ALB - Albemarle Still Has Options After The Liontown Resources Fiasco

2023-10-18 01:03:32 ET

Summary

- Albemarle has decided to pull out of its non-binding agreement to acquire Liontown Resources, signaling market disappointment.

- The company could explore other prospects for acquisition to increase shareholder value.

- Three potential prospects for Albemarle include Pilbara Minerals, Mineral Resources Limited, and Livent Corporation.

Back in early September of this year, I found myself feeling bullish about natural resources company Albemarle ( ALB ). At that time, the company had announced a non-binding agreement to acquire lithium mining operation Liontown Resources ( LINRF ) in a deal valued at $4.3 billion. I lauded the transaction as incredibly bullish for the company because, although operations were still limited, growth potential was tremendous and the long-term outlook for the lithium space was appealing.

Since then, management has had time to evaluate the potential purchase and, due to reasons we don't know entirely, has ultimately decided to pull out of this transaction. Initially in response to this development, shares of Albemarle moved higher by roughly 2.7%, while shares of Liontown Resources dropped approximately 7%. This is a clear signal of how the market feels about the deal falling through. But to be perfectly honest, my opinion is the exact opposite. In the near term, the market may rejoice at this change. But unless Albemarle can find some other prospect to acquire, I would argue that the investment opportunity facing investors is not as appealing as it otherwise would be. The good news is that there are some prospects that the company could target now. And while nothing is guaranteed, investors should keep a close eye on them.

A look at the news

According to a press release issued on October 15th, the management team at Albemarle had decided not to pursue its non-binding offer to acquire Liontown Resources for the $4.3 billion it initially agreed to purchase the company for. Management was given ample time to evaluate the transaction and they even went so far as to thank the Liontown Resources team for the cooperation that was offered up. Specifics were not mentioned as to why the deal fell through. But management did say that it noted, ‘growing complexities associated with the proposed transaction as a factor in its decision’.

Leading up to this, there was some concern that the deal would fall through. The most significant argument involved natural resources billionaire Gina Rinehart and her decision to use a company called Hancock Prospecting to acquire a significant stake in Liontown Resources in recent weeks. The most recent update indicated that her firm ended up buying 19.9% of the company’s outstanding shares. This is an important threshold because, any number above this, would then force the company, according to Australian law, to make a bid for the entirety of the firm. And while the deal still could have gone through theoretically with her having this stake, the odds started to stack up against Albemarle since they would likely need a 75% shareholder vote in order to get the deal approved.

Other opportunities abound

Regardless of why this opportunity did not come to pass, it does not change the fact that Albemarle is a tremendous producer of lithium. In 2022, the company produced 34,000 metric tons of lithium across the world, with 22,000 metric tons of it coming from Australia alone. Because of the rising price of lithium, 68.4% of the company’s revenue last year came from the metal. That was $5 billion and it dwarfed the $1.14 billion in revenue generated from it just two years earlier. But as I wrote in the aforementioned article regarding the transaction, the lithium market looks incredibly appealing on a forward basis, with a surge in electric vehicle production that is anticipated over the next several years driving up demand and, in turn, prices.

Technically speaking, Albemarle does not need any other lithium purchases in order to do well for itself. But acquiring as much in reserves as it can will only help increase shareholder value. One option for the company to explore would be to buy within. It currently owns a 49% stake in the Greenbushes mine, which happens to be the largest producing hard rock lithium mine on the planet. Management has even gone so far as to state that increasing this ownership is a possibility at some point down the road. In the long run, its growth in reserves that will result in value for companies in this space. But in the near term, management is doing what they can to grow output at that property. In May of this year, for instance, they even stated that they are working to double the lithium hydroxide output that the company captures from its operations in Australia.

The very fact that management even made a bid for another company, however, underscores just how they are thinking about major expansion efforts. Buying up the competition is not necessarily a bad idea. Since the Liontown Resources deal has clearly fallen through, however, investors would be right to question what other prospects might be on the table. To try and figure this out myself, I decided to take a look at the universe of lithium opportunities that are on the market today. I found countless companies, ranging from some with market capitalizations of $10 million or less, up to ones in excess of $10 billion. So I decided to narrow down my search based on two primary criteria.

The first is that I decided to only focus on prospects that have a market capitalization of between $2 billion and $8 billion. This range is between being just under half the size of Liontown Resources to being nearly twice its size. This ruled out some of the major deals that are out there and it ruled out many smaller firms. My rationale behind this is that the company clearly set its own criteria when looking at Liontown Resources to begin with, and I have a difficult time believing that it would radically change that criteria now.

{kind=link}

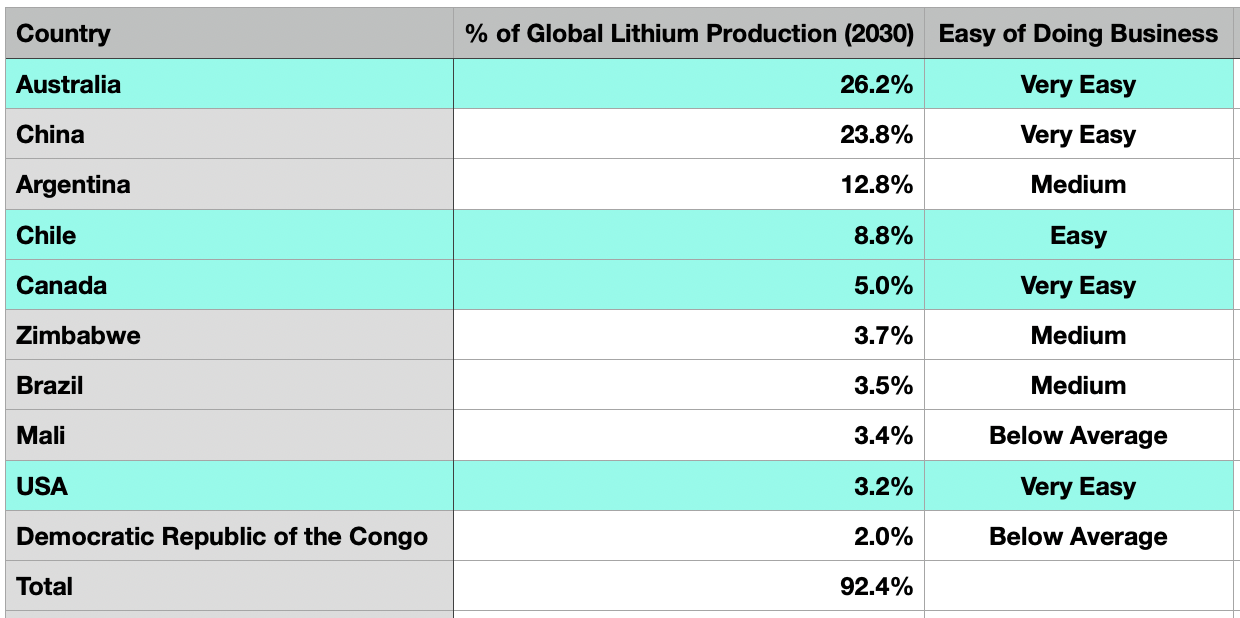

This still does leave a number of different prospects. But there was one more thing that came to mind. The fact of the matter is that not every country is easy to do business with. Some nations are very restrictive about foreign companies operating within them. Others are strict when it comes to natural resources. And others have significant amounts of corruption that can be difficult to deal with. So to narrow down the opportunities further, I relied on the Doing Business 2020 report. Within that report, there is a ranking of businesses from those that are below average to do business with to those that are very easy to do business with. I cross paired this list of countries with those that are slated to account for the largest portion of lithium production globally by the year 2030. As you can see in the chart above, the 10 largest producers of lithium by the year 2030 are expected to account for 92.4% of all lithium production globally.

