ALBO - Albireo Pharma: Elucidating The Ipsen Buyout (Rating Upgrade)

Summary

- Albireo Pharma, Inc. has entered into an agreement to get acquired by Ipsen.

- Bylvay is already approved for PFIC. Nevertheless, the stellar drug is poised to gain additional labels for Alagille syndrome and biliary atresia.

- Other younger pipeline assets for orphan diseases would add further value to the deal.

{kind=link}

The successful investor is usually an individual who is inherently interested in business problems. - Phillip Fisher (Warren Buffett's one of two mentors)

Author's Note : This is an abbreviated version of an article originally published in advance on Jan. 09, inside Integrated BioSci Investing for our members.

In biotech investing, it's an exciting time when you see your stock getting acquired by a larger company. After all, the acquisition price is typically 40% to 80% higher than the current market valuation. More importantly, the deal would allow the drugs to reach the most number of patients and thereby deliver hope in seemingly hopeless situations. The stock that illustrates the aforesaid phenomenon is Albireo Pharma, Inc. ( ALBO ). As you will see, Ipsen is set to acquire Albireo at a substantial market premium. In this research, I'll feature a fundamental analysis of Albireo while focusing on the deal.

{kind=link}

Figure 1: Albireo Pharma chart.

About The Company

As usual, I’ll provide a brief overview of the company for new investors. If you are familiar with the firm, I recommend that you skip to the subsequent section. As noted in the prior research ,

Operating out of Boston, Massachusetts, Albireo Pharma is focused on the innovation and commercialization of novel medicines to fill the unmet needs in orphan liver conditions. As shown below, the company has an interesting portfolio of two approved drugs and other early-stage developing therapeutics (i.e., A3907 and A2342). As the crown jewel of this pipeline, odevixibat (Bylvay) is authorized to treat the rare genetic liver condition, progressive familial intrahepatic cholestasis (i.e., PFIC) that is characterized by extreme itching. The other notable molecule is elobixibat, approved for the treatment of chronic constipation (of which Albireo receives royalty payment from EA Pharma).

{kind=link}

Figure 2: Therapeutic pipeline.

The Ipsen Acquisition

Today, Albireo disclosed that the company had entered into an Agreement whereby Ipsen would acquire all remaining shares of Albireo. With the acquisition, Ipsen can now take ownership of Bylvay to boost its rare (i.e., orphan) disease portfolio. As you know, Bylvay was already approved and launched in the U.S. and EU back in 2021 for PFIC.

In the U.S., Bylvay is approved for kids at least 3 years or older who are suffering from PFIC. In the EU, it's being launched for kids at least 6 years old. As you can see, pruritus (i.e., itching) can be quite cumbersome for patients afflicted by this genetic condition. Due to orphan exclusivity, there are 7 years of exclusive protection for Bylvay. Commenting on the deal, the CEO of Ipsen (David Loew) remarked:

We are excited about the potential of Albireo’s assets and scientific expertise, which we gain through this acquisition, and we believe this is a compelling growth opportunity for Ipsen. Our Rare Disease franchise is strengthened with Bylvay, which, in addition to being the first-approved treatment in PFIC, has two further indications being investigated in rare liver conditions that are underserved. Additionally, Bylvay and the clinical and preclinical novel bile acid transport inhibitors in Albireo’s portfolio complement our own pipeline in liver disease.

