AYX - Alteryx: Be Patient Until This Company Unlocks Its Value

2023-08-08 16:47:38 ET

Summary

- Alteryx, a data integration company, has seen its share price drop tremendously year to date on lower guidance.

- The company's pivot to a subscription model, large total addressable market, and best-in-class gross margins make it an attractive long-term investment.

- Short-term challenges are largely macro driven, and the company has identified sales processes to improve upon.

- A six-point boost to pro forma operating margins embedded in the company's FY23 guidance helps to offset revenue weakness.

With very few exceptions, the entire tech sector has breathed a sigh of relief this year as massive rebounds took place, especially over the past few months. But now is not the time to get complacent: especially now as uncertainty looms over the future of interest rates, it's time for investors to be very choosy with individual stocks and focus on "growth at a reasonable price" names that won't get whacked if interest rates start rising again.

Focus on Alteryx ( AYX ) in particular. This data integration company, which helps enterprises pull together data from disparate streams in order to enable deep analysis, has seen its share price retreat ~40% year to date, one of the few tech companies to do so. It's difficult to remember now that Alteryx used to be one of the highest-flying tech darlings in the software sector. Today, the stock remains ~80% below its 2020 peaks above $170.

Alteryx just reported Q2 results: and its decelerating cut to full-year guidance caused the stock to drop more than 15% as a result, creating a strong buying opportunity.

Though it has been a painful slog to remain invested in Alteryx throughout this time, I remain bullish on Alteryx. I think the company's pivot to a subscription model opens the door to its ultimate "analytics for all" vision for the modern enterprise, by lowering barriers to entry and price. The company also has an inherently profitable business model driven by high margins that just needs more scale to shine. While the short-term may be challenged for Alteryx as it is a pricey solution that is likely to get deprioritized in a tough macroeconomy, I think the company continues to build a solid foundation that will help it succeed once we're out of the down cycle.

As a refresher, here is my full long-term bull case for Alteryx:

- Automation, data-driven decision-making, and analytics are all powerful secular drivers for Alteryx. Companies want to use data to drive decisions. Unfortunately, data is sometimes locked in different formats and takes hours of manual work to untangle. Alteryx's technology helps with that process and automates one of the most labor-intensive pieces of adopting a "big data" strategy in the C-suite. Investing in technology like Alteryx may not have been a top priority during the pandemic, but it will become a much hotter-button topic as we look ahead.

- Large $113 billion 2025 TAM. Alteryx's current ~$1 billion annual revenue run rate is only a fraction of its estimated current $65 billion TAM, leaving plenty of room for growth. Alteryx additionally expects its TAM to expand to $113 billion by 2025.

- Truly horizontal software serving a wide variety of use cases across many industries - Alteryx's software is broadly applicable to clients in virtually any industry. An illustrative cross-section of Alteryx's customer base: Netflix ( NFLX ), Walgreens ( WBA ), Abbott Laboratories ( ABT ), Chevron ( CVX ), Wells Fargo ( WFC ), Visa ( V ), Marriott Hotels ( MAR ), and Facebook ( META ) are all among Alteryx's anchor clients, spanning every industry.

- Best-in-class gross margins of ~90% are among the highest in the software industry - Virtually every dollar of revenue for Alteryx flows through to the bottom line, justifying the efforts that Alteryx makes on the initial sale.

- Plans for significant profitability - Already, Alteryx has hit significant pro forma operating profits. Over the long run, it plans to generate pro forma operating margins in the 25-30% range, primarily by achieving economies of scale on sales and marketing. When a company like Alteryx has huge recurring revenue, over time the cost of sales support for that revenue base will eventually dwindle.

Valuation is also another key draw to investing in Alteryx, and one that I think offsets the fundamental risks the company is flagging. At current share prices near $31, Alteryx trades at a market cap of $2.20 billion. After we net off the $748 million of cash and $1.23 billion of debt on Alteryx's most recent balance sheet, the company's resulting enterprise value is $2.68 billion .

