PFLT - Alaris: A 9% Yield Worth Biting On

2023-08-17 13:35:30 ET

Summary

- Alaris Equity Partners Income Trust invests in private companies, primarily in the United States, in exchange for preferred equity, common equity, subordinated debt, and promissory notes.

- The typical businesses that Alaris invests in are family or individual controlled entities looking for a capital boost, and Alaris receives periodic distributions or interest in return.

- We examine the recent results and compare Alaris' valuation to Canadian royalty and US BDCs to show that it is undervalued currently.

All values are in CAD unless noted otherwise. The ownership of this stock is generally restricted to Canadians .

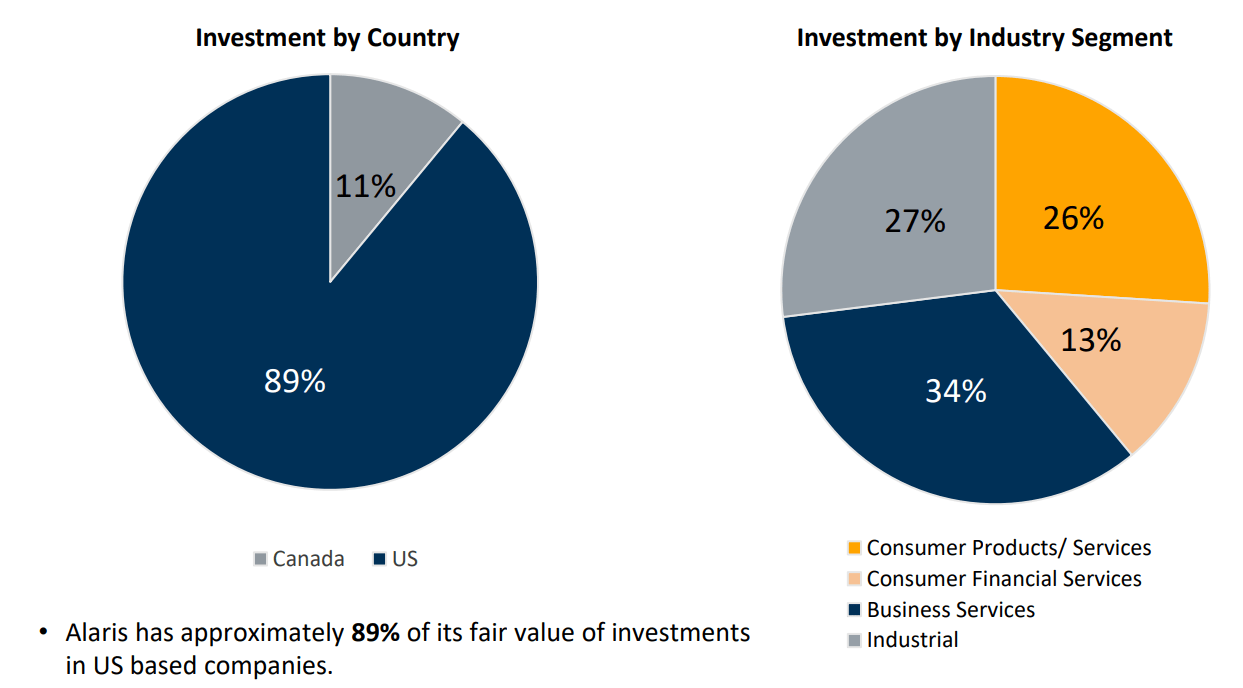

Alaris Equity Partners Income Trust ( AD.UN:CA ) invests in private companies looking for a shot of liquidity. Alaris extends these funds primarily in exchange for preferred equity, but at times they are funneled via common equity, subordinated debt and promissory notes. The majority of this Canada-based company's investments are in the United States, with the Business Services sector forming the bulk of them.

{kind=link}

The profile of a typical business that Alaris invests in, is that of a family or individual controlled entity, looking for the capital boost for growth, generational transfers, buyouts etc . The existence of these businesses is generally not in peril when they approach our protagonist. In return, Alaris receives periodic distributions or interest, depending on the type of investment they make in the company. These payment amounts are determined 12 months in advance, and adjusted annually based on top-line metrics such as net sales or gross profits etc. This payment pre-determination does not hold true in cases where Alaris is a common equity holder. The revenue in those cases depends on the cash flow and dividend declaration of the respective businesses. Besides the regular inflows, the preferred equity investments generally include a premium on exit or redemption for Alaris.

