AMR - Alpha Metallurgical Resources: Still Cheap And Returning 15%

2023-09-20 12:12:37 ET

Summary

- Alpha Metallurgical Resources has experienced a significant stock price increase of 48% since our bullish call was issued a few months ago.

- Bullish factors, like AMR's strong financial performance and attractive capital return stack, still hold true.

- However, we're becoming concerned about softening demand for AMR's end product, worsening global macro conditions, and the company's overbought stock.

- Getting more cautious and selling put options on AMR shares is the best way to play this excellent company & generate cash-on-cash returns as a new investor.

A few months ago, we wrote an article titled " Alpha Metallurgical: Debt-Free And Printing Cash ", where we issued a bullish call on Alpha Metallurgical Resources ( AMR ) stock, talking about how the company had undergone a number of changes that could allow for significant total return potential for shareholders.

At the time, the valuation was also cheap as chips, with shares trading at a mere 2.3x FCF multiple.

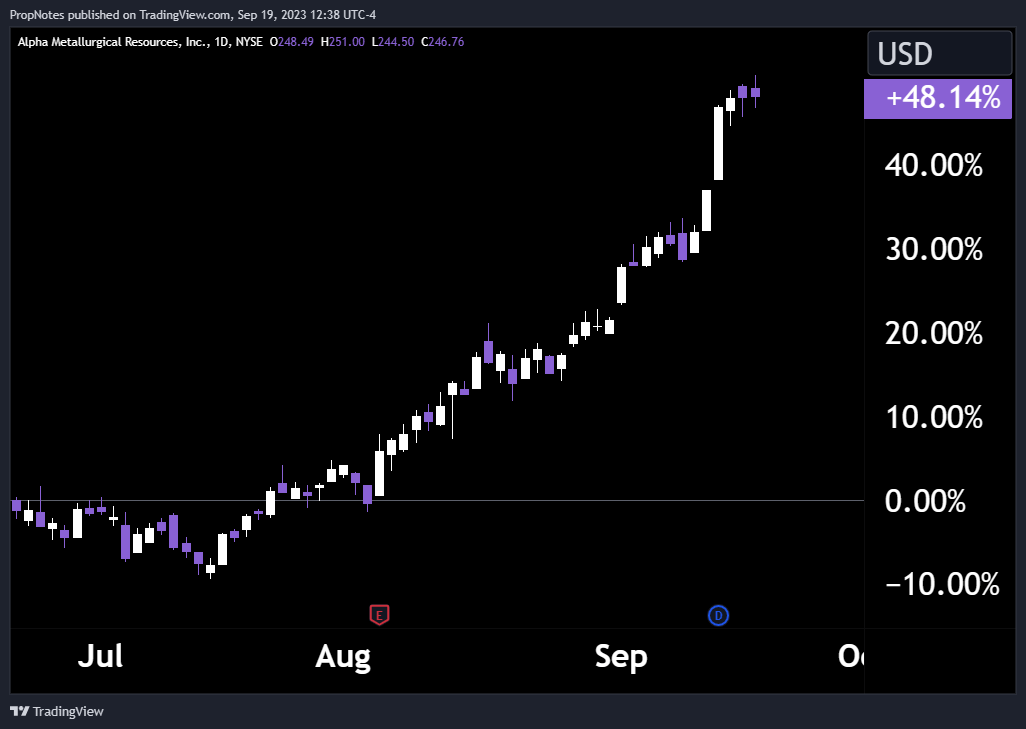

Since then, the stock has gone on a massive 48% run, almost from the very day we published our take:

{kind=link}

TradingView

We liked the potential for returns in the stock, but plainly, we didn't expect things to move so quickly.

Thus, today, we're updating our thesis with all of the new developments since then, looking to answer one question: What happens next?

