AYX - Alteryx: No Sign Of A Turnaround (Rating Downgrade)

2023-08-30 21:06:33 ET

Summary

- Alteryx shows weakness in Q2 FY12/2023 and lowered FY company guidance, indicating a lack of business turnaround.

- The company is struggling to attract new customers and convert new accounts due to increased competition and evolving market demands.

- Credit risk remains high, with doubts about the company's ability to pay back its debt and limited options for raising cash.

Investment thesis

Alteryx ( AYX ) shows no definitive signs of a business turnaround, with KPIs showing weakness in Q2 FY12/2023 and lowered FY company guidance. With credit risk remaining high, we believe the company will continue to struggle. We rate the shares as a sell.

Quick primer

Alteryx is a provider of data preparation software called Designer, sold as packaged software on desktop PCs for individual licenses and servers for multi-users, with a cloud version released in 2022. The product is targeted primarily at 'citizen' data scientists, as opposed to highly skilled analytics experts. Current CEO Mark Anderson was appointed in October 2020, replacing co-founder Dean Stoecker who was made chairman. Peers include Power BI from Microsoft ( MSFT ), Tableau ( CRM ), and Domo ( DOMO ).

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

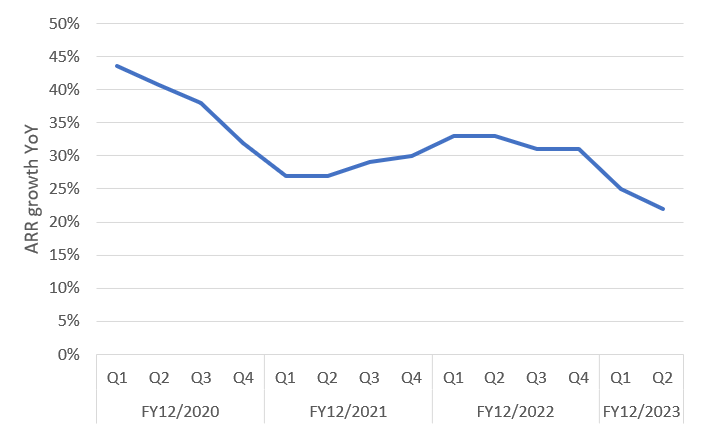

The trend in quarterly ARR growth YoY

{kind=link}

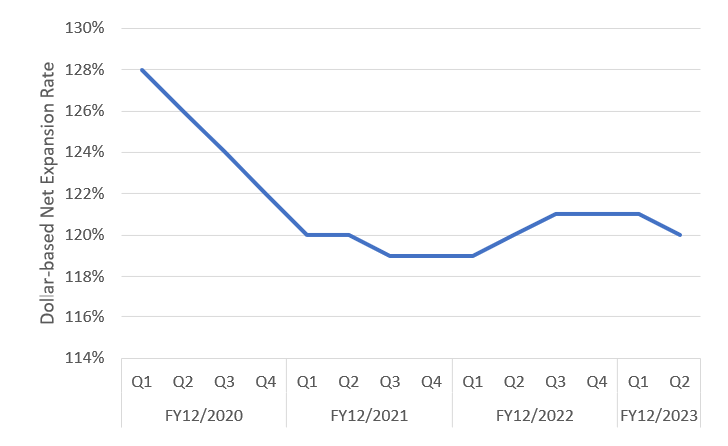

The trend in quarterly dollar-based net expansion rate

The trend in quarterly dollar-based net expansion rate (Company)

{kind=link}

Updating our view on Alteryx

We last wrote on Alteryx in April 2023 with a neutral rating, and the shares have fallen nearly 50% since that time. We want to assess whether the shares are now attractive given the correction, and any developments related to the creditworthiness of the company.

Negative read from Q2 FY12/2023 results

With Q2 FY12/2023 ARR growth at 22% YoY ( page 6 ) which was below expectations, the company appears to be experiencing a mixed customer reception at best. Although negative macro conditions have been primarily blamed for slower-than-expected customer activity into the end of the June quarter, management did highlight material weakness in the uptake of new initiatives by existing customers. Whilst this could be a temporary blip, we believe that with CIO spending priorities still firmly set on improving operational efficiencies , there is the risk that customers are moving away and not investing in the Alteryx platform as much as before. Why would this be the case? We simply view this as symptomatic of a maturing digital transformation market. Whilst there will be continued demand and progress for greater efficiencies in IT and data curation, enterprises have developed and evolved significantly over the last 4 years, and Alteryx's Designer is not necessarily a definitive go-to solution. The drop in the dollar-based net expansion rate QoQ to 120% would support this view, particularly if the downtrend was to be sustained.

The lack of management commentary over new customer wins in the earnings call (apart from ' positive early trends ' in cloud ELA) indicated to us that limited ARR growth also stemmed from new customer acquisitions. Again, this points to customers becoming more particular about their digital transformation needs, and with the huge amount of choice and sophistication available in the market, we believe Alteryx is finding it more challenging to convert new accounts.

With the company lowering FY12/2023 guidance ( page 32 ) with ARR growth now expected at 12%-13% to 22%-23% previously, this highlights expectations of a significant headwind into H2 FY12/2023. If negative factors in macro and high competition persist into FY12/2024, we see downside risk to current consensus estimates (please see Key financials table above) where sales growth re-accelerates with profitability improving YoY.

Credit risk remains high

With fundamentals currently weakening, the company is not strongly positioned to make a major improvement to its credit quality. Although it has financed to pay back USD398 million of convertible bonds in August 2023 ( page 19 ), it still needs to find another USD396 million by August 2026. With increased financing costs, we are not confident that the business will be in a position to pay back this debt within the next three years. This view is based on the company's track record over the last 3 years, where both ARR and dollar-based net expansion rates have remained on a negative trend, with no real indication of a turnaround. This scenario could also be a negative for any potential customer who would conduct due diligence on the longevity of a new technology partner.

With no assets available to dispose of in order to raise cash, and with equity financing being potentially too dilutive, we believe management is in a difficult situation to effectively remain solvent. Other options available are a capital tie-up with a business partner, or being wholly acquired in order to access liquidity - but either option hints at the company bargaining from a position of weakness, with limited upside for the equity holder.

Valuation

On current consensus estimates, the shares are trading on PER FY12/2024 26.1x on net income growth of 74% YoY. This growth recovery profile looks attractive in isolation. However, given our view that this looks too optimistic, as well as the low credit quality of the company, we believe the shares are not unduly cheap.

Risks

Upside risk could come as management has instigated cost reductions and improved sales activities to win business, which could show an improved trend in KPIs into Q3 FY12/2023. Major new customer wins could also turn the tide for the company.

The downside risk is a continuation of the trend of falling growth. Although management has talked of no sales attrition, we could see key personnel jumping ship despite a challenging job market in the tech sector.

Conclusion

The shares have corrected but we see no reason to invest, as we do not see evidence of a business turnaround. Whilst credit risk may be priced in, we believe that despite a 3-year window, the company is unlikely to generate USD400 million of cash to redeem the second tranche of convertible bonds. On balance, we rate the shares as a sell.

For further details see:

Alteryx: No Sign Of A Turnaround (Rating Downgrade)