AQNU - Algonquin: No Statistical Discount At 0.8x Book Value With Soft Q3 Low Economic Value

2023-11-15 00:55:51 ET

Summary

- Algonquin Power & Utilities posted soft Q3 earnings, leading to a continued downtrend in its stock price.

- The company plans to liquidate assets in its renewable energy segment and focus on becoming a pure-play regulated utility.

- The lack of economic value, high leverage, and low capital turnover make recommending AQNU as a long-term investment difficult.

Investment outlook

Algonquin Power & Utilities ( AQNU ) posted Q3 earnings last week, missing consensus estimates at the top and bottom lines, with revenues down 6% YoY on earnings of $0.11/share.

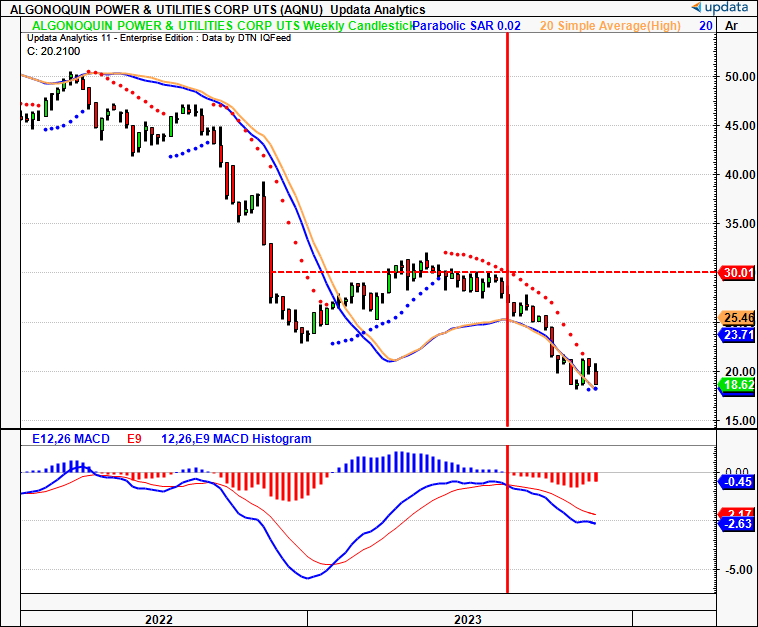

The Q3 post-earnings drift in stock price continues a longer-term downtrend that's been in situ since Q3 last year. AQNU's market value was hammered in FY'22 after it booked a larger than forecast Q3 loss thanks to (i) surging rates weakening the balance sheet, and (ii) tax incentives on its renewables projects, the timing of these. After this came a haircut to investor dividends and a failed attempt to buy Kentucky Power ( AEP ). Investors immediately saw a period of tighter business for the company in '23-'24 and discounted its market value to multi-year lows (Figure 1).

The multi-utility company has employed ~$18Bn of assets on the balance sheet, distributed mostly into core assets, a chunk of this comprised in net interests in >4GW of installed renewable energy capacity.

Critically, it operates through 2 segments:

- Regulated Services Group

- Renewable Energy Group.

Looking forward, the company is committed to liquidating assets in its renewable energy segment. As the CEO notes on the Q3 call , "I am even more convinced that moving to a pure-play regulated utility is the right answer for both businesses" . The market's response to the planned asset sales this year has been fairly muted, implying the consensus is for only a marginal change to AQNU's outlook.

Forensics on the company's economic characteristics is unsupportive of a buy over a mid to long-term horizon. Moreover, the company sells at 11.5x forward EBITDA, a discount to book value and a 16% cash flow yield. There may be scope for a relative value buy for the next 12 months at these prices. Still, considering a more realistic holding period, I rate AQNU a hold.

Figure 1. Figure 1. Continued selloff to multi-year lows. Tested + rejected marabuzo line of November '22. Bearish cross of MACD sustained into the current day. Bearish cross beneath 20-week highs and lows? Have we bottomed?

{kind=link}

Q3 earnings insights

AQNU's Q3 numbers were mixed, with profits down but operating cash flows stretching ~30% higher from last year. The critical takeouts were as follows:

- Weaker than expected financials

Sales were down 6% YoY as expected to ~$625mm, on adj. EBITDA of $281mm and earnings of $0.11/share, flat YoY. It also booked $132.6mm in operating cash flow, growing 30% YoY.

The critical takeout is the impact of " unfavourable weather" that trimmed operations in the renewables business. Due to such unfavourable weather, management has narrowed in its FY'23 guidance, now expecting to come in below the $0.55 per share in earnings guided earlier this year.

Moreover, the impact of the weather was palpable throughout the P&L:

(1). Whilst regulated services grew pre-tax earnings by 7.5% to $264.4mm, the renewables had a difficult period of business, with operating income down 7.3% YoY to $66.2mm.

(2). Management said it estimates " the weather impacted our year-over-year performance by $5.1 million ".