What I did was rank these countries based on how easy they are to do business with. And from that point on, I removed from the list any country that was not categorized as either ‘Easy’ or ‘Very Easy’. This does unfortunately remove some major lithium production nations from the list. The most significant omission then would be Argentina, which is expected to account for 12.8% of global lithium production by 2030. It also excludes Zimbabwe, Brazil, Mali, and the Democratic Republic of the Congo. China is, interestingly, listed as being ‘Very Easy’ to do business with. However, I have also decided to remove it from the list. Although Albemarle does have some assets in China, they account for only 5.6% of the company's long-lived assets. That is fairly small in the grand scheme of things. For instance, 41.7% of its long-lived assets are in Australia, while 26.4% are in Chile.

The reason why I decided to exclude China from the list is because of the country has, itself, been on a massive buying spree when it comes to lithium. Since 2018 and through late August of this year, 20 different lithium mines have come up for purchase across the world. Chinese firms purchased ten of these for a combined $12.3 billion. This makes sense when you consider that China leads the way in electric vehicles, but it is also quite troubling. One country controlling so much of a crucial natural resource, which is not the only crucial natural resource that China has focused on in recent years, can create significant issues in the long run. And regulators have not failed to notice. Australia, for instance, recently prevented a Chinese linked company from acquiring Alita Resources. And in November of last year, the federal government in Canada ordered three Chinese companies to divest themselves from three junior Canadian lithium explorers. Given the country's thirst for lithium and pushback it is receiving from other nations across the globe, I would argue that a company like Albemarle would have significant difficulties not only purchasing lithium assets there, but it would also face severe regulatory oversight.