August 2023 Presentation

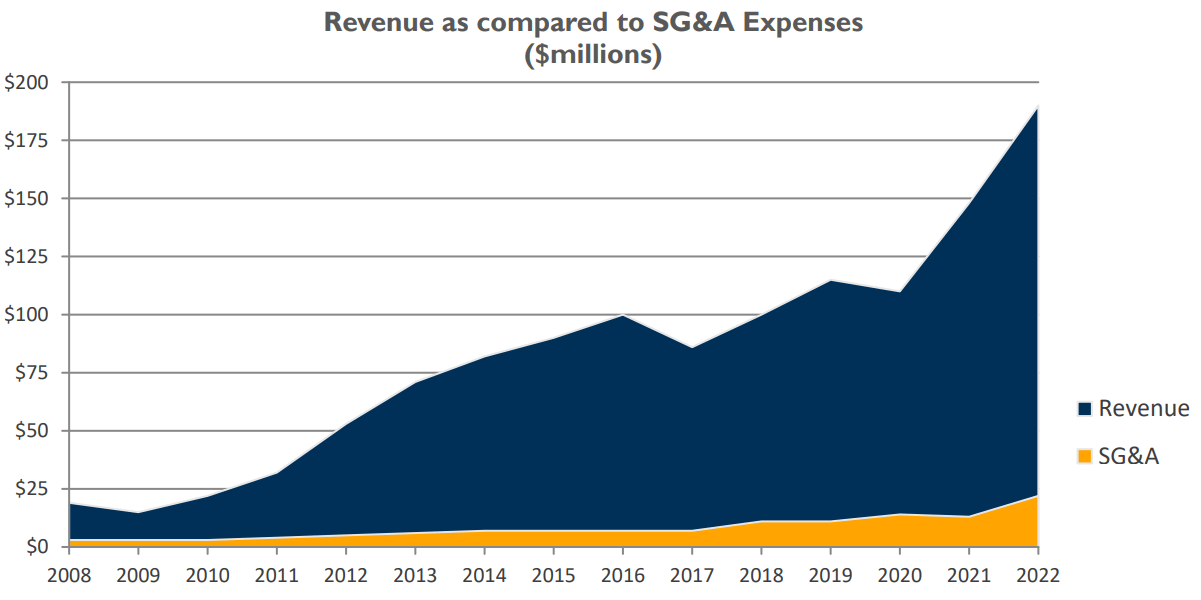

Alaris boasts of a streamlined structure with regards to expenses with only 18 employees. Additionally, since the partners retain control over their businesses and operations, expenses for Alaris are limited to monitoring of their investments and hence are limited in nature.