(3). Notably, maintenance expenditures, approximated at the booked depreciation charge, was $104.8mm. If maintenance CapEx is in fact in the c.$100-$105mm ($400-$420mm annualized) range, then net earnings [defined in my analysis as net operating income post-tax, after interest] of $111.2mm (~$445mm annualized) isn't sufficient to maintain a pace of reinvestment growth. This is discussed in further detail later.

- Renewables asset sales ready to take bids

Management also noted on the call it has " kicked off the formal sale process " for the renewables business. It has not received any commitments, but apparently, there's been early interest. The interim CEO set the oath as well, noting no asset will be sold " at a buyer sale price ". Investors will hold the company to these words when bidders do arrive.

As a reminder, renewable energy operating profits were down 7.33% YoY to $66.2mm, driven by an exogenous event - the weather. The firm has substantial capital tied up in the segment as well. It has 400MW of solar underway in its pipeline and started commercial operations for its Sandy Ridge II wind facility last quarter, another 88MW of capacity. Then at Shady Oaks II, it has added 108MW. That is nearly 600MW of capital at risk - none of which is well funded by company cash flows - but could potentially be redistributed to the regulated services business, if management were to unlock value through a sale.

The renewables segment is also AQNU's least profitable division, producing an annualized pre-tax return on capital deployed of 1.6% in the 9 months to September 3 (Figure 2). This is after consuming $109.5mm in capital expenditures to maintain its competitive position. The profile of the company's economic earnings (discussed later) may improve with a sale based on this analysis.

Figure 2.

BIG Insights

So, whilst freeing up capital from the balance sheet and monetizing the renewable assets may be an inflection point, there are many adjacent points to be considered in the investment facts pattern before calling this a situational buy.

Cash flow durability and economic value

Extending from the above, the lack of economic value on offer here is a major headwind that has me suspicious of AQNU's prospects as a statistical discount at 0.8x book value.

For starters, careful observation of the CFO's language on the call regarding capital allocation moving forward is telling-" we got to show restraint and capital discipline" .

Moreover, the company is highly leveraged-6.95x annualized adj. EBITDA by the end of Q3. Cash interest totalled $114mm with $94mm directly to long-term debt, up $19mm YoY. It also has $184mm booked of preferred equity, ahead of the commons and reducing our equity value by that amount.

But it's the profitability factors that create the biggest hurdles to rating AQNU an investment-grade company. This is exemplified in two ways, (i) gross capital productivity, and (ii) the rate of earnings on capital deployed.

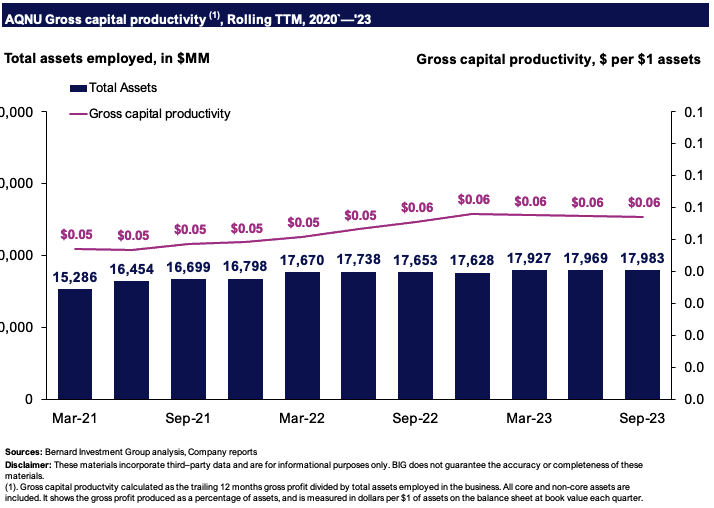

(i). Gross capital productivity

- Here we examine the value of $1 investment to asset growth in terms of gross profit produced. All core and non-core assets are included to judge the choice of asset utilization.

- AQNU produces $0.06 in gross for every $1 of assets employed on the balance sheet, having grown by $0.01 since 2020.

- For reference, a figure of $0.30 is considered high. Anything above $0.50 is superb. A figure of $0.06 on the dollar implies the bulk of costs are derived from generating revenues, so we'd hope to see high capital turnover as a result. AQNU's numbers don't indicate this is a firm that can throw off piles of cash to its shareholders.

Figure 3.