Our three prospects

{kind=link}

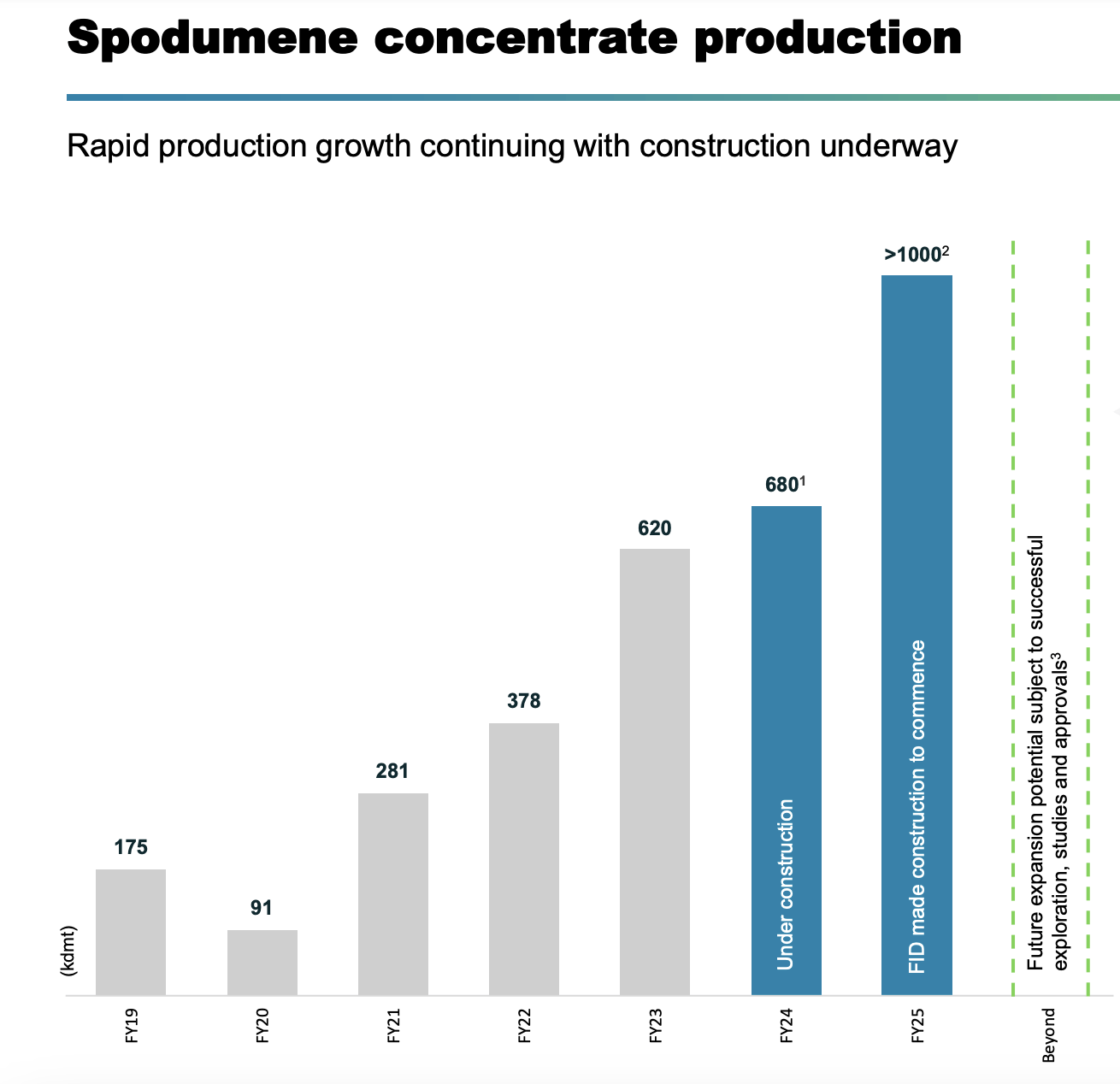

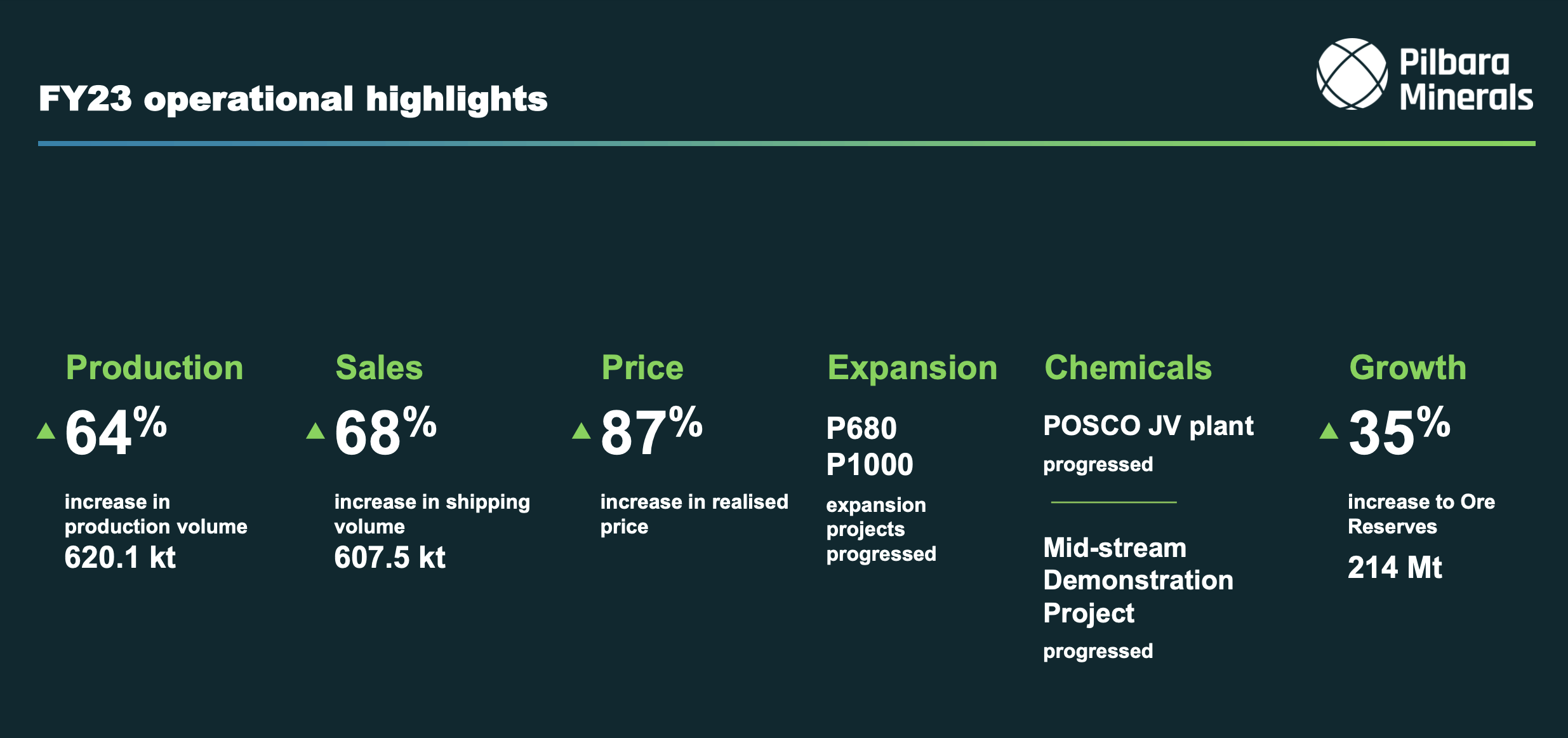

After putting these different criteria in place, I narrowed the list of firms down to three. The first and largest of these is Pilbara Minerals Limited ( PILBF ). With a market capitalization of $7.9 billion, Pilbara Minerals is the largest of the three companies on the list. Based in Australia, Pilbara Minerals operates in a market that Albemarle is intimately familiar with and that is identical to what Liontown Resources is in. It's a major producer of lithium that has made the precious metal a major priority for shareholder creation. By investing significant amounts of capital into its lithium projects, the company saw its production jump by 64% last year from 378 kdmt per annum to 620 kdmt per annum. But the growth doesn't stop there. The company's objective is to grow output further to approximately 680 kdmt per annum in 2024 before growing it to more than 1,000 kdmt per annum in 2025.

{kind=link}

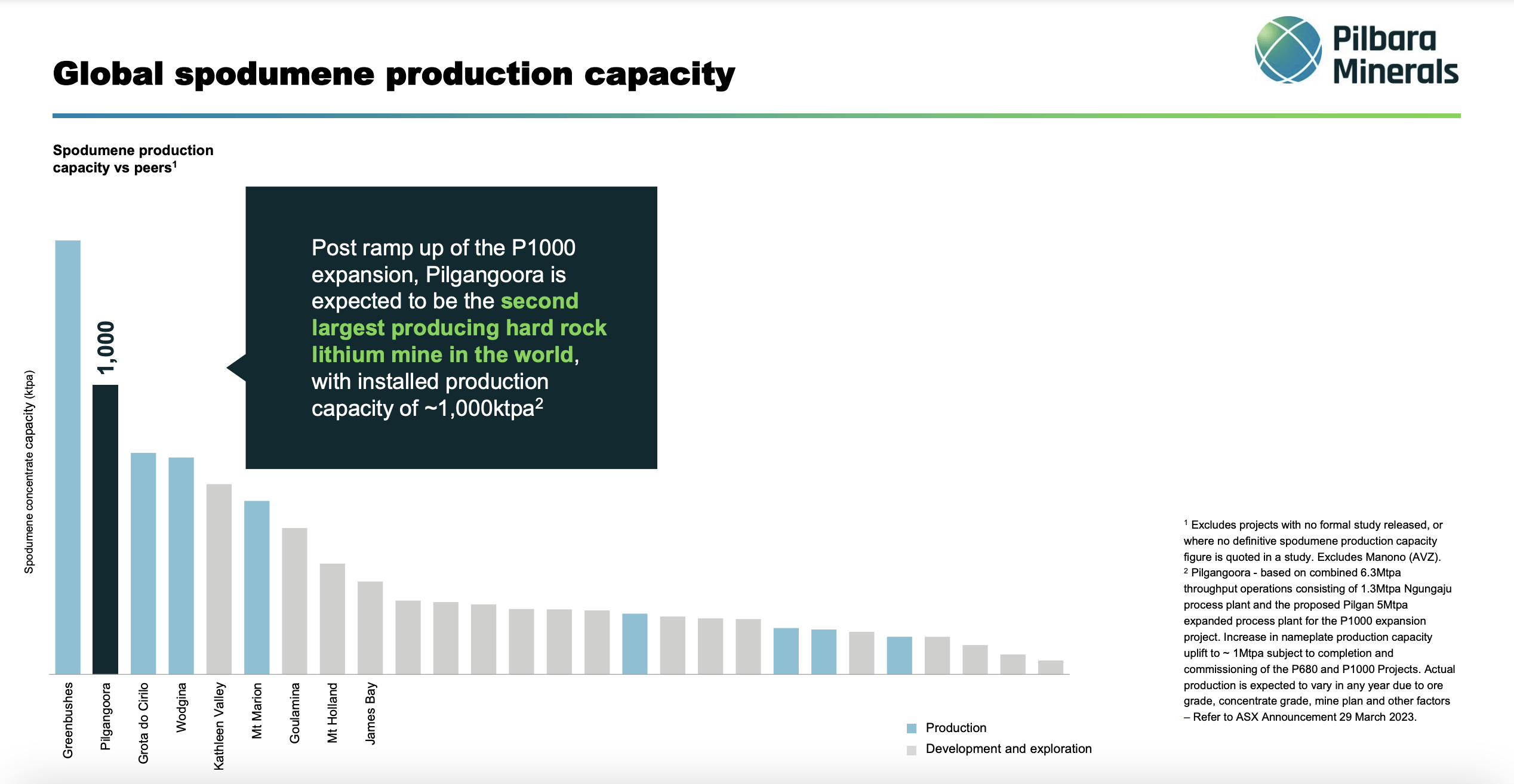

Following the ramp up of what management calls the company’s P1000 expansion, the Pilgangoora mine that the company owns will be the second largest producing hard rock lithium mine on the planet, only behind Greenbushes. The company has other operations as well, but these are really tied to what it does with lithium. For instance, it boasts a joint venture with Calix that could be categorized as midstream and that focuses on creating lithium enriched products. And it has a joint venture with POSCO in the downstream space to create 99% purity battery grade lithium hydroxide. The lithium hydroxide facility being produced will have total annual capacity of 43,000 tons of the product and the company at this time has the potential to capture up to 30% of the ownership in that joint venture. It's also possible that the Pilgangoora will continue to yield strong growth prospects in the years to come. I say this because, from 2022 to 2023, the company reported a 35% increase in the quantity of reserves at that location. That should increase the life of the mine, given projected annual output, by nine years to 34 years in total.

