ASTL - Algoma Steel: Deeply Undervalued Steel Producer Undergoing A Radical Transformation

2023-09-25 10:44:47 ET

Summary

- Algoma Steel is transitioning to Electric Arc Furnace steel production, which will reduce maintenance costs, increase steel production, and improve margins.

- The company is undergoing a modernization project for its plate mill, which will double production capacity and generate incremental revenue and EBITDA.

- Algoma Steel has a strong financial position, with enough cash on hand to fund the remaining costs of the EAF project without relying on debt or cash flow.

Editor's note: Seeking Alpha is proud to welcome River Capital Investor as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Algoma Steel Thesis

Algoma Steel (ASTL) (ASTL:CA) is a Canadian steel producer that, I believe, is significantly undervalued by the market. Though there are currently cyclical concerns in the steel industry as a result of recession fears, Algoma Steel's cost model makes it so that they can generate significant cash flow even when steel prices are low. In the next year, through the modernization of their plate mill, Algoma will be able to produce double their current steel plate production, increasing income significantly. Looking even farther out, the company is currently undergoing a switch from Basic Oxygen Furnace method of production to Electric Arc Furnace, which will save significantly on maintenance expenditure and increase production and efficiency. These two projects make Algoma Steel radically different from the typical independent steel producer and gives them a clear competitive edge, a fact the market is missing.

Company Overview

Algoma Steel is a steel producer located in Sault Ste. Marie on the Great Lakes. Its current production capacity is 2.8M tonnes per year. It has many normal elements of production for a BOF producer with an internal coke oven, slab caster, strip mill, but its most notable machinery are its Direct Strip Production Complex ((DSPC)), Cold Mill, and Plate Mill, which give it a large differentiator in terms of product cost and quality. As of current, 65% of sales are to U.S. customers with the rest being Canadian customers, with the top 10 largest customers making up 50% of sales, and another 150 making up the latter half, all across a diverse set of industries. The company, over the last 30 years, has been through multiple bankruptcies and restructurings due to steel price collapses and bad governance, but now, it is my opinion that proper governance practices have been restored.