{kind=link}

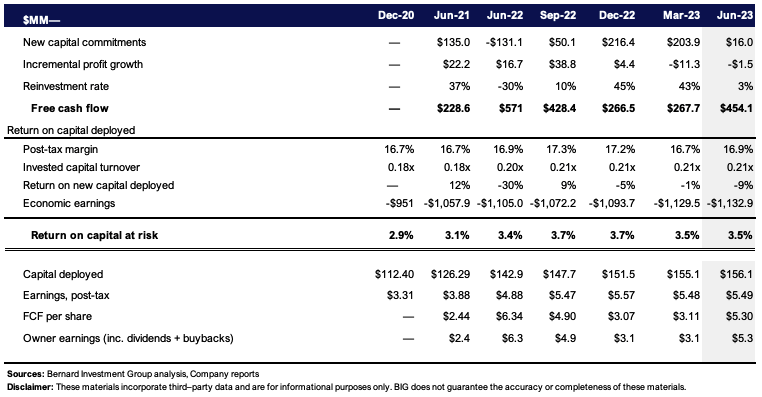

(ii). Rate of earnings produced on capital investments

- The company had $156 per share of capital required to run the business at the end of Q3. It produced ~$5.50/share in net operating profit after tax on this, a 3.5% return on investment, in line with historical range.

- Critically, capital turnover is tremendously low-0.2x sales, similar to the function of the asset intensity outlined earlier. Post-tax margins of ~17% don't mitigate the pace of capital turns. This squares off with the economics of the business. The company is a low capital turnover, modest margins outfit that relies on consumer advantages vs. production advantages. This to me, would signal why it is exiting the renewables space, to (i) reduce the ratio of sales to capital required to run, and (ii) focus on its consumer advantage at the margin.

- The incremental investments are essential too. Profits earned on new capital aren't pulling their economic weight (from 2020-date). For example, AQNU has invested up to 45% of post-tax earnings at negative rates of return this year. This will likely pare back moving forward, reducing the scope for value-adding performance of the stock price.

- As a result of this setup, ability to finance its growth operations through internal cash flows is compromised. This is a capital-hungry business that requires substantial maintenance CapEx + asset replacement costs, reducing cash flows available for shareholders, as these must be consumed by the firm to maintain its competitive position.

Two final observations are relevant here.

One, over the long-run, stock returns closely mirror business returns. Compounding wealth at <5% per rolling TTM period doesn't outpace the 4-5% investors can get on cash and/or investment grade corporates right now.

Two, the economics of opportunity cost means the firm is destroying shareholder value. Long-term market average returns are c.12%. Benchmarking the company's ROIC against this threshold, it has produced a loss of $12Bn in economic earnings since 2020. Not surprising to see it has been valued down from $10.5Bn in market value in '21 to $3.78Bn as I write.

Figure 4.

{kind=link}

This brings me to the primary issue I find with investments in multi-utilities companies in the first place. There is no differentiation in product or price. Each is selling the same utility. Price is more or less dictated by the market. So rates on cost are fixed in many instances. It therefore boils down to production advantages, i.e., who is the low-cost producer, and who has the highest capital efficiency.

You can see ANQU enjoys neither of these benefits. The pivot into renewables? Likely an attempt to differentiate on product + cost in my view. I've seen it more commonly these past few years. However, the core unit economics tell a story of a capital-hungry business with low profitability and ongoing investment needs.

Valuation and conclusion

As a result, the market's appraisal of the company's operating assets and earnings power is soft at best. My investment cortex initially piqued when I saw AQNU selling at 0.8x book value. A statistical discount? When peeling back the layers a little further, my judgement on this is simple- fair priced, no discount.

Consider this facts pattern:

- ANQU sells at an EV of $14.1Bn as I write. EV is the market value of equity plus the market value of debt (of which it has $8.4Bn booked on balance). Invested capital is the book value of debt + equity required to operate. AQNU trades at 1.06x EV/Invested capital (Figure 5). The market has a 6% premium on the valuation of its investments-more or less at par. AQNU hasn't unlocked any additional market value from each $1 it has invested into the business.

- Comparing this to the ratio of its ROIC and our 12% hurdle rate, as a 'no growth' multiple, it appears the market has well and truly captured the earnings power on these at ANQU's current market value.

The company also sells at 5x forward sales and 11.5x forward EBITDA. Net of the depreciation charge required to operate, it sells at 25x pre-tax earnings at a 16% cash flow yield. So you are getting value (the yield) but are paying a premium for it (the 25x multiple).

Figure 5.

BIG Insights

It also sells at 8.2x trailing NOPAT, which gets you to $3.86Bn in market value as I write (8.2x470 = 3,860). However, the profit generated on its new capital in Q3 was negative 9%. Assuming the same 8.2x multiple, the company is now worth $3.53Bn in my eyes (470/1.09x8.2 = $3,535). This supports a hold rating, and no statistical discount to book value.

In short, ANQU presents a number of economic hurdles to overcome to warrant an investment grade rating for equity investors. The investment facts are:

(1). No economic value on capital deployed and required to operate business,

(2). Capital-hungry business with low capital turnover and modest margins,

(3). Needs to find an adequate buyer for its renewable energy assets,

(4). Replacement costs at its current asset base are high and don't rotate back to gross profit growth,

(5). Valuations are not statistically discounted at 0.8x book value.

Collectively, these data points support a neutral rating. Net-net, rate hold.

For further details see:

Algonquin: No Statistical Discount At 0.8x Book Value With Soft Q3, Low Economic Value