3 years. With the potential economics improving as projects go through their milestones and get into their later, cash cow stages, the EV/Revenue metric looks fair as it eventually converts into EBITDA.

Support for the green agenda is very unlikely to stop at this point, even after a year of unpopularly high energy costs. Considering the infrastructural profile, a rapidly shrinking EV/Revenue to closer to one renders the current price rather fair - certainly nothing to worry especially about after a year of discounted markets.

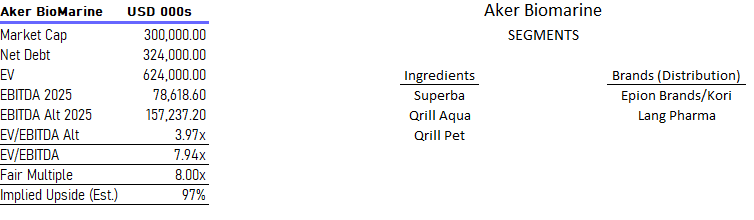

Aker Biomarine

Aker Biomarine is a very interesting Norwegian issue that owns several vessels for catching Krill. We've been covering them on the Value Lab for almost a year now. They have over 70% market share in the Krill market, and no one else has the ships that they have, which are designed specifically for Krill fishing by sucking them up from the ocean so that they don't get bludgeoned and start to putrefy. The ships conduct some of the initial processing for making Krill products.

Critically, the current global Krill catch is 50% of the quota, which means there's a huge margin before overfishing or fishing limits get hit. China is still in the process of developing their first high-tech ship and probably aren't going to create problems for years either commercially or ecologically.

Krill has a couple of end-markets. It's a source of Omega-3 for consumer products, and Aker Biomarine sells its Omega-3 products under its own brand as well as white label and through their medical nutrition business Lang Pharma. The consumer end-markets are about 50% of the business, where the other half goes into the aquaculture market as a feed product. Salmon and shrimp have been doing well, and are less grain-feed intensive than typical livestock - therefore they've benefited from inflation of grain as a consequence of the Ukraine war. Krill prices for aquaculture are up 15% and this is driving up overall 28% EBITDA growth. Furthermore, they are spending millions in advertising for an Omega-3 product for the US market, and this will start to decrease relatively soon, and the recovery of China should drive purchases in that traditionally strong market. Finally, supply chain issues hit some of their US-focused consumer segments and those should be resolved. All in all, we should see continued scale in consumer and ingredients for aquaculture, with aquaculture prices also holding fast and with upside potential since Krill is still a very new source of feed and likely not fully priced.

Aker Biomarine Valuation (The Value Lab)

{kind=link}

The valuation rests on the assumption that in 2025 the EBITDA margins go from the current 20% level to the assumed 30% level at higher scale economies and also reduced marketing spend since now is a time of discretionary push. Moreover, revenues are assumed to double from 2021 FY figures, and the 10% rates we've seen this year despite supply chain pressures, delays, and a dormant China means that the doubling assumption by 2025 remains relatively feasible in our view. Overall, the company is an interesting proposition in itself, and the valuation, which currently reflects a stock price close to all-time lows, is by no means overextended. We think the market value is a fair valuation to use in the SoTP.

The Rest

The rest of the public holdings account for 3% of the overall NAV of the public instruments. Akastor ( AKKVF ) is just an investment company that invests in oil assets, much like Treasure ASA ( TRSUF ) of Wallenius Wilhelmsen ( WILWY ) does, and can be taken at market value pretty comfortably. Solstad Offshore ( SLOFF ) is another rig supply and subsea services company. It trades in line with TechnipFMC but is a lot more marginal. It has much more scope for growth than the subsea incumbents, and has achieved that growth while the others haven't as much so the multiple seems more than fair. AMSC ASA ( ASCJF ) is an interesting company - they own bareboats that they lease out, which means ships without crew. The weighted average tenor is of two years , and they own a tanker fleet. They comply with the Jones Act, and therefore can do business in the US. While tankers charters get volatile, a 2 year weighted average duration is good, and the 10x EV/EBITDA multiple doesn't appear excessive. Then there's Philly Shipyard ( AKRRF ) which builds AMSC's tankers. They're unprofitable but also marginal.