Bylvay for Alagille Syndrome

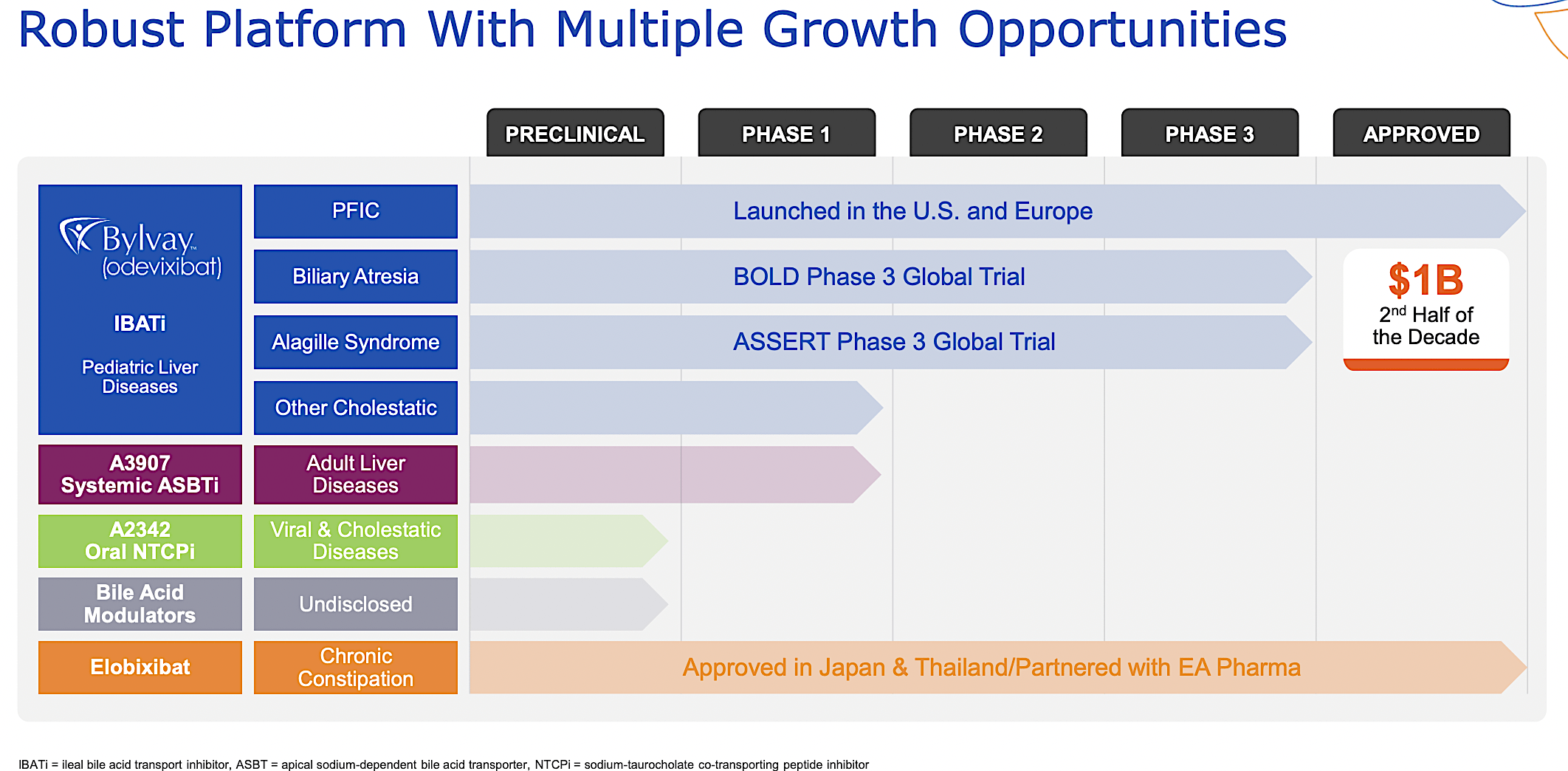

As you can appreciate, Albireo is expanding Bylvay's label for other rare diseases. One such condition is the rare genetic disorder, Alagille syndrome (i.e., ALGS), which causes a reduction in bile flows and affects different organ systems. Due to its therapeutic prowess, Bylvay posted robust clinical data for the Phase 3 (ASSERT) trial.

This past December, Albireo filed a supplementary application for Bylvay with both the EU and the US regulatory agencies. The next stop for Bylvay is another label expansion, which you can expect in either Q3 or Q4 this year.