{kind=link}

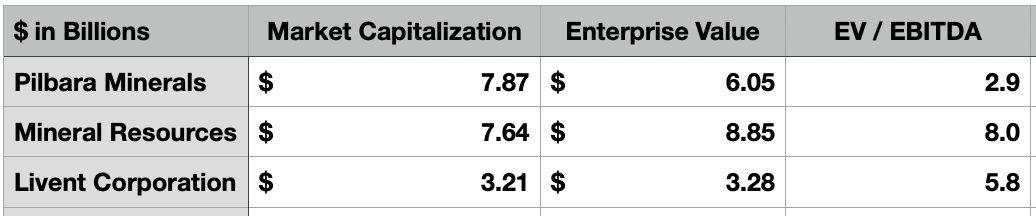

Even without growth, Pilbara Minerals is a large player in the lithium market. The company has cash that exceeds debt in the amount of $1.82 billion. So although it has a market capitalization of $7.9 billion, its enterprise value is only $6.1 billion. And in its 2023 fiscal year, the company was responsible for generating $2.10 billion worth of EBITDA. That implies an EV to EBITDA multiple of only 2.9.

{kind=link}

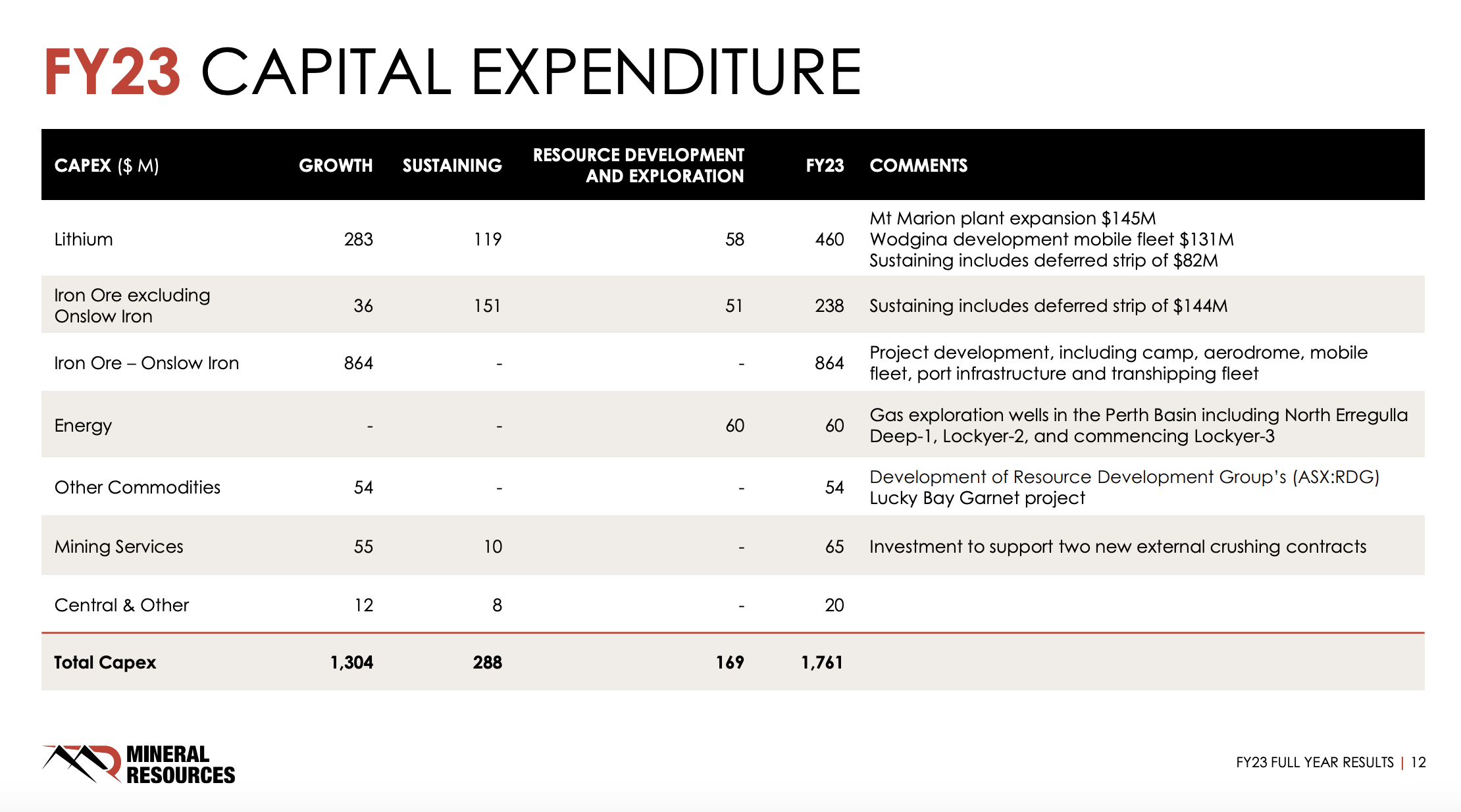

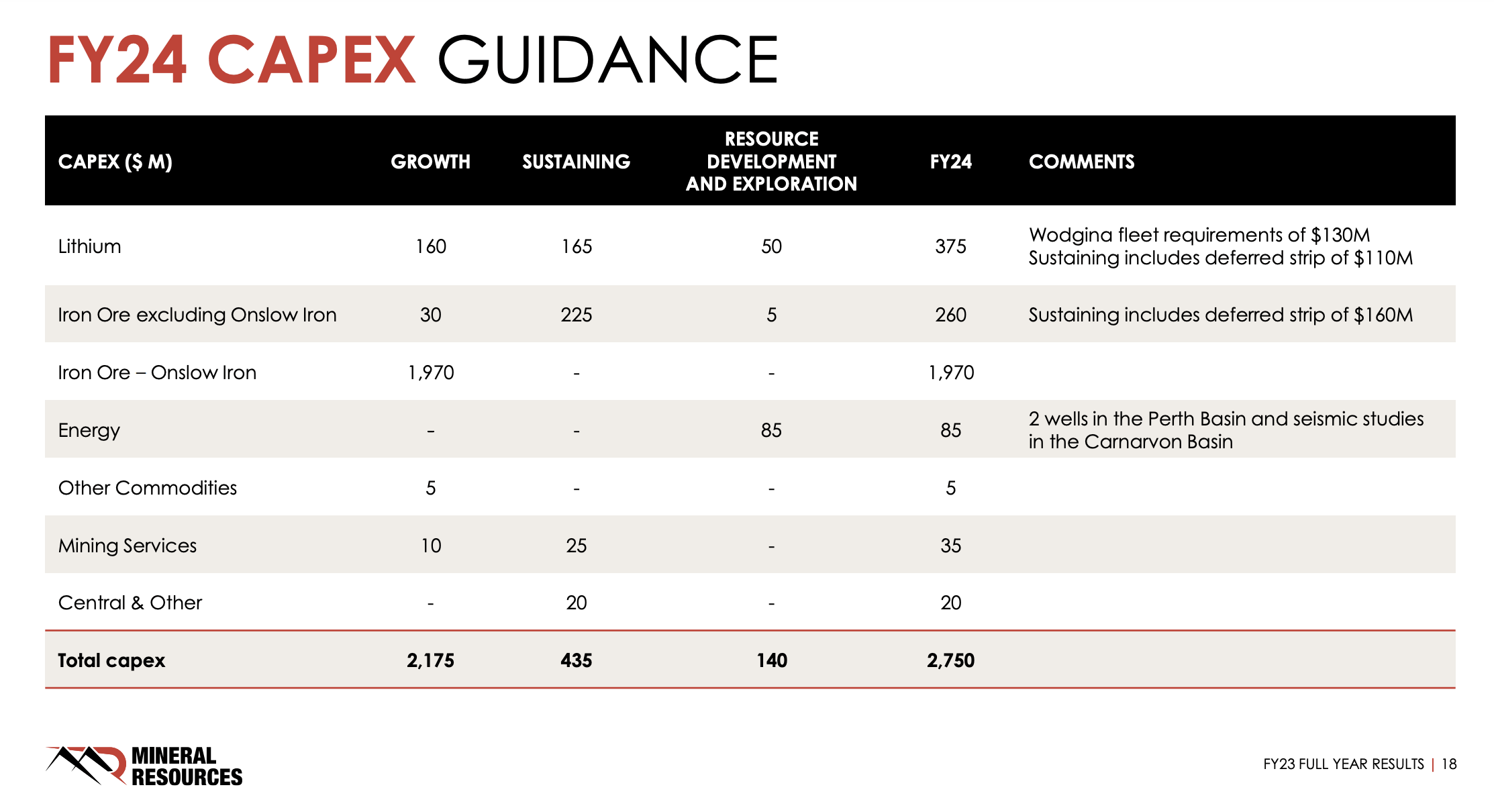

Next in line, we have Mineral Resources Limited ( MALRY ) ( MALRF ). With a market capitalization of $7.6 billion, it's nearly as large as Pilbara Minerals. But when you factor in net debt, its enterprise value is even larger at $8.9 billion. However, I think that this is less likely a prospect than the other two I am covering in this article. And this is because, although 75.5% of the company’s EBITDA came from lithium during its 2023 fiscal year, management is not investing all that heavily in it. In fact, the company seems to be much more interested in an iron ore. During the company's 2023 fiscal year, only 26.1% of its capital expenditures were focused on lithium. That compares to 62.6% that was focused on iron ore. For 2024, 81.1% of capital expenditures are expected to be directed toward iron ore, while 13.6% will be focused on lithium.

Mineral Resources Mineral Resources

{kind=link}

{kind=link}

This does not mean that management has not recognized the potential that exists in the lithium market. They most certainly have and they are focusing on growing their exposure to some extent. In the long run, the company wants to grow its SC6 production to 1Mtpa, placing it on par with Pilbara Minerals. But this pales in comparison to the 35Mtpa that it’s targeting for the Onslow Iron project that it’s a joint venture partner with Red Hill Iron Joint Venture partners Baowu, AMCI, and POSCO on. Based on the $1.11 billion in EBITDA that the company generated last year, it is trading at an EV to EBITDA multiple of 8.