Overall, the rest of the public holdings can more or less be counted upon.

Private Holdings

Then there's the private holdings which are a smaller part of the NAV, which is good because their valuations are harder to determine. Still, it is worth coming to some defensible figures to see how much more upside there could be in Aker ASA, especially as a calming of the economic environment potentially restores activity in the capital markets, and in particular VC activity which plummeted after ill-fated 2021 outlays largely devalued and the IPO exit on a shot equity market became useless for generating IRR. The return of sponsor activity is one of the big reversals that we expect over the next 1-2 years as we lap 2022 inflation figures and as cooling-off economies give time for inventory levels to build again after shortfalls that began and accumulated throughout the pandemic. This would drive the upside case, but for now we give the conservative case, and we'll explain the values that we get in this table over the coming section.

Private Holdings ((VTS))

Aize

Aize is an emerging industrial visualization software used to visualize and collaborate on 3D schematics of industrial assets. It is profitable on an operating basis and is deploying its solution full scale with some oil and gas companies and has signed several pilots in the last quarter.

Aize Highlights (Q3 2022 Report)

Annualizing its EBITDA and revenues we get the following.

Optimistic Valuation ((VTS))

We get the above valuation using the P/S ratios of peers like Dassault Systemes ( DASTY ) and Autodesk ( ADSK ). Between the two of them the multiples are pretty in line, and while Autodesk is for less industrial uses for the most part than Dassault Systemes' suite which is leading in its industry, an average P/S multiple between them gets us where we want to go. The book value used for NAV calculations in Aker's disclosures is 37 million NOK or around 3.7 million USD, which is too little for a firm that generates around 370 million NOK in revenues, and already 2.5 million NOK in EBITDA, and this is after various scaling costs were incurred.

While a 1% EBITDA margin is very low, it was closer to 5% last year. Still, while using ADSK and DASTY multiples illustrate the potential upside in a holding like Aize if it matures well, a smaller multiple would be the conservative thing to do. Therefore, for our valuation base case we'll use a more conservative multiple of 2.5x P/S, which is consistent with more marginal enterprise tech players in our coverage universe.

Fairer Valuation ((VTS))

Cognite

This is the crown jewel of the Aker ASA portfolio, and is probably going to become Norway's first ever VC unicorn, but with the current VC environment: probably later rather than sooner. Q2 2021 was the last precedent, which is before markets saw a downturn, and this VC round valued the company at close to $700 million. VC markets are going to be worse than then, and Cognite has widened its EBITDA losses.

Still, the company has a lot of potential. They deploy a DataOps solution that collects industrial data for customers and uses ML and dashboards to help companies with predictive maintenance and with taking other actions to keep assets as productive as possible. They recently partnered with SLB who will use Cognite as part of their solution, but have other customers too including Saudi Aramco ( ARMCO ), Total ( TTE ) and of course Aker BP. Cognite has a J.V with Aramco related to general industrial digitalization in Saudi Arabia. They also partnered with Rockwell Automation ( ROK ) in the US in an OEM capacity, similar to SLB. Growth is phenomenal at more than 50% YoY in revenue.

Cognite Highlights (Q3 2022 Report)

Nonetheless, we think a 20% down round would be possible, in addition to dilution effects. We don't have the cash position so we can't know if they're going to raise capital and dilute, but a revaluation down 20% consistent with most tech devaluations makes sense.

However, if the VC markets are to return over the next two years, which is the prognosis we have for the market based on inflation rate and likely interest rate evolutions, Cognite could easily achieve its unicorn status within a medium-term investment horizon for Aker ASA.

SalMar Aker Ocean

SalMar Aker Ocean can be discussed briefly. This is a venture with leading salmon farming company SalMar ( SALRF ) in Norway. It is an innovation, because instead of pens in the Fjords or in the Hebridean Archipelagos in Scotland, the farming will occur offshore, in deeper waters. There is uncertainty about the success of such a thing, but it is more sustainable at least.