Getting Up To Speed

On the off chance you're new to this stock, allow us to get you caught up with the main points we made about AMR in our original, aforementioned article :

Strong financial performance : At the time, AMR had shown strong top-line growth, with TTM revenue soaring to $3.94 billion, a 34% increase year-over-year. This growth had been driven by a combination of factors, including increased coal demand, resulting from improved economic activity, coupled with a limited supply response. Additionally, AMR had been able to successfully pass on higher coal prices to customers, which had further boosted its revenue.

Favorable demand outlook : Global steel demand was forecasted to rebound in 2023 and continue to grow in 2024, which should have supported demand for AMR's metallurgical coal. This growth was expected to be driven by a number of factors, including increased construction activity in China and other emerging markets, as well as continued growth in the automotive and manufacturing sectors.

Attractive valuation : AMR was trading at a revenue multiple of 0.69x and a free cash flow multiple of 2.3x, which was well below its historical averages. This valuation was attractive given the company's strong financial performance and favorable demand outlook.

Streamlined business model : AMR had a streamlined business model with a focus on metallurgical coal. The company had essentially zero debt and solid free cash flow margins. This strong financial position gave AMR the flexibility to invest in growth opportunities and return capital to shareholders.

Where Things Stand

Fast forward to today, and many of these things still hold true.

AMR remains debt free, and its main mine assets shouldn't require any ongoing Capex, which means that profits should drop straight to the bottom line for shareholders. This streamlined dynamic is incredibly powerful when it comes to returning capital via share buybacks and dividends.

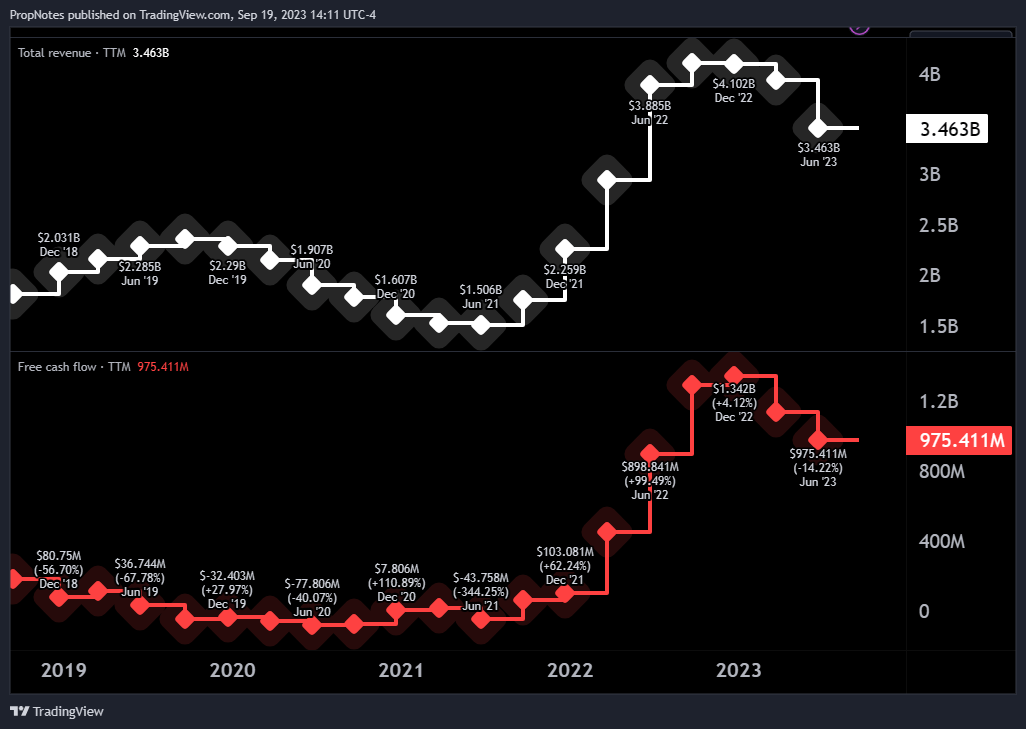

Secondly, profits remain strong. In their most recent earnings report, AMR reported more than $262 million in free cash flow on $868 million in revenue, a tremendous 30% FCF margin:

{kind=link}

TTM Numbers Are Holding Up (TradingView)

That said, there are concerns.