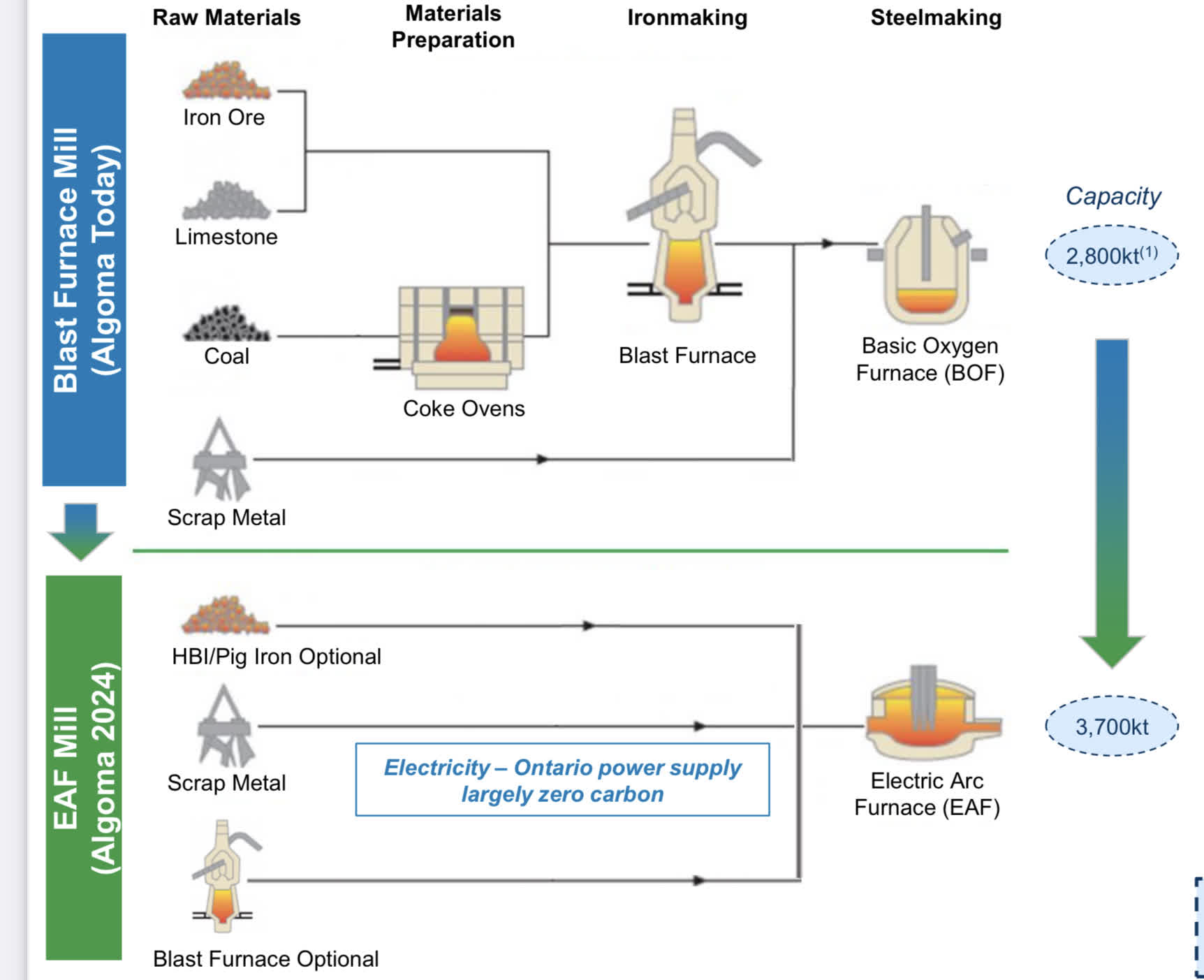

First Aspect - EAF Transition

The major driver of long-term value for Algoma Steel is its transition to an Electric Arc Furnace from the Blast Oxygen Furnace method of production. By mid-to-late 2025, the EAF will be operational at 70% capacity, with it being fully done by 2030, though benefits will be realized earlier.

Algoma Steel Transformation Process (Algoma Steel Investor Relations Website)

{kind=link}

It is my belief that maintenance will be slashed from $110M CAD to $60M CAD a year, when comparing to EAF peers, crude steel capacity will increase by 900kt, and increasing employee efficiency as no employees are planned to be added, but revenue will increase significantly.

This should all result in an outstanding 30%-35% ROIC for the project, with a total cost of $850M CAD, of which 40% has already been spent, and 25% of the remaining cost will be covered by a grant, lowering project budget risks significantly.

Second Aspect - Plate Mill Modernization - PMM

Though this is a smaller project, the company is currently undergoing a modernization project for its plate mill for a total cost of $135M CAD , of which $90M CAD has already been spent on phase 1, which improved production quality. This first phase focused largely on quality of steel plates, with it taking longer than expected due to "software intensiveness." I have evaluated the problems and determined the issues weren't of fault of management, and it should not occur in the second phase as management and workers are competent & experienced.

The second phase will improve automation and double production capacity from 350kt to 700kt. Though this only expands downstream capacity, it adds value because steel currently used to make hot rolled sheets ((HRS)) can be used to make steel plates, which carry a significant price and margin premium of $832/MT over HRS, or double their price. Though it is hard to calculate ROIC, at current prices, it adds roughly $270M CAD in incremental revenue simply due to high prices, which should translate to $50-$100M CAD in incremental EBITDA, an even higher range of ROIC than the EAF project.

Project Completion Timeline and Continued Earnings

The plate Mill Modernization project should be fully complete by April 2024, and then a 6-month ramp-up period subsequently occurs. This represents the most near-term direct catalyst, with the EAF project milestones in spending and building representing the derisking of project expenditure and modeling increasing. There is also the more clear catalyst of improved earnings due to higher steel prices.

Relevant Financial Details

In this last quarter, the company produced $191M CAD in adjusted EBITDA and $150M CAD in OCF ex-CNWC, with $106.4M CAD in total capex of which $77.4M CAD was for its growth projects and $29M CAD for maintenance capex . Along with this, the company, as of Q2 2023 , had $300M CAD in cash on hand, $134M CAD in SIF grant funds available, and $115M CAD in governmental loans. When this balance sheet position is combined with the expectation of $150M CAD more in liquidity being released from inventory over the next couple of quarters, the company will have enough cash available to fund the entirety of the remaining costs of the EAF project, without relying on debt or cash flow.

This financial position and lack of reliance on future cash flow for project funding significantly derisks the two projects, in my opinion, as it allows for the company to be evaluated on its current merits and future possible growth.