The issue here though is that the Norwegian government has recently started a process to tax salmon farming resources at very high rates. Between 20% to a 40% tax rate will be applied additionally to EAT (net income) of large salmon farmers. SalMar is one of the largest. The treatment of this effort is unlikely to be favorable vis-à-vis size considerations for aquaculture taxation because it is not a J.V, with Aker ASA taking a minority stake in the project. It could be under fire once these new tax laws become ratified.

Overall, best to give it a 0 value to be conservative although fish farming has amazing economics when done in the ordinary fashion in Norway. It is very unlikely that their investment in SalMar Aker Ocean, which at cost was around $70 million, will be written off.

Aker Energy

The very last asset to discuss is Aker Energy. This was an interesting project to be an E&P company with specific focus on a field in Ghana. The problem is Lukoil ( LUKOY ) has an important stake in the license which makes it complicated, and also supply chain issues have created problems to move forward. The project development plan submissions have been postponed. This is all very early stage.

In principle, the project is not sanctioned by the US despite Lukoil's interest due to some technicalities over when this Ghanaian project was started. Moreover, Lukoil is in a grey area because the Chairman Alekperov who was named in sanctions stepped down, and companies like Eni ( E ) announced new projects where Lukoil also has a stake. Lukoil's presence does not necessarily doom the project, but it makes it uncertain. Lukoil could always sell their share of the license, and Aker has suggested that as a resolution. It will likely resolve itself eventually, but let's give it a 0.

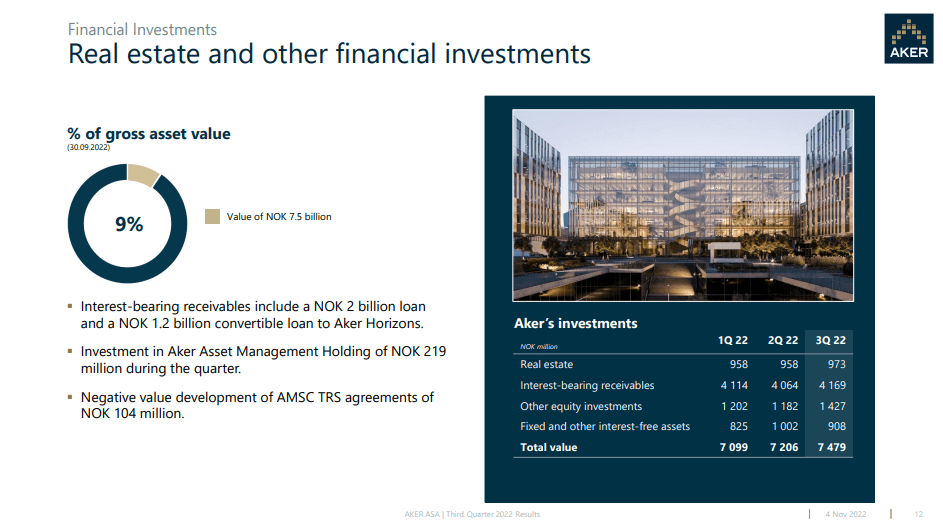

Minimal Leverage and Other Incidentals

There are more non-operating assets to consider as we sum the parts of Aker ASA. They have real estate, cash, interest bearing receivables and other equity investments as well as other random assets that also make their mark by offsetting fully the gross debt.

{kind=link}

Net Debt ((VTS))