The company reported that demand for their end product was set to continue softening due to a variety of macro conditions:

"Metallurgical coal markets continue to soften as economies across the globe attempt to find stable footing. As the Russian war in Ukraine persists, inflationary impacts remain, and monetary tightening continues in the United States and Europe, economic indicators, like manufacturing production data, indicate that many regions of the world are still contracting instead of expanding. The recovery growth expected following China’s reopening from its zero-COVID policy has instead been muted, and China’s June producer price index continued its multi-month decline, fueling concerns of economic weakness and possible deflation in the world’s second-largest economy and a significant consumer of steel."

In addition to that, China, one of the two largest steel producers in the world (and a massive end market for Met Coal), has had major issues lately in their economy, especially around construction and credit.

Country Garden ( OTCPK:CTRYF ), the country's largest real estate developer, just narrowly avoided defaulting on its debt, and the Yuan has seen its exchange rate fall further as Chinese exports have fallen.

While the World Steel Association has noted that Chinese steel production is still growing, the overall picture for demand has worsened considerably vs. where we were in early summer, and prices continue to slide:

"As compiled by the World Steel Association (“WSA”), June 2023 global crude steel production of 158.8 million metric tons represented a slight 0.1% decrease from June 2022. While the overall market was down, the two largest steel producing countries, China and India, both had increases in their production levels. China produced 91.1 million metric tons, 0.4% more than its year-ago June production amount, and India produced 11.2 million metric tons, an increase of 12.9%.

...

In the second quarter, metallurgical coal indices remained volatile, continuing the downward trajectory of recent quarters. Each of the four indices Alpha closely monitors decreased by 20 percent or more over the course of the second quarter."