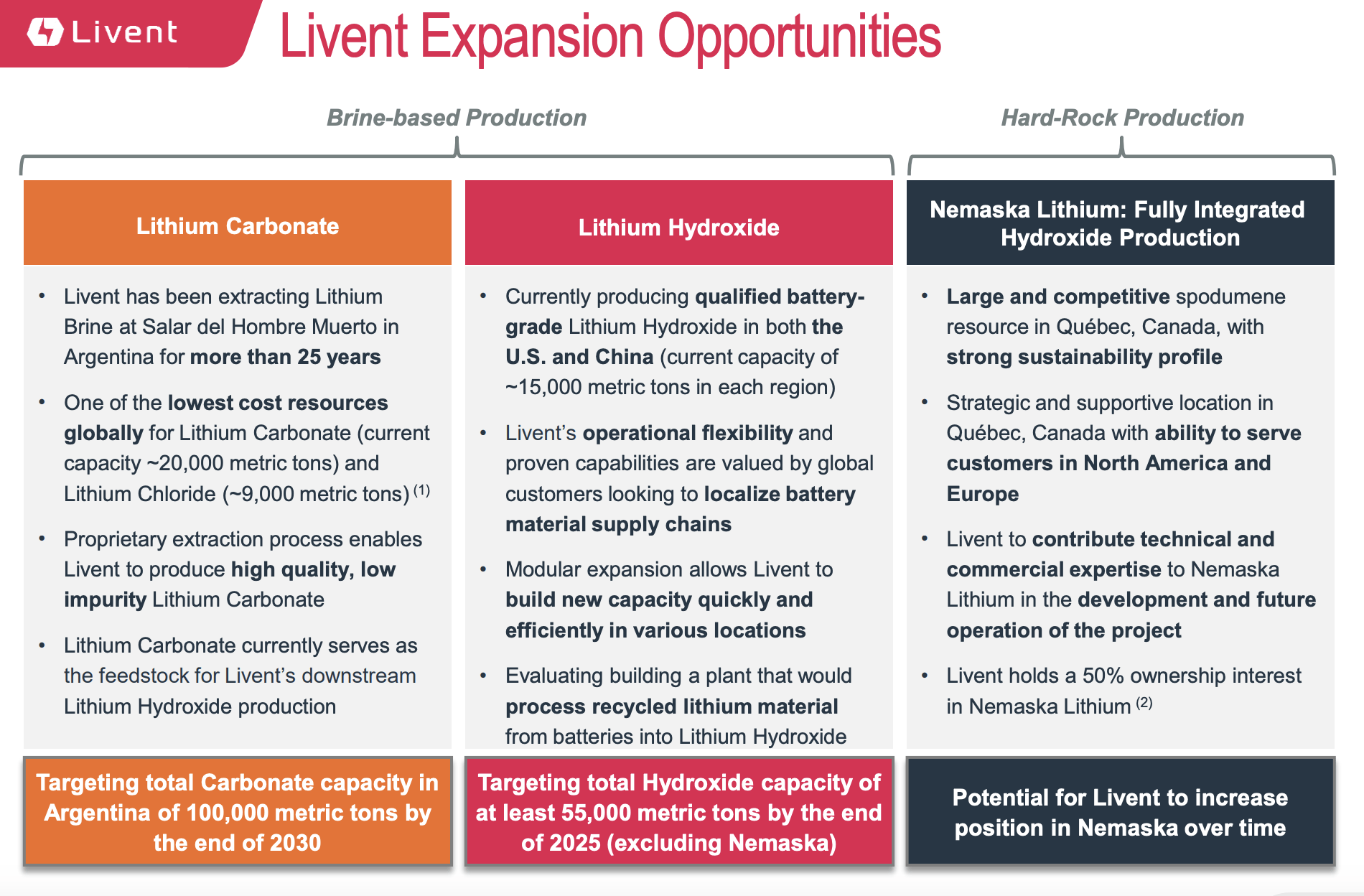

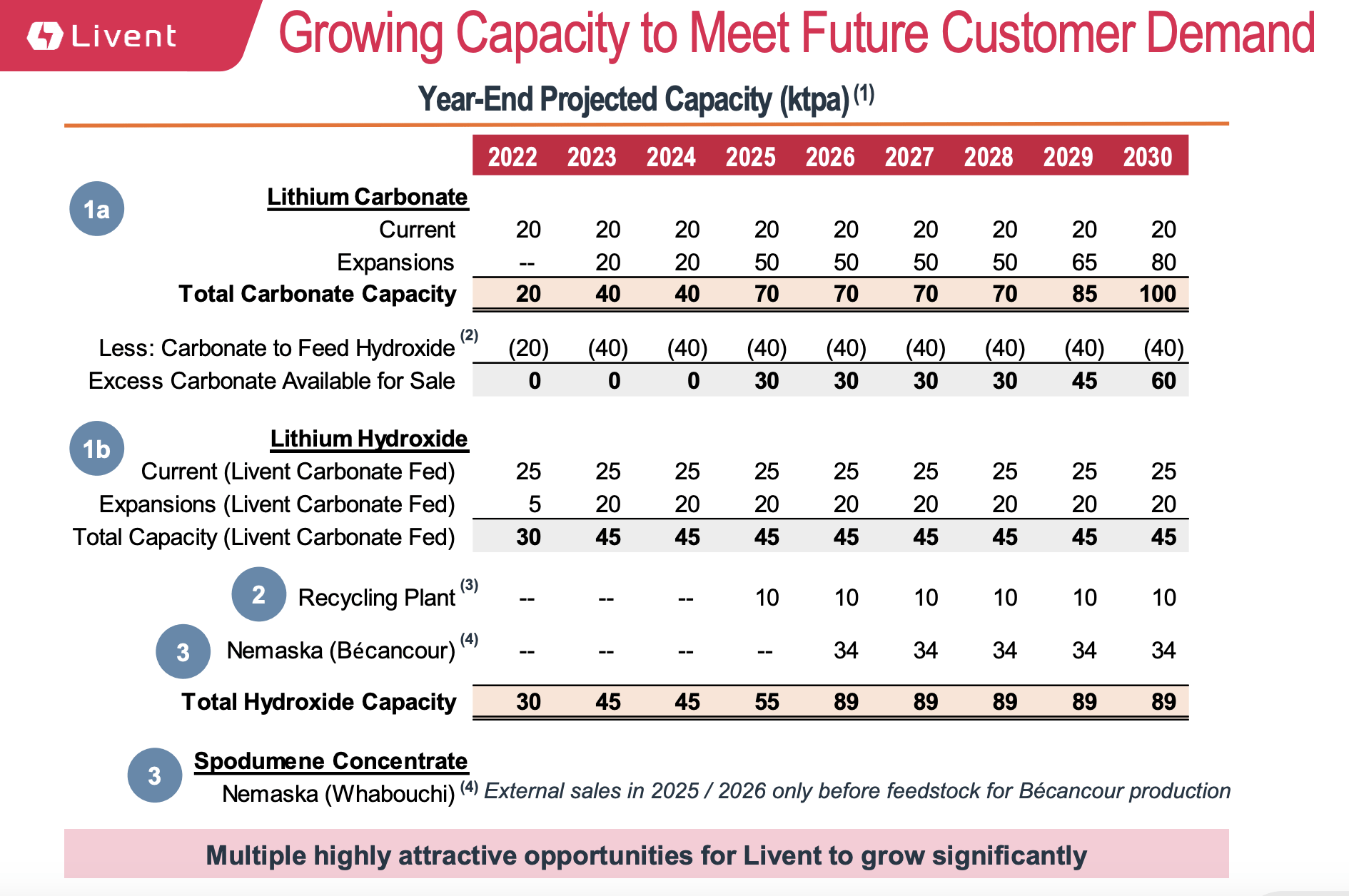

Lastly, we have the US-based Livent Corporation ( LTHM ). This one is a bit of a step back for me. Earlier in this article, I mentioned not focusing on companies that have a presence in certain nations, such as Argentina and China. Technically, Livent has a presence in both. When focusing on its brine-based production , it has 20,000 metric tons per annum of lithium carbonate capacity and 9,000 metric tons per annum of lithium chloride capacity in Argentina. The company also hopes to grow its exposure of lithium carbonate capacity up to 100,000 metric tons by the end of the year 2030. However, the company also has a significant operating history in that nation, with operations dating back more than 25 years. Any company that can navigate a less business friendly country that long deserves an exception in my book.

{kind=link}