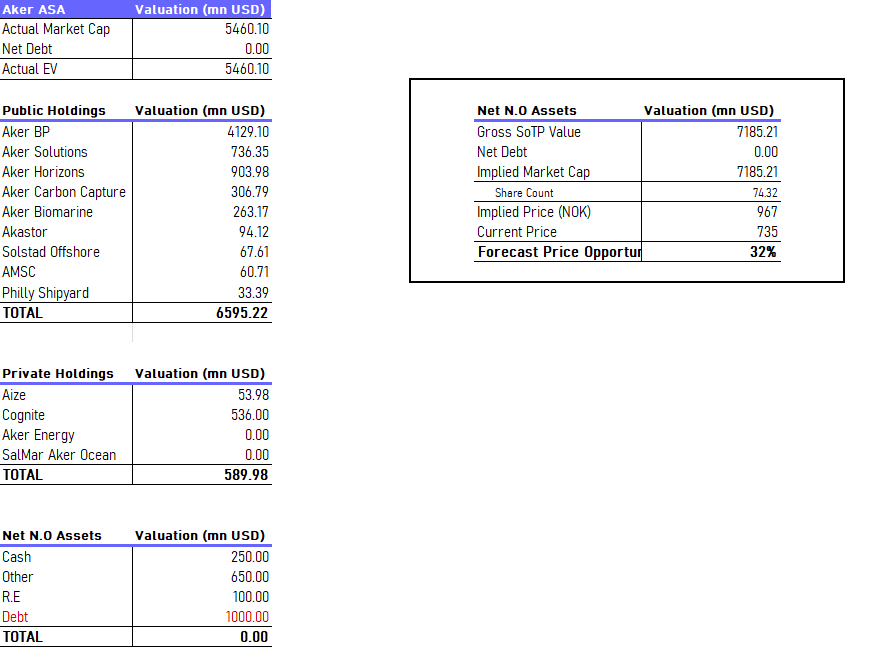

Valuation Scenarios

The end-point of the base case is the following:

{kind=link}

The upside is 32%, just from using market values for the public holdings, writing off several of the private holdings and assuming Cognite, the closest thing Norway has to a tech unicorn, takes a 20% hit to its valuation in VC markets despite equity markets already recovering this year which directly drives VC valuations due to the staple IPO exit. Moreover, the Fed has finally acknowledged that there aren't many more rate hikes coming at this point noting the low inflation. We believe they are ultra conservative to avoid speculative perpetuation of inflation and other flywheels, so this is a very strong bullish indicator for the likely market reality in six months' time. At least a partial return to normalcy, including in private capital markets, can be expected without being foolish in our opinion.

If we were to be more generous in our assumptions by just using book values, so:

- Valuing Cognite at its 2021 valuation

- Valuing Aize with the same multiple as larger peers

- Valuing Aker Energy at book value

- Valuing SalMar Aker Ocean and book value

We would get the following:

More Optimistic Valuation ((VTS))

Cognite represents 10% of Aker ASA's overall asset value. If that were to be revalued more favorably than it was in 2021, for example by becoming a unicorn in the next couple of years, the upside would continue to grow to 50% . Moreover, a general recovery in equity markets, which are still discounted 15% from beginning of 2022 levels, would grow the values of the public holdings too, and that is 90% of the asset value of Aker ASA. In particular, Aker BP has volume growth coming right now, Aker Solutions is substantially undervalued relative to peers, and Aker BioMarine is growing its profitability with scale economies and latent consumer demand push, and it dominates its niche market. Aker BioMarine is also trading close to all-time lows.

Bottom Line and Catalyst

Aker ASA offers a discounted way to expose yourself to companies that even when market-valued, offer propositions for upside through either secular growth or low multiples. It is levered to the general market recovery, and particularly sharp effects from greater market certainty will be felt on its earlier stage private holdings, in particular their predictive maintenance and AI jewel of Cognite.

Most importantly, Aker ASA benefits from a potential catalyst. Typically, these 'holding company' discounts come about because ownership is too concentrated in a controlling interest. While Røkke will probably not give up his controlling interest, there is scope for the float that generally trades to grow by 20% because Røkke has moved his residence to Switzerland due to wealth taxes being newly implemented in Norway. In doing so, he has an incentive now to realize decades of capital appreciation at low Swiss capital gains taxes, which can't exceed levels around 12% as of now (in Norway it's more than twice that). Greater potential liquidity for Aker ASA by 20% will mean more price discovery to close the NAV discount. Moreover, at the holding company level Aker ASA is known to monetize its ownership and isn't fussed with maintaining controlling interests, which means NAV discounts in companies like Aker Horizons could dissipate and help price appreciation.

At any rate, the 4% dividend yield is appreciated in the meantime.

For further details see:

Aker ASA Well Positioned For 2023 And Valued Substantially Below The Sum Of Its Parts