{kind=link}

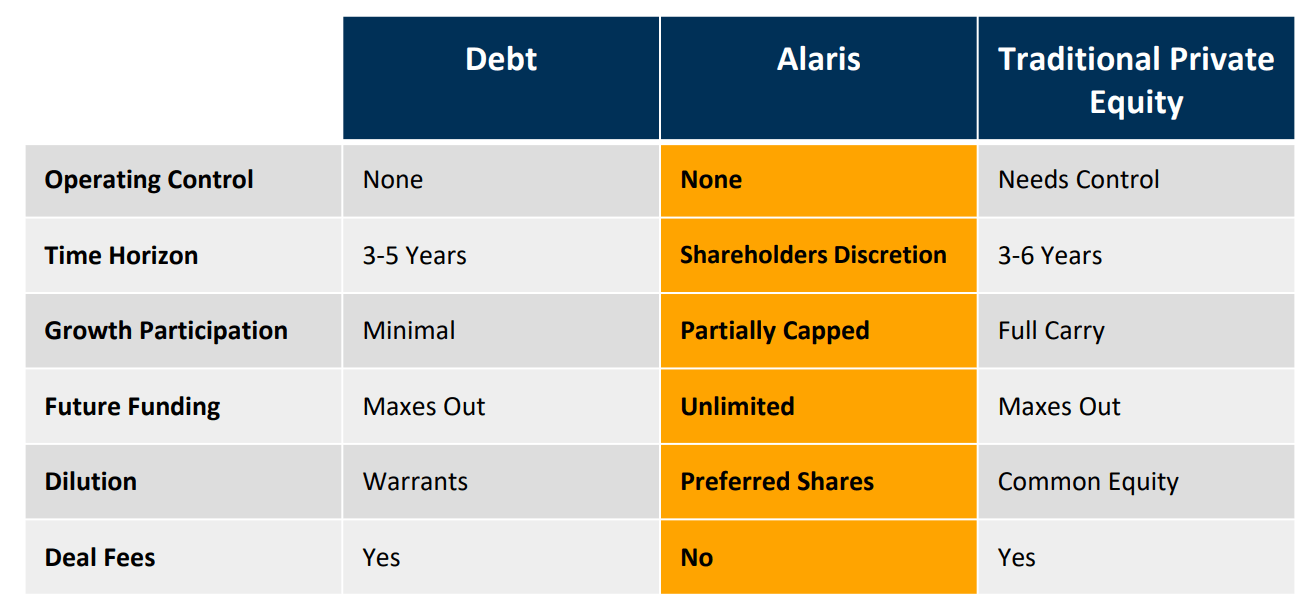

Alaris identifies itself to be a source of funding that falls between debt and traditional private equity and lays down the reasons in the following graphic.

{kind=link}

Prior Coverage

We reviewed the Q3-2022 financial results of this company at the beginning of this year and the last eight months have not been kind to it.

Seeking Alpha

We liked the appeal of its close to 8% distribution yield at the time, supported by its sub-50% payout ratio and a solid revenue base. We only held the debt of this company at that time and were prepared to own the common shares when the setup was compelling enough. Our concluding thoughts to that piece laid out our sentiments on the two modalities of investing in Alaris.

Alaris has failed to find a new investor base after the move to becoming an income trust. The current price to operating cash flow is the at the lowest multiple outside of the COVID-19 crash. The current price to tangible book value is also showing a similar symptom.

Gone are the days of euphoria at 2.5X tangible book value. What we are left with is a beaten down company with gobs of free cash flow. The stock is worth considering for tax deferred Canadian accounts and the debentures are even stronger plays for those that emphasize safety. We own the debentures and will consider the common units if we get the right setup.

Source: Alaris Equity: Solid 8% Plays For The Canadian Income Investor

We did become buyers of the common stock since then, and we review the recently released Q2-2023 results in light of that.

Recent Results

Alaris added Sagamore and FMP to its list of partners subsequent to Q2-2022, while KIMCO and FNC investments were redeemed. The total number of partners remained at 19, with the top 5 continuing to contribute close to 50% of the inflows.

August 2023 Presentation

Body Contour Centers formed a more substantial 17% back in Q2-2022, however, in Q1-2023 Alaris redeemed its US$156 million preferred equity investment for a US$9.3 million realized gain. US$20.3 million of the proceeds were in cash, the balance US$145 million was in the form of newly issued convertible preferreds. The new preferreds will pay a 8.5% annual distribution in cash or kind, and Alaris is also entitled to an annual transaction fee of US$1.5 million, with a fourth being due each quarter. There are other accretive terms to the new agreement which include participation in the common distribution above a certain threshold, along with additional performance-based returns that can be read in more detail in the Q2-2023 MD&A . Since the 2023 agreement has a lower distribution, it contributed to the overall decline in year-over-year revenues.

{kind=link}

Most of the decline is attributable to KIMCO however, an investment that was redeemed in Q2-2022 and for which Alaris received all the deferred distributions of $17.2 million at the time of redemption. Additionally, margin compressions due to the inability to pass on the steel price hikes to the customer put pressure on LMS third-party loan covenants. As a result it deferred its distributions to Alaris for the first six months of 2023. Alaris expects distributions to resume from this quarter due to normalizing of the steel prices, and the repayments of the deferred amounts to start in early 2024. The distributions from the new partners, along with the strong USD helped offset some of the above declines and the redemptions that preceded Q2-2023.