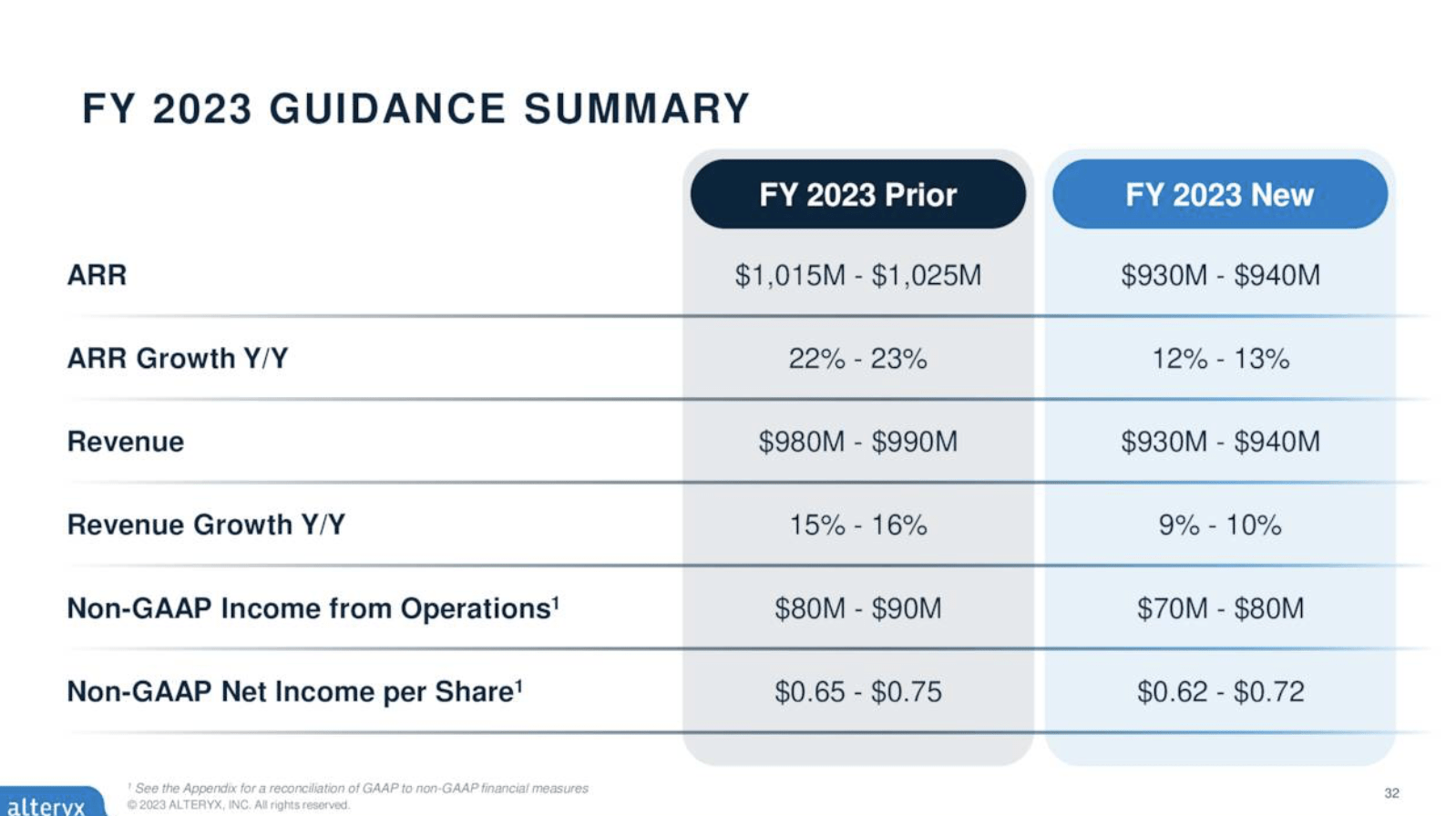

Meanwhile, for the current fiscal year, Alteryx has cut its guidance to $930-$940 million (+9-10% y/y), which represents six points of weaker growth relative to its prior outlook calling for 15-16% growth. Its Q3 guidance, meanwhile, is calling for revenue to dip negative to a -2% to -4% y/y decay.

{kind=link}

Note that despite the company's top-line guidance cut, it has identified headcount reduction opportunities that have resulted in a substantial boost in pro forma operating income expectations to $80-$90 million (nearly double the prior guidance at the midpoint), representing an 8% pro forma operating margin.

Taking the midpoint of Alteryx's annual guidance at face value, the stock trades at just 2.9x EV/FY23 revenue - which, for a software company currently growing ARR at a >20% y/y pace and which has nearly 90% pro forma gross margins, is quite a bargain.

Stay long here until the market wakes up to Alteryx's true value.

Q1 Download

Let's now go through Alteryx's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Needless to say, it wasn't the most pleasant quarter for Alteryx investors to endure. Revenue grew just 4% y/y to $188.0 million, though this was better than the company's guidance as well as consensus, which had expected $182.0 million in revenue (or flat y/y growth). Revenue, however, decelerated sharply from 26% y/y growth in Q1.