{kind=link}

Figure 3: Massive Bylvay opportunities.

Other Albireo Assets

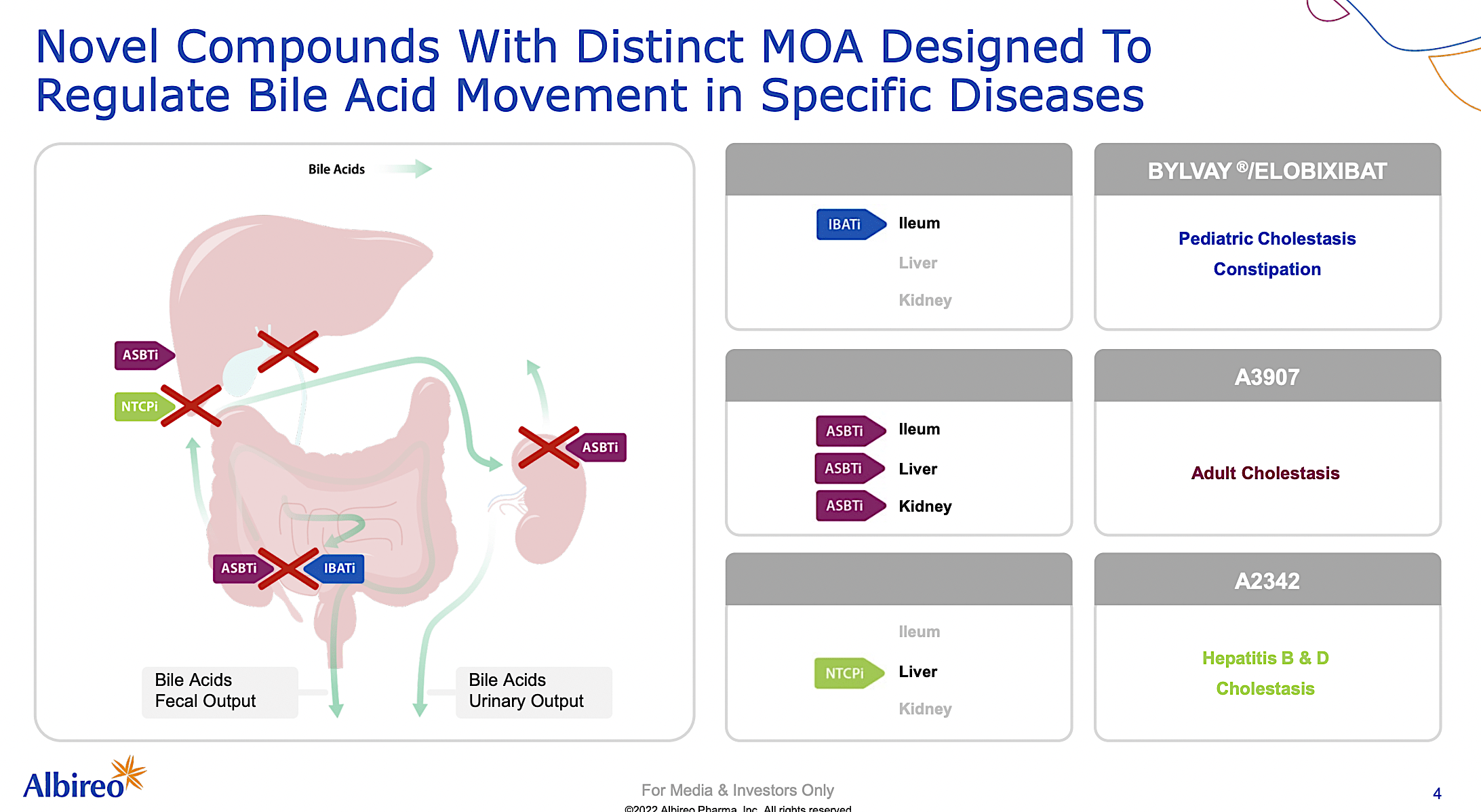

As part of the deal, Ipsen will also take ownership of all other clinical assets, including A3907 and A2342. As a novel oral systemic apical sodium-dependent bile acid transporter inhibitor, A3907 is currently being developed in the Phase 1 study for the liver disease known as primary sclerosis cholangitis (i.e., PSC) in adults. Ipsen believes that this molecule adds complementary to its portfolio of drugs.