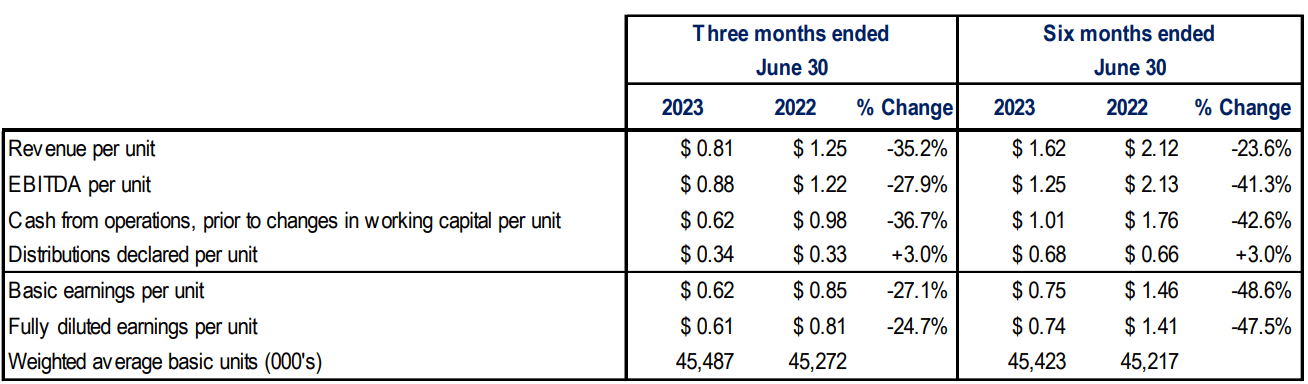

The decrease in revenue was partially offset by the increase in the fair value of the investment holding, but the year-over-year EBITDA was still lower by a whopping 28%.

{kind=link}

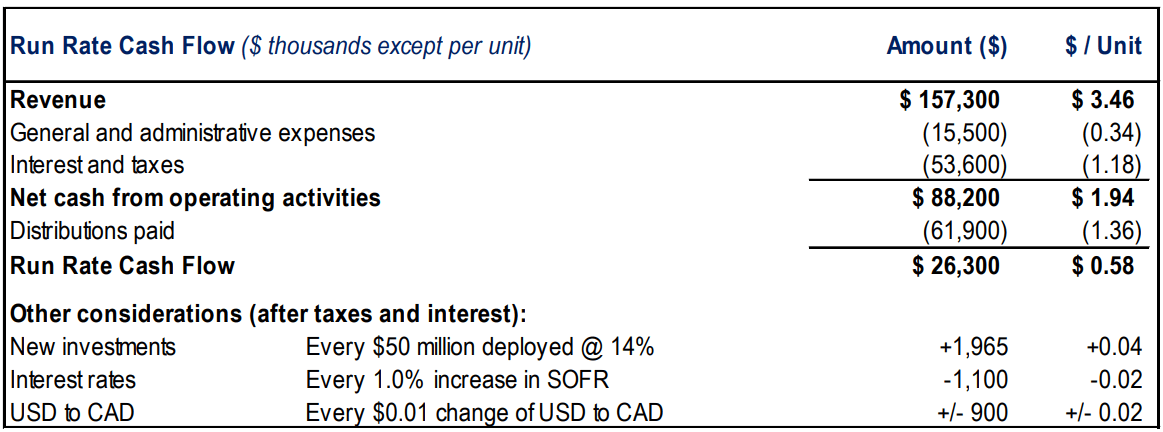

What also did not help was the foreign exchange loss in Q2-2023 versus the gain in the prior comparative quarter. $13.7 million in litigation costs for Sandbox, added to their woes and the 41% decline in the year to date numbers. But they finally put the Sandbox matter to rest, so they have that going for them, which is nice. The first half of the year has been littered with few one-time events, but Alaris laid out what it expects its normal to look like for the next 12 months.