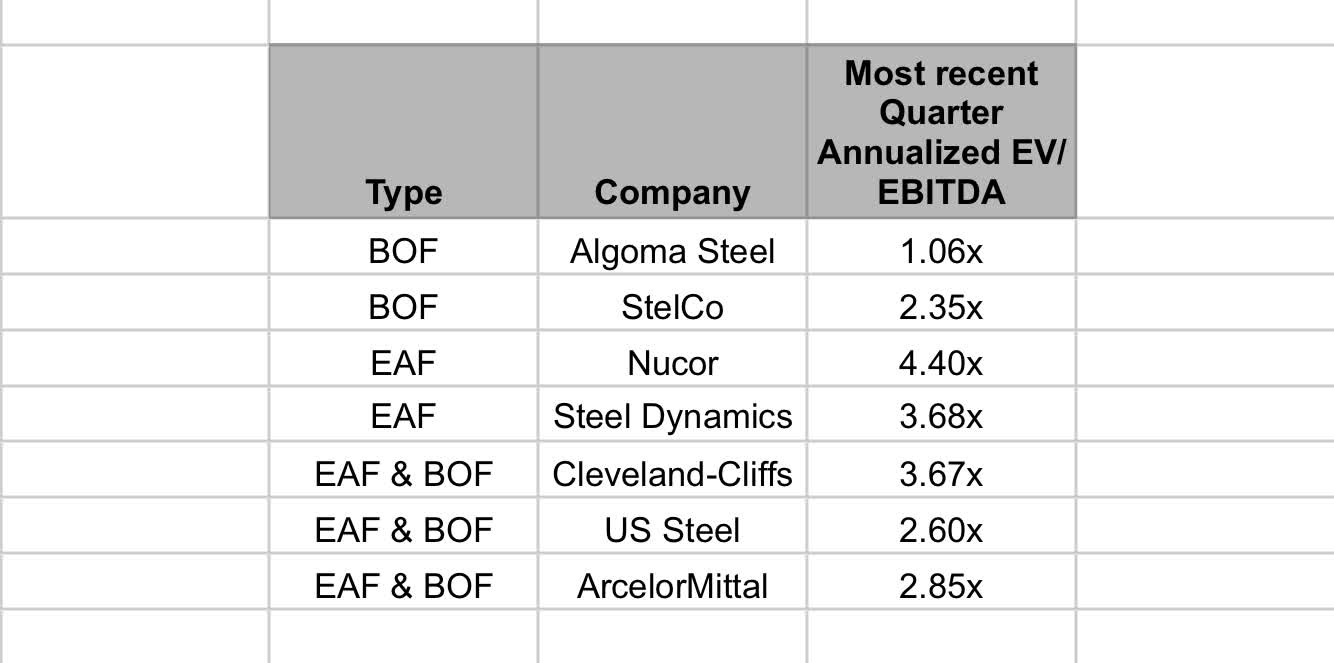

Peer Valuation

Looking at the last quarter to understand how undervalued they are compared to peers, their discount can be clearly visualized:

Peer Comparison (SEC Filings & Tikr Terminal Website)

{kind=link}

Of course, this is only looking at one quarter, given none of these players had any large event skewing performance, it gives a solid visualization of just how undervalued Algoma Steel is relative to peers.

Because we can't just look at one quarter to base our investment thesis off of, let's get a look over the next few quarters.

Looking at the next few quarters, I expect the total cost per ton to stay the same at $990 CAD/MT as a result of fixed price contracts, though due to the fact that coal prices have dropped since the last time contracts were negotiated, it is likely that by the end of 2023, cost will come down around $40-$60 CAD/MT based on the 1.3M tonnes of coal bought annually for current production levels of 2.3M tonnes of steel.