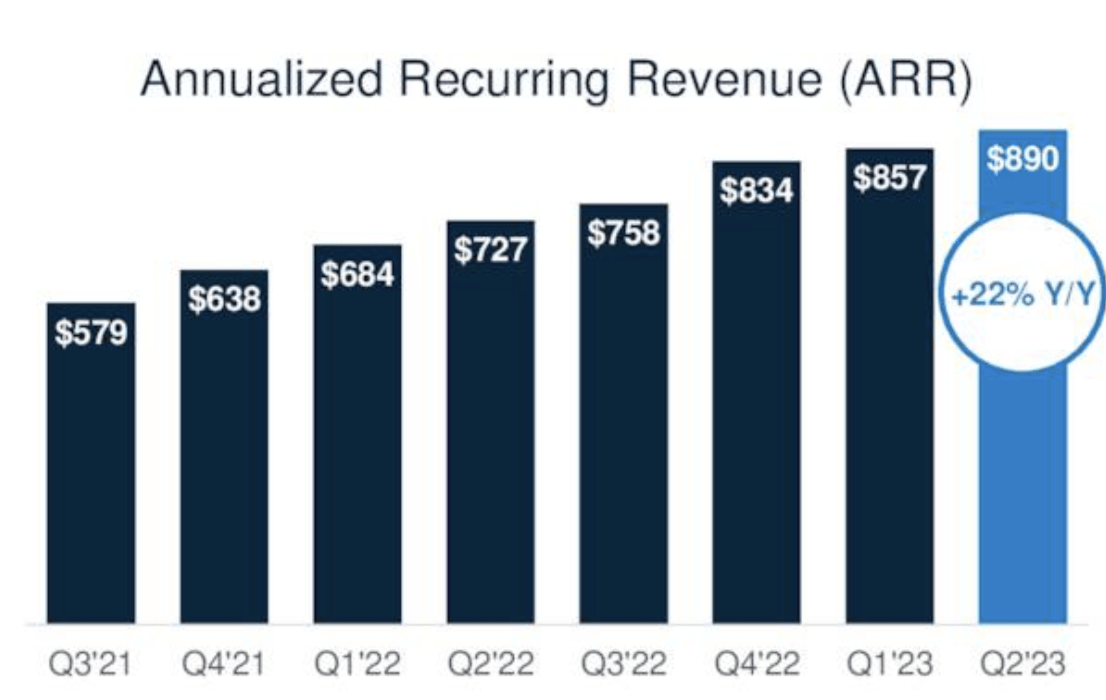

ARR, meanwhile, held up better. The company added $43 million of net-new ARR in the quarter to land at $890 million, up 22% y/y. We'll note that this is a stronger sequential add versus Q1, and the same sequential add in nominal dollars as Q2 of 2022.

{kind=link}

Management has called out several challenging execution realities that are causing deals to delay or diminish in size. Per CEO Mark Anderson's remarks on the Q2 earnings call :

While we had incorporated a tougher macro into our Q2 guidance, we encountered a pronounced change in customer buying behavior in the last two weeks of the quarter. This was especially apparent with larger customer expansion projects outside of the normal renewal cycle. As a result, many large customer upsell opportunities to which we thought we had a clear line of sight ultimately pushed out of the quarter or closed with a reduced size.

We recognize that we need to improve our execution on deals like these, particularly in North America. These are significant opportunities, and they require a higher level of engagement and diligence in the current macro backdrop. We're implementing a significantly higher regimen of dual scrutiny and discipline going forward, plus enhancing sales enablement, which should, in turn, improve our pipeline quality and conversion rates. We're also focused on identifying higher probability win opportunities with a strategy more attuned to the current macro. This is absolutely key to driving improvements in our sales productivity."

Still, in spite of this, we like the fact that Alteryx notched a 120% net revenue retention rate in Q2, which indicates that the typical customer is still consuming and spending 20% more than the prior year. Note as well that if Alteryx is citing deals to delay out of the quarter, there's a chance that slippage will help Q3 revenue accelerate relative to Q2, not decelerate as the company's conservative guidance is calling for.

Reacting to the slower execution trends, Alteryx notes that it is boosting its sales enablement opportunities to help its reps close more deals, as well as increasing its internal deal scrutiny, especially on its enterprise sales opportunities.