{kind=link}

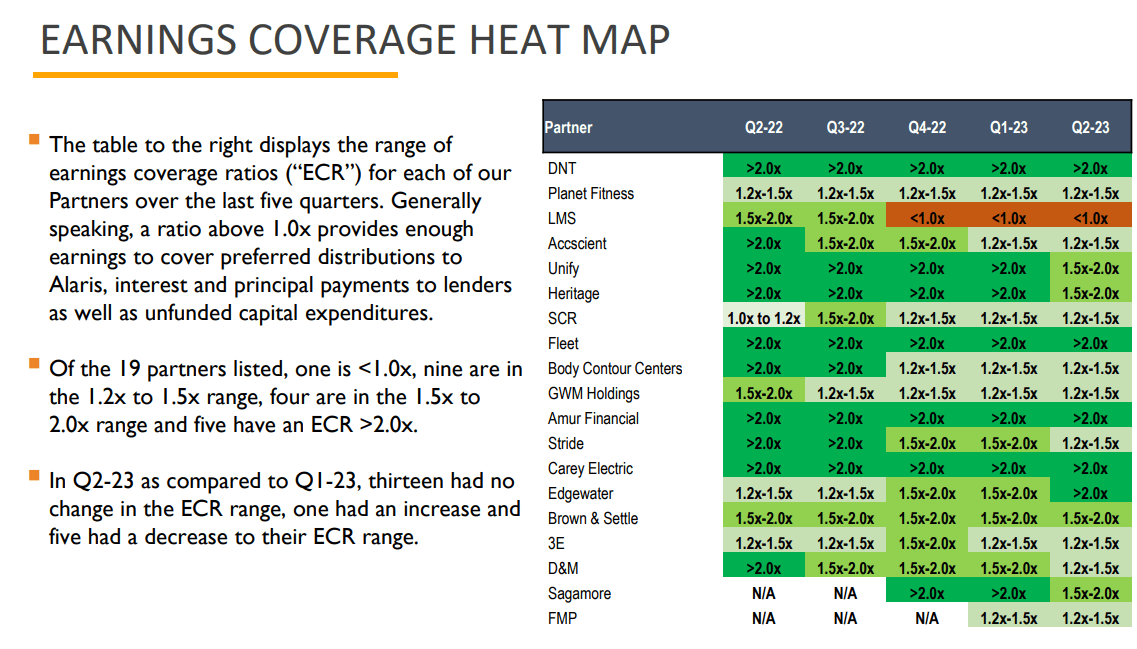

Which brings us to the sources of revenue and one of our favorite data points of the Alaris earnings report, the earnings heat map. It is very helpful as it reflects the financial health of the Alaris investments. When we wrote our previous piece, all the partners had coverage > 1.0X. We discussed the distribution deferrals by LMS earlier in this piece, and we can see the reason in the graphic below.

{kind=link}

While all the rest are comfortably over 1.0X, several have come down a notch compared to Q3, the quarter we last covered.