Additionally, the other oral drug (A2342) is still in the preclinical study for other viral and cholestatic diseases (i.e., bile flow blockage conditions). Notably, this drug works by a different mechanism of action. Specifically, it inhibits the systemic sodium-taurocholate co-transporting peptide ((NTCP)).

Simply put, these earlier-stage molecules all work to deliver hope for bile diseases despite having different modes of action. More importantly, you can bet that the Ipsen partnership will fully unlock the value of these drugs for patients. Highly enthused by the deal, Albireo Chief (Ron Cooper) stated,

Unwavering dedication to patients and commitment to science have always been the north star for Albireo. This focus has driven us to develop and gain approval for Bylvay as the first drug treatment for PFIC. Our talented team at Albireo have advanced the first Phase 3 studies in three different pediatric liver diseases while discovering two promising new clinical stage bile acid modulators. We believe that Ipsen is well positioned to apply its global R&D and commercial capabilities to make these medicines available to more cholestatic liver disease patients and accelerate the mission of providing hope for families.

{kind=link}

Figure 4: Interesting pipeline molecules.

Financial Assessment

Just as you would get an annual physical for your well-being, it's important to check the financial health of your stock. For instance, your health is affected by "blood flow" as your stock's viability is dependent on the "cash flow." With that in mind, I'll analyze the 3Q2022 earnings report for the period that concluded on September 30.