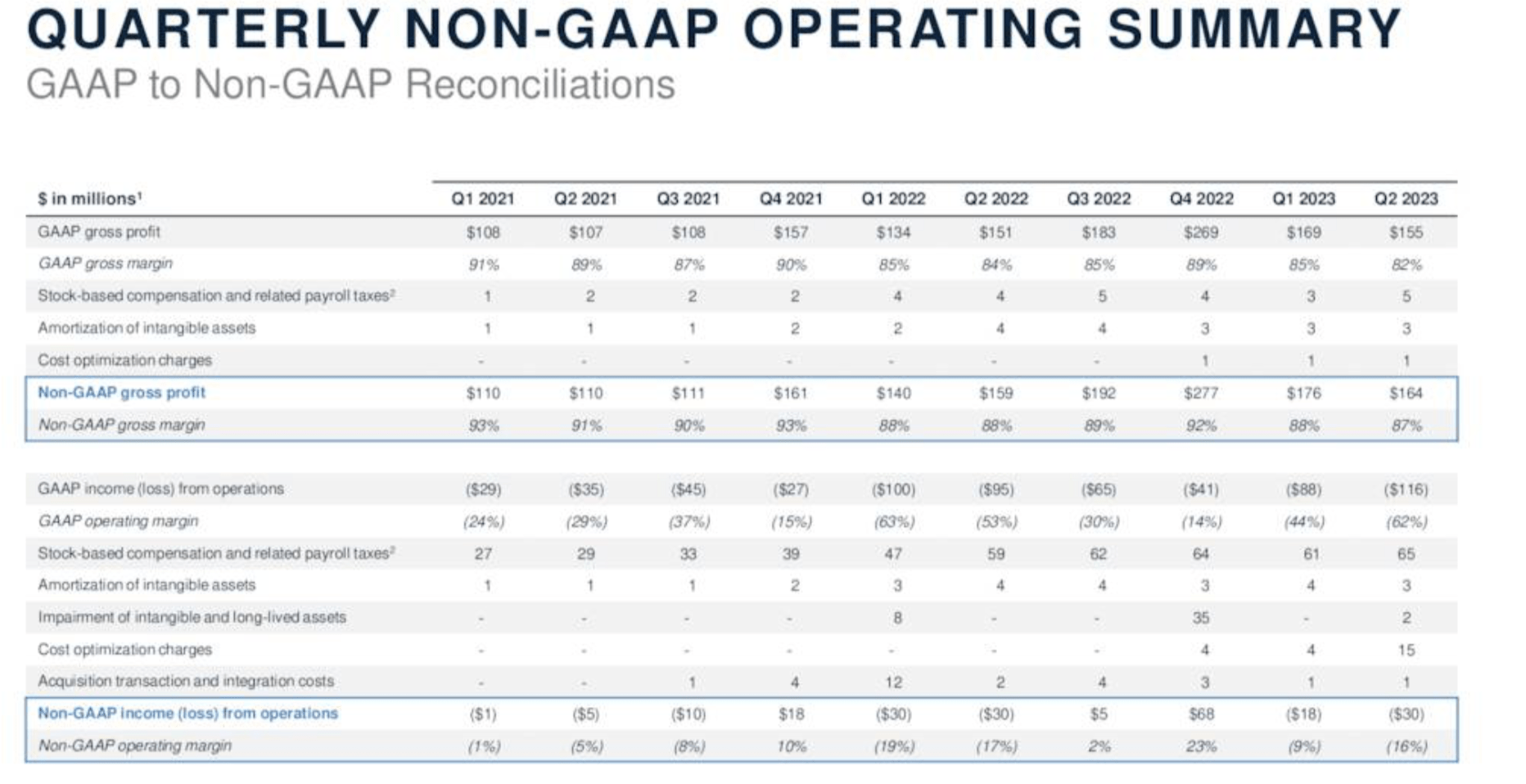

The company is also doubling down on its commitment to profitability. From a margin perspective, Alteryx's pro forma operating margins stood at -16% in the quarter, one point higher than the prior-year Q2 at -17%.

{kind=link}

The company typically sees seasonality take over and provide lifts to profitability in the back half of the year, and as a reminder, it's still guiding to an 8% pro forma operating margin at its midpoint this year - which would be six points of improvement versus 2% in FY22.

Key Takeaways

There's no doubt that Alteryx is facing a challenging cycle as IT departments pull back on expensive capital investments. At the same time, however, we like that the company is setting the stage for better future profitability and working on its sales processes to take advantage of its large market opportunity when macro clouds clear up.

For further details see:

Alteryx: Be Patient Until This Company Unlocks Its Value