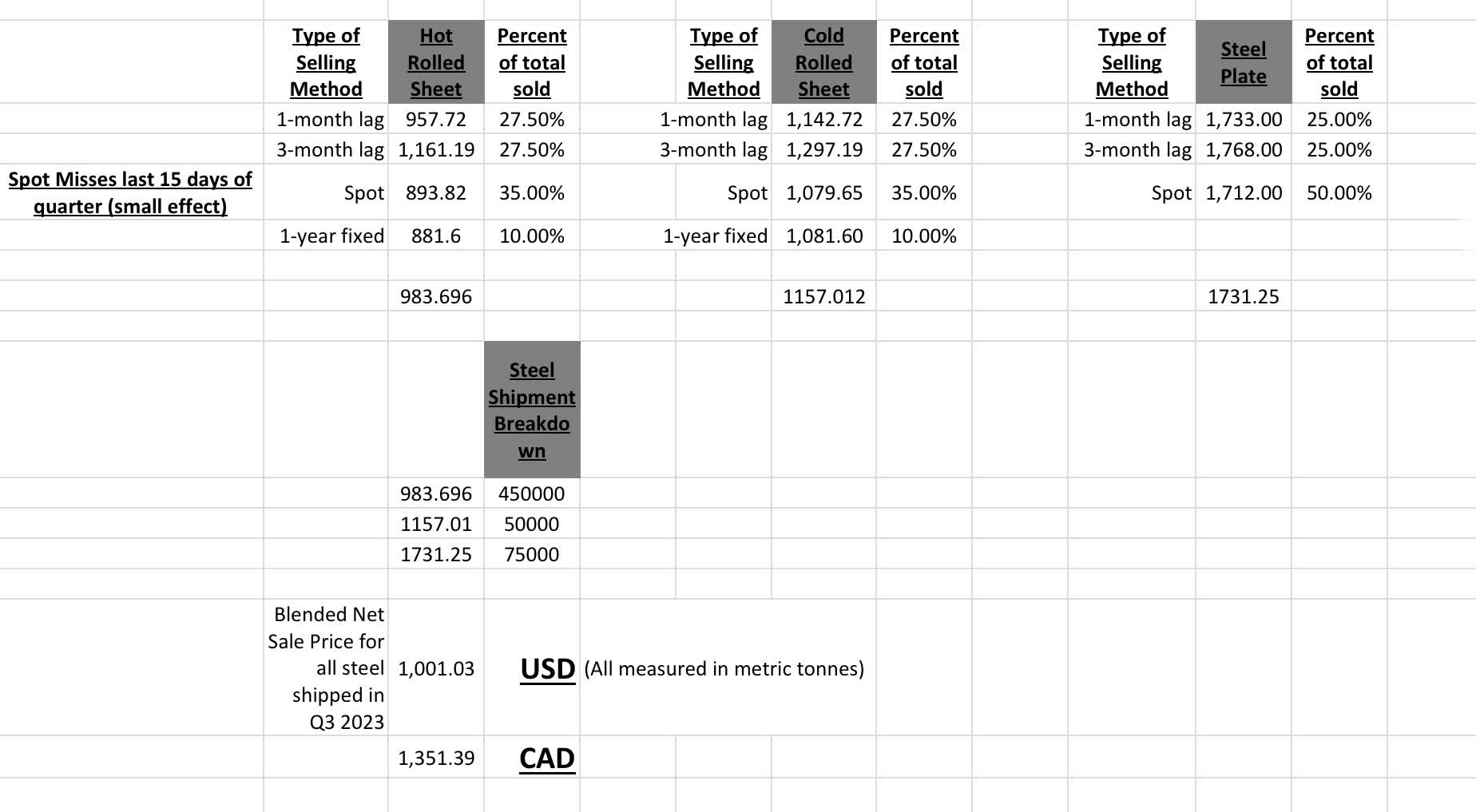

Now we can calculate the sales price for the third quarter of 2023. Here is the pricing model I used for sales price expected in Q3 2023 as of September 15th, which incorporates the contract pricing they have based on steel indices:

Steel Price Calculation for Q3 2023 (InvestorObserver.com for prices and SteelBenchmark )

{kind=link}

Using these shown prices and a $990 CAD/MT cost expected, EBITDA should be roughly $200M CAD in Q3 2023, which makes sense considering the $187M in EBITDA and a $1323 CAD/MT Net Sales Price ((NSP)) and same cost structure in Q2 2023.

Also, to add some insight into Q4 2023, if I just plug in the current prices into the model shown, the result is a nice $1230 CAD/MT NSP and $140M CAD in EBITDA.

Though I don't believe that Algoma Steel should be trading at the same valuation as EAF peers like Nucor and Steel Dynamics yet, they most definitely should be trading at a similar valuation to Stelco, a Canadian steel producer with similar quality production, efficiency, and positioning. Using the given multiple of Stelco's 2.3x for Algoma Steel's valuation, we calculate a 120% upside or a per-share price of $15.34 USD compared to the current price of $6.92 USD.

To note

The company has 24.17M warrants outstanding due in November of 2026 with an exercise price of $11.50. Their current price is very cheap at $1.12, though if you are playing it safer by only buying the shares, to avoid future dilution, it would be wise to purchase warrants at a 1:4 ratio to common stock will offset this dilution for only 4% more cost to offset 25% in possible dilution.

This is a worst-case scenario valuation where all cash on hand and non-debt liquidity is used to fund its two growth projects which fail to materialize any net benefit. Assuming the highly probable scenario that the EAF transition and PMM come to fruition, the upside will be significantly greater due to the benefits previously mentioned. The valuation for this scenario is not included as it is dependent on a variety of variables that needlessly complicate the currently clear opportunity.

Possible Risks

There is the clear risk that Algoma Steel is a cyclical company and is entirely reliant on the price of steel it can fetch and the cost of its inputs (coal, coke, iron, industrial gasses, etc.), though this is partially mitigated through its eventual transition to EAF reducing price sensitivity on the cost side due to the correlation between the prices of steel sold and scrap steel used for production

The EAF transformation project incurs additional costs or delays above current expectations, though this is partially mitigated by 70% of project expenditure being fixed price as of July 31, 2023 .

Conclusion

In conclusion, I view Algoma Steel as a greatly undervalued opportunity in the Steel industry not only because of its predicted $340M CAD in EBITDA or 35% of the market cap over the next two quarters, but also because of its plate modernization and Electric Arc Furnace projects create a situation with both compelling short-term and long-term value creation.

For further details see:

Algoma Steel: Deeply Undervalued Steel Producer Undergoing A Radical Transformation