In China, the company also has capacity of 15,000 metric tons of lithium hydroxide each year. The company's goal is to grow its lithium hydroxide capacity, excluding its Nemaska joint venture that it owns a 50% interest in, up to 55,000 metric tons per annum by the end of 2025. But that also includes growth on the 15,000 metric tons per annum of capacity that the company has in the US. Add on top of this the 34,000 metric tons of capacity for the aforementioned Nemaska venture, and only a small portion of overall output today comes from China.

{kind=link}

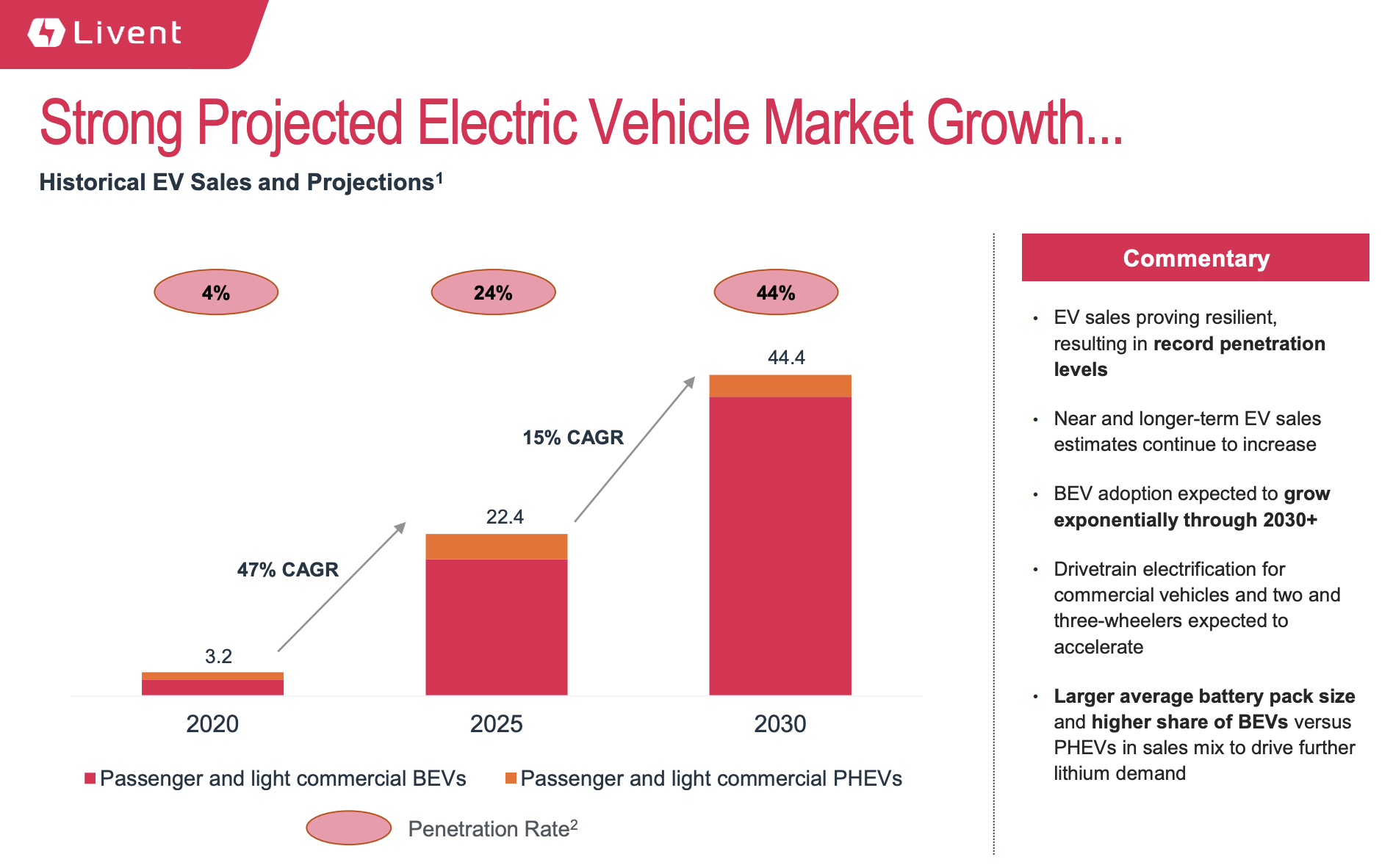

One thing that really struck me about this particular prospect is how much of A cheerleader it is for the lithium market. Management is forecasting annualized growth in the adoption of electric vehicles of 47% between 2020 and 2025, taking the global fleet from 3.2 million vehicles to 22.4 million and growing market share of electric vehicles from 4% to 24%. From that point on, it should grow another 15% per annum, hitting 44.4 million vehicles, or 44% of all passenger and light commercial vehicles, by 2030.