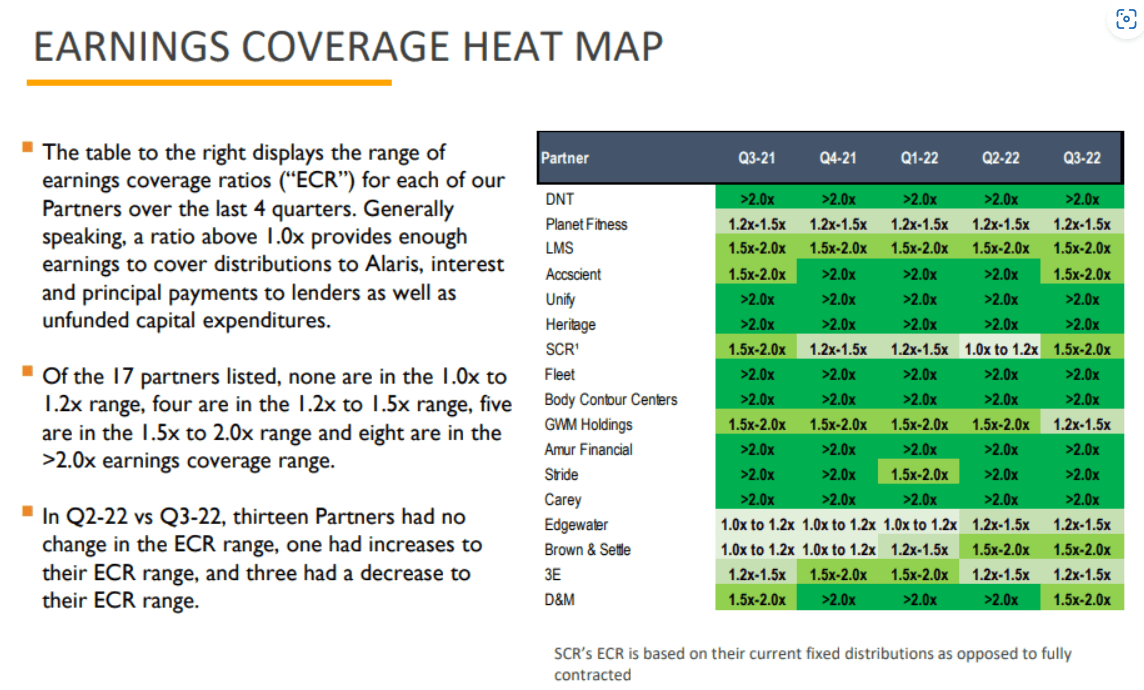

{kind=link}

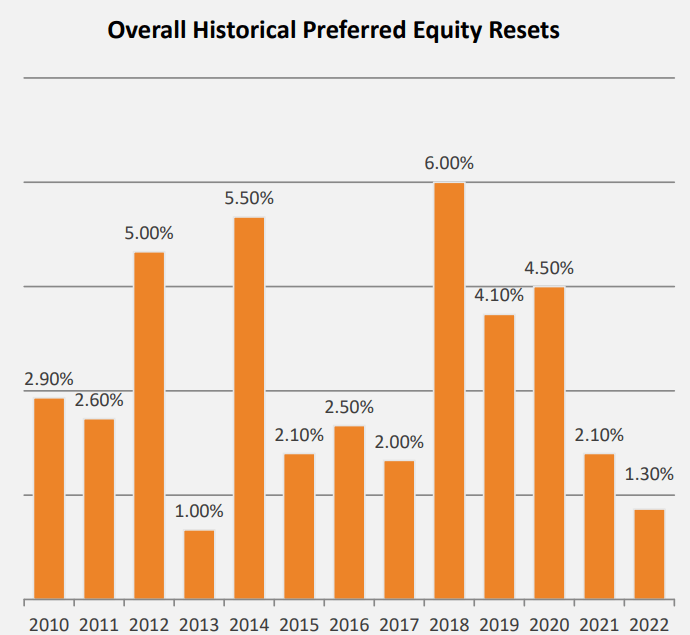

Multiple sub 1.0X partners were a norm for this company prior to 2021, so the current situation is still a step-up. Additionally, preferred equity resets while accretive to Alaris, likely do increase pressure on the coverage ratios of the partners.

{kind=link}

Valuation

Alaris increased its quarterly dividend to 34 cents from 33 cents at the end of last year. That, coupled with the decline in stock price now has the Alaris common stock yielding over 9% (based on a $15.08 stock price). The decline in revenues and the costs associated with settling the Sandbox litigation, however, pushed the payout ratio to 85% versus the 39% in Q2-2022.

The Actual Payout Ratio (2) for Alaris for the six months ended June 30, 2023, was 85%, an increase from 39% in the comparable period of 2022, primarily due to decreased revenue per unit and increased general and administrative costs both as discussed above. Excluding the settlement and associated legal costs in the six months ended June 30, 2023, the adjusted ratio would be 62% as compared to 85%.

Source: Q2-2023 MD&A

Alaris expects its regular payout rate to be around 70% when it is business as usual, which it has not been in the first half of this year. The numbers have been impacted by events such as the Sandbox litigation and the prior year KIMCO redemption. Alaris functions as a de facto royalty company due to its exposure to the top line metrics of its partners. On a forward P/E comparison, it is one of the cheaper Canadian royalty companies. Trading at close to 8X forward P/E, it is cheaper than Diversified Royalty Corp ( DIV:CA) , Boston Pizza Royalties Income Fund ( BPF.UN:CA ) and Pizza Pizza Royalty Corp. ( PZA:CA ).

If we take the stand that it is more like a BDC and compare it to some of the mid-quality US names like FS KKR Capital Corp ( FSK ), Pennant Park Floating Rate Capital Ltd ( PFLT ), and Pennant Park Investment Corp ( PNNT ), it is still the cheapest of the lot on price to tangible book values.

That discount offers a great buffer, and generally you have not got Alaris this cheap in the past. Recession likely does impact all of Alaris' investments but a generalized top-line exposure alongside the discounted valuation makes this good enough to play. We also believe the US Dollar will go higher over the coming months and that will boost the company's revenues. Alaris has hedged a small portion of its US Dollar exposure and its strengthening should be beneficial. We like it here and have bought a little of the common equity and will add if it goes lower. Alaris gets a 4 on our potential pain scale.

{kind=link}

Our primary exposure remains the debentures (discussed more in the last article) which are a safe source of income in our view.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Alaris: A 9% Yield Worth Biting On