ONLN - Alibaba's FQ1: A Terrible Quarter

- Shares of Alibaba rose 2% after the e-Commerce company beat FQ1'23 predictions.

- Alibaba generated 0% revenue growth year-over-year, the worst on record.

- Still, pockets of Alibaba’s business are performing well.

Alibaba Group Holding Limited ( BABA , BABAF ) presented earnings for its first fiscal quarter of the year yesterday which were better than expected EPS, in large part because expectations were low heading into earnings . Alibaba also reported its first quarter ever with flat revenue growth due to a storm of challenges in the second-quarter that included wide-spread COVID-19 lockdowns which compounded existing supply chain problems. While Alibaba's FQ1'23 was terrible, I believe we could be near a bottom here if the Chinese economy opens back up!

Alibaba: Better than expected EPS, but still a terrible quarter

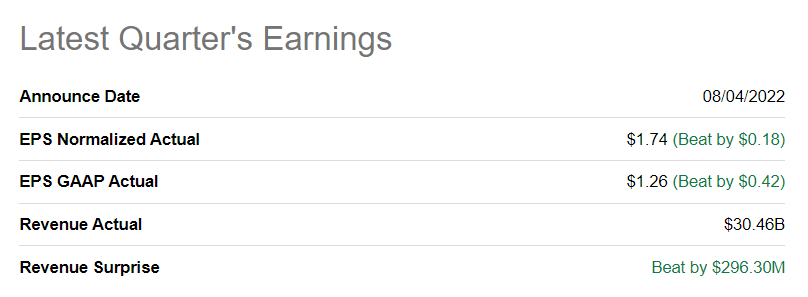

Alibaba suffered in the quarter from COVID-19 lockdowns that equally weighed on manufacturers and on consumers. Despite those challenges, Alibaba beat consensus predictions regarding its top and bottom line for FQ1'23.

{kind=link}

Alibaba generated total FQ1'23 revenues of 205.6B Chinese Yuan ($30.9B), showing no revenue growth at all year over year. The firm's domestic e-Commerce business -- which accounted for 69% of Alibaba's consolidated revenues -- even saw its segment revenues decline 1 percent to 141.9B Chinese Yuan, which calculates to $21.2B, due to logistics problems and a higher amount of order cancellations during COVID-19 lockdowns.

Alibaba's profitability also continued to come under pressure with adjusted EBITA margins in the domestic e-Commerce segment dropping from 35% in the year-earlier period to 31% in FQ1'23. The decline in margins is due to macroeconomic headwinds, the rise of COVID-19 infections weighing on revenues as well as growing competition in the e-Commerce market in China.

Alibaba: FQ1'23 Segment Revenues And Margins

But even within the struggling e-Commerce business there were two bright spots for Alibaba: direct sales and China's e-Commerce wholesale segment. Alibaba's direct sales business includes brands like Sun Art, Tmall Supermarket and Freshippo. Supermarkets operated under these brands are smart phone-centered, high-tech direct sales outlets that are seeing strong customer acceptance and providing an opportunity for growth in a difficult market challenged to generate growth.

Direct sales generated 8% year over year revenue growth while China e-Commerce wholesale saw a 26% year over year uptick in its top line due a higher revenue from its duty-free wholesale segment. Direct sales and China e-Commerce wholesale together are now responsible for about half of Alibaba's domestic e-Commerce revenues and prevented Alibaba from reporting larger negative revenue growth in FQ1'23.

Alibaba: FQ1'23 Direct Sales And China Wholesale Business

Free cash flow and buybacks

Alibaba is profitable regarding free cash flow ("FCF") which is something that investors seem to forget sometimes and which is why I believe Alibaba's shares continue to have revaluation potential.

Alibaba generated 22.2B Chinese Yuan ($3.3B) in free cash flow in FQ1'23 which calculates to a FCF margin of 11%. In FY 2022 -- which was a very challenging year for Alibaba due to persistent government crackdowns on technology and e-Commerce sectors -- Alibaba generated total free cash flow of 98.9B Chinese Yuan ($15.6B), representing a FCF margin of 12%. Despite Alibaba's slowing e-Commerce business, the firm continues an enormous amount of free cash flow.

Alibaba: FQ1'23 Free Cash Flow

Alibaba spends a large part of this free cash flow on buying back its shares. In April, Alibaba up-sized its stock buyback from $15B to $25B. Alibaba spent 23.9B Chinese Yuan ($3.6B) on stock buybacks in FQ1'23, showing an increase of 235% year over year.

The market is too worried about Alibaba

Alibaba is spending a lot of money on diversifying its e-Commerce business model and expanding overseas with brands such as Lazada and Trendyol. The entry into the direct sales market is promising and shows that the firm can generate growth even in difficult markets.

Alibaba did not give revenue guidance for FY 2023, but the expectation is for 8% top line growth this year and 13% next year. The revenue estimate for FY 2023 implies a stronger rebound in the second half of the year which is possible if Chinese authorities lift COVID-19 restrictions, especially in big cities like Shanghai or Beijing.

Revenue estimates may trend down after Alibaba's disappointing FQ1'23, but I see a reopening of the Chinese economy as a potentially big catalyst for Alibaba's shares. Since Alibaba continues to generate a ton of free cash flow each quarter, I believe investors have become too fearful of touching Alibaba's shares.

Risks with Alibaba

The biggest risk, obviously, is that Alibaba's top line growth could dip into negative territory in the short term. Alibaba barely managed to avoid negative revenue growth in FQ1'23 and a resurgence of COVID-19 infections in China's largest cities could weigh on Alibaba's shares longer than expected. What I see as a more specific risk for Alibaba than negative top line growth is a decline in margins that has crystallized lately. I would change my mind about Alibaba if margins continued to decline and Alibaba started to see weaker free cash flow in its business.

Final thoughts

Alibaba's FQ1'23 was a terrible quarter in many ways -- top line growth slowed to 0%, margins weakened -- but there are segments that see robust growth like direct sales or wholesale in China... and they saved Alibaba's FQ1'23 from worse results. Despite challenges, Alibaba remained solidly profitable on a free cash flow basis which investors sometimes appear to forget. A full reopening of the Chinese economy would likely be a big catalyst for Alibaba's shares and allow a return to positive top line growth!

For further details see:

Alibaba's FQ1: A Terrible Quarter