{kind=link}

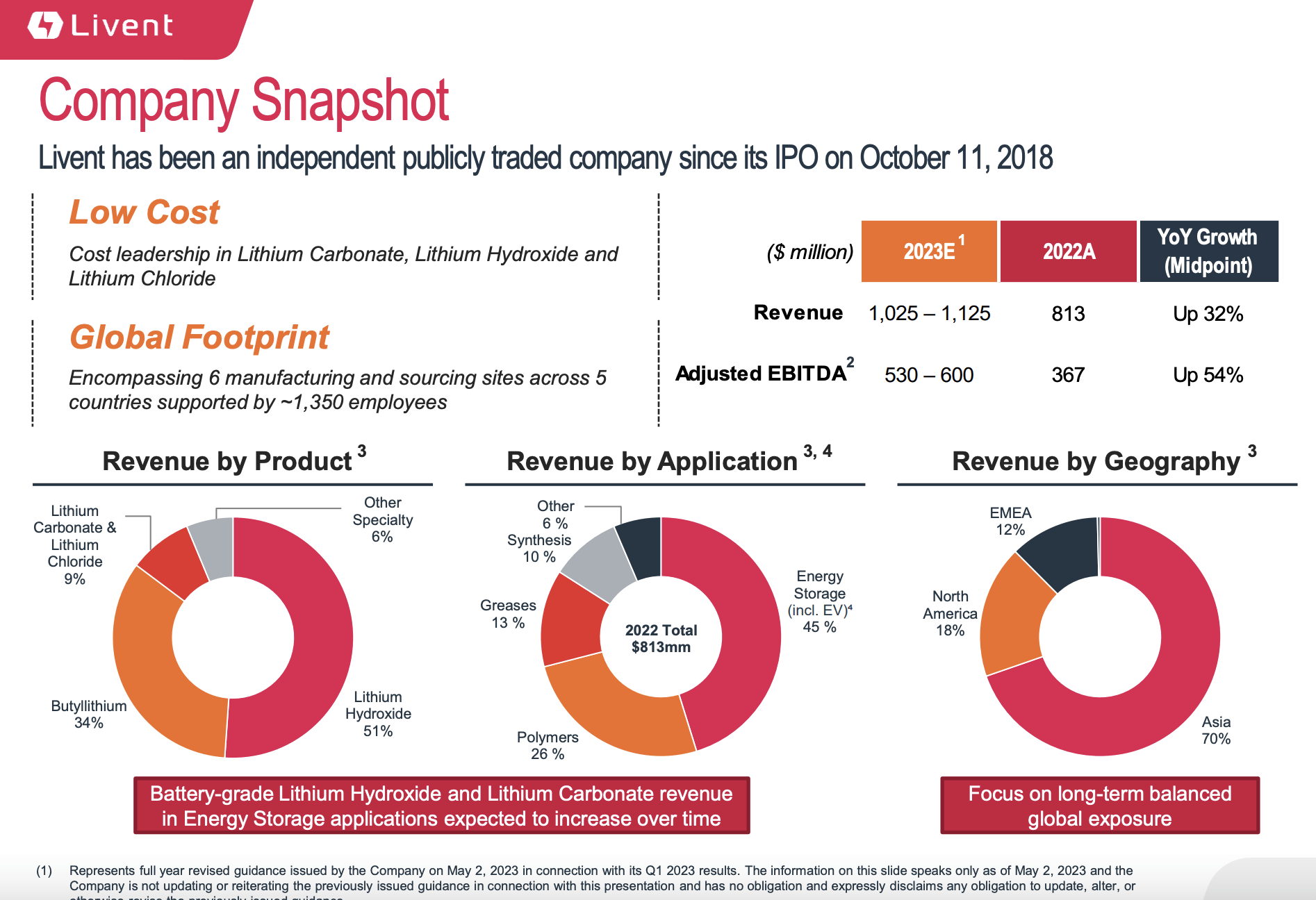

We should expect to see, then, a similar rise in demand for lithium hydroxide. Considering that, as of 2022, 45% of the company's revenue came from energy storage products, which included electric vehicles, with a total of 51% of its revenue coming from lithium hydroxide itself, and it's clear that management is in the right mindset. And this kind of mindset would definitely be appealing to Albemarle. While China most certainly will favor its own lithium production sources, it is also highly probable that the supply of lithium will not be high enough to meet demand over the next several years. And with Livent already generating 70% of its sales from Asia, the firm does have a nice foot in the door.

{kind=link}

Based on current estimates provided by management, EBITDA for 2023 will come in at between $530 million and $600 million. That's up from the $367 million generated in 2022. While this will almost certainly grow over the long run, using the midpoint of guidance for the year, we can see that the company is trading at an EV to EBITDA multiple of 5.8.

An obvious choice left out?

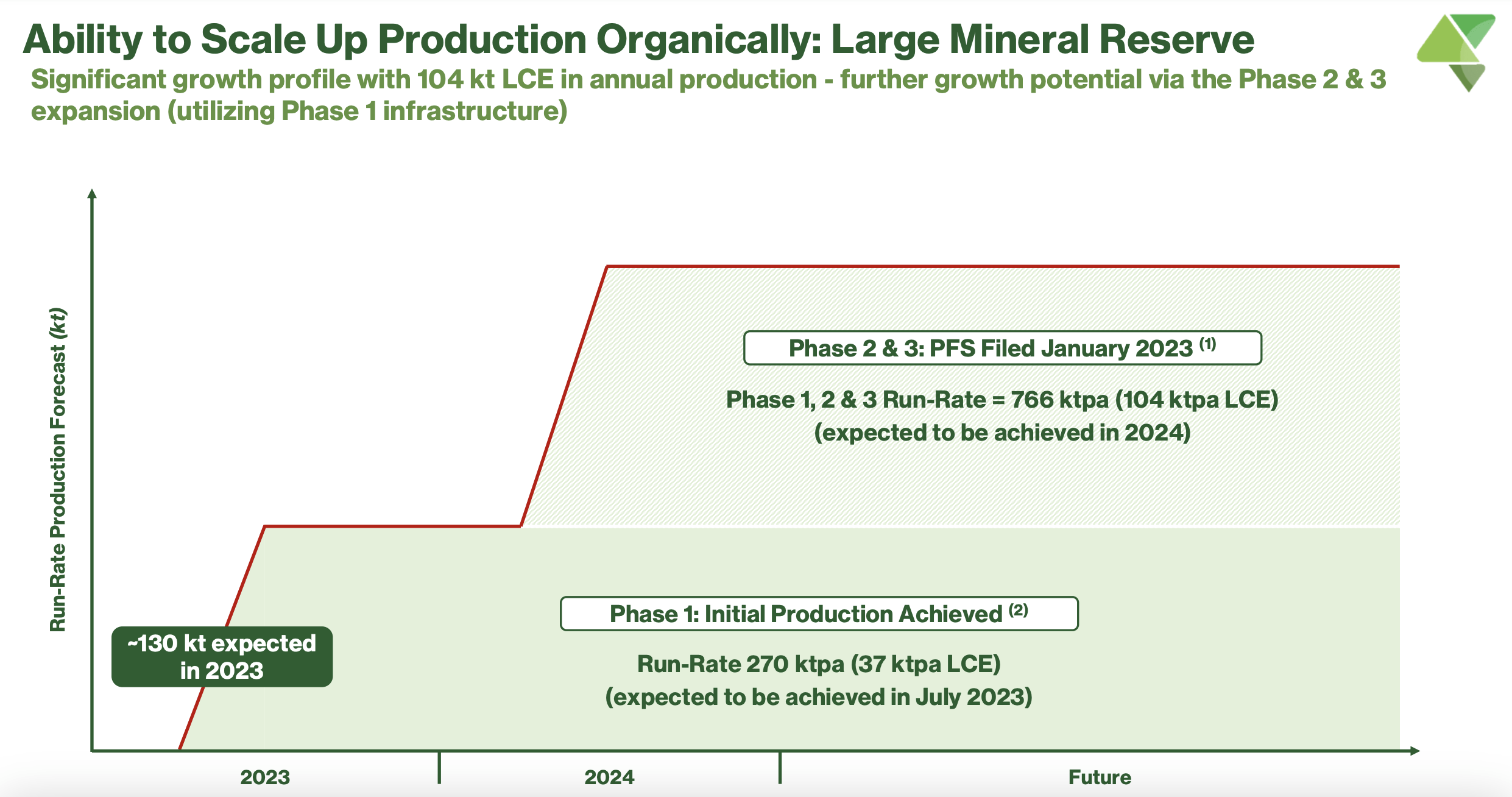

Those reading this article can justifiably point out that one company being left out is Sigma Lithium ( SGML ). This is because, even though the company meets the size requirement with a market capitalization of just under $3 billion, it is based out of Brazil. But when you consider that the company is currently looking for strategic alternatives , it does seem to stick out as an obvious prospect even with its focus on Brazil. Up until recently, Sigma Lithium was not producing any lithium. But this year in its entirety, the company is forecasting 130,000 tons of the product. In fact, they have already achieved an annual run rate of 270,000 tons per annum thanks to the initial production from Phase 1 of its production there.

{kind=link}

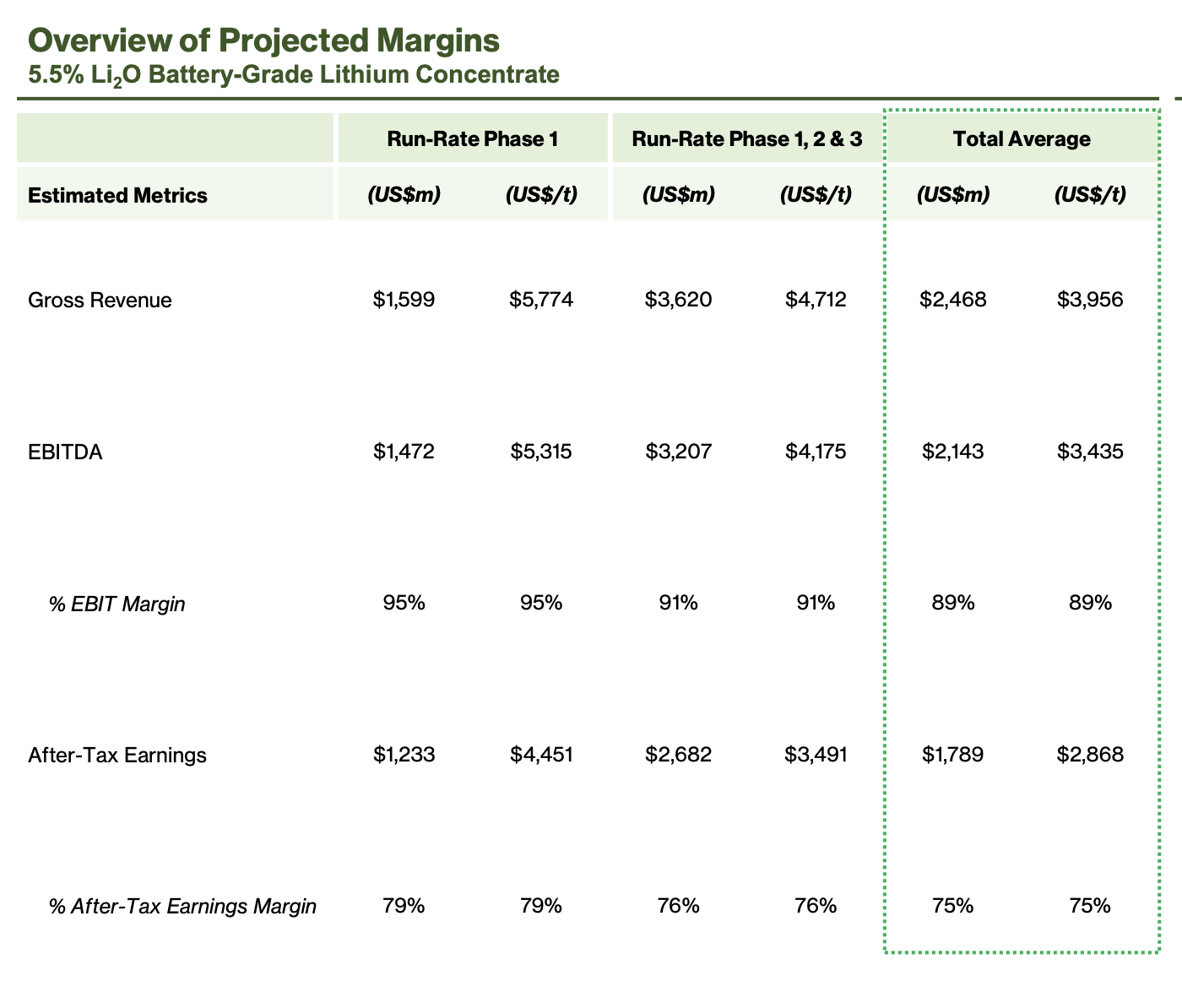

Future growth is currently anticipated. Phases 2 and 3 are expected to push annual production up to 766,000 tons sometime next year. And there is the prospect of a Phase 4 pushing production up even further. Management claims that the cash costs, excluding royalties and transportation costs, of some of the lithium it's producing will be amongst the lowest of any major project on the planet. And they are forecasting annual EBITDA from just Phase 1 alone of $1.47 billion, with the next two Phases pushing this up to $3.21 billion annually. But ignoring for a moment the fact that the company operates in a country rife with corruption, there's also the fact that, according to a press release issued just last month, there are already multiple interested parties looking at the company’s assets. Whether it was the deciding factor in Albemarle backing away from Liontown Resources or not, we did see the company step away from that particular purchase after only one major nuisance, Gina Rinehart, came into the picture. So it's unclear whether Albemarle is open to what could be a bidding war.

{kind=link}

Takeaway

Based on all the data provided, I must say that I am disappointed that the deal between Albemarle and Liontown Resources fell through. If it were for the fact that shares of Albemarle had already fallen quite a bit since the deal was announced, I would be inclined to downgrade the company because of this development. Having said that, the stock has dropped over 16% since announcing its non-binding offer for Liontown Resources, so that improvement from a pricing perspective makes up for this loss to some extent. Having said that, I would like to see some other deal come to the table. And I would say that it's quite probable that such a deal would involve one of the three companies that I focused on most in this article.

For further details see:

Albemarle Still Has Options After The Liontown Resources Fiasco