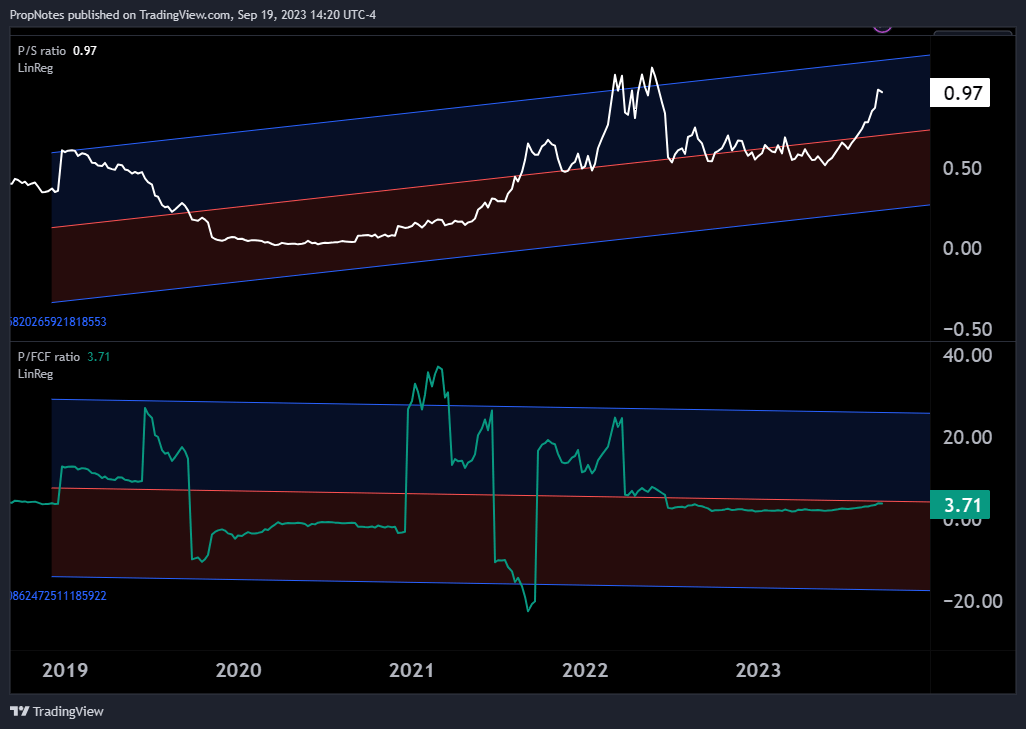

At the same time that the outlook has worsened, the company has also gotten more expensive.

When we wrote about AMR in June, the company was trading at a comfortable 2.3x FCF. Today, that number stands much closer to 4x FCF, and the Price / Sales ratio is nearing 5-year highs, around 1x:

{kind=link}

TradingView

While the valuation still remains depressed by many metrics, the low hanging fruit we identified in our first article seems to have been seized on by the market. As the multiple has rightfully re-inflated, further gains will likely be slower going.

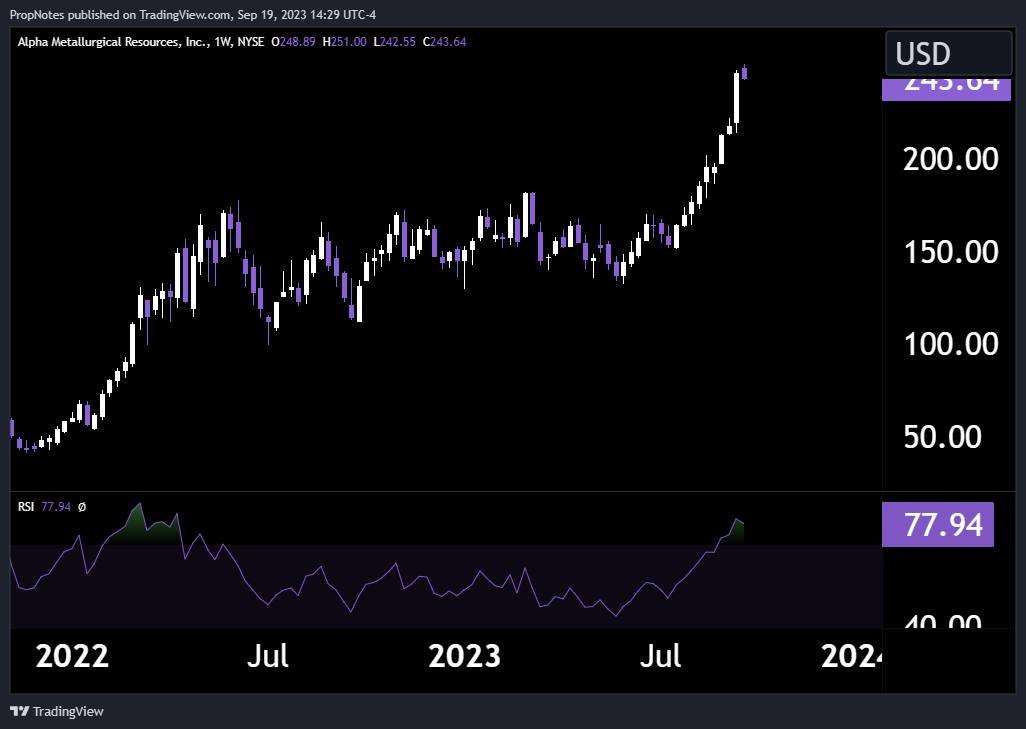

Finally - when we last reviewed the stock, the price was in the middle of a range. Now, shares are overbought, with the weekly Relative Strength Index reading ~77:

{kind=link}

TradingView

This doesn't immediately disqualify a new entry into the stock, but given the worsening demand backdrop and the less forgiving valuation, the best course of action, for those who still want to get into this operationally excellent materials play, might be to wait for a dip.