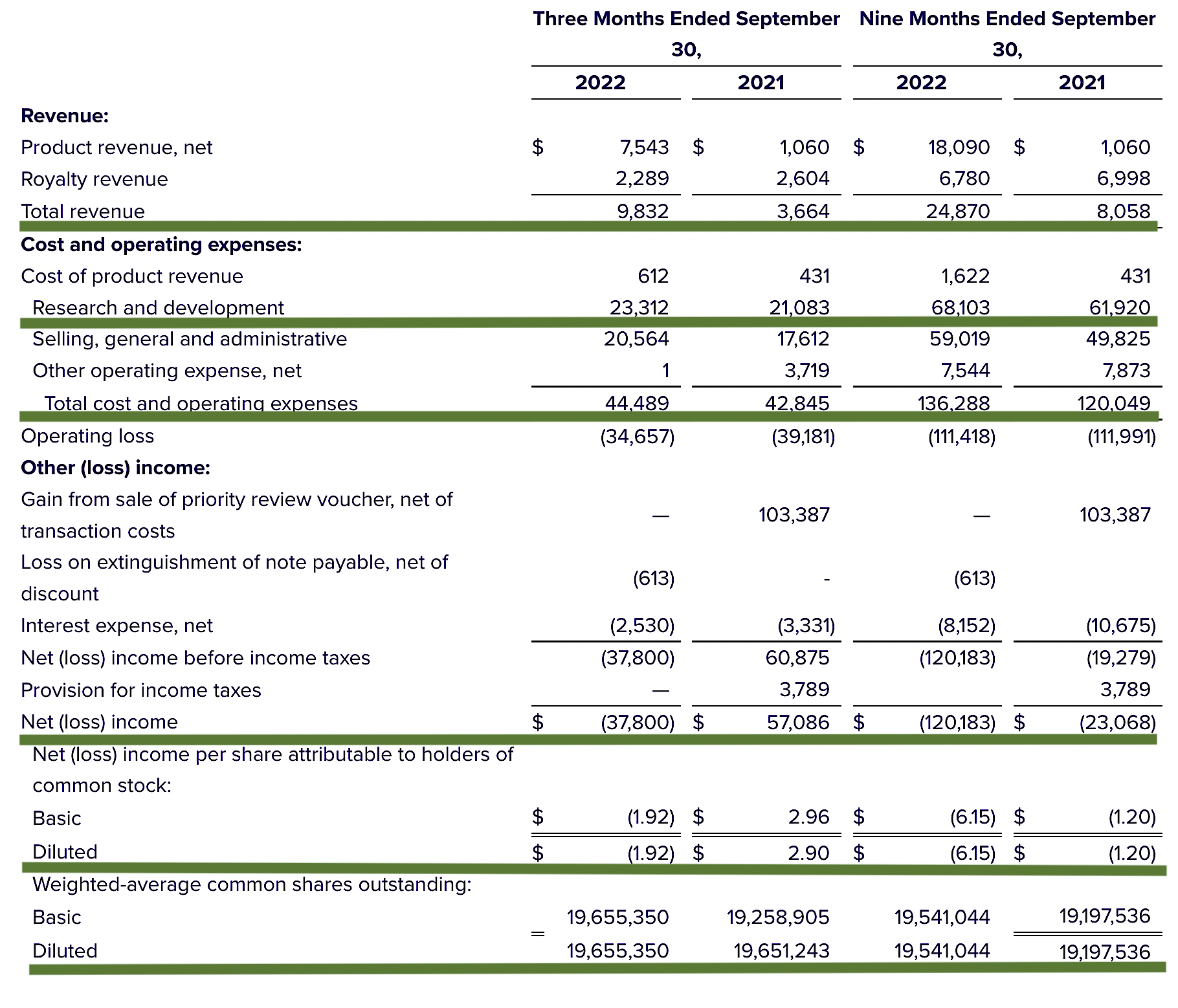

As follows, Albireo procured $9.8M compared to $3.6M for the same period a year prior. On a year-over-year (YOY) basis, the topline grew by 172.2%. Given that Albireo is launching the drug alone and only recently, it'd made sense the sales have not been robust.

That aside, the research and development (R&D) for the respective periods registered at $23.3M and $21.0M. I viewed the 10.9% R&D increase positively because the money invested today can turn into blockbuster profits. After all, you have to plant a tree to enjoy its fruits.

Additionally, there was a $37.8M ($1.92 per share) net loss compared to $57.0M ($2.90 per share) decline for the same comparison. As you can see, the increasing R&D and launch activities contributed to the higher spending and thereby cuts into the bottom line earnings.

{kind=link}

Figure 5: Key financial metrics.

About the balance sheet , there were $272.5M in cash and equivalents. Against the $44.4M quarterly OpEx and on top of the $9.8M quarterly sales, there should be adequate capital to fund operations into the next two years without worrying about the cash runway. Riding the merger/acquisition, Albireo can leverage Ipsen's deep pocket without worrying about cash flows constraint.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strengths. More importantly, the risks are "growth-cycle dependent." At this point in its life cycle, the main concern for Albireo is whether the deal would get consummated. Notably, this risk is extremely small because the deal is already approved and moving forward. The other small concern is that Bylvay might not generate the positive BOLD data needed for approval.

Final Remarks

In all, I have raised my recommendation on Albireo Pharma, Inc. from a speculative buy to a strong buy and raised the stars rating from 4.8/5 to 5/5. Riding the therapeutic prowess of Bylvay, Albireo has come a long way as an orphan disease innovator. Already approved for PFIC, Bylvay is set to gain approval later this year for ALGS. Going into next year, you can anticipate robust ASSERT data for BA. While shareholders are already handsomely rewarded, the biggest reward is the delivery of hope for patients afflicted by these rare conditions.

For further details see:

Albireo Pharma: Elucidating The Ipsen Buyout (Rating Upgrade)