That, or sell some puts on the stock.

The Trade

We still like AMR's overall setup, but given the combination of an increasing multiple and a worsening demand picture for the end product, it makes sense to begin looking at shares more cautiously.

Selling put options is the perfect way to express this view.

If shares drop between now and expiry, then put sellers may be forced to purchase the stock on a dip.

If shares continue higher or trade sideways, then put sellers are able to lock in a more conservative profit.

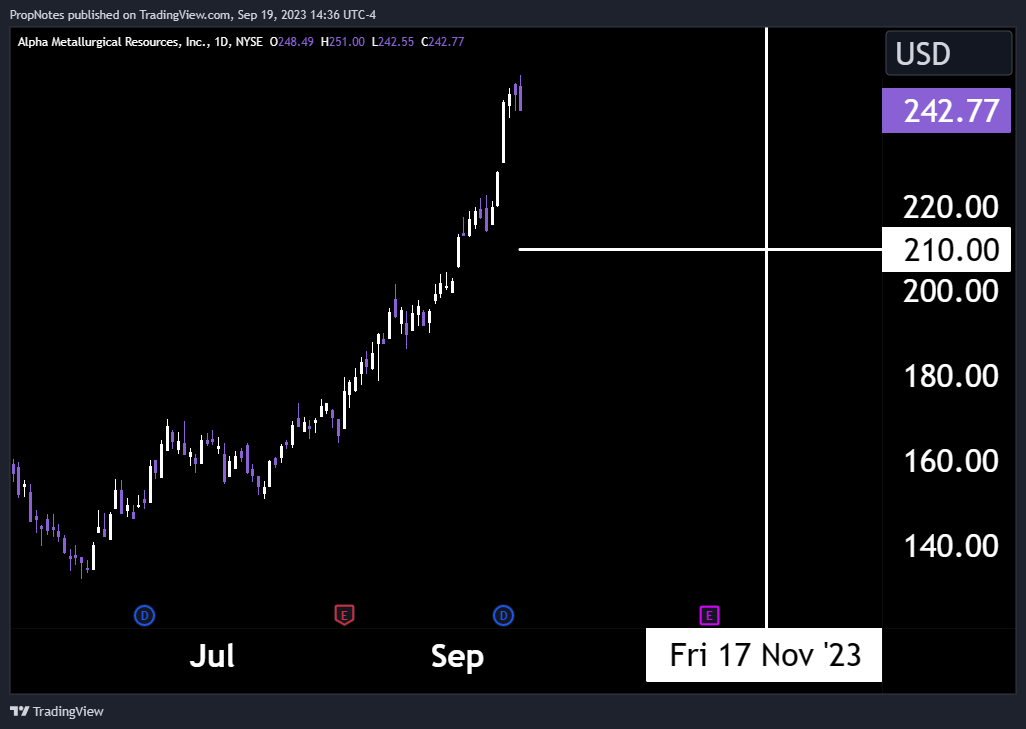

In this case, we like the November 17th, $210 strike call options:

{kind=link}

TradingView

These options are currently trading for $5.00, which represents a potential $500 profit per contract, or a 2.44% return over the next 59 days (this annualizes to a solid 15% cash-on-cash return).

Should the stock drop, then put sellers would get a better price for shares. If the stock trades above $210 by expiry, then the full $500 per contract is theirs to keep.

Given the 81% chance of Max Profit by mid-November, and it seems like a solid win-win trade to us.

Summary

AMR is still an operationally excellent company. The streamlined structure should allow for robust returns in the future, and both nominal profits and percentage margins remain strong.

That said, the valuation has re-inflated somewhat, shares are now overbought, and the cyclical met coal market appears to be softening on global macro concerns. Taken together, it makes sense to be more cautious with this name & take advantage of the setup by selling put options.

We think it's a great win-win way to play this long term winner.

Cheers!

For further details see:

Alpha Metallurgical Resources: Still Cheap And